Small Caps Live Weekly Summary

Mello SAA ADVT ZYT VANL KINO SHOE BWNG SMRT PMP TND WRKS

The first physical Mello for a while is next week and the schedule is now confirmed. Mark will be on the BASH Panel on Wednesday evening, and delivering a talk called “A Portfolio with Personality & Style” at 9am on Thursday. Make sure you catch those. If you haven’t got tickets yet then it is not too late. The code “TwitMM50” should still work for 50% off.

Leo has also previewed all of the companies presenting at Mello here.

“Large Caps” Live - M&C Saatchi (SAA.L)

In a break from tradition, WayneJ looked at a small cap this week, M&C Saatchi that is facing bid interest.

M&C is subject to a bid from AdvancedAdvT ( £ADVT). ADVT is essentially a bid vehicle created for / by Vin Murria with assistance from Marwyn Investors. Vin Murria is of course well known for creating 10 baggers at a couple of previous companies. And before we go further let me declare that I or accounts that I have influence over have positions in ADVT and SAA bought in the last couple of days.

So ADVT floated at 100 and is now trading at 83p. It has a market cap of £110.56M (as of Sunday night). But it has:

- £105.1M of cash as of the last report

- 12M shares in SAA which were bought at £2 (now worth circa 159p each so £19M)

- Given that there are 133.2M shares outstanding that computes to 93.28p per share

At the weekend the stock had closed at 83p so basically the cash covers the share price (cash = 78.9p-ish) Vin has made a bid for SAA (ie M&C) and revised it a couple of times and is in talks with the company. Everything is pretty complicated, however:

- Vin owns 12.46% of SAA (M&C) of which she is vice-chairman (this was bought significantly below the current share price) – I think the current market value is £24M

- She owns 13.14% of ADVT which is currently worth £14.5M (she paid £1 per share vs the 83p currently)

- ADVT owns 9.82% of SAA (M&C)

So on a lookthrough basis Vin owns / controls about 22.28% of SAA (M&C)

As of Friday 13th, the last offer for SAA comprised of:

OPTION 1: 1.939 shares of ADVT plus 40p per 1 share of SAA valuing each SAA share currently at 200.9p

OPTION 2: 2.347 shares of ADVT per 1 share of SAA valuing each SAA share at 194.8p

The value of the bids has changed as ADVT’s share price has moved. By my estimates, the bid values have been at 182p, 220p and 250p initially but my calcs may be wrong on that so please do your own work.

When there is a bid approach a bidder has a timeline to ‘PUT UP or SHUT UP’ known as a PUSU limit. The PUSU time limit has been extended several times and the next closing date is 5pm on 20th May 2022. I have lost count of the number of extensions of PUSU there have been but I think there is a key difference now.....

The Annual Report for 2021 for M&C came out on the 10th May 2022. So why does all the above matter?

(1) Clearly Vin has some serious skin in the game here.

(2) There have been several extensions of the PUSU

(3) The Annual Report has come out so the clock should be starting to announce an AGM

(4) Given the bid process has been going on so long I think it is reasonable to think that the bidder ie ADVT is talking to institutions about irrevocables before making a further bid.

(5) Given that Vin controls over 1/5 of the shares and not everyone turns up that is a significant number.

a. If SAA and ADVT cannot decide on a bid price that is agreeable to the board then I think at the forthcoming general meeting the board gets pushed out.

b. If ADVT walks away then I also think the board gets under significant pressure at the AGM

Hence whether by the 20th or within a few further weeks I think the board of SAA (who (except for Vin) own the square root of a pear worth of shares between them) will have to acquiesce.

Second point – usually one sets up a merger arb play by buying the target and shorting the bidder. But in this case:

(a) There is likely to be a tight borrow of ADVT given that the free float is limited

(b) There are two options and one of them (my option 1) has a further mix and match option

(c) Both companies are relatively small

(d) The bid process has been going on for a while

So I am thinking that there will not be that much arbitrage left to do and also there is a real risk for traders of being short ADVT and long SAA if Vin walks away.

Thus I have put on a long in SAA. And as a bit of a hedge I have actually gone long ADVT, as if the bid fails potentially ADVT could wind up and return its cash OR find another bid target.

This was timely and actionable since on Tuesday ADVT upped their offer. Which was rejected by the board. Then on Friday, Next Fifteen Communications stepped in with a higher offer that was accepted by the board.

WayneJ is not convinced this is a done deal though:

I note in the announcement today: “a multiple of 7.6 times M&C Saatchi's forecast headline profit before tax for the 12 months to 31 December 2023, expected to be in the region of £41.0 million.”

And yet the board was moaning of undervaluation on a previous bid which IIRC was circa 250p (the NFC bid is 247p). I think there is a comedian involved in all of this:

- SAA board complained that ADVT had only 6% or something irrevocables from independent shareholder but for the N15 bid the irrevocs are only 0.6% (only the SAA board)

- the scheme requires approval of 75% of shareholders - I think Vin is not too far away from being able to block it

I think the market is marking this as a done deal on the basis that NFC could move the conditions to 50% - I am not entirely sure of the ins and outs of that but I think that is the right assumption. What I think it goes to show is that despite my natural cynicism another bidder thinks SAA is on about 7x 2023 earnings pre-tax.

Small Caps

Zytronic (ZYT.L) - Interim Results

These are exactly as you would expect them to be from recent trading statements:

· Group revenue of £5.9m (2021: £4.8m)

· EBITDA of £0.8m (2021: £0.2m)

· Profit before tax of £0.4m (2021: loss of £0.3m)

· Basic earnings per share of 3.0p (2021: loss per share 1.2p)

· Positive cash generated from operations £0.1m (2021: £0.4m)

· Net cash of £7.5m (30 September 2021: £9.2m)

Revenue & gross margins are in line with Mark’s expectations, distribution costs slightly higher and admin costs slightly lower meaning a small beat on his PBT expectations, but at these levels the absolute values are small and the company are guiding for admin costs to increase slightly in H2 due to wage agreements.

Cash flow from operations is weak but this is due to inventory build as trading has normalised plus requirements to hold larger stocks of components. The trade payables has not increased with increased trading which suggests they are also using their balance sheet to mitigate some of the component supply challenges.

Despite these results being ahead of Mark’s expectations, the challenge is perhaps the outlook:

While the previously noted post-pandemic issues look likely to present a headwind for the remainder of the financial year, the Group remains well positioned to progress in its recovery, particularly now as the global sales and marketing activities resume and provide the basis for the generation of new future opportunities.

Mark was expecting 22H2 to be a similar 25% ahead of 21H2 on revenue. They still expect to have a H2 weighting, but an increase of this magnitude is perhaps looking less likely today. The order book is up 16% and while this is not particularly indicative, this would be Mark’s new guess for the increase for H2 over H1.

Delays due to component supply are more about customers not being able to build the final products rather than their access to components where they have upped inventory to protect themselves. The management view is that these orders are delayed not lost.

The other disappointment was this:

it will again not pay an interim dividend and will consider recommending a final dividend dependent on the full-year performance of the Group.

The market has read this as a message about H2 trading. The management confirm that their commitment is to pay a covered dividend and the smaller amount that this would represent in H1 is not worth the admin of an interim dividend. While we shouldn’t read this as negative for H2 trading, it remains uncertain, as you may expect from a business doesn't have a lot of forward order visibility.

The market reaction to these results has been quite mixed. Initially, the MM's appear to have marked the shares up at 180-195p vs 175-190p the previous day. However, it appears to have been hit by continuous small sales and now sits at 160-170p.

Longer term, the management view definitely seemed to be that pre-covid revenue and mid-30% gross margins were very possible again. For example, financial touchscreens are largely now just replacement kit for existing ATM designs and will keep declining. However, EV charging points are forecast to grow 30% CAGR to 2030 and Zytronic already provide some touchscreens to this market. So, as one end-market declines, another increases.

This is still a specialist niche manufacturer so not going to be a mega-cap but Mark doesn’t see why £3-4m pa free cash generation with a 15x FCF multiple won't be a sensible rating at some point in the next few years.

Van Elle (VANL.L) - Trading Update

This trading update has been well received:

The Board is pleased to report the elevated levels of demand in Van Elle's core markets detailed in the Interim Results in January continued through the second half of the year. Consequently, the Group now expects to report results for the Period ahead of the recently upgraded forecasts, with revenues of approximately £125m.

Stockopedia has £117m forecast so a 7% revenue beat. It is also interesting that they say:

Supply chain challenges are showing some signs of moderating, with the impact of material price inflation being managed through contract pricing mechanisms.

Perhaps a read through for other companies struggling with supply chain issues.

Even assuming an upgrade this looks expensive on near-term earnings, so those buying today are putting a lot of faith in:

The Board is therefore increasingly confident of achieving its mid-term financial targets of 7-8% operating profit and 15-20% ROCE.

They will probably get there at some point, at least on operating profit margins, but this is a cyclical, capex-heavy industry so paying up for cyclical peak earnings has never been a smart strategy. Paying up for the hope of cyclical peak earnings arriving soon, even less so!

Kinovo (KINO.L) - Update on DCB

Kinovo has today been informed that two partners of CFS Restructuring LLP have been appointed as joint administrators of DCB (the "Joint Administrators").

This is potentially good news as any risk of Kinovo being disadvantaged should now be stopped. However, the situation regarding liabilities is unclear:

We are very disappointed to be informed of the appointment by DCB of the Joint Administrators. We are actively engaged with our legal advisors in establishing Kinovo's position in consequence of an administration of DCB, and we are also in direct discussions with the Joint Administrators.

We notice that the news of the administration was posted on advfn at 14:27 but that RNS was not released until 16:33. Given the large subsequent price movement, this was clearly material news and there was a false market created. Not a good look for all involved.

Shoe Zone (SHOE.L) - Interim Results

Leo was impressed by these results in several ways. Firstly they are to 2nd April and are being issued on 17th May. Secondly, the cash flow is very impressive:

Net cash balance of £13.9m (2021 H1: £4.1m) at period end

Thirdly this has been achieved despite a clear one-off headwind:

Stock at cost is higher for the Period by £2.7m at £31.1m (2021 H1: £28.4m) due to a portion of the Autumn Winter ("AW") 2021 boots and wellington intake being delayed.

Although overall gross margins are only 20%, we would expect these lines to be at least average in terms of margin, so that's £3.2m cashflow/profit lost. And inflation should mean they are able to sell them for that this winter even though some of the boots will be ageing styles.

The fourth thing is the EPS of 5.7p on what has been traditionally been by far the weakest half. For example: 2017 H1/FY was 0.5p / 15.77p, 2018 was 1.7p / 19.03p, 2019: 1.65p / 11.43p. And today's EPS figure excludes a positive £2.6m movement in the pension schemes due to interest rate movements and despite weak equity performance to 2nd April.

So how has this been achieved? Well, the evidence is there has been a step-change in gross margin, presumably due to the larger store strategy. And we’re pleased this hasn't come at the cost of long lease commitments with the average (albeit perhaps not cost weighted) length falling from 1.9 to 1.8 years.

Zeus leave their forecast inline implying results were as expected. At first sight, these forecasts of 10.4p look around 50% too low. However, we have not run a detailed model and the share price of 149p surely already has this priced in since this, rightfully, never trades at a high multiple. Anyone buying in October at 65p certainly has the right to be very pleased with themselves, but it isn't clear how much further this can go in the short term.

N Brown Group (BWNG.L) - Final Results

After a slow start, the market really liked these results on Wednesday with the share price up 32%. Although part of this is a reversal of recent weakness.

The results themselves look in line:

Perhaps a small beat on adjusted EPS, but then it can be hard to judge whether the adjustments are the same. The reality may be that this simply got too cheap on P/E of around 4 prior to today's rise. In light of this, the following outlook makes it look very cheap on forward metrics too:

Our expectation for FY23 Adjusted EBITDA remains unchanged from our year end trading statement issued on 3 March 2022. This reflected Adjusted EBITDA at a level similar to that reported in FY21 before growing again as the Group's strategy is executed.

Net assets increased again, although some of this was a pension surplus that there will be some doubt over their ability to access in full, or at all. Even after this week’s rise, the shares trade at around half TBV, which for a profitable business is unusual. They also don't seem to be facing issues with obsolete or excessive inventory build that other retailers that trade at a discount to TBV have either.

There are two potential downsides. The first is that this is a credit business and we are potentially entering a time where credit risk may increase significantly. You've got to assume the way they calculate the bad debt provision is to take the current overdue balance and impair it by some conservative historical numbers on the recovery they get. However, this means that it is largely a backwards-looking number.

Those buying on credit here are not necessarily a worse credit risk than the general population - they tend to be sites for niche sizing and they push you to take credit even if you pay it off in full the following month, much like Next or others do. But it would be daft to assume that bad debt isn't going to increase significantly given the energy price rises and the number of people now reliant on food banks.

The second is the litigation with Allianz. Today they say:

The Group is involved in a legal dispute with Allianz. More details of the Allianz claim and the JDW counterclaims and defence are set out in note 6. The eventual financial outcome of the dispute is highly uncertain for both parties. We believe that it remains in the best interest for the parties to settle the dispute and an accounting provision of £28m has been made to cover settlement, or award at trial, plus future legal costs.

If this is a good estimate of the eventual cost to the company then this is good news since this amount will be easily met through existing facilities. However, they do say:

Given the nature of the issues in dispute, the Court will have considerable discretion in reaching its conclusions relating to, amongst other things, which sums should be brought into account and what proportions of the liabilities each party should have to bear. Accordingly, the range of potential outcomes, in either direction, could be many times materiality and involves a significant level of estimation.

This does look good value though for those willing to bear the consumer credit and litigation risk.

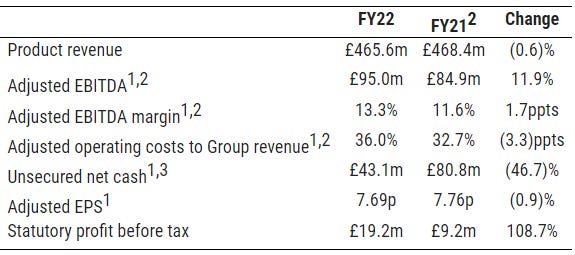

SmartSpace Software (SMRT.L) - Preliminary Results

The first thing to note here is that what they released on Tuesday were unaudited results and therefore contained no going concern statement. Issuing preliminary unaudited results with the audit in a later annual report used to be standard practice, but it is becoming increasingly unusual now. Indeed, SmartSpace themselves were expecting to have final results on Tuesday, since on 9th May they said:

SmartSpace Software Plc, (AIM:SMRT) the leading provider of 'Integrated Space Management Software' for smart buildings and commercial spaces - 'visitor reception, desks and meeting rooms', announces that it will issue its Final Results for the twelve months ended 31 January 2022, on Tuesday 17 May 2022.

Last year, they issued Final Results a week earlier.

The annual report was published the next day, where the going concern statement said:

As the Group’s software businesses build their SaaS customer bases the Group continues to be loss making. The losses incurred are controlled, predictable and planned to allow the business to continue to grow. In the short term the Group will continue to be lossmaking. As reported in the Strategic Report, SwipedOn has continued to grow despite the worldwide disruption caused by Covid-19 and is now consistently generating cash. Space Connect has made significant growth to its customer base and recurring revenues but is not yet cash generative. The Audit Committee has considered the Group forecasts which underpin the presumption that the accounts should be prepared under the going concern principle. In particular it has considered a scenario whereby the SaaS business does not exceed its historic growth rates in the next twelve months together with the mitigations available to the Group. On this basis, the Audit Committee was able to advise the Board that it was reasonable to prepare the accounts on a going concern basis.

Not exceeding historic growth rates doesn't seem like a cautious downside scenario.

It also appears the auditors were not initially happy with the goodwill assessment and they:

Challenged management to consider the outcome if the perpetuity were removed, and the product’s life were limited to 10 years.

As a result of performing the procedures above management revised their model. Clearly, perpetuity was a crazy assumption. It is a red flag that management tried to get away with that.

On impairment testing, they say a fluctuation of more than 2.5% in the discount rate would result in further impairment(s). However, growth rate assumptions as I understand them are low. Happy enough there.

In summary, the main issue appears to be the implication that if growth does not accelerate then they will need to cut costs. But we knew that already.

So, blank sheet, what is this company worth?

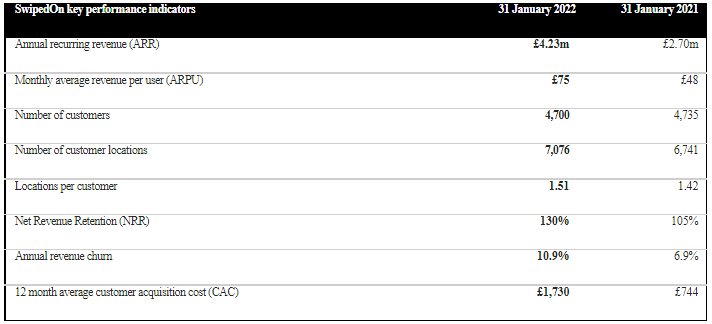

First the trend in locations for SwipedOn:

The actual number of customers has fallen for the first time too:

Although they seem to be driving more revenue from existing customers. This is only about ARPLocation growth. The closest approximation to that we have is ARPU. This shows that number of users per location is falling:

SwipedOn ARPU £85 (NZ$165) at 30 April 2022 up 58% year-on-year

SwipedOn ARR £4.79m (NZ$9.33m) at 30 April 2022 up 56% year on year, restated to the prevailing exchange rate at 30 April 2022

GBP NZD is pretty flat over the period. Total users are probably rising, but users per location pretty much must be falling. So, how long can ARPU keep growing? To be conservative, let's say another 20% before it hits a wall. Probably generously, lets say they manage to stabilise users indefinitely.

So we have a group ARR of £5.5m + 20% = £6.6m. Gross margins are about 70%. Admin expenses were £7.3m, but assume that this is taken into a larger group. Assume maintenance capex and marketing is 20% of revenues. This comes out as £1.3m which seems too low, so call it £2.0m. Cashflow of £2.6m before tax. So the company might be worth 5x that = £13m. The current market cap is around £19m. So from that perspective it there isn't much room to fall, but that assumes a takeover.

OK, what about trying to continue as a stand-alone business?

They are hoping to be cash flow positive by the end of the year:

Cash and cash equivalents decreased during the year by £1.76m (2021: increase £1.93m) due to a cash outflow from operating activities of £1.61m (2021: £1.44m). As we move into FY23 cash consumption is at lower levels than at the beginning of FY22 and further growth in recurring revenues for SwipedOn and Space Connect, combined with a return to profitability for A&K, is expected to transition the business to being cashflow positive by the end of the financial year.

But £2.758m cash looks tight if they face any delays in this. They have £0.6m inventories & receivables but owe £3.2m payables & contract liabilities. So even if you don't assume they have window dressed their Y/E position then any slow down would see significant cash outflows.

Realistically they need to raise £3m or so to comfortably see out the year. That would not be a major dilution at current levels. But what would it be worth then?

They probably think ARR will increase another 50% to £8.25m. Gross profit of £5.8m. So cash ongoing admin costs of £6.2m would need to be cut by £0.4m without incurring any exceptionals. That is possible and then would make them marginally profitable going forward.

So in summary: We don't think this is a zero, but the longer they leave the fundraise the less it will be worth.

There are many loss-making SaaS companies whose accounts look like SmartSpace right now. In the past, I think investors just didn't worry about profitability because they knew that at a certain size somebody would come along and pay 10xARR, and whether that person was a greater fool or not didn't matter. But that game is over now.

Portmerion (PMP.L) - AGM Trading Statement

We are pleased to report that sales for the first four months of 2022 are up 2% on the same period last year.

This doesn't seem much to be pleased about. Inflation was about 5% in that period. Yes, I know they have their energy costs fixed, but they should at least be keeping the prices of their non-essentials up with inflation. It is also significantly below the growth rate Leo had pencilled in for H1.

Gross margins have increased by 50 basis points, demonstrating the strength of our brands in passing on cost increases through in price rises.

Gross margins are a very strange thing to quote for a company that doesn't separate out cost of sales or include gross profits in its accounts. The closest they have is "cost of inventories recognised as an expense". This isn't even given in the interim results, but at the FY 2021 inventory gross margin was 55%. Perhaps they are trying to indicate adjusted operating margin is likely to also be 0.5% higher but don't have all of the non-cash costs worked out yet. H1 net margins tend to be weak, but if it continues for the whole year it is material on the 7.2% achieved in FY 2021.

There has been a significant change to consumer sentiment and spending since last year as consumers deal with the impact of inflation in food staples, energy and fuel prices. In addition, there has been further Covid related disruption in supply chains and sales markets, including China. So far we have successfully mitigated these challenges by forward-ordering stock and having long term energy contracts in place until March 2024.

No indication of them signing new energy contacts yet.

order books for both our key Christmas trading period and our wider international markets remain healthy.

FY expectations were for a 3.8% increase in revenue over the full year. Accordingly, they are in line for a miss now. But, as they say:

with a traditional heavy second half sales weighting, we remain cautious and watchful as to how macro conditions develop as the year progresses.

No broker updates we’ve seen, however, it is not surprising the market has reacted negatively to this update.

Tandem (TND.L) - Directorate Change

Surprisingly, a non-exec takes the CEO reigns at Tandem. He seems well experienced:

Peter Kimberley was appointed as a non-executive director of the Company in November 2021 and has more than 30 years retail experience across a number of sectors including the cycle retail sector with specific experience in e-mobility across omnichannel, B2B and B2C offerings - most recently as Chief Executive Officer of Pure Electric Limited, a specialised omnichannel retailer of e-bikes and e-scooters in the UK and Europe.

Peter was previously Managing Director of Cycle Republic (omnichannel), Tredz (online proposition) and Boardman Bikes (brand and design) within Halfords Group PLC between 2013 and 2020.

However, we are always wary when non-execs become execs. They usually become non-execs for an easier life and stepping back into exec roles doesn’t always come easy. The last non-exec to permanent CEO change we can recall is Tekmar and so far the CEO there hasn’t delivered any step-change in performance or overcome the issues that occurred under the previous management.

The Works (WRKS.L) - Full Year Trading Update

...trading update for the 52 weeks ended 1 May 2022 (the "Period" or "FY22").

Highlights

· Strong trading performance; two-year LFL(1) sales increase of 10.4% and total two-year sales growth of 12.7%(1),(2).

· Improved proposition helping to offset external headwinds; FY22 EBITDA forecast of £15.0m is reiterated.

· Strong financial position: net cash(3) of £16.3m at the Period end, an increase of £15.5m during FY22.

· Dividend re-instated; the Board expects to recommend a dividend of approximately 2.4 pence per share alongside its FY22 results in September and maintain a progressive dividend policy thereafter.

The company seems to have achieved this by hitting a recent sweet spot in terms of popular trends:

Sales since our last update in January 2022 have been driven by the further development of our customer proposition, in particular the expansion of our front list book ranges, which has coincided with the emergence of the "BookTok" phenomenon. By capitalising on this trend, we have been able to draw attention to previously best-selling books and prompt renewed customer interest in them. Branded toys and games have also continued to perform strongly, through reinforcements to our ranges of, for example, Peppa Pig, Paw Patrol and Cocomelon.

BookTok for those who don’t know:

BookTok is a subcommunity on the app TikTok, focused on books and literature. Creators make videos reviewing, discussing, and joking about the books they read. These books range in genre, but many creators tend to focus on young adult fiction, young adult fantasy, and romance novels.

The market liked this update with the shares up over 10%, although this simply reverses the decline over the last couple of weeks as the market feared that these sorts of companies would start to miss forecasts due to inflation feeding through to poor customer spending. On the outlook they say:

There continues to be uncertainty relating to the external environment and how this might affect levels of consumer spending in the months ahead. This has been taken into account in setting the Group's internal plans for FY23.

This, presumably, is why Stockopedia has forecast EPS to fall slightly again in 2023.

The headline figures of 5-6x P/E look good, particularly with net cash. However, that net cash figure may be a little misleading. They tend to run with negative working capital. At the half-year this was around -£20m which was larger than the cash balance at the time. For the FY they say:

The Group ended the Period in a strong financial position, with net cash(3) of £16.3m (FY21: £0.8m). This is higher than the £10.0m level noted in the FY22 Interim results statement, due to the unwinding of certain working capital timing differences taking longer than anticipated.

Adjusting for this negative working capital we get a 2023 adjusted earnings yield of around 11% for the company. This is cheap but not outstandingly so since this is in line with other retailers or suppliers such as Supreme, Character or Sanderson Design currently trade on

The 2.4p proposed dividend is significantly higher than market expectations and certainly backs up their positive messaging, but at 4.2% yield, again, this isn't a standout for the sector.

As part of a basket of relatively good value stocks, in order to gain exposure to UK physical retail, then owning The Works makes sense. However, the metrics don't look any better than other similar companies in the current market.

That’s it for this week, see you all at Mello.