Small Caps Live Weekly Summary

CLX IQE RBG HOST RTN AFRN SOM WAND Car Dealer Live

A quiet week this week for news, if not share price moves, not least because Mark was on holiday and Leo was visiting Car Dealer Live as part of his scuttlebutt on motor dealers. For those into on-the-ground research, it’s not too late to get your tickets to the UK Concrete Show next week!

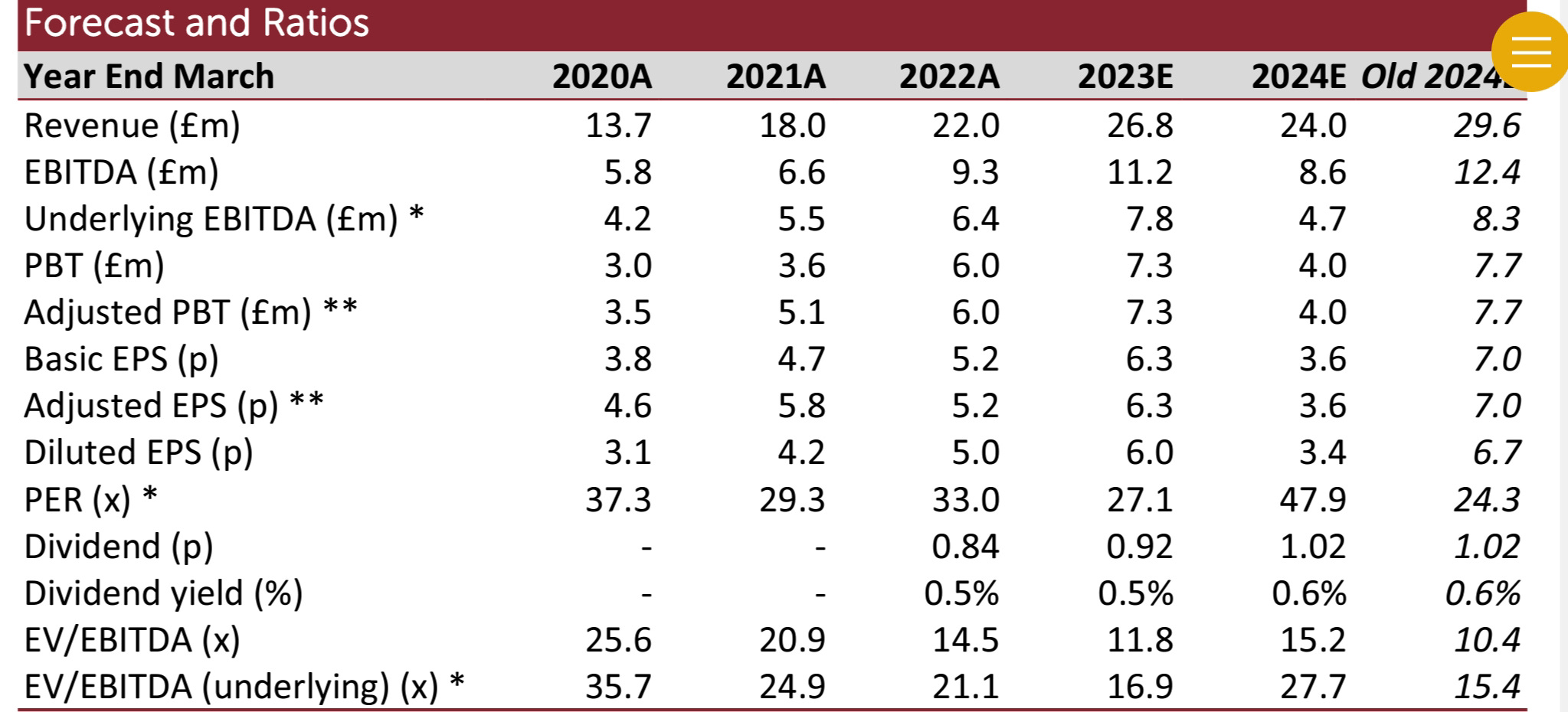

Calnex (CLX.L) - Trading Update

Calnex report that they expect to be in line with expectations for FY 23, ending March 31st. However:

Based on short-term order run-rates, the Board believes that the financial performance in FY24 will be below that achieved in FY23, with the Company's revenues more heavily weighted to H2 of FY24.

Unfortunately, this is very highly rated:

So revenue dropping for a growth stock is not going to be well received. Cenkos have a 48% downgrade on 2024 PBT:

Meaning that the company was trading on a forward P/E of 50 prior to any fall on the day. We commented that the early reaction of only a 20% drop looked light. And indeed, the price kept falling and ended up down 32%. Big drops in high-quality companies can provide opportunities for the contrarian investor. However, in this case, you have to consider that EPS estimates have fallen, plus the company should de-rate to reflect poorer growth prospects. If we apply a fairly generous 15x multiple then we still only get a c50p valuation, so this looks like it has a lot further to fall to reflect the new reality.

IQE (IQE.L) - Trading Update

IQE appear to be making the wrong stuff as they face an inventory build:

Management's expectations for FY22 results remain in line with the update provided on 16 January 2023. Since that update, the Group has seen an acceleration of the trends anticipated, with weaker demand leading to inventory build-up throughout the supply chain.

But they do have plans to make the right stuff:

IQE continues to make positive progress towards the Group's strategy as set out at the November 2022 Capital Markets Day, diversifying into high-growth markets including Power Electronics and MicroLED.

Power Electronics is still an evolving area as small incremental improvements in efficiency, e.g. from 95% to 96%, result in significant reductions in power dissipation and, therefore, weight. More exotic semiconductor materials and finer controlled processes have a big part to play in this. Despite many companies reporting shortages of semiconductors, the market as a whole is falling, with worldwide chip sales down 18.5% year-to-year.

Global semiconductor industry sales totaled USD 41.3 billion during the month of January 2023, a decrease of 5.2% compared to the December 2022 total of $43.6 billion and 18.5% less than the January 2022 total of USD 50.7 billion, report SIA.

Note, however, this is by value. Leading the fall is likely to be reductions in the price of flash and dynamic memory. But in the area of microprocessors using older processes, there is a structural issue in that there is not enough expected lifetime demand to justify switching factories over. As I've said several times, users of these parts need to pull their finger out and update their designs. It is no surprise that auto OEMS with complex supply chains had the most difficulty here.

However, this is nonsense:

This near-term market softness is expected to be temporary and a return to year-on-year growth is anticipated in H2 2023 based on dialogue with our existing customers and our pipeline of new opportunities.

IQE is not a growth company, with a revenue CAGR of just 3%.

Nor is it likely to be anytime soon. Making the current market cap appear absurd, even after a 36% fall in response to this week’s trading update.

Revolution Bars (RBG.L) - Interim Results

There was some controversy about the Peach Pub acquisition here. The two schools of thought are a) they needed to water down (diversify, if you prefer) the poor core business, and b) it was a reckless expenditure. So Leo’s eyes were drawn to this:

As reported in the Group Annual Report and Accounts 2022, the constantly changing economic environment, including the cost-of-living crisis, increasing costs, and impacts on guest confidence, as well as ongoing risk of COVID-19, indicates the existence of a material uncertainty which may cast significant doubt over the ability of the Group and Company to continue as a going concern. Although the Group is hopeful of the continued normality in trading, it is not clear what level of trade may be possible should the UK Government impose restrictions again.

It is not currently expected that COVID-19 would result in further significant impacts on trading, but it remains a key area of review.

Splurging on an acquisition and then immediately declaring a material uncertainty over going concern is not a good look, but perhaps six months back, they genuinely believed COVID was a wildcard. This surely cannot be the case now. I think they are simply using it as an excuse and hoping investors will discount the going concern statement because they don't think covid will come back and missing the fact that it is just one of many factors, including "cost-of-living crisis, increasing costs, and impacts on guest confidence".

So, how is the balance sheet?

So, no improvement from year-end and worse YoY. Most of the damage is from impaired leases to the tune of £42m, but there is also the debt of £23m, plus heavily negative working capital. The current ratio is 0.44. Plus, on the asset side, they have £12m of goodwill from the recent acquisition. So on a balance sheet basis, the company is worthless by a massive margin. Investors must hope the lease values will come back, they have generated some goodwill not on the balance sheet, and perhaps the debt is on non-commercial terms.

Regarding liquidity, they have £6.9m headroom on debt facilities, but the facility size is due to shrink by £1m at the end of June this year and then by another £2m the following June. Adjusting out the acquisition of Peach, cashflows were negative £5.1m in the six months. £4.6m of this was the purchase of PP&E. With the refurbishment programme now on hold, perhaps this can be cut to £2m every six months? It was £2.4m for calendar 2021 H2 during covid on a smaller group, so that could be a stretch. So £2.5m burn every six months gives them until this time next year before they run out of cash.

Finally, and least importantly, profitability. There is no accounting profit, but they have given us an IAS17 adjusted EBITDA figure of £5.1m. So if they stopped all capex and ran it for cash, they could probably do that for a year of that before customers started shifting elsewhere, with progressively lower operating profits over the next five years before they got shut down for public safety reasons. Over that period, they might earn 3x annual EBITDA, so maybe £5.1m x 2 x 3 = £30.6m. The best case would be extracting half of that in dividends before they go under, giving a valuation of £15m before any NPV adjustment. Unfortunately, the balance sheet shows large accumulated losses, so they'd have to go to court to pay a dividend. These figures don’t include full trading for Peach Pubs, so may be slightly better, but how much better remains to be seen.

So, has something fundamentally changed in the outlook?

We are pleased to have navigated January through active cost management to start the second half of the year.

We also remain hopeful of continued positive news including improving energy prices and a stronger economy, which are expected to improve guest confidence in the coming months.

There's always hope.

As we enter spring with improved weather, the Group is excited to see the benefits of the outstanding outdoors spaces at Peach Pubs to capitalise on trade typically missed with our original brands.

The word "excited" has long proven its worth as a red flag for investors.

The Board expects, assuming industrial action subsides, and energy prices hold at current levels, that the Group will deliver adjusted EBITDA (on an IAS 17 basis) in line with current market expectations.

Their broker finnCap, says:

At yesterday's close it was valued at 10.5x EV/EBITDA (IFRS 16)...for FY23.

As this doesn't include rents, that appears utterly insane. Perhaps the only bull case is that something like Fuller Smith & Turner is on 1.9x EV/Sales, and applying the same to Revolution would be a 5-bagger. FS&T looks a world away in terms of margins and execution.

Hostmore (HOST.L) - Revised Results Publication Date & Trading Update

We imagine they are trading really well and have brought the results date forward?

Hostmore plc (the "Company" and together with its subsidiaries the "Group") indicated in an announcement on 10 January 2023 that its Preliminary Results for the 52 weeks ended 1 January 2023 would be published on 16 March 2023. The Group is currently in discussions with its lending banks to amend its existing facilities.

Oh, dear! And an interesting paragraph construction. Shouldn't there be some kind of connective for the last sentence, like a "However, "? As it is, the presentation makes it sound like an aside, and the juxtaposition with the previously announced results date suggests it is something they've told us about before. Anyway, we’re sure companies are having discussions with their banks all the time, and this is absolutely nothing to worry about?

This process is progressing well and the Company now expects it to conclude in the first half of April.

That's good, sounds like this almost certainly previously announced discussions might complete earlier than expected. But hold on, isn't that going to make results by 16th March difficult?

A further announcement confirming the new date of the Preliminary Results will be made in due course whilst an update on the Group's amended banking facilities will also be provided as part of the Preliminary Results announcement.

Being serious for a moment, there now has to be a good chance they will never again issue results as a listed company.

The above matter is unrelated to recent trading, with the Company generating VAT adjusted revenues (note 1) for the first nine weeks of the 2023 fiscal year that are similar to 2022's comparable revenues.

That's slightly worse than Restaurant Group’s equivalent business (see below.)

Restaurant Group (RTN.L) - Full Year Results

This is another company that had a fundamentally poor business and tried to climb its way out of a hole by buying a better one. This is rarely a good way to add value because shitcos usually have a higher cost of capital than viablecos. It is more conventional for the viableco to buy the shitco either from administrators or using overpriced equity and then try to de-shitify it using their superior management.

Wagamama is the (at least previously) successful restaurant chain they bought, Pubs are mostly/all branded "Brunning & Price", Leisure are "captive market" restaurants like Frankie & Benny's and Chiquitos that no soulless out-of-town leisure site would be without. They obfuscate the relative importance of each by fail to provide segmental reporting.

Broadly flat for the 8 weeks to 26th February is pretty good. Unfortunately that was two weeks ago. They reiterate their plans for Leisure:

Proactive estate management and further rationalisation plan to enhance future cash generation

Or to put it another way "closing these abominations down as quickly as the leases will allow".

Aferian (AFRN.L) - Trading Update, FY22 Results Delay & Board Update

When we last looked at this we said:

Perhaps the only bright spot is that H2 was actually better than H1 at an operating profit level, just much below expectations. The share price would need to more than halve today to get anywhere near a reasonable valuation though.

This week, we get the 2nd Profits Warning here. Their problems are continuing into FY23:

Whilst it is early in the new financial year, in light of the above performance from the Amino division, the Board now expects Group revenue and adjusted EBITDA for the year ending 30 November 2023 to be substantially below its original expectations.

We’d noticed the SP had been weak recently, so not only is “substantially below” bad but it has clearly leaked to the market. Or perhaps the developers who have been selected to “deliver efficiencies in the Group's cost base” by being fired have got the message out.

Notwithstanding the difficult trading conditions of the Amino business in the first half of the year, the Company is still expected to generate a positive material adjusted EBITDA for the full year.

We’ve no idea what positive material adjusted means. It could be an attempt to say not negligible, but could also indicate it needs massive adjustments to be positive!

The Company is in compliance with its banking covenants and is in discussions with its banks to ensure future covenant compliance. This will delay the announcement of the full year audited results for the year ended 30 November 2022. A further announcement will be made as and when practicable.

So looks like they need covenant waivers to ensure future compliance. That EBITDA can’t be that “material” then! And the results delay to make sure the accounts can be presented on a going concern basis.

We’d assumed the board update would be a CFO falling on a sword, but in this case it is someone from 26% holder Kestrel Partners coming on the board to try to salvage something from their investment. They are going to need a strong lager to fortify them for the work required!

With the share price down 47% in response to this news we’ve got our halving. Unfortunately, trading has declined even further. With a weak balance sheet and no tangible asset backing its hard to make a case that this is worth investigating further.

Somero Enterprises (SOM.L) - Final Results

Somero have declared a 18.0 US cents per share final 2022 ordinary dividend and a 7.7 US cents per share supplemental dividend. Added to the 10c interim that totals 35.7c versus prior finnCap guidance of 37.5c. The ordinary dividends are calculated as 50% of adjusted net income, given as 55c / share for the full year, down 10% you. Regarding the supplemental:

after reviewing anticipated future cash requirements for the business, the Board has also declared a supplemental dividend of US$ 0.077 per share, calculated as a 50% distribution of December 31, 2022 cash that exceeds the Board approved year-end US$ 25.0m minimum cash reserve.

Compared to finnCaps's already lowered January expectations, we have:

Revenue missed: $133.6m vs $134.0m

Profits (net income) hit.

Adjusted EPS missed: 55c vs 60c.

Cash missed: $33.7m vs $34.0m

There's an updated note from finnCap:

We clip FY23 revenue by 1.4% to $133.1m with EBITDA maintained at $42.8m but adj PBT declining by $2.0m to $39.3m and adj EPS down 4.8% to 53.2ȼ. Unchanged net cash of $31.0m and dividend of 31ȼ, down 12%.

There’s quite a reduction in units sold too:

Meaning they've managed to increase prices but at the expense of volume. Their key market of US Boomed Screeds appears to have now peaked. There is some evidence that that non-US markets are undeveloped and there are clear advantages to using Somero machinery, labour issues as well as flatness.

The board think there is still growth to go for:

The Board expects the Company to deliver strong revenues, profits, and cash flows to shareholders in 2023. While the risk of supply chain delays and concrete shortages in North America may persist, the healthy and active non-residential construction markets in the US, Europe and Australia form the foundation of the Company's 2023 expectations. With all factors considered, 2023 revenues are expected to be comparable with 2022, and with targeted added resources 2023 EBITDA is expected to be down modestly from 2022, and with 2023 working capital investment expected to remain elevated, year-end 2023 cash is expected to be at a comparable level to year-end 2022.

The bull case is that these results reflect their investment for growth. The bear is that they are merely putting a sticking plaster on cost rises. In general, investors are much less forgiving of a profitable company choosing to reinvest for growth compared to one that has never made a profit, despite the former having a better track record of being able to do it. And investors love a company that grows by acquisitions since the cost don’t go through the income statement.

The big problem Somero has had in the past is a lack of reinvestment opportunities to compound growth, hence the large dividend. If that has changed, then that is positive, despite slightly disappointing results for the last year. Given previous execution, management probably deserves the benefit of the doubt on this one.

WANdisco (WAND.L) - Trading Revision

We didn’t follow this one closely since the odds of investing in a £900m market cap on 112xSales never favours the long side. Kudos to those who spotted issues with revenue recognition here, since this week they say:

Following investigations undertaken by the CFO and CEO, and as reported to the Board of Directors of the Company (the "Board"), significant, sophisticated and potentially fraudulent irregularities with regard to received purchase orders and related revenue and bookings, as represented by one senior sales employee, have been discovered. These irregularities give rise to a potential material mis-statement of the Company's financial position.

This is pretty shocking:

The identification of these irregularities will significantly impact the Company's cash position and lead to a material uncertainty regarding its overall financial position and significant going concern issues. The Board now expects that anticipated FY22 revenue could be as low as USD 9 million and not USD 24 million as previously reported. In addition, the Company has no confidence in its announced FY22 bookings expectations.

The company is understandably suspended from trading. The odds perhaps favour it never coming back from this, giving shareholders a total loss. As Warren Buffett says:

Only when the tide goes out do you discover who's been swimming naked.

Car Dealer Live

Leo attended this mainly industry event and spoke to lots of interesting people with varying views and standpoints. Here is his report:

First up was Mark Lavery, who remains CEO of Cambria after taking it private in 2021. He did not enjoy life as a public smallcap CEO, saying that small investors were "sucking the energy" out of him. Of course, that meant I had to introduce myself to him afterwards. A nugget on the buyout: Family owned 40% already, and it was easy to get a majority, but some of the overseas investors were not happy with the price, and it was a struggle to get the last few per cent to reach the 75% required. But as I said to him, if they thought it was undervalued at a 60% premium, then maybe they should have been more supportive earlier.

I mention this as read-across for potential future M&A in the sector. Clearly, a large single holder makes things much easier, as it did for Marshalls. Vertu does not have this. Slido was used for audience interaction, and given Mark has said he doesn't expect any publicly listed franchise dealers to remain by the end of the year, the vote was on who will be bought next. 38% said Vertu, 33% Pendragon, and 29% Lookers.

This reflects the massive difference between what these shares are trading at and recent acquisition valuations. This being Car Dealer Live, you might expect the audience to be full of car dealers who would think that the high private group valuations are fair and the low public group valuations are unfair. However, I spoke to many people there, and they were all suppliers except BCA (owned by Constellation), who are not quite car dealers either. James of Car Dealer later told me he thought 2/3rds of the audience were car dealers, but given the price was far higher for suppliers, I don't think his data was completely reliable. I certainly wasn't the only one on a dealer ticket who wasn't a dealer.

There was then various discussion about the size of distribution franchise dealership groups going forward. On the agency model, Mark's view was that ultimately the customer will decide, and they are not asking for it. He repeatedly declared himself as "curious" about the whole thing, something that was subsequently picked out by Polestar UK's CEO as not being ideal from an OEM's perspective. Mark doesn't see 100% online sales ever exceeding 50% of the market. We learned from google later that when you see surveys saying 22% of people bought online, that includes many who actually visited a dealership etc.

There was some discussion about the loss of market share Mercedes has apparently seen since they switched to an agency model, and later I was told of terrible reviews from customers being ignored in Mercedes dealerships because staff couldn't be bothered.

Mark sees Chinese brands as the biggest seismic shift since the Japanese and then the Koreans. Later the MG commercial director said they are committed to the traditional dealership model and expect to open many more and increase the range of their offering in the near future. There seemed to be a consensus generally that although the degree of the shift was difficult to predict, connected car would drive a closer relationship between the OEM and consumer. Brief mention of the block exemption (to competition rules), which is always a tail risk.

Acknowledges that the market will move to back to the normal "push" model of sales where OEMs are pushing through the cars, dealers are preregistering, cashing volume bonuses etc. Elsewhere we heard that this is problematic for the agency model.

Here and elsewhere, there was much gloating about Cazoo's problems, although, of course, these are much more visible than whatever (TF) is going on behind the scenes at Cinch because Cazoo has a share price.

Here are the EV numbers from the Autotrader presentation:

YoY supply of EV: +261%

YoY demand for EV: +48%

The facts are that the main OEMs have stopped developing new ICE cars because of the Europe-wide 2030/35 ban. They have also moved away from traditional volume models, the most obvious example being that Ford has cancelled the Fiesta and Focus from 2025. Autotrader forecast that the 0-5-year-old ICE vehicle parc will never recover from the 2023 levels, down 34% on 2019. e.g. total -42% for 2025 and -49% for 2027.

The poll on whether the government ban of 2030/35 would be achievable was 66% against it, but with 7-year development cycles, unless the taper on OEM CO2 emission mix is relaxed this year, then there will be very few ICE cars to buy. Those that are available and attractive will likely demand an equal or premium price to EVs for those with no access to overnight charging. Oh, and extending the life of ICE models will become increasingly difficult as the already long-obsolete microchips they rely on become even harder to find. In contrast, the amount of EV supply coming online from all sides is massive. So I could see a situation where a quality light hybrid or low-capacity plug-in bought now could suffer unprecedentedly low depreciation over the next ten years, whereas new EV prices will be falling each and every year by double-digit percentages.

On various panels, various used car dealers said they would not touch EVs / take them as PX except at far below-normal valuations. There was some crazy figure of 1 in 4 who said they would never stock an EV. Those Tesla price cuts (which are ongoing) have really hit confidence. Even the Autotrader person, who, of course, urged dealers to look at their data to make a decision, said it "might be rational" to not stock used EVs for 1-2 years. And, to point out the obvious, buying an electric car without access to overnight charging is actively harmful to the wider environment to run (that is, ignoring up-front material costs) because it consumes more fossil fuels per mile than a modern mild hybrid petrol. So even if you didn't care about losing tens of thousands of pounds, there are large numbers of people where it makes no possible sense. While on the topic, Tesla has actually done well out of the publicity around the price cuts, with enquiries up 50% and remaining stable (Autotrader), whereas total EV queries (google) fell in Q1.

That’s it for this week, have great weekend!