Small Caps Live Weekly Summary

CAPD COM KETL TND XAR

It seems some readers may disagree with the summaries of the company news we cover here. Great! We absolutely want to be challenged on these views. And given that these summaries are usually edited out of a back-and-forth discussion on Discord, many of us may disagree, too. The whole point of these weekly posts on Substack is to encourage knowledgeable investors to join in the conversation. However, the place to do this isn’t the comment section of these posts since they are unlikely to be read or responded to. The place to debate, agree, disagree, or add detail is on our discord channel. That way, readers will get the full context of the discussion, plus be part of an ongoing community of serious investors aiming to gain an informational or analytical edge on the UK small cap market. It is structured by thread, with each company having its own place for discussion under either a smallcap, midcap, or largecap channel. A bot posts all regulatory news and any interesting articles or broker research into the threads automatically. For those getting started, the discord search function will allow you to find the companies you are interested in. The bot for each channel will give a regular summary of the ongoing popular discussions.

Capital Limited (CAPD.L) - Contract Win

One of the concerns many investors have with Capital is that the vast majority of their assets and revenue comes from operating in one of the more unstable parts of the world, Africa. Since they have been growing their labs business, the company has said that this opens up contacts and opportunities outside of this region. This week, we see the fruits of this:

A three-year comprehensive drilling services contract with Nevada Gold Mines LLC ("NGM") in the United States of America ("USA"): The contract spans a wide range of drilling services including diamond, both surface and underground, and underground reverse circulation. Drilling spans a number of operations across NGM including:

o Underground diamond drilling in the Leeville underground mine within the Carlin complex

o Underground reverse circulation drilling in Carlin

o Diamond drilling at the Robertson project within the Cortez complex

NGM is a JV majority owned by Barrick, so presumably, this win comes out of their strong relationship with Barrick through drilling operations at their African mines. Of course, this is not the sort of contract where you redeploy used equipment, even if it were practical to transport it, so:

Capital will purchase new rigs with associated equipment for the contract with capex expected to be ~$20 million, predominantly falling in 2024.

The stock market has been pretty consistent in demanding a high equity risk premium for Capital as an Africa-focused company, but they would like us have believe there is no such premium in contract pricing:

The contract is expected to generate annualised run rate revenues of ~$35 million once all the rigs are fully operational from 2025, at margins commensurate with the broader group.

We are pretty sure the company will be referring to EBITDA margins, as they normally use this metric. They target at around 25%. The labs business will likely do at least this when not growing. But the rest of the business currently has EBITDA margins of 30%, and they are clear that this is unsustainable in the long run, and we should be thinking 25%. So, this is what we would assume they are targeting for Nevada, adding around $8.75m incremental EBITDA from 2025.

This contract is for 9 rigs, but we also get the following details about NGM:

…consisting of 10 underground mines, 12 open pit mines and associated facilities.

So, a land and expand strategy like they have done successfully on a number of other mines is very possible. The current limit to the scope of the contract is probably due to the level of risk both companies are willing to take.

The market is largely unmoved by this development, perhaps because it reinforces the other concern many other market participants have, which is that the company is increasing debt to invest in future growth:

Capital will purchase new rigs with associated equipment for the contract with capex expected to be ~$20 million, predominantly falling in 2024.

However, $8.75m annual EBITDA for $20m capex is a decent return. Assuming 10 years for rig depreciation and 10% interest on the debt, they are likely generating a 24% pre-tax return on this investment. In line with their current 23% ROCE. In any other business, investors would be screaming for the company to take on more debt at 10% to fund investments generating these sorts of long-term returns.

Comptoir (COM.L) - Interim Results

Mark thought this was an interesting opportunity when the company did 0.77p EPS in H1 2022, versus a share price at the time of around 5p. However, he quickly lost faith when the 2022 full-year results showed just 0.48p EPS, meaning H2 2022 was loss-making.

This trend has continued with -0.66p EPS in these results. As the company says:

The Group controls remained strong, but profit declined due to the aforementioned impact of VAT and Business Rates returning to previous levels, as well as the utility, food and wage inflation.

These are incredibly tough times for anyone in the casual dining sector.

One of the attractions was a cash balance in excess of the market cap at the time. However, this keeps declining:

Net cash and cash equivalents at the period end of £5.7m ((H1 2022: £8.2m; 1 January 2023: £7.7m)

This is still a significant proportion of the £8.2m market cap. However, this is due to a large negative working capital position. The presence of £1.9m of debt on the balance sheet suggests that this amount varies significantly during the year. Combined with lease liabilities significantly exceeding lease assets, net tangible asset value is around £3.75m, or about 3p per share.

Mark is unlikely to be tempted back in here unless the outlook for casual dining improves significantly, or they trade at a big discount to the NTAV figure.

Strix (KETL.L) - Interim Results

These results get progressively worse as you head down the income statement:

Given a 2-yr chart that looks like this, one could be forgiven for thinking that this was in the price:

However, the market reaction on the day was for the shares to fall 40%. On the surface, this looks to be an overreaction as, apart from the dividend payout, brokers only cut forecasts by around 20%. Here are Equity Development’s changes:

One reason for the bigger fall is that the market may not believe these numbers as they rely on a significant H2-weighting to come in inline. However, the main reason was probably this:

As anticipated, the Group's net debt increased to £93.1m (FY 2022: £87.4m). This represents a net debt/adjusted EBITDA ratio (calculated on a trailing twelve-month basis) of 2.66x which complies with the Company's debt covenant threshold of 2.75 times.

That looks pretty tight, and one could be forgiven for thinking they are about to breach covenants. Especially as these step down to 2.25 times from the end of the year.

The Equity Development presentation gave some comfort, though. They have declared a 0.9p dividend, and given that the banks have a blocker in pace above 2.5 times, this means that the current net debt to EBITDA must be below this level. This was confirmed by the company, who said they now had “significant headroom” to the 2.5 times level. Partly, this is due to postponing any capex that isn’t immediately revenue-enhancing. However, they point out that Q4 tends to generate maximum operating cash flow, so they are confident of getting down to the target of 2.1x at the year-end.

Overall, the CEO was adamant that they won't breach covenants, won't require any equity raise, and their banking syndicate is supportive. He said that when he joined the business (under Private Equity ownership), they had a 7x leverage ratio because the kettle controls business is very resilient over the long term.

On hitting full-year targets, they pointed out that Q3 was almost over, so they have good visibility of the £6.5m adjusted profit after tax for that quarter. This leaves £9m adjusted PAT to do in Q4 to hit their full-year target of “in excess of £21m”, a number they seemed confident with.

Putting it all together, Mark doesn’t think this is crazy cheap on the short-term numbers. However, he is fairly confident they will hit their H2 EPS and have very little chance of breaching debt covenants or there being severe negative consequences if they do. As such, the 40% drop in share price looks like an overreaction. Anyone selling on concerns over debt covenants or H2 weighting has probably jumped the gun.

Tandem (TND.L) - Interim Results

Weak revenues here mean a loss-making half:

Group revenue in the six months to 30 June 2023 of £9.8 million (H1 2022: £12.9 million)

Loss before taxation of £0.9 million (H1 2022: profit of £0.3 million)

And net debt continues to rise:

Net debt as at 30 June 2023 of £3.1 million (30 June 2022: £1.5 million)

This is the crux of the matter, but it doesn’t exactly seem clear what they are saying:

Given the challenges mentioned, the Board anticipate that the Group's sales for the FY23 full year will reduce between 11 and 13% against market expectations and that the Group will be approximately break-even at an underlying Profit Before Tax (PBT) level for FY23.

So we need to turn to the updated Cavendish note:

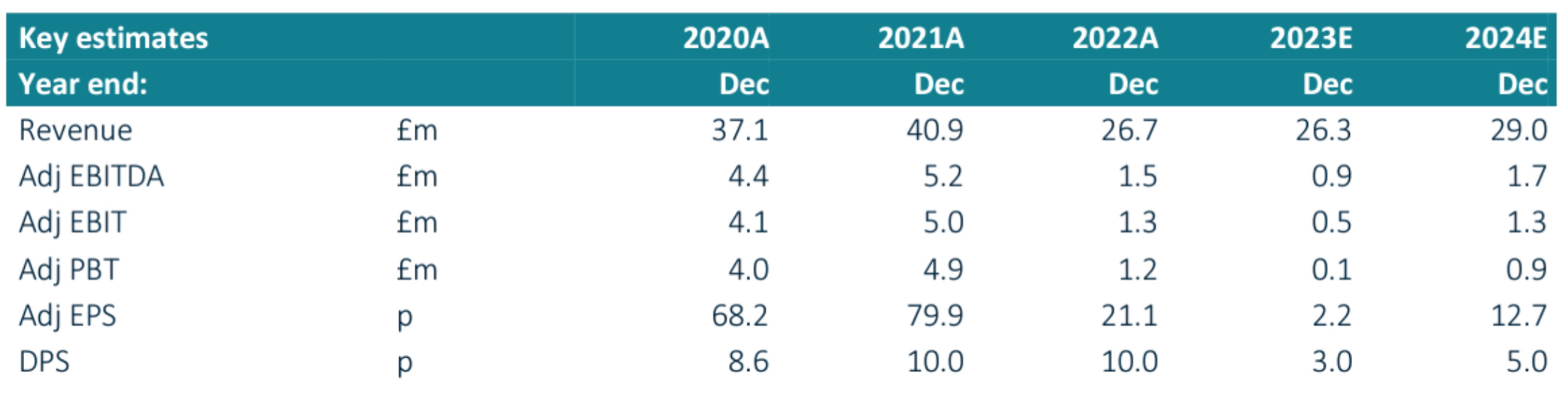

So 2.2p EPS this year, 12.7p next year. Down from 17.2p and 23.4p respectively. They’ve taken an absolute axe to these forecasts. And in light of this, the 20% drop in the share price looks very light. If we believe FY24 estimates, then they are on a forward debt-adjusted P/E of around 20.

But we are reaching the point where tangible asset backing is starting to provide support. At around 0.5 TBV this could interest deep value investors, but it looks like a wait of many years before these assets have any chance of being acceptably productive.

Adding insult to injury, company secretary David Rock saw so much value here following the share price drop he spent a massive £737 on shares (no k missing here, this is actually less than a grand). To be fair, they also announced a bigger buy from another PDMR, but frankly, a £737 buy from a director after terrible results looks bad.

Xaar (XAR.L) - Interim Results

More terrible results, as usual, from the supposed growth company:

Cost cutting and a lot of adjustments get them to an increase in adjusted PBT:

But the cash balance reveals the true state of affairs:

The shares dropping less than 10% in response to these results looks light, given that this company has largely defied gravity in the small cap sell-off. And it is on a forward P/E of 50 with declining EPS, even if you believe the heavy adjustments.

That’s it for this week. Have a great weekend!

Thanks for the insight on Discord, both it and the Small Caps Live presence there are until this last week completely new to me, I personally was only aware of SCL at all, through Substack.

This week's clarification/ guidance is therefore helpful and enlightening, and if in future I have something to say I'll do so there. Best wishes, (and no hard feelings Mark, I remain a big fan of your very practical 'Excellent Investing' book).

TEIN.