Small Caps Live Weekly Summary

CAPD CAU DBOX HEAD RCH SDG SHOE

Here’s a selection of what we looked at this week:

Capital (CAPD.L) - Q4 Update

We’d previously commented that the revenue guidance looked a challenge, and so it has proven to be:

As detailed below, FY 2024 revenue was $348.0 million, up 9.3% on FY 2023 ($318.4 million) but marginally below our guidance of $355-375 million.

This has marked the 8th Quarter where the company has disappointed, and while each disappointment was relatively minor, they are starting to add up.

The key problems are:

Nevada Gold Mines ("NGM") has seen delays which has had significant impact on Group margins with the contract revenues not yet supporting the cost base put in place to deliver the project.

The MSALABS ramp-up is slower than expected. Plus, the unexpected end of their mining contracts. There is some news on the mining side:

The Company is pleased to announce that it has a letter of intent from Barrick, the operators of Reko Diq, to significantly expand our service offering at its 50% owned major copper-gold project in Pakistan beyond the reverse circulation and diamond drilling geotechnical services we have provided since early 2023.

These additional works will utilise the majority of the Group's combined mining fleets and cover two components: early works civils and mining services contract plus a longer-term tailings storage facility services contract.

Given the strength of the relationship with Barrick and the fact that they are already the drilling contractor at Reko Diq, this looks like a done deal, even if the paperwork isn’t finalised. However, the majority of their kit could mean 90% or 51% so it would have been good to get more detail on this. While the first contract is for three years starting mid-2025, the TSF construction will only be fully operational in 26H2.

They say this generates a higher return than selling the kit, but many shareholders would have liked to see the back of the troubled mining part of the business. With hindsight, all of the diversification efforts look to have destroyed shareholder value so far. If they’d not bothered with mining or going into the “safer” US and remained an African-focused driller, they would have almost certainly generated higher shareholder returns. Especially considering that a dilutive raise was used to find the initial mining contract.

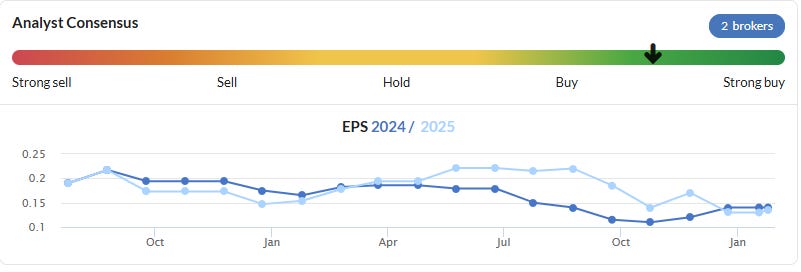

Strangely, and as far as we can see, this revenue miss has not been converted into an EPS change by the brokers:

Indeed, the only change in consensus this week is a slight upgrade in 2025 EPS! This may be previous conservatism in forecasting on the part of their brokers or incompetence. We probably need to wait for the financial results to be sure.

Despite these worries, the company remains cheap on both assets and earnings. However, management have much to prove. Redeploying the mining kit means that debt remains higher than we would like too, and although capex is guided to moderate:

Capex for 2025 is expected to be ~$45-55 million

…they are not forecast to have paid off their debt until the end of 2026.

Centaur Media (CAU.L) - Trading Update

The price has been unusually strong here recently, and this may be the reason:

Trading, since our last update in October, has been ahead of our outlook and the Board now expects the Group to achieve revenue for FY24 of c. £35m at an adjusted EBITDA1 margin of approximately 16%, ahead of consensus

This works out to be a 10% EBITDA beat. Is this a case of walk it down and then back up, though?

At least the previous downgrades were RNSed profit warnings. There's nothing worse than a company quietly lowering expectations via the broker before declaring a minor beat on expectations.

The share price is back up to where it was when the EPS forecasts were around 50% higher. So, while this week’s news might be the start of a recovery trend, quite a bit of that recovery is already priced in.

DigitalBox (DBOX.L) - Holding in Company

We assume that this means that the Downing overhang is cleared here:

This seems to suggest that 20m of the shares have gone to another Downing fund. If this was the case and we were holders in the closing down Downing Strategic Microcap Fund, I’m not sure we’d be too happy to transact at 3.7p when the mid-price at the time was closer to 5p. We are also not sure why Downing didn't just do that in the first place rather than wasting their time asking for a new NED and forcing a strategic review?

Headlam (HEAD.L) - Trading Update

The Group expects the underlying loss before tax for the year to be circa £34 million, subject to audit.

The last trading update said the underlying LBT for H2 was similar to H1, which was £16.4m, so that would be £32.8m if exactly the same. Today, they say £34m LBT, so that’s potentially a small further miss, although perhaps not outside of the range that could match the earlier statement.

Now, in net cash after the sale of properties:

The Group ended the year with net cash1 of £11 million and a property portfolio valued2 at £95 million.

The problem is that the bulk of the debt was turned into lease liabilities. This was much more driven by liquidity requirements than a sale of surplus property. They absolutely have to stem these losses because, at these levels, they will quickly eat into all of the asset value.

They blame it all on market conditions, but Likewise are massively outperforming them. The time to buy maybe when they actually accept they are being outcompeted, not just unlucky.

Reach (RCH.L) - Trading Update

It’s not all doom and gloom in advertising land.

Trading in Q4 was strong. As a result, we now expect to deliver results ahead of current market expectations for the full year.¹

However, the additional announcement re-inforces how much of this business is run for the pension funds, not shareholders:

The West Ferry Printers Pension Scheme (WF Scheme) is a legacy scheme inherited in the 2018 acquisition of Express Newspapers. As part of the due diligence to prepare the WF Scheme for buy-out, a historical error has been discovered resulting in an estimated £5m additional funding requirement, which we expect to pay in 2025.

For trading, it’s an ahead for adjusted operating profit but with absolutely no details on whether revenue is ahead, whether it’s due to circulation or digital, advertising rates or even just cost cutting, or they’ve managed to make more adjustments than usual. With the lack of details and the history of the company, you have to assume the lack of detail is intentional.

Sanderson Design (SDG.L) - Trading Update

The Board now expects Group sales for the year to be approximately £101 million (FY24: £108.6m), a shortfall of less than 5% to its earlier expectations, but the resultant sales mix will have a significant impact on full year profitability.

The licensing side of the business is doing pretty well but it means the core business is now heavily loss-making:

Licensing has shown good momentum since the half year results and is expected to end the year delivering revenue in the region of £10.1 million to £10.9 million (FY24: £10.9m), with the final outturn dependent on the timing of signature of contracts in work.

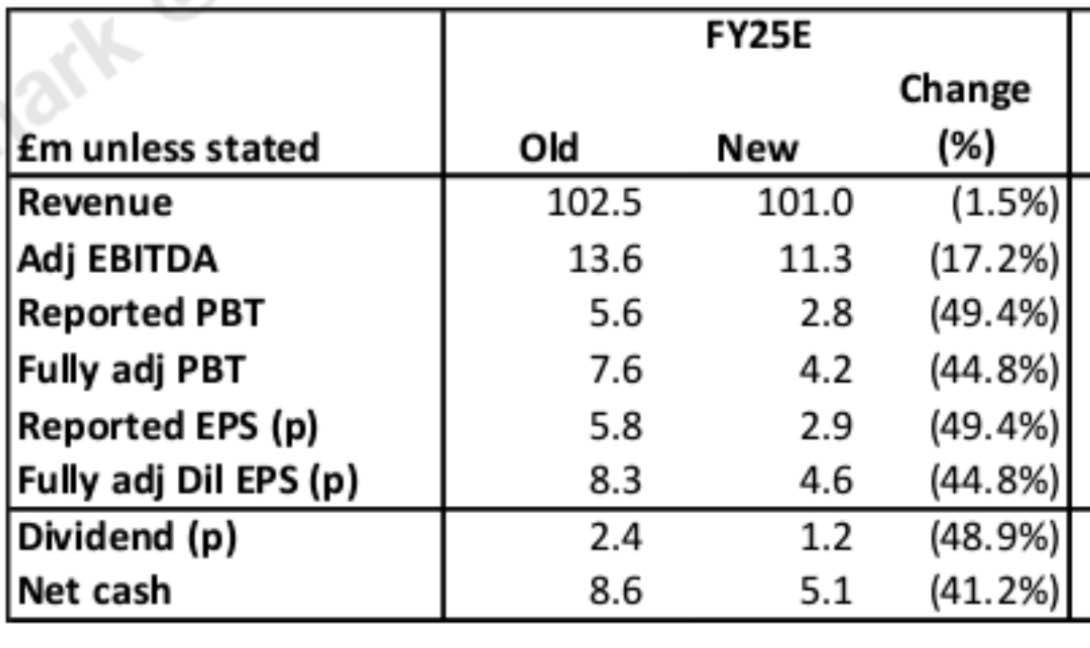

After the brokers have run the numbers, pretty much every metric that matters down 40-50%. Here’s Progressive’s take:

It shows how finely balanced things are here, though, with just a £1.5m revenue miss and an unfavourable mix halving EPS. Again, it seems they are either slow or unable to take costs out of the business.

On the bright side, licensing probably supports a valuation above the current valuation, assuming they eventually get the costs under control. This is clearly a cyclical business that will eventually have its up cycle. We were cheekily hoping that in bad markets, the price was going to fall by similar amounts to the PBT. In the end, a 20% fall left it a bit meh. Probably undervalued on a long-term view but more expensive on earnings than prior to this update, and with little idea of when things would turn.

To make matters worse, Colefax reported reasonable first-half results this week:

Group sales up 1.8% to £52.79 million (2023: £51.84 million) and up 4.1% on a constant currency basis

Group profit before tax down 0.5% to £4.36 million (2023: £4.38 million)

Earnings per share up 12.5% to 53.2p (2023: 47.3p)

This suggests that it isn’t all market conditions causing the issues at Sanderson.

Shoezone (SHOE.L) - Final Results

In isolation, these results don’t read too badly:

But they simply don’t seem to comment on the outlook, presumably, because it is terrible. Broker, Zeus, is forecasting a further halving of EPS and suggests they can’t afford to pay a dividend. At least these are not a further downgrade, though. They didn’t report Christmas trading with the Final Results last year. However, in the trading update on the 18th December, they said:

A further trading update will be provided alongside the announcement of our FY2024 annual results on 21 January 2025.

So to just ignore this commitment is a bad look. They talk about investment plans and a possible H2 upturn, but we are left to assume that the last month was terrible, and this will continue for the rest of H1.

Inexplicably, the share price rose this week despite it trading on at least double the rating of other similar struggling businesses, a P/TBV of 1.6, and 17x forward earnings (adjusted for cash and onerous leases, etc.). We suspect many investors are anchoring on past glories, which don’t look to repeat anytime soon, or perhaps ever.

That’s it for this week. Have a great weekend!

Thanks Mark and Leo. Your pin-sharp observations on company statements (or lack!) provide fascinating reading.