Small Caps Live Weekly Summary

GTC HEIQ HSS MORE PGH ZOO

The sheer volume of recent news means that it can be hard to keep up with everything going on in the small cap space. Here are just a few of the things we looked at:

Getech (GTC.L) - Interim Results

We have long been critical of this company’s attempts to branch out from its core oil & gas geospatial data business. The logic that their seismic database would be ideally suited to the process of locating what, to our simple minds, sounds a lot like petrol stations for hydrogen vehicles, seemed far-fetched to us. As was the idea that such a small company could fund construction projects of this size

As usual, at this point, we present the following timeline without comment:

27 April 2011: Getech Chairman, Dr Stuart Paton, is awarded 900k share options at 17.5p that expire on 27 April 2021.

9 June 2020: H2 Green Ltd is incorporated with 1p of share capital.

20 November 2020: Dr Stuart Paton is appointed as a director of H2 Green Ltd. The Getech share price is 11.25p. At this point, options exercisable at 17.5p expiring in around 6 months have negligible value.

26 January 2021: Getech’s exclusive strategic partnership with H2 Green is announced to great fanfare. The Getech share price rose 85% to 25.2p.

28 January 2021: Getech announces that after a handover period, Dr Stuart Paton will leave the Getech Board. The Getech share price is 33p, making Dr Paton’s options worth around £140k on this date.

Now, a completely new management team has come in. The Executive Chairman, Richard Bennett, will become CEO and a new non-exec Chair appointed:

Interim executive Chairman Richard Bennett, appointed in February 2023, has agreed to become Acting Chief Executive Officer of the Group with Michael Covington, currently Non-Executive Director, to be Chairman Designate. Both appointments expected to be confirmed as permanent in due course.

In these results, we find out that their new strategy is back to the old one, to:

re-focus the Company on the core business of locating subsurface resources;

It seems H2 Green has become a holding company for their green “assets” and they will “switch to developing H2 Green's assets in partnership.”

Richard Bennet’s Twitter handle appears to be @CleanTechRich. We are yet to see if he will change this to @DirtyTechRich now the company he is CEO of generates almost all of their revenue from the Oil & Gas industry.

Seriously, though, this does appear to be the move the company needed to make to stem the losses. In the IMC Results Presentation, Richard seemed keen to point out that all of the H2 Green stuff happened before he joined the company. And he apologised for appearing to be enthusiastic about H2 Green in previous presentations. It also seems that they were hoping to spin H2 Green off as a separate company. This is why Graham Cooley only lasted 3 months as a director of H2 Green. Presumably, their brokers pointed out that this isn’t 2021 anymore.

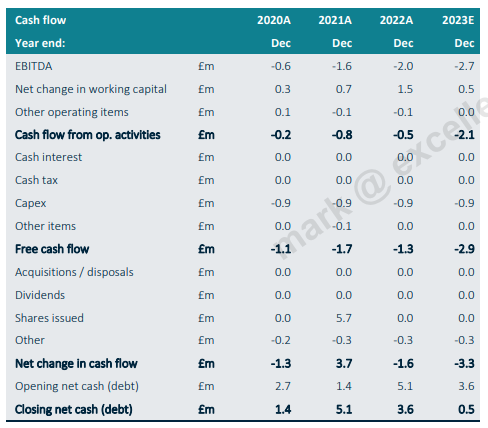

Realistically, Richard has come into a very tricky situation, as despite cost savings, broker Cavendish have net cash down to £0.5m at Y/E:

They also have NWC improving to -£1.1m from the current -£1.3m:

So that's a £1.0m cash outflow for H2. £0.8m from trading and £0.2m from working capital. The big question is: Do they get a going concern statement in the annual report with that level of ongoing cash outflow? Since they wouldn't appear to have 1 year's worth of cash left. They would need very material improvement in FY24 trading to make that argument, in our opinion.

On top of this, there seems to be some question over whether they should have adopted a going concern basis in the current Interims, as they appear to have left in one of the review comments:

“Andrew” here is presumably Finance Director Andrew Derbyshire. That they left a review comment in the final RNS, leaves shareholders with some doubt as to whether this process has been done, or if the unknown commenter knows what a going concern cash flow projection looks like.

When Getech first said they were aiming for net zero, we didn’t realise they were talking about the share price!

Heiq (HEIQ.L) - Accounts Update

Heiq claim to be doing better than everyone else in their industry:

Whilst management considers the Company to be performing better than many of its peers, the significant disruption in market demand across HeiQ's value chains has impacted the Company's financial performance for FY2022. HeiQ expects to report FY2022 revenue in line with the most recently published guidance but gross profit and loss from operations for FY 2022 are expected to be materially below previous market guidance

But it turns out they are still materially below market expectations! These were expectations that have already been slashed a couple of times by the broker Cenkos (now Cavendish, after the merger with finnCap). We must be well into loss-making for both 2022 and 2023 by now.

They blame goodwill write-offs and inventory write-downs. But I also note that Leo was right to point out the following table in their 2021 AR when we looked at them last:

As they now say:

Specifically, restatements have been recorded around impairment of goodwill from acquisitions as well as in relation to the accounting treatment of a significant take-or-pay contract. This contract has been renegotiated in 2023 and accounts receivable have been waived in exchange for a right of first refusal on the supply of a wide product range to a large industry player.

You always find the bodies of revenue recognition in the balance sheet. So, how is this affecting them:

The cash balance as of 31 December 2022 was US$8.5 million, in line with market guidance. To manage its cash balance, the Group has access to credit facilities totalling CHF9 million (approximately US$9.8 million).

But it seems the credit facilities can be withdrawn with 12 months’ notice and become repayable at that point.

While the facilities are not committed, the Board has not received any indication from financing partners that the facilities are at risk of being terminated. Nevertheless, the Board acknowledges the uncommitted status of the facilities which could be terminated requiring the refinancing of debts, and which casts material uncertainty on the going concern assessment.

And now they are using the facilities:

As at June 30, 2023, the Company had cash balances amounting to US$7.3 million with a total of CHF6.3 million drawn under the facilities.

Net cash is roughly zero, then, and probably net debt by now. They are unlikely to be able to repay that debt if it is called. We expect an equity raise together with results and re-listing.

HSS Hire (HSS.L) - HY Results

These aren’t bad results considering the market backdrop:

But all eyes are on the outlook:

However, the weak macro environment has caused trading in the first twelve weeks of H2 23 to slow considerably to 2% (H1 23: 6.3%), albeit with significant week on week variation.

Surely that's not so bad? Looks pretty much in line with the fall in the inflation rate.

the Board currently expects full year Adjusted EBITA to be in the range of £23m to £30m. Even at the lower end of this range, the Group will deliver the second highest Adjusted Profit Before Tax in its listed history

The AGM update did not give market expectations, and there is no broker coverage we can access, but Stockopedia appears to have the updated summary:

The January 1st Year end has confused the titles here, so the dark blue line is 2023 and light blue 2024 estimates. It appears that Numis have kept 2023 estimates the same but halved 2024 estimates to 1.2p of EPS on 3.6% revenue growth. They still appear to be predicting a 10% increase in dividends though, giving a 5% yield. But without seeing the details of the note, and without a management presentation accessible to individual investors, we are largely flying blind here.

Hostmore (MORE.L) - Interim Results

There's evidence fresh management is helping here. Here's what the old Hostmore plc management believed:

We have to keep opening restaurants due to the franchise agreement with TGI Friday's in the US

Investors expect the growth that was promised to them when the company spun out

We are operating a premium destination restaurant

The TGI Friday's brand needs to be renewed as "Fridays"

Here's what the new management understands, with the evidence from these results:

US Corporate would much rather have some franchise revenue than none, and would prefer to have very little in the short term than completely destroy the brand in the UK

Previously announced annualised cost reductions of £5.9 million now increased to £8.2 million

a substantial reduction in central costs

Remaining investors don't care about growth: they are either speculating some value might remain or can’t read a balance sheet.

The Group has committed not to make any new restaurant openings in FY23 and FY24.

They are operating a mid-market restaurant popular with particular market segments and convenient for large group celebrations. Nobody is interested in an upmarket version.

we delivered compelling value offers for customers, such as our kids eat free initiative that ran throughout the August school holiday

Our "2 for 1" cocktail pricing was trialled at six restaurants in early 2023.

Everybody calls it "TGI Fridays" or "TGIs". Nobody calls it "Fridays" or cares about a new "63rd+1st" brand.

it is clear that TGI Fridays is a highly recognised brand with a rich heritage

There’s no recent financial data in the results themselves, but they do say:

Our LFL revenue in H2 2023 to 24 September is already +2% versus H2 2022.

Clearly, that is behind all measures of inflation and wage costs, though their overall costs are reducing as per the above. Looking at the cash flow statement over the 6 months, it is not too bad. We would expect them to be H2 weighted due to school holidays, Christmas, and, to some extent, the typical UK pattern of better weather in May/June than in August. It would really help if they could renegotiate leases (again?), although exiting unprofitable sites clearly helps.

However, the balance sheet looks awful at every level:

Negative tangible assets

Goodwill still does not look credible

Receivables looks to be a temporary low

Payables are either stretched or may benefit from timing

Current ratio of 0.26x

They also need to refinance, and increasingly, it looks like fresh equity will need to be a component of that. Don't expect any news soon, though:

Refinancing process commenced with existing and potential new lenders, expected to be concluded by end of Q1 2024

Until this is out of the way, this will remain an option-like gambling chip, with all the share price volatility that this implies.

Personal Group (PGH.L) - Interim Results

The face-to-face sales, recurring revenues, but inevitable attrition of their core insurance business means that they were hit hard by COVID-19, but both the decline and recovery lagged significantly behind other companies. Here is whatthey report today:

Basic EPS increased to 4.5p (H1 2022: 1.7p)

Trading remains in line to meet market's full year expectations

These are (according to Stockopedia) for 15.1p normalised EPS versus -1.21p in 2022, but still significantly short of the peak of 28.4p in 2019 and resilient 22.1p in 2020.

Cavendish (formerly finnCap) have introduced FY 2024 forecasts, but these are rather disappointing, showing only a progression from 14.3p to 14.8p EPS on their adjustments. Also disappointing is the lack of financial income on their insurance float.

Performance is adversely affected by high inflation as insurance premiums and benefits are set at a fixed level which is generally maintained until the customer cancels, changes job, or dies. After all the expense of face-to-face sales, sending out letters suggesting that they should increase their premium to match inflation could be counterproductive. Any communication that reminds the customer that they have a policy in place also gives them a reminder that they may not be getting value for money!

Meanwhile, costs and investor expectations rise with inflation. As their main product pays out for hospital stays, their liability is limited by the capacity of the NHS, which had actually been increasing. The recent strikes will have had a positive effect for them, but this is not mentioned today.

Revenue is not a useful metric here due to the level of pass-through in non-core business, something they are quite clear about. They imply there may be scope to materially monetise this in future:

Since being appointed CEO in August I have commenced a quantitative review of our operations in order to identify the greatest available opportunities to improve profitability and drive longer term growth in the business to increase shareholder value.

However, with a forward P/E of 12 and little growth in the near term, this potential looks fully priced.

Zoo Digital (ZOO.L) - AGM Trading Update

As we (and it seems the rest of the market, given the share price weakness) predicted, there is a further profits warning. Broker Progressive slash current year forecasts:

Given the severity of the decline, one may imagine that this isn’t the first point management realised they may be in trouble with these forecasts, as they say:

Despite this progress, the ongoing disruption continues to have a significant short-term impact and market expectations for ZOO's FY24 outcome assumed former order levels would resume from October 2023. This now looks unlikely, and therefore a range of revenue outcomes for the second half of the financial year is possible ranging from a similar level to the first half to an increase in revenue in Q4.

But more worryingly, Progressive remove FY25 estimates:

The current markets are pretty brutal with any company that misses short-term forecasts, even if the risk was known, and the share almost halved on the open. Sadly, Mark had not heeded his own advice that a further warning may be on the way and started buying some prior to this statement.

The shares recovered during the day, helped by a £50k buy by the CEO at 40p/share. The company’s finances are actually pretty robust, given that they had net cash and then raised money at 160p to fund an acquisition. That is on hold due to the state of the end market, which means that net cash is forecast to be at least $16m at the end of this month. Progressive forecasts this down to $8m at the end of the year as a worst case, assuming no resumption of major orders, but then the company says:

The Board has taken steps to mitigate ZOO's position through the implementation of cost reductions with the objective of achieving break-even in respect of fiscal Q4.

Given the impact here, one can easily see that smaller suppliers to the industry may now be in trouble, which is why, presumably, Zoo say:

…the Board will continue to pursue small investments in strategic locations at attractive valuations that strengthen ZOO's proposition for international dubbing.

And there may well be some truth in it when they say:

The Board is confident that the changes arising from strategic reviews by ZOO's major customers will be favourable for the Group. These include accelerated transition to an End-to-End approach, studios engaging with fewer, more capable suppliers, and greater dependence on ZOOstudio, all of which will strengthen ZOO's market position.

So, it is easy to see why the share may have bounced significantly off the initial lows. Their $400m 2028 revenue aspiration looks a loooong way off, though.

That’s it for this week. Have a great weekend!