Small Caps Live Weekly Summary

GDP GKP HUM QUIZ SOM

Another quiet week, as expected, with Monday a UK Bank Holiday. UK-listed companies reporting this week tended not to be UK-based for the majority of their operations:

Goldplat (GDP.L) - Q4 Operating Results

Although these are billed as operating results, they contain quite a lot of trading information. Given that these are for the period ended 30th June, investors could be forgiven for assuming they were going to be terrible, and the recent price action suggested this. However, instead, we got this:

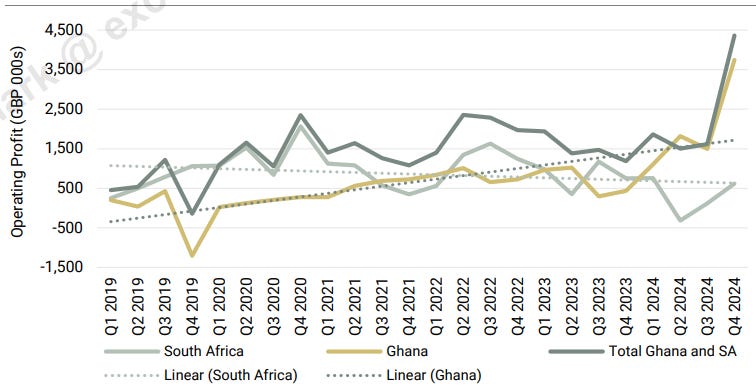

The two recovery operations achieved a combined operating profit for the quarter of £4,360,000 (excluding listing and head office costs and foreign exchange losses) which represents a 267% increase against Q4 in the previous period (Q4 2023 - £1,188,000).

Bear in mind this is a £4.4m operating profit for a single quarter vs £10m market cap! Their recovery operations in Ghana made the bulk of the profit, but at least South African operations are profitable and improving this time.

Broker Zeus has a nice chart putting this in a historical context:

It may be a stretch to assume similar levels of performance going forward, but the trend, at least in Ghana, is looking good. One of the mysteries is that Zeus didn’t upgrade their EPS for this amazing quarter, choosing to keep their 1.7p forecast. However, given the figures are largely known, Mark gets 1.9-2.1p EPS depending on how any historical tax liabilities are treated. So, it seems likely that the results will show an EPS beat unless there are any unexpected banana skins prior to release.

There are reasons that many avoid this sort of company. The usual complaint is that they don’t pay a dividend but have a large net cash balance. The reality is that they have big working capital swings and interest costs to fund a pipeline of material they have sent to gold refiners. This should ease in the future, with a focus on producing more dore bars in Ghana and the recent start of an in-country refinery. However, it will take time before this works through the system, and more free cash accumulates. Secondly, management appears to be very cautious and not very proactive. This has hurt them in some areas, such as the timing of backup generator delivery, but we guess you have to be cautious to be able to operate long-term in African gold recovery!

This sort of company will not be investable for most investors. Still, it is hard not to see opportunity at a P/E of 3 and the chance of improved free cash flow over the next few years for anyone with a high enough risk appetite to consider a resource company in Africa. Those dividends and buybacks must surely appear at some point, despite the glacial pace on this front. When they do, with quarters like the one they’ve just had, they could be very material compared to the current market cap.

Gulf Keystone Petroleum (GKP.L) - Half-Year Results

With many companies such as this, the financial results are not that interesting. Here, they reflect the lower price realised from local production, offset by lower costs:

Adjusted EBITDA increased 6% to $36.4 million (H1 2023: $34.2 million) as higher production and cost reductions offset the decline in realised prices related to the transition from exports to discounted local sales.

Revenue decreased 11% to $71.2 million (H1 2023: $79.6m) as the increase in H1 2024 production was more than offset by the 49% decline in average realised price to $26.3/bbl (H1 2023: $51.3/bbl) o Gross operating costs per barrel decreased 25% to $4.2/bbl (H1 2023: $5.6/bbl), reflecting higher production and cost control

This is the new news:

Strong gross average production in July of c.47,900 bopd and in August to date of c.48,200 bopd

Realised prices have fluctuated between $25/bbl - $28/bbl and are currently at c.$27/bbl

This is all fairly positive, especially as they get paid upfront in cash for these barrels. However, the market wasn’t a fan, and the price dropped slightly. This is probably because no further dividends or buybacks were announced with these results. This could mean they think the pipeline restart is imminent or simply don't want to take the risk. Either the pipeline restart or a dividend declaration will probably be required before any material move in the share price, both of which are a little unpredictable.

Hummingbird Resources (HUM.L) - Pasofino Update

Having had a torrid time this year, shareholders will be pleased that one area of the business is going well:

Pasofino is actively engaged in discussions with several interested parties, two of which have submitted non-binding expressions of interest to acquire the company.

Hummingbird divested their Dugbe project to TSX-listed Pasofino in return for funding the drilling and studies required to progress it, retaining 53% at the company level. Shareholders will be relieved that they are not considering funding another huge project with debt, as the last one, Kouroussa, has left them financially stretched. If an offer does come in toward the end of this year, then this could also transform the Hummingbird balance sheet. However, this hummingbird is definitely in the bush, not the hand, at this early stage.

Quiz (QUIZ.L) - Final Results

Given the collapse in trading, our first port of call is always the balance sheet. Things are slightly brighter with net cash up since the year-end, but a material uncertainty remains, as expected:

As at 31 March 2024, the Group had £2.0 million of total liquidity headroom, being a cash balance of £0.3 million and £1.7 million of undrawn bank facilities (31 March 2023: £8.3 million of total liquidity headroom).

On 28 August 2024 the total liquidity headroom available was of £2.3 million, being a £0.4 million cash balance and £1.9 million of undrawn bank facilities.

They confirm bank facilities have been renewed and:

In addition, discussions have commenced with Tarak Ramzan, the Company's founder and largest shareholder, with regards to the provision of a £1.0m loan facility to provide additional liquidity headroom for working capital purposes.

Regarding the material uncertainty, the base case includes a lot of chicken counting, assuming various trading initiatives are about to suddenly spike revenue by 12.5% (they have had no time to take effect yet). The downside scenario involves no further downside regarding YoY trading, and even with the (yet to be agreed) shareholder loan, they run out of cash.

Adding to the risk, they also reveal:

Subsequent to the year end the Company received a claim letter from a supplier of IT software in relation to a contract for services entered into February 2020. Further to the provision of initial advice from Kings Counsel, the Group does not consider that any monies are due under this contract and as such does not accept any liability in respect of this matter. The potential claim amounts to £673,000 plus VAT with the potential for interest of £573,000 to be sought on this amount.

Why would the lender have renewed under these circumstances? This is why:

facilities are repayable on demand

Why would a company director agree to a director loan rather than just trying to take the company cheaply? This is why:

During the year we completed the previously announced investment at our Distribution Centre which was focussed on accommodating more efficient working practices. This work provided a new mezzanine level to increase storage space and an improved layout at a cost of £1.3 million.

To spell it out: It might look bad if money spent improving somebody else's property was the reason for running out of cash. We suspect the shareholder loan is just awaiting advisor sign-off and is a done deal.

Somero (SOM.L) - Half-Year Results

When previewing these upcoming results, contributors on the discord server were expecting between 14-18c EPS. The actual result, therefore, came in at the lower end of expectations for many:

Diluted adjusted net income per share $0.14

A few things have not gone well for the company this half. For example:

Revenue from ROW declined 38% mainly driven by lower volume in Middle East compared to prior year

And:

H1 2024 North American sales declined 8% from H1 2023 to US$ 38.8m mostly driven by lower sales of Boomed screeds. Customers in the US continue to report healthy project levels, however they are not operating at full capacity due to project start delays and pauses caused by elevated interest rates, labor shortages and concrete rationing, as reported in the 30 July 2024 Trading Update.

As we have commented before, machine demand is more related to peak construction demand than the absolute level of construction, so a continued lack of concrete will have an ongoing negative impact. On the positive side for mitigating competition-related market share losses:

Products released since 2019 contributed US$ 3.1m in revenues, up from US$ 0.8m in H1 2023

Despite the weak H1, the outlook continues to guide the full year in line due to an unusually high H2 weighting:

The Company anticipates improvement in H2 2024 trading in compared to H1 2024, driven by a combination of new product revenue growth, including the launch of a third new machine, and an expectation of improved weather conditions. This confidence is supported by our primary means of gauging market health, which is direct feedback from customers.

As such, the Board remains confident that 2024 results will fall in line with the revised market expectations published following our 30 July 2024 Trading Update, with revenues of approximately US$ 110.0m, EBITDA of approximately US$ 30.0m, and year-end cash of approximately US$ 27.0m.

They are also benefitting from being US-based and able to rapidly reduce headcount without significant costs being incurred:

Implemented company-wide workforce reduction of 15% combined with strict cost controls for the remainder of 2024 to partly offset the profitability impact of the revised 2024 revenue expectations

So, how likely is it that they report in line for the full year? $110m FY revenue guidance at 55% gross margin means $32m GP for H2, and if they reduce headcount by 15% in all departments, they could generate, say, 10% savings after inflation & adding in the addition costs in Belgium, and end up with $16.3m PBT for H2 vs $10.6m for H1, which would be 23c for H2 with a 21% tax charge. So, it is undoubtedly within touching distance of the in-line for the year at 24c forecast for H2. However, this is only if investors believe the company has good revenue visibility over H2 trading. Hence, it remains a riskier proposition than it was in previous years.

That’s it for this week. Have a great weekend!