Small Caps Live Weekly Summary

IMMO WYN NANO SCS SOM PGH DSG MYX

Another fairly volatile week for UK small cap shares, but nothing compared to what has been going on stateside. Many of 2022’s “losers” have been on a tear in 2023. This tweet thread is one of the best explanations as to what is going on:

So not so much Planet of the Apes 2, but the usual crowded hedge fund momentum trades blowing up. This shouldn’t really impact UK small cap markets. However, in the short term, fund flows are the only things that matter, and if the bounce in risky stocks bolsters investor sentiment over here, this could have a sizeable impact on short-term investment returns.

Immotion (IMMO.L) - Proposed disposal of LBE

Lots of announcements from Immotion within a few minutes of each other this week, but the most significant was this:

Whilst the Board believes that considerable growth opportunities are available to the LBE business, it is of the view that as a result of the current and continuing challenges presented by the macroeconomic environment, not least the cost-of-living crisis and inflationary pressures in the US and UK, the trading environment could become much more challenging. In addition, to accelerate growth of the LBE business further capital may be required. The Board is doubtful that debt finance could be secured on acceptable terms and it is unwilling to seek to raise further equity capital at the Company's current valuation. Accordingly, and in order to minimise risk for Shareholders and provide a significant liquidity event in highly uncertain markets, the Board has decided to pursue the Proposed Transaction.

This second announcement perhaps has something to do with it:

Immotion, the UK-based immersive entertainment group, is pleased to announce that it has signed a new 3-year framework agreement (running through to 31 December 2025) with Merlin, covering the 26 sites at which Immotion has already installed or agreed to install a VR attraction.

The new framework agreement streamlines the trading relationship between the parties, as well as the process for agreeing installations into further Merlin venues.

26 sites plus what could be a big expansion to further Merlin sites for LBE may require significant capital that isn’t forthcoming from either banks or shareholders. Hence the sale of LBE:

· Sale of the LBE business agreed, subject to shareholder approval, for an enterprise value of $25,211,739

To be clear, Location-Based-Entertainment (LBE) is their main and only proven part of the business. However, they are retaining the Home-Based Entertainment (HBE) part and intend to remain trading on AIM.

But first, they intend to buyback shares from leaving management:

The Company will buy back the Leaver Shares and Ordinary Shares resulting from the exercise of the Leaver Options for cancellation at a price of 3.65p per Ordinary Share (the "Transaction").

In aggregate, we estimate the cost to be £0.94m. And that compares very favourably to the 2.2p close the day before announcing this. And will leave 380,597,057 shares in issue, which will receive:

· Intended return of the majority of the LBE sale proceeds to Shareholders (up to circa £13.5m, equating to approximately 3p per share), retaining circa £6.5m within the Company for future opportunities.

These future opportunities are acquisitions, presumably also in the HBE space. 3p +£6.5m = 4.6p per share. So buying out former management at 3.65p isn’t egregious. The problem is that we don’t know what the cash shell/HBE will trade at. It probably deserves a discount to net cash but could easily trade at a premium. There would be some irony if it traded higher than the Immotion market cap prior to this sale!

We think these announcements show two more general points:

The first is that UK markets are pretty bad at pricing this sort of stock. With LBE clearly worth far more than the listed market cap in private hands. Instead, listed stocks go through massive booms & busts, which shareholders can take advantage of.

The second is that the Immotion board aren’t very confident about getting a job elsewhere. This really should have been structured as a takeover at the PLC level. If the bidder didn’t want HBE, then they could sell it or close it. We don’t think shareholders would care if they paid nothing for it. At the moment, it is being valued at about minus £5m by the market. Shareholders have potentially been let down by the non-execs, who are expected to protect their interests with this sort of thing.

We’d expect the £13.5m to be paid out fairly quickly, although the mechanism is not clear:

As soon as practicable post Completion, a further circular will be sent to Shareholders setting out the procedure and mechanism for returning the majority of the cash proceeds to Shareholders and requesting the necessary Shareholder authorities.

A special dividend would probably require a court order to create sufficient distributable reserves. They could make a tender offer, but where would they price it? If they do 4.6p or above, then everyone would be daft not to take it in full, and they'd be in the same position as a special dividend due to the scale back but with higher costs. If they price it below 4.6p, then it is a tacit admission that the board and listing are currently detracting value from the remaining business. A tender at below cash screams that the remaining business and board are totally useless, something you'd expect them not to want to shout from the rooftops.

Still, the downside is limited to the 3p payout, and some upside remains, which may make it a good risk-reward bet.

Wynnstay (WYN.L) - Final Results

The company are extremely open that they are getting both one-off revenue gains and one-off margin gains due to commodity price inflation.

· Record results reflect a strong trading performance and substantial one-off gains arising from macroeconomic events (which management does not believe will be repeated)

· Revenue up 42% to £713.03m (2021: £500.39m), primarily the impact of commodity inflation

· Underlying Group PBT* (incl. one-off gains) up 98% to £22.61m (2021: £11.44m)

The question is, what happens next? If commodity prices continue at average FY 2022 levels, then revenue will hold up, but the removal of one-off inventory gains will cause profits to fall as margins normalise. If commodity prices fall, then they could easily be pushed into a loss, but the cash flow will improve.

Looking ahead at prospects over 2023, the sector is facing inflationary headwinds, as we have previously commented. We anticipate this to impact raw material prices, as well as the Group's energy, labour and distribution costs.

So they expect inflation to continue (and it has been since 31st October year-end)? Apart from labour which naturally lags, that contradicts all figures we have seen.

Farmers are facing similar pressures although there have been some welcome downward moves in energy and distribution costs in recent weeks.

The CEO's outlook is slightly more specific:

Trading in the first two months of the new financial year was in line with management expectations, and, looking further ahead, we remain confident of continuing progress against our strategic plans.

They don't quantify the one-off stock gains (mostly on fertiliser), but assuming the volume of inventories held across the year is unchanged, then it is around £20.5m. However, there was an acquisition that the breakdown shows included £2.1m of inventories, so the net figure is closer to £18.4m. This also accords with the figures shown in the breakdown of cash flow.

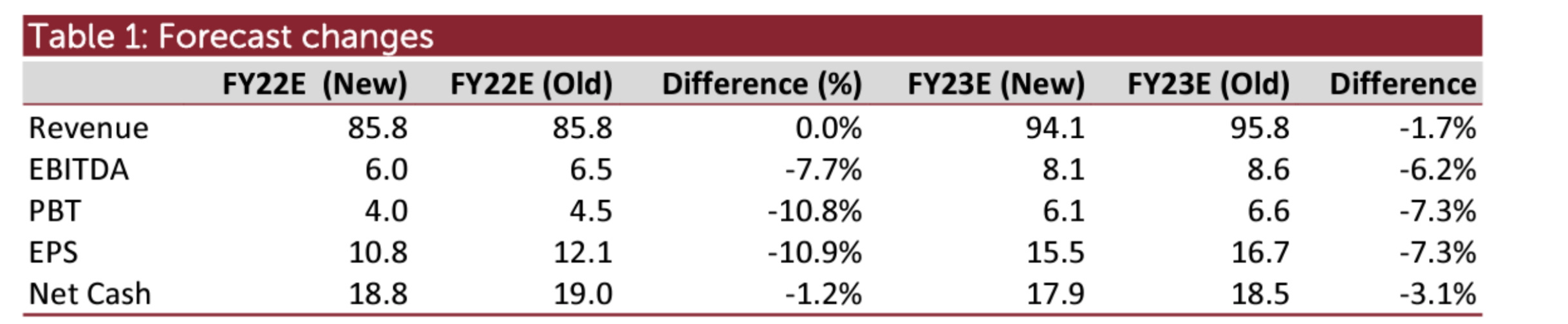

We've got an update from Shore.

Conservatively, we leave our FY23F estimates unchanged

FY 23 seems to build in some further falls in farm input costs. FY 24 EBITDA grows, but after IDA (interest, depreciation, amortisation) is flat and is lower post-tax. They expect higher investment and cash to continue to deteriorate, so presumably, that's the source of higher IDA. So we're looking at a "new normal" of 42p EPS, but with high uncertainty in the short term until volatility in commodity prices normalises.

Cash appears to be sufficient to weather a further increase in inventories caused by any conceivable further commodity price increases. If commodity prices fall, then significant cash would be freed up. The whole industry would be in the same situation making acquisitions less attractive, and it may be more than they could invest internally. Therefore a buyback or special dividend might be possible, providing a good return for those that participated in the fundraise last year that was partly to fund increased working capital.

So a forward PE of 12.7x and a 3.3% yield. Not bad, but this contrasts with a PE of 7 and yield of 6% prior to recent inflationary tailwinds. However, this is significantly below recent peaks of around 15x earnings.

Nanoco (NANO.L) - Litigation Settlement Update

We knew there was a settlement on the way, but not the details, so two weeks ago we were trying to predict where it may come in at. This week we find out:

Definitive Agreements Signed with Samsung for $150 m Litigation Settlement. ·Litigation concluded with $150 m cash settlement to be paid in two equal tranches. ·Nanoco retain over $90 m net proceeds after litigation costs.

So $150m gross, $90m net. This is below many of our estimates. Mark had estimated $150m net (but was not a buyer anywhere near the recent trading price due to doubts as to how much of any cash would make it back to shareholders). Board contributor @otemple was not far off with their $112m estimate, though.

In addition, there is “Modest tax” payable. And any distribution to shareholders will not be before Feb 2024, if at all. So overall, we would say that this was disappointing. The market reaction of 27% down suggests that many were expecting more too.

We also got a separate trading statement:

So not terrible, but still loss-making.

So what's it worth today? That requires assessing the ability of the management to use the extra capital they will retain to drive sales. The Samsung deal shows that the technology is real. However, they have failed to get any significant sales elsewhere for a decade. Net Cash will be around £80m vs a market cap of around £90m at 27p. If they trade at a significant discount to net cash in the future, then this may be worth a punt. However, at the current premium to net cash, this requires the ability to assess the future sales potential of a complex technology product. This goes in the too-hard pile for us.

ScS (SCS.L) - Interim Trading Update

Like-for-like order intake momentum improved significantly throughout the Period and the Group returned to growth of 2.6% in the last 10 weeks, which included the key winter sale. As previously reported, like-for-like performance in the first 16 weeks was impacted by a tough comparative.

As a reminder, their claim that the first 16 weeks’ LFL of -9.1% was only poor due to strong comparables appears false: The calendar year 2021 was only up 0.7% LFL compared to calendar year 2019. Those 16 weeks were very bad, and DFS did far better. So what we believe happened is they (rightly or wrongly) judged that they would not get a strong return on marketing spend for the first 16 weeks, but when they pumped it up for boxing day / new year, the sales came through well. The earlier underperformance against DFS appears to be a business decision, not a fundamental problem.

Two stores have been added during the period, and they have £76.9m cash i.e. their current market cap. Although we don’t know how much of this is customer deposits without seeing the accounts. They say that trading is in line with expectations before any snugsofa acquisition costs or trading profits.

While there has been a lot of inflation since 2019, and we don't know what their marketing spend was, and attempted LFL comparisons are getting increasingly inaccurate and narrow, we think being in line with pre-covid during the winter sales is a very strong position to be in. Consumers spent heavily on sofas in the later stages of covid, reducing the average age, and there is no doubt the cost of living is starting to bite.

Forecast EPS doesn’t make it look obviously cheap tho, excluding the cash:

A 5% forecast dividend and an ongoing buyback help assuage these concerns, though.

Somero Enterprises (SOM.L) - Trading Update

Somero reports record revenue in Europe and Australia, but a lack of customer availability of cement held back sales in NA. They are slightly behind revenue & EBITDA guidance overall. However, this means customers have a backlog, and the outlook is positive:

underlying market conditions in North America remain positive, with customers reporting a significant volume of work comparable to 2022 levels and extended project backlogs.

No sign of a slowdown elsewhere, either:

Market conditions across these regions were positive during the second half of the year and remain so entering 2023.

The Board is pleased with the strong finish to 2022 and looks forward to 2023 with confidence based on the strength of the US market, direct feedback from our customer base on activity, and the growth opportunity in Europe and Australia and from new products. To capture this opportunity, the Company remains committed to adding product development, sales, and support resources; a necessary near-term investment and cost with longer-term benefit.

However, the guidance is for EBITDA to be down in 2023 due to investment:

With consideration to these factors, the Board expects 2023 will be a highly profitable year with healthy cash generation, revenues that are comparable to 2022, and EBITDA that reflects the planned investment to add strategic resources for future growth.

Last year a slight miss and investing for growth would have caused a big sell-off. However, 2023 is different, and we only saw a minor weakness in the share price.

However, it is possible that revenue and profits are being flattered by and only held up due to inflation. A volatile dollar complicates matters here, but the vast majority of sales still come from the US, where inflation is currently 8.6%. So nominally flat revenues have fallen significantly in real terms. Somero's inflation could be different, but at H1, they did talk about cost inflation and raising prices. Using an average of $18m inventory for the year and 8.6% inflation would nominally give a $1.5m P&L benefit. Assuming that wasn't factored into forecasts, that turns a 4% EBITDA miss into a more chunky 7%.

This has also had a knock-on impact on cash levels. As their broker, finnCap put it:

Net cash is expected to be $34.0m, with some impact from the timing of tax refunds and an increase in working capital.

And given their tendency to pay special dividends based on cash levels, forecasts here are cut:

Lower net cash of $34.0m is also reflected in dividends, which we reduce by 22% to 37.5ȼ.

Of course, a dividend cut is what you'd expect for a share priced at a previous 9% yield. And, personally, Mark doesn’t care about dividends here. One of the bear points for him is that Somero hasn’t been able to deploy additional capital to grow and has had to pay it out as dividends. (Given that they expense R&D, this looks like higher short-term EBITDA.)

They have flagged to finnCap that working capital will continue to grow. For 2023 they say:

The reduction in net cash forecast from $44.9m to $31.0m mainly reflects the profit impact on cash but also the prolonged need for higher buffer stocks and inventory to support international sales growth.

Again perhaps this reflects that starving your growth markets of stock to keep the home market happy is no way to run a long-term business. We would say it is also a reflection that there is now strong competition in Europe, and they need to compete on availability, not just reputation.

Despite the miss, they remain very cheaply rated and are not flagging any slow-down in their end markets. Something investors have been anticipating for years. The jury remains out on their more innovative products, but at this price, they are the icing on the cake.

Personal Group (PGH.L) - Trading Update

This reads well, with positive momentum in a number of areas. Although, in line overall and 2022 adjusted EBITDA is down slightly on 2021 on increased revenue suggesting weaker margins. On outlook, they say:

Our products remain extremely relevant in a growing market. This, together with a strong balance sheet, quality customer base and leading technology platform, mean that we are well placed to capitalise on opportunities as employee engagement remains high on the agenda and have a strong platform from which to grow further.

Despite their obligatory bullish narrative, broker Cenkos has interpreted this trading statement as a profits warning:

They’ve taken 11% out of EPS for the year just gone, and, perhaps more worryingly, they’ve cut forward EPS estimates by 7%. Cenkos say:

The table below sets out our headline changes to forecasts, very much driven by the eternal factors affecting its Let’s Connect operations.

We think they may have meant "external", but "eternal" also certainly fits. Overall, this doesn’t look that cheap:

However, there is some real long-term momentum:

Insurance Annualised Premium Income ("API") increased by c.15% to £28.0m (2021: £24.4m)

This is a high-margin product, and after fixed costs and depending on where they set the marketing budget, much of that increase should drop into the bottom line.

Momentum continued into H2, with new business sales records achieved for both the best month

Although the product is high margin, marketing costs are also high, so retention is very important:

Encouragingly, retention levels continued to remain above the Group's pre-pandemic averages and are a validation of the value placed on our products by our policyholder base.

So although this does not look particularly cheap on a P/E basis, the cash flow is strong, supporting a sustainable 5% dividend yield with good momentum on the insurance side.

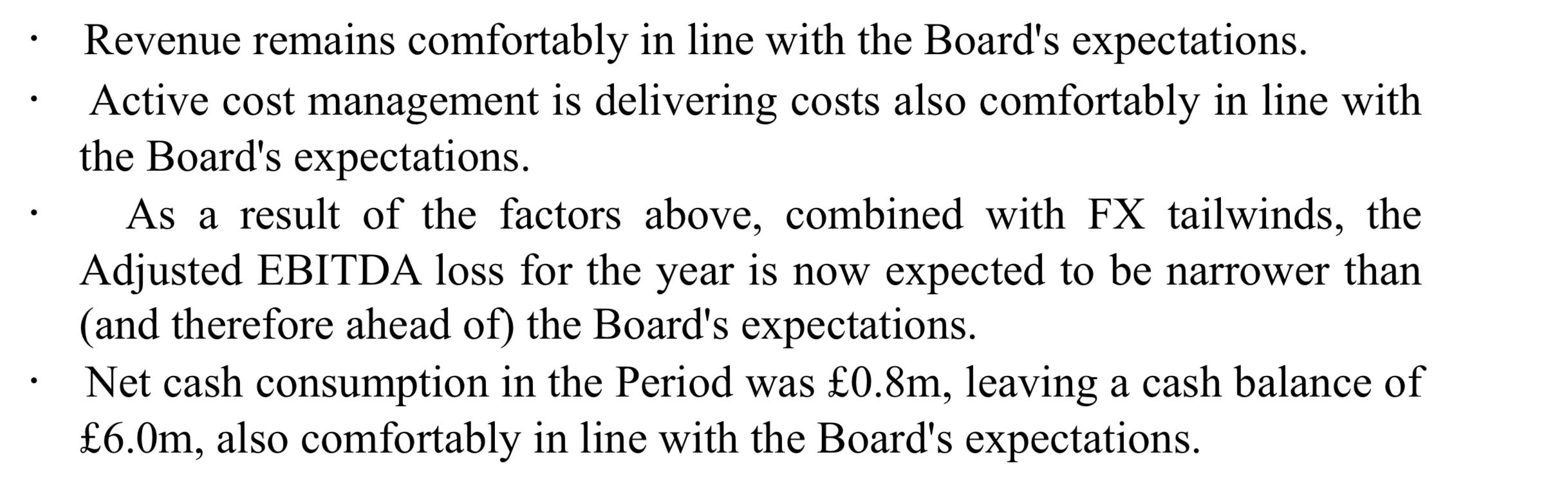

Dillistone Group PLC - Trading Update

The Board is pleased to report that these trends continued through the second half and, as a result, the Group expects to report its first full year of revenue growth since 2016.

Sounds good.

Furthermore, the Board expects 2022 results to be broadly in line with market expectations before acquisition related items and other one-off adjustments.

But in reality, they couldn’t hit expectations despite throwing everything they could into the adjustment bucket. And their massively negative working capital position makes this a lot less reassuring than they might think:

As at 31 January 2023 the Group had £0.697 m in cash.

Cash is similar to the last balance sheet date, and they had a current ratio of just 0.49 then, one of the worst we have seen.

MyCelx (MYX.L) - Trading Update

We follow this company because they have some interesting technology, and after a large property sale, they were a net net for a while. However, ongoing losses mean that financial strength has disappeared, and they really need to grow revenues pretty quickly. So how are they doing:

The Company exceeded previous guidance by achieving 2022 revenue of ca.$10.0 million,

Nice! So profits looking good then?

EBITDA of ca. negative $2.5 million and a net loss of ca.$4.0 million due to an increase in activity in the final month of the year

Oh dear! And surely, if increasing sales lead to bigger losses, then they should stop trying to sell things. At least as a blue sky tech company with ongoing losses they are well capitalised to sustain these losses.

As at 31 December 2022, the Company had cash and cash equivalents of $1.65 million, and the Company continues to manage its working capital in support of future growth.

Oh &?@¥! The big problem is that the market cap is only $8m, so they probably need to raise this much again to survive to sustained profitability. That the shares haven’t sold off this week perhaps reflects extreme illiquidity rather than confidence in the company’s finances!

That’s it for this week, have a great weekend!