Small Caps Live Weekly Summary

Takeovers Mello FA SDG TRI BSE CARD DSG GMS LGRS MAI SLP NUM HSS TUNE

Mark’s latest Value Trapped podcast with Bruce Packard was out this week, so be sure to check this out:

Also, there is a physical Mello in London in May that we will all be attending:

This really is the premier event for individual investors to meet companies, hear great speakers and meet like-minded investors. It is worth prioritising the time to attend in person. Code ML23EB50 will get investors in for half price. Check out organiser David Stredder’s Twitter feed for other offers.

Takeover season is well and truly arrived in the UK markets. And as usual, it is quite hard to predict. For example, we didn’t see Medica being high up the list. If a Private Equity fund pays a 20x P/E, then they need to cut costs and massively leverage the cash flows to get an acceptable return in the current interest rate environment. It perhaps helps that valuations are higher in the private markets than in public markets right now. The assumption is clearly that Medica's cash flows are annuity-like in their stability. Whereas COVID shows that there is always a risk investors haven’t thought about. Cinema chains were considered one of the most stable (and therefore leveraged private-equity-owned) businesses prior to COVID. Medica always had a capital intensity and lack of free cash flow for what is little more than a specialist employment agency. If this gets a Private Equity bid, almost anything could!

FireAngel (FA.L) - Trading Update

Never has a market sin been more rapidly punished! Last week, we wondered if all the bad news was now in for FireAngel and that this would be the start of a turnaround. Instead, this week we got a trading statement that said:

Trading in the year to date is in line with the Board's expectations with two particular exceptions

Or, to put it another way: trading is not in line. Those unfamiliar with FireAngel might think from the wording that the "two particular exceptions" are minor, but of course, they are not. The first is supply chain issues leading to:

restricted or intermittent supply to its end customers.

The company has suffered supply difficulties of one form or another in most years over the last 10, taking a break only to have too much stock and more than once having both shortages and excess at the same time. Perhaps this is all the fault of their "long-term manufacturing partner", which they cited as a strength in last week's announcement, but the buck stops at the board.

The second issue is the failure to win an expected contract award:

Two significant contracts…were originally expected to contribute strongly to Q1 2023. However, only one of them…has been secured to date.

In addition, the previous year’s results have been further delayed from March/April, to "late April" only last week, now to May. One question here is how the miss will affect cash. Normally we would say EBITDA "materially lower" means zero and use this as a proxy for cash, leading to net debt of around £5.3m. This is within claimed facilities of £6.9m at H1, assuming they have enough receivable coverage. However, it is hardly comfortable nor leaves much room for further problems.

On the other hand, if they are lucky/good, then parts shortages will have resulted in a rundown of working capital (inventories especially, but also receivables) and freeing up cash. But knowing FireAngel, it is equally likely to result in a build-up of work-in-progress-inventories which cannot be completed.

Sanderson Design (SDG.L) - Full-Year Results

The share price has had a significant run-up into the results, increasing the risk of disappointment for shareholders. In the event, revenue is a tiny miss and EPS a small beat:

On outlook, they say:

We will continue to deliver our strategy, to control costs carefully and to focus resources on international market opportunities given the ongoing uncertainty in the UK consumer environment.

As we start the current financial year, inflationary pressures on input costs persist but the US market continues to perform well, licensing income has performed strongly and hospitality contract orders are encouraging....The Board's expectations for the year remain unchanged.

Looking at the balance sheet, a further increase in inventory on flat revenue stands out. Some of this will be inflation, but they also say:

We made a strategic investment in best-selling SKUs during the year, resulting in a high quality, year-end inventory of £27.8m (FY2022: £22.7m).

On the analysts’ call, they said that the inventory is the cleanest it has ever been. 10% higher than optimal, with some remaining buffer after supply chain issues, but this is already coming down.

Earlier this month, paid-for research broker Progressive said:

With FY23 results due be published in April, alongside a review of opportunities and prospects for FY24, our forecasts remain unchanged with a view to updating them at that time.

On the evidence so far, it looks like there will be no upgrade, which is perhaps a little disappointing, although the shares still look cheap on the old forecasts.

This week, house broker Singer say:

Adj. PBT came in fractionally shy of our forecast at £12.6m. This was flat YoY in extremely tough global market conditions and included a c£0.7m drag YoY after ceasing trade into Russia. FD EPS increased by 10% to 14.3p, which was ahead of our forecast (SCMe 13.8p) due to a slightly lower tax charge.

So unchanged forecasts for FY 2024, but they have added 2025 forecasts at 13.6p EPS, giving a PE a shade over 10. Equally importantly, they expect FCF to bounce back and stay positive even after dividends. As it was, these results were a disappointment to some, as the share price fell during the day. The nimble may have even been able to take advantage of the rollercoaster of investor emotions here. Selling first thing and buying back at a decent discount.

Trifast (TRI.L) - Trading Update

Marginally ahead of expectations. Although of course, these expectations have been massively reduced during the year:

Expecting 2024 to be better than 2023, but this is also as forecast. This statement should stop the fall tho, as the share price was weak going into this. The shares bounced back to around the 70p level they were in April on this news. However, they are still not obviously cheap on 2024 earnings once you adjust for the debt.

Net debt (before IFRS16) reduced to £38m, within both facility headroom and covenant levels

Investors here have to believe this is just the start of a long-term recovery and 2025 will be better still.

Base Resources (BSE.L) - Q2 Production Report

For night owls, one of the nice things about stocks dual-listed on the ASX is you can read the news before going to bed. Plus, you get a nice pdf formatted table:

Production is lower here in Q3 as mining commenced on North Dune. It sounds like a few teething issues were encountered, but nothing that can’t be solved:

Mined tonnage was lower at 3.3 million tonnes (Mt) (last quarter: 4.5Mt) due to stoppages associated with the move to the North Dune and associated commissioning activities, as well as slower than expected mining rates in the lower ore zones of the North Dune. These ore zones have elevated oversize and slimes and have proven more challenging to mine at the planned rates than anticipated. Options for improving mining rates in these ore zones are being investigated, with the Company optimistic that mining rates will improve in the coming quarter.

The good news is that they say production guidance has not been impacted. Looking at the figures, you can see why - they only have to do slightly better in Q4 to hit the top of the range

Sales for the quarter are higher than production as they had stockpiles to shift:

They have still produced 16.3mt of Ilmenite more than they have sold over the last 5 quarters, so that may be sold in Q4. However, since Ilmenite and Rutile are bulk shipped, then sales can be a little lumpy. The best news is that pricing is surprisingly strong, with positive momentum at the end of the quarter, as they say:

After moderate price declines late in the December quarter and early in the March quarter, ilmenite prices resumed an upward trend in recent weeks generating positive momentum for the June quarter.

They now have $77.2m cash despite paying a $15.6m dividend. So $32.6m of FCF in the quarter despite elevated capex at Kwale. Q4 should be even better due to stronger pricing. This compares favourably with a $150m market cap.

However, there is still no concrete news on Toliara, or Kwale mine life extension. Both of these seem to be taking an age to get over the line and are, of course, key to ongoing profitability here.

Card Factory (CARD.L) - Acquisition of SA Greetings

At H1, they said:

We are continuing to analyse and identify new partnership opportunities with a focus on building the right partnerships to grow the business.

· Completed research and sizing of international opportunities, working with Global Data. From this work we have identified new potential international markets in India and the Middle East.

This week, they bought a South African wholesaler. In FY2022, 1.9% of revenue was from overseas, down from 2.6% the prior year. However, they now claim:

South Africa is one of the target territories for Card Factory's partnership expansion.

Consideration appears to be £2.5m plus £2.7m of debt (derived from gross assets less net assets), an EV/EBITDA of 8.7x.

The acquisition was financed from Card Factory's working capital

That doesn't really make any sense unless the company acquired already owed them the £2.5m. Or perhaps they plan to delay payment to suppliers to the tune of £2.5m to fund it? We think what they mean is it was funded from existing cash resources.

Speaking of which, at H1, they had £8.5m of cash, down from £38.3m a year earlier. There was some repayment of debt, but even without that, there was a heavy cash outflow due to seasonal factors and rent payments not fully included in EBITDA or operating cash flow. They apparently had £30m of debt headroom at H1 and £45m on 31st December 2022.

In view of the level of debt, lease liabilities, and acquisition strategy, this a high-risk investment. Especially, since last year the banks were holding a gun to their head, telling them to raise more equity.

Dillitsone (DSG.L) - Final Results

A strong start? Not really:

Revenue increased by 2% to £5.699m. First revenue growth since 2016.

As you would expect from a company that trumpets its first revenue growth since 2016 of 2% as a highlight, the rest is terrible.

Negative NTAV, and the current ratio has gone from a terrible 0.51 to an appalling 0.41. This may not be quite as bad as it seems since they are a software company, so they get paid upfront and have managed to survive this long. The debt is government-backed CBIL loans which is why the banks have been relatively lenient. It looks like they may be replaced by director loans in the near future. That other lender of last resort.

Realistically, we can’t see a situation where they get themselves financially secure enough to pay a dividend any time soon, potentially making the equity worthless if they never manage to pay one.

Gulf Marine Services (GMS.L) - Final Results

This company has quite a following with private investors since it trades at a big discount to tangible book value. And superficially, a low P/E. However, the reality is that there is a very large debt in the capital structure, and in recent times those assets have been unproductive. The bull case is that increased utilisation and rates rapidly increasing will make these assets productive again, and as the debt is paid down, the share price will approach book value. So how are they getting on with this:

Basically, poorly. For the bull case to pan out, rates need to be double or triple where they are today, and these results show little sign of that kind of growth. Flat profits do them no favours. One bright spot is that debt is coming down since they are depreciating their ships and not buying new ones, so that cash goes to debt holders:

Net bank debt reduced to US$ 315.8 million (2021: US$ 371.3 million). Net leverage ratio reduced to 4.4 times (2021: 5.8 times).

The problem is that they could pay the debt off and be left with rusty hunks of scrap metal. Maintenance capex will need to increase to keep these assets earning, and if they want to grow, they will need to buy new ships. But the current rates don’t make a business case for investing. So neither should equity holders.

Loungers (LGRS.L) - Trading Update

Leo has covered the company in the past, and it is worth continuing to do so, if only as a case study of where the right offering can be successful even in a structurally declining and economically challenged marketplace.

The Group has continued to deliver industry-leading like for like sales growth, up 7.4% on a one-year basis and 17.6% ahead of pre-pandemic levels on a three year basis.

The marked growth of 11.8% in one year like for like sales in H2, whilst partially reflective of the impact of Omicron in the comparative period, also reflects a strong final 12 weeks to the financial year.

These are fantastic figures under the circumstances. And they continue to grow:

During FY23 the Group opened 29 new sites, comprising 24 Lounges, four Cosy Clubs and our first roadside site under our new Brightside brand, taking the portfolio to a total of 222 sites at year end.

Thus:

total revenue for the financial year of £283.5m, up 19.5% on the previous year (FY22: £237.3m)

However, it looks like they have ended up with a small EBITDA miss:

The strength of our sales performance has enabled the business to manage the macro-economic backdrop and accordingly we expect EBITDA for FY23 to be broadly in line with market expectations.

They have been paying down bank debt, but this was tipped into reverse in H1 by the purchase of some freeholds as well as maintaining new site openings. This has never looked cheap, apart from, with hindsight, during COVID, when there was zero visibility on revenue or earnings. Perhaps, all things considered, it is better value today than when it came to the market, though.

Maintel (MAI.L) - Final Results

Adjusted EBITDA is down 54% here. The statutory loss is £4.9m. Which is not a good look for a struggling and highly indebted business. They are keen to point out that:

Recurring revenue increased from 69.2% to 77.0%, due to pandemic having a positive customer effect in accelerating change of technology, with transitioning to cloud services.

But is this really because of a “customer effect” or just because sales collapsed elsewhere? 77% of £91.0m revenue is £70.0m, whereas 69.2% of £103.9m is £71.9m, so recurring revenue has actually declined.

At least net debt is down:

The business significantly reduced year-end net debt[4] to £16.6m, (2021: £19.4m)

But again, is it really? They’ve achieved this by delaying paying suppliers. We’ve commented in the past how they are in a vicious cycle of not being able to get components to be able to complete builds, yet can’t afford to pay suppliers upfront (or even on time) to get priority for delivery. The solution is a large equity raise, but presumably, any pre-raise roadshow didn’t go well as the CEO subsequently fell on his sword. This is what they say about trade payables these results:

The £7.8m increase in Trade payables in the year is predominantly due to delays in receiving certain materials from suppliers which were required for customer installations, in particular switches. The Group has agreements with suppliers to delay payment until the materials are delivered and installed. A payment was made to a key supplier in February 2023 for £4.2m of the outstanding balance, following the receipt of the related materials.

So the delays were planned, but we can’t see suppliers being particularly happy about this arrangement. Net assets declined by £4.1m during the year. And NTAV went from -£32.5 to -£33.6. Given the lack of asset coverage, suppliers appear to be stuck between a rock and a hard place. They either agree to get paid after a long delay, or they put the company into admin and get nothing.

Yet the share price has risen on these results. How bad were shareholders expecting them to be for these to be a beat?!

Sylvania Platinum (SLP.L) - Q3 Results

Some Partridge from Sylvania this morning. EBITDA has halved for the quarter on lower PGM prices, which in itself was down on Q1:

Group EBITDA of $9.8 million (Q2: $20.0 million);

This is some 20% below Mark’s expectations, and it would appear below analysts, too, despite these being downgraded recently.

However, unsurprisingly their headlines focus on:

The SDO delivered 17,926 4E PGM ounces for the quarter, which was ahead of expectations.

Realistically, they have done well in what they can control, which is production, where they have upped their guidance for the year:

…the Company is pleased to increase the annual PGM production guidance to between 72,000 and 74,000 4E PGM ounces for FY2023.

And lower-value production has released working capital:

Group cash balance of $144.2 million (Q2: $123.9 million);

Logically, the market should be aware that the PGM prices dropped and take that into account. However, the share price barely responded to the significant deterioration in the financial outlook caused by weaker commodity pricing this year. The bull case here has always been that it is cheaper than other SA miners. That is no longer the case.

Numis (NUM.L) - Takeover Offer

Mark’s preferred companies in the small cap broker segment have been Numis and finnCap because of their higher proportion of M&A advisory revenue, which has helped offset weak Equity Capital Markets revenue.

Deutsche Bank perhaps feels the same as this week as they have made an all-cash offer for Numis:

The Transaction Value represents:

o a premium of 72 per cent. to the Closing Price of 204 pence per Numis Share on 27 April 2023 (being the last Business Day before this announcement); and

o a premium of 60 per cent. to the volume-weighted average price of 219 pence per Numis Share for the three-month period ended 27 April 2023 (being the last Business Day before this announcement).

That is a pretty decent premium on a share price that hadn’t been particularly weak, given the market backdrop.

Sadly, Mark doesn’t own any. Whereas, finnCap (that he does own) turned down a mooted 20.3p in cash from Panmure Gordon. Instead, they are pursuing an all-share merger with Cenkos, with their share price at an all-time low. It is an illiquid stock, so we have to be careful about drawing too many conclusions based on short-term price action. And the Numis takeover suggests that the market has mispriced the sector versus what industry players are seeing. However, with hindsight, his capital has clearly been in the wrong place in this sector so far.

HSS Hire (HSS.L) - Final Results

Is anyone interested in a company on a P/E of 5.4, with a ROCE of 22.8% and a Leverage Ratio of 0.8x? That’s what shareholders got with this week’s HSS Hire Results:

While they are clearly exposed to the building trade, there have been encouraging in the sector recently, and the outlook looks reasonable for so early in the year:

Current trading and outlook

o Q1 23 revenue growth, EBITDA and EBITA in line with management expectations

o Expanded ProService offer to include building materials through our merchant partner network and equipment sales including small tools

o Capex investment forecast in 2023 is expected to be £34-£38m including c£5m to support further delivery of our technology roadmap

o Management remains confident that full year EBITA will be in line with market expectations

Capex looks in line with the typical £40m D&A, so their free cash flow should remain robust and allow them to pay an increasing dividend.

This just looks too cheap to Mark compared to peers, at least on earnings and free cash flow. The P/TBV is over 3, whereas Speedy Hire is on a discount to TBV (even after accounting for the missing inventories recently announced), but those assets appear to be a lot less productive at the moment in Speedy.

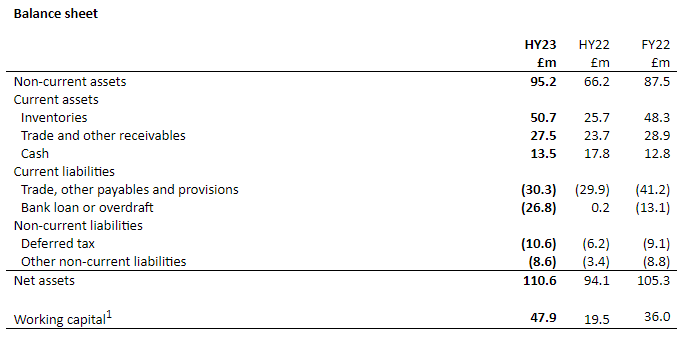

Focusrite (TUNE.L) - Half-Year Results

Although they say...

Trading since the half year has remained solid. The outlook for the Group is positive with inventory in the channel beginning to improve and continued strength in the buoyant live sound market.

…these results look poor, with basic EPS down 38%. Not only this, but the implication of the outlook statement may be that margins will be lower. And gross margins holding up was one of the only bright spots here:

Gross margin at 47.1% (HY22: 46.6%) is 0.5% points higher than HY22 and 3.0% points higher than H2 FY22. Freight costs have reduced significantly, with some of that benefit reinvested in promotions to support sales

Of course, this is daft. Having a sale because revenue is weak is not an "investment". Still, higher GMs, despite some promotions is a good thing.

The big negative cash swing is not great, but it is largely working capital:

We anticipate that the inventory position will remain stable across the second half of the year, but creditors will have normalised by the end of the year enabling the Group to return to historic and more resilient levels of working capital at around 20% of revenue. As is our practice, creditors continue to be paid in a timely manner.

So some benefit going forward, but it looks like inventories are not going to reduce anytime soon. Overall debt is small compared to the market cap, but it doesn't do the valuation any favours. Nor this bit:

We anticipate revenue growth in the second half to be in line with expectations, driven by a number of planned key product introductions alongside elevated costs due to promotions for existing products.

Revenue growth in line isn't the same as saying revenue will be in line for the FY. Saying revenue in line isn't the same as saying PBT in line. Saying PBT in line isn't the same as generating cash to make acquisitions and pay dividends.

Broker consensus for this year has been cut to 40.7p, with 41.9p for the next year. Given the share price has dropped, this is now not that expensive for a quality company with a good long-term track record. The risks are that there are further EPS downgrades to come, and that there appears to be a large seller in the market. If it is Buffetology continuing to sell down to meet redemptions, this could remain a big drag on the price for a long time to come.

That’s it for this week. Have a great weekend!