Small Caps Live Weekly Summary

March SCL Meet, SLP STU JOUL WYN SCS DX.

New SCL Meet - 23rd March

First up, after the success of the last SCL Meet in December, we are planning another one for the afternoon of 23rd March. This will be a free-to-attend event with a couple of relevant presentations and plenty of time to meet other fellow investors, somewhere in the West Midlands with good transport links. Get your registration in here.

Mark will be doing a short presentation at Mello Monday next week called “How to gain an investment edge using public information.” Should be an interesting show.

A calmer week this week in UK small caps. However, US markets have been anything but calm. The single-day moves, up and down, in some of the world’s largest companies, in response to newsflow is unprecedented. Many long-term winners have become losers in 2022, and it has claimed some high profile casualties. Fundsmith, for example, had its worst month ever in January 2022 and may suffer further in February given its Paypal and Meta (Facebook) holdings. It goes to show that even the greatest of investors have challenging periods. And even the greatest of companies will be poor performers if you overpay. In the long run, the price you pay matters more than anything else.

Small Caps

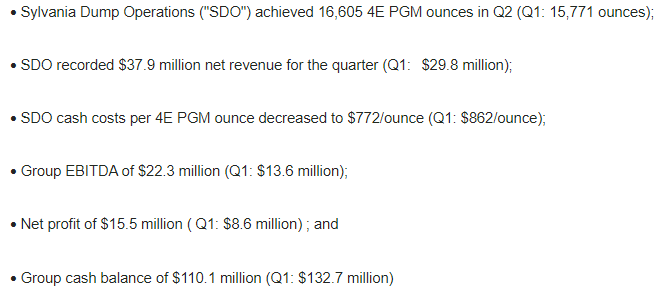

Sylvania Platinum (SLP.L) - Q2 Report

Here are the highlights:

So, plant feed is down slightly, but the grade is up meaning that production ounces are up around 5%. Following the Q1 production Report, Mark commented that their 70koz production target looked a bit of a stretch, and this turned out to be the case, since they now say:

A modest adjustment in PGM production estimate, with 66,000 to 68,000 ounces now targeted by the Company for the full year.

The midpoint of this range still requires production to increase a further 4% in Q3 & Q4 so will require continued operational improvement. PGM pricing has helped this quarter with their average basket price up around 5%. Admin costs are up on the quarter, as are other costs (which you have to infer from the figures given).

The overall result is that EBITDA for the quarter increases quite significantly, although is still below every quarter of last year. While Q1 Free Cash Flow was significant, this is now reversed in Q2. Without changes in working capital, the company should have generated Free Cash Flow of around £16.5m. However, the cash movement was actually $22.6m of outflow. Some $39.1m difference. This is explained as:

The Group cash balance decreased 17% from $132.7 million to $110.1 million during the quarter. Contributing factors to the decrease in cash quarter-on-quarter include the impact of the lower Q1 ounces paid by the smelter in Q2. The Company paid the annual dividend ($14.6 million), provisional income and royalty taxes of ZAR163.3 million ($10.2 million) and ZAR42.6 million ($2.7 million) respectively, during the quarter.

The tax accrued for the quarter is probably around ZAR90m = $5.6m. So this works out to be around a net $17m cash outflow into working capital.

The share price today is this week, presumably on the production forecast cut and the cash outflow for the quarter. But H2 is looking better. If they can hit their revised production forecast and PGM pricing remains similar to today's levels, they should do $45-50m of EBITDA in H2. This puts them on a forward P/E of about 7 and a forward EV/EBITDA of about 2.7. Bulls will point out that this rating looks good value compared to other market sectors.

The problem is that investors have been historically very reluctant to pay a high multiple for these earnings. A P/E of 4 and an EV/EBITDA of 1.5 is a much more common trading range for Sylvania. The Bears will point out that the riskiness of the operations, the heavy reliance on volatile Rhodium pricing, plus the reluctance from the management to do anything with their large cash pile haven’t changed. As such, a de-rating is, perhaps, as likely as a re-rating here.

Studio Retail (STU.L) - Trading Statement

This is one of the biggest small cap fallers this week on this trading statement. At least they lead with the scary bit rather than hiding it further down:

SRG, the digital value retailer, today gives an update on its trading during its peak Q3 trading period, being the 13 weeks to 24th December 2021, in addition to advising it is exploring a range of options to meet a short-term working capital funding requirement.

If you only looked at the trading part of the statement you would have come away with a fairly positive view:

The comparatives with last year are distorted due high street lockdowns consequent to Covid-19. A more appropriate comparison is against the performance two years ago. On this basis, Q3 product sales were up 18%, bringing the total growth against FY20 for the first 39 weeks of the year to +28%.

Then on the outlook:

As a result, our current expectations for Adjusted PBT(1) for the full year are now likely to be in a range of £28m to £30m.

This is below market expectations prior to yesterday's statement, which they helpfully give:

Current market expectations of Adjusted PBT of 35m (FY20: £27.3m, FY21: £48.8m)

But then this was on a very low P/E anyway, so you could consider it was in the price. But here is the sting in the tail:

The industrywide (and acknowledged) supply-chain challenges in calendar 2021 have not only caused higher shipping costs for Studio, but have also led to late-arriving unsold stock of continuity ranges, which will be sold throughout calendar 2022. This has led to a higher level of inventory than normal at this time of the year. This is further compounded by commitments to current and future season stock needing to be made earlier than normal due to ongoing nervousness in supply chains.

This is exactly the issue Mark fears may cause problems for the big faller from last week, IG Design - late-arriving seasonal stock not being able to be sold plus the need to order earlier for next year's seasonal stock adding significant pressure on working capital:

In January, we have identified that these higher levels of good-quality stock, in a market where demand is anticipated to soften, is at a level that creates a surplus stockholding position whilst we sell through the ranges to our customers. We are exploring a range of options to meet the resultant working capital funding requirement, including discussing the current level of our working capital facilities with our long-standing UK lenders.

This doesn't sound great then. The gearing covenant is not exactly high though:

Studio currently has a fully drawn revolving credit facility of £50m and, with a 12-month EBITDA of c.£50m, is well within its key gearing covenant of 1.75x.

Some companies operate with 3.5x gearing covenants, for example. And they are cutting back as much CAPEX as possible:

In addition, we are considering other controllable actions to increase short-term liquidity, alongside steps already taken to manage the pace of some of our medium-term capital investments.

Looking at the last set of results, we see that they sold their education business for £30m in April 2021 and agreed the RCF in June 2021. So to go back to lenders so soon is a tad embarrassing. And, of course, this is a company that is mainly about selling via finance arrangements, so that "core net debt" is after securitisation of their lending book:

Similar to IG Design, this is another company that seems to become undone by its pursuit of revenue over profit. Indeed, Studio explicitly say:

The medium-term ambition is to achieve over £1bn of revenue, through the following three levers for growth: Value, Choice, Payment.

And when that growth involves selling via high-risk consumer finance, that growth can easily stretch finances. The other issue is that there is a cost of living crisis on the way. With basics food prices up some 50% or so, and peoples' energy bills about to soar, then paying for the cheap stuff bought online via financing may be low down the list of priorities.

In light of both the working capital strain and the consumer finance funding, Studio looks massively risky bet, in a way perhaps IG Design isn't, since it doesn't have the consumer credit part of the business. Perhaps the only light at the end of the tunnel is that Mike Ashley’s Frasers has added to its stake again post this announcement. Frasers made a compulsory offer for Studio (under its old name -Findel) back in 2019. Their 161p offer wasn’t particularly generous and was rejected by shareholders. Perhaps shareholders will be more receptive this time? Mike Ashley will be keen not to overpay though, given the tricky situation the company finds itself in.

Joules (JOUL.L) - Trading Update

Continuing the theme of looking at companies struggling to manage their inventory in light of shipping delays, the Joules share price has more than halved this week on the following statement:

Group revenue for the 9 weeks to 30 January 2022 was up 31% against FY21 and 19% against FY20, however, this performance, along with the Group's PBT performance over the same period, is behind the Board's expectations.

Here are the reasons given:

· Weaker than expected revenue in January, in part as a result of the negative impact of the Omicron variant on retail footfall (down 36% vs. the comparable period two years ago) ;

· Delays to new stock arrivals as a result of global supply chain challenges, resulting in a lower full price sales mix, in turn impacting revenue and gross margin;

· Lower than expected wholesale revenue due to delayed stock and customer cancellations;

· The continued impact on gross margin of increases in freight, duties and distribution costs; and

· Continued operational disruption, lower productivity, and higher than expected costs within the third-party operated Distribution Centre (DC). DC costs for December and January were c.£1.2m above expectations, which is more than double compared to the prior year. In the second half of FY22 so far and post peak trading, wage rates have reduced but are still higher than seen in the comparable prior year period.

They are doing all the expected cost-cutting plus:

· Liquidation of aged and slow-moving stock via outlets and third parties;

That's not great, since selling via TK Maxx or similar may impact brand value as well as undercut store sales. The overall impact on sales & profitability doesn't seem too severe:

The Board's base case expectation is for trading for the balance of the year to recover in line with its previously stated expectations, supported by recovering footfall and an improved level of newness in the stock position. The wholesale orderbook for Spring / Summer 22 remains strong and the DC operation is normalising with delivery times back to standard service levels and productivity improved.

Assuming the Board's base case is met, adjusted PBT for the full year is not expected to be less than £5.0m (FY 2021: £6.1m).

Assuming normalised tax rates this would be a Profit After Tax of around £4m and 3.6p EPS. And herein lies the problem, at 60p this is a forward P/E of 17 which means Joules doesn't look cheap even after today's fall. It does make you wonder what those who bought shares at £3 last summer were smoking.

On top of this we have a rather worrying phrase in the trading statement:

The Group is in the process of finalising its Interim Results, including completing its going concern analysis, reflecting the impact of trading performance up to the end of January. The Group intends to release its Interim Results as soon as this is concluded.

It is not normal to mention your going concern statement in a trading statement unless there is a material doubt that your auditors will consider you a going concern without raising fresh equity.

When Mark looked at Joules following their last profit warning he said:

However, given the way that these things work, another profit warning cannot be ruled out, which would further dent confidence and lead to a further de-rating.

Joules is a well-run company and I suspect it will be a potential buy at some point. But it will be when the market hates it, has given up and it trades at a big discount to the sector, not a premium.

Whether this is now hated enough to be good value really depends on how well it can recover in 2023 and how much equity it may have to raise in the meantime. These uncertainties put Joules in the “Too Hard” category at the moment.

Wynnstay (WYN.L) - Final Results

A trading update on 24th November led to a 15% EPS upgrade, but these results are further ahead still, with a 2% revenue beat and a 5% EPS beat. With the trading update issued relatively soon after the period end, some degree of variance is inevitable, but the direction demonstrates forecasts are set conservatively.

There were a couple of acquisitions in the period and the underlying revenue growth was 12% YoY. Gross margins have been uneven over the last few years, dipping in 2019 and being higher than normal in 2020, but have now returned to historical norms. Outside of the cost of sales, the dip in revenue in 2020 was not matched by falls in "manufacturing, distribution and selling" costs, causing them to rise as a percentage of sales, but again this has normalised.

Insensitivity of administrative expenses to revenue levels mean that operating margins were at record levels, translating a 16% YoY increase in revenue to a 35% rise in adjusted EPS. Unadjusted results benefitted from the absence of re-organisation and impairment costs.

However, it is important to understand that there were several one-off factors. Firstly, despite FY 2020 EPS having grown YoY, there were headwinds from weather and covid. Without these FY 2020 EPS would have been significantly better.

And this year has benefitted from higher commodity prices, sharply higher in the case of fertiliser. To quote:

Revenue up 16% to £500.39m (2020: £431.40m), including significant commodity price inflation

outperformance from Glasson, benefiting from three-fold price increase across the market in fertiliser raw material prices in H2

Regarding 2020's year's bad weather, for 2021 they say:

arable activities benefited from a return to more normal harvest tonnages and yields and a good autumn 2021 planting season

There are however some medium-term drivers behind performance:

Specialist Agricultural Merchanting Division...

- excellent performance reflected increased farmer confidence and return to farm investment

But this inflation situation needs some further digging. As we have said on many many occasions, FIFO inventory accounting, as mandated by IFRS, flatters profits when inflation is high. This is artificial and not sustainable - profits will fall back if inflation stops and reverse if prices reverse. That is, some of the profit is due to an increase in the value of goods whilst held in inventory, and not due to fundamental operations. Although profits are flattered, cash flow is not. To maintain the same size of business they must replace inventory at a higher cost. The details are in the notes to the cash flow statement:

That negative decrease in inventories is also known as an "increase". Some of it will be from acquisitions, some of it will be noise, but some of it is from inflation. Netting off receivables and payable movements, most of the poor cash flow in the period is down to this. From the commentary:

The Group generates good operational cash flows although, this year, cash generated from operations was affected by commodity inflation

While it is good that they are open about this, it would have been nice to get it quantified. And Leo disagrees with the phrasing: it is not "cash generated from operations" that was affected by commodity inflation, but "profit and loss".

Looking at the outlook, they say:

The UK agricultural sector is emerging from a prolonged period of uncertainty created by Brexit. However, farmer sentiment has greatly improved and the sector has returned to investment, with the landmark UK Agriculture Act providing clarity over future financial support to farmers. Whilst there is a significant level of general economic uncertainty and rising costs, with farmgate prices remaining strong, prospects for the industry continue to be very encouraging…

Trading in the new financial year has started well, and we view the year ahead with confidence and expect the Group to deliver its ongoing growth objectives.

So that's a pretty strong outlook. So why, even after annualising of acquisitions and a small upgrade, is the adjusted EPS forecast to fall from 45.9p to 41p in FY 2022? Two reasons:

lack of that FIFO tailwind from inflation including 3x on fertiliser

higher corporation tax.

Even factoring out corporation tax, adjusted PBT is forecast to be below 2021 levels in 2023. Extrapolating it looks likely to match it in 2024. So Wynnstay has the same problem many companies have right now, including Vertu and ScS: poor short-term profits growth. And Wynnstay is on a far far higher rating than either ScS or Vertu. Why?

It is likely to be resilient earnings with a low correlation to the economic cycle and consumer in particular. They've been around for a long time and have increased their dividend for 18 years at an average of over 7% compound. This makes it a comfortable hold for the long-term investor wanting steady returns. Every few years the market worries about certain aspects of farming and Wynnstay sells off. These times often represent good buying opportunities to generate above-average returns. Although with the share price close to 5-year highs, now is probably not one of those times.

ScS (SCS.L) - Interim Trading Update

The Group traded well through the important winter sale period and order intake for the first half of the year was in line with the Board's expectations, with one year like-for-like order intake growth of 16.6%.

This is in line with what Leo was expecting for orders from his Trustpilot review analysis. But perhaps most importantly:

Two year like-for-like order intake is in line with that achieved in the pre-pandemic 26 week period to 25 January 2020.

This would be better if we knew whether online was included in LFL numbers or not and what percentage of total revenue it made up:

The Group's online offering and appeal to customers continues to strengthen, with online order growth of 55.8% compared to the equivalent 26 week period to 25 January 2020.

Since there was an online offering two years ago then you could argue it must be in the LFL figures, which are for adjusting out closed / added stores. Online sales are likely to be running at around 16% of the total in Q2.

The Group's order book has grown significantly against previous comparative periods, driven by the ongoing demand and supply chain challenges which have extended product lead times. As at 29 January 2022, the Group's order book is double the size it was at 25 January 2020, at £148.0m.

This is significantly higher than Leo expected, but unfortunately, this is bad news for H1 revenue as they have delivered less than he expected. They could yet make it up in H2, indeed they say:

The Group is working closely with suppliers to mitigate the risk of continued supply chain disruption in the second half of the financial year…

The Board is pleased with the Group's bookings performance to date and it remains on track to meet full year expectations.

They do say they are pleased with bookings. However, they don't say they are pleased with revenue. Also, the update is closer in style to the January 2020 update than the more recent ones. For example, the January 2021 update included a table showing bookings performance over the past 5 weeks broken out as well as the total H1. It also detailed the cash position. This week’s update doesn't even give exact 2020 comparisons.

So we think the risk of a revenue miss for the FY remains, and investors may not be happy when they see the H1 revenue and therefore H2 weighting. However, it is worth emphasising that the order book has the benefit of advertising spend embedded in it. Their "call to action" advertising is effectively a cost of sale and it can be seen to drive orders more than the actual discounts, but is recognised as an admin cost just before the order is made, long before the revenue is recognised. As the broker Shore points out, this has traditionally led to losses in H1 (just ended) and profits in H2, and this is what they expect in the current year.

However, that order book has to normalise at some point, either by catch-up deliveries or lower orders (hopefully associated with lower advertising costs, as in the past). We could be looking at bumper H2 profits, or, failing that, aberrant profits in 2023H1. There are lots of moving parts here but we see profit forecasts as much more secure than revenue.

Plus, if they have a £148m order book i.e. customers’ cash plus about £50m or so of their own cash then we could see a bumper cash balance announced, way in excess of the £80m market cap. We know that isn’t all shareholders cash but the headline numbers could get a few hearts racing.

DX Group (DX.L) - Resignation of NEDs & Auditor

For DX Group, the past month or so has been less Delivered Exactly, and more Lobbed Over The Hedge while ticking Left in Your Safe Space. The company’s shares are, of course, suspended from AIM for failing to file timely accounts after a corporate governance inquiry relating to an internal investigation prevented their publication. The suspension starts a 6-month clock ticking to be delisted completely.

This week saw the resignation of two Non-Executive directors. Although board changes are normal, multiple NEDs resigning at the same time usually means some kind of boardroom bust-up over strategy, or they don't want to be legally responsible for events about to happen. Friday’s RNS confirms that the two NEDs resigning were the ones conducting the investigation:

The Inquiry which, until their resignations as announced on 2 February 2020, was led by Non-executive Directors, Ian Gray and Paul Goodson, has not proceeded as expediently as initially hoped by the Board.

Then losing the auditor too, is a very bad look. It would be tempting at this point to make a jibe along the lines of "If it is Grant Thornton resigning then you really are in trouble". However, in Mark’s opinion, the past criticism of GT has meant that they are maybe now keener than the average auditor to be doing the right thing and seen to be doing the right thing. Here are the concerns that they have given as reasons for resigning:

(i) actual or potential breaches of law and/or regulations by the Company and/or by an entity in the DX (Group) Plc group and/or by employees;

(ii) the performance of the investigation and subsequent corporate governance inquiry referred to by the Company in its announcement on 25 November 2021, and action in response to the evidence generated by that investigation and inquiry;

(iii) the provision of inaccurate information, which in Grant Thornton's view did not give a full picture of the scale and seriousness of the facts referred to in (i) and (ii) above;

and concerns over insufficient access to relevant information and documents, in relation to the matters being investigated by the Company.

The company disagree with these assertions, though:

However, the Board of DX does not consider that the Reasons provided by Grant Thornton accurately reflect the current situation.

Although an alternative way of reading that statement could be that they did consider that they represent the past situation but not the current one!

They are quick to point out that the enquiry doesn't affect their financial position, though:

The Board reiterates that the Inquiry is a corporate governance investigation and, in addition, notes that it is connected to a disciplinary matter. It does not relate to the financial performance or the financial position of the Group, consistent with the trading update released on 2 February 2022.

Here is what they said in that trading update:

Trading over the period was in line with the Board's expectations, despite the tight labour market and customers' supply chain disruptions. Group revenue was approximately 11% ahead of the first half of the previous financial year, and the trading momentum has continued into the third quarter of the financial year.

However, even if this is purely a conduct issue now, then it contains the possibility of becoming a financial one if it continues. Customers and suppliers won't be sleeping soundly when a listed company has been suspended, lost the directors conducting the enquiry and their auditors. So the longer this goes on the more likely it could spill over into trading.

The company is suspended so there is little that investors can do. Although they have net cash, the balance sheet wasn’t the strongest going into these issues due to their working capital position. So perhaps investors should be preparing psychologically for a rescue fundraising, or even worse. It is presumably the chance of the former that keeps finnCap & Liberum in place. Although, finnCap won't want to risk their reputation for doing the right thing purely for a one-off raise. There is a real risk that DX. find themselves minus a NOMAD next, which would start a much shorter 1-month timer for being delisted.

That’s it for this week. Remember to get your SCL Meet Registration in. And have a great weekend!