Small Caps Live Weekly Summary

Semiconductors FA. PRP DX. CMH CAPD RCH

With limited trading hours on Christmas Eve the email is going out early this week. We’ll miss all the ‘bury the bad news’ announcements that traditionally arrive on Christmas Eve, but there is unlikely to be any opportunities worth deep-diving.

Hope everyone has a safe & relaxed Christmas plus a well-earned break from the markets. And always, thanks for reading.

Large Caps Live

Today I (WayneJ) want to dive into semiconductor supply constraints. You will think that it has no direct relevance if you are a UK only investor but I would suggest it impacts eg new car availability and sales of electronics eg via Currys / Dixons / PC World or whatever it is called. So at the far end of the value chain for (silicon) semiconductors is sand - which on last check we have plenty of. Anyway - 'polysilicon' (ie highly refined) is converted to silicon wafers. So the bottom line is you cannot make semiconductors if you don't have wafers. And I am going to suggest to you all that there is a 'corner' occurring in the wafer market.

The definition of Corner in Investopedia is:

In investing or trading, a corner is an act of one entity obtaining a controlling interest of a business, stock, commodity, or other security so that they may manipulate the price. Cornering may happen to a specific security or a market area if an individual or group of people have established a significant degree of control. Another term for cornering is market manipulation. In most instances, cornering and market manipulation are illegal.

Not all corners are illegal and some people would call that an oligopoly in formation. This year I would suggest we have seen several situations of cornering by suppliers – whether passively or actively is an interesting question:

Gas

Oil (?)

Silicon chips

online advertising (has this gone on over a decade?)

As investors, we clearly are interested where a supplier has (to excuse the language) ‘the customers by the balls’. I was having lunch with two friends last week and we were trading war stories during which we turned to silicon wafers which we all used to have an interest in. The conclusion of the lunch, for me, is that silicon wafers are in a ‘corner’.

So who are the big players: - Shin-Estu Chemical - Sumco (= Mitsubishi / Sumitomo Metal Industries) - Global Wafer – which bought MEMC - Siltronic – under bid from Global Wafer – currently bid under investigation by regulators

One thing I found really useful when I used to cover this industry is to look at the reports and investor relations presentations from competitors. And one of the key players whose presentations my friends and I used to look at was Sumco.

Note that Sumco are suggesting customer forecasts are for 8.4% annualised growth:

In particular look at the operating ratio (global) at the bottom of the slide. From 2022 they are forecasting that the market will be short of silicon. Now, this is an industry that has historically been at the prey of customers (ie fabs and foundries) who would overorder and then suddenly cut back. As a result, the silicon wafer producers are very cautious at overinvestment. So as a result they monitor the inventory down the supply chain very carefully:

What I also thought interesting was the discussion on the market environment:

Siltronic is German listed – but as mentioned above – has been bid for by Global Wafer. - Regulatory approvals in Germany / China and Japan are still awaited. They recently presented their Q3 2021 results:

Again we see all fabs loaded and shortages mentioned. Shin-Etsu is a massive Japanese chemicals conglomerate: From its half-year figures we see them talking about shortages persisting.

So far we have talked about silicon wafer suppliers. Let’s turn to foundries. And the biggest beast in the jungle is TSMC. What is interesting for this company is that it also tends to be the leading edge adopter of new geometries – and has overtaken Intel in that regard. Hence eg Nvidia and Apple chips are made (/suspected to be made) at TSMC. Obviously, as geometries get smaller you should be able to put more chips on a wafer (ie higher densities) – but that is offset by higher transistor accounts (which means fewer chips on a wafer).

There are always arguments that an Intel 10nm geometry is equivalent to a TSMC 7nm etc – but whatever the truth I find it stunning that over half of TSMC’s sales are below 10nm. I want to put that in big letters - OVER 50% of TSMC SALES ARE BELOW 10NM - that is stunning. But the key point is their outlook:

And then we have megatrends....

There is a lot more stuff in that transcript but I think I would be comfortable in saying supply is going to be tight until mid-2022 with a knock-on impact to many industries.

Small Caps

FireAngel (FA.L) - Trading and Business Update

This is a company we follow due to historic interest, or perhaps it is car-crash voyeurism, rather than any serious investment opportunity. This week they issued a trading update:

The Company announces that it remains on target to meet market expectations for adjusted loss before tax for the year ending 31 December 2021 ("FY21"), which represents a significant improvement on 2020.

We believe these expectations were set in May after the most recent fundraise and reiterated several times since. This is quite an impressive length of time for FireAngel to go without a profits warning…

However, it expects that the Group's revenue for FY21 is likely to be at the lower end of market expectations.

We can only see two forecasts on Research Tree. Singer from September:

And Shore from May:

So we think they are saying that they will significantly miss the current Singer forecast and non-materially miss the out of date Shore one?

Furthermore, the Company's net debt at 31 December 2021 is expected to be ahead of market expectations.

Which implies they have stretched working capital. But as you can see from the above figures, it is 2022 that really matters.

This resilience reflects the Company's ongoing and extensive efforts to mitigate the impact of COVID-19 and the related global supply chain issues, through continued careful management of costs and price increases.

Should be good news.

The remaining risk to the Company achieving its market expectations for FY21 is from developing COVID-19 related measures in any given country and related shipping variability.

But hold on! There are "remaining risks" to the FY 2021 forecasts from the last 11 days of trading! Clearly, we have underestimated how popular unreliable fire alarms are as Christmas presents. On revenue recognition, you’d expect all of the Christmas sales to have been made to retailers my now and them not to be ordering anything else in the last 10 days. So this is now sounding like a badly disguised profits warning - on target but also:

At the bottom end of forecasts

Dependent on last-minute orders

Dependent on exactly what is happening with COVID from not happening

Its improving financial results are driven in part by the Group's "self-help" gross margin improvement plan which is resulting in improving margins and a stronger control of costs.

This is a bit better and more what we'd hope to hear, even from this serial disappointer: Existing actions helped them not report a massive miss, and by implication, they would have beaten without headwinds.

The adjusted gross margin for FY21 is expected to be in the range of 22% to 24% (2020: 19.8%) depending on precise currency movements.

We'd expect that most of their revenue would have been converted into sterling by now. So either they have a lot of revenue to receive at the last moment, or they are holding a lot of foreign currency, or they are expecting biblical levels of currency volatility on a small amount, or they are just using this as cover for other uncertainties.

The well-documented supply chain issues, as outlined in the Group's unaudited interim results for the six months ended 30 June 2021, which were released on 27 September 2021, have continued to intensify during the second half of 2021, with rising costs and component shortages affecting the Group's ability to build products and increase stock inventory to meet the growing demand for its products.

That sounds like a potential profits warning for 2022.

FireAngel has recently been seeking to forward procure more components than it has historically and will continue to focus on this use of working capital to help mitigate any further impact from these issues.

And that sounds like a cash warning. Also, we should point out that FireAngel has a terrible terrible record of stock control: Buying too much ahead of a factory move and then having to write it off, then being short and having to airfreight some in, and then simultaneously being short of some SKUs and having to write off others.

The Company is pleased to report that its key partnership with a German energy and efficiency service provider for the real estate sector (the "Partner"), details of which were announced on 7 April 2021, continues to progress well.

FireAngel is working with the Partner on a fully funded research and development programme for a new generation smoke alarm which entered the second development phase earlier this month. Phase one of the project was focused on defining the specification for the new generation alarm, mainly for the German market, while phase two aims to develop the new alarm to be available for sale by early 2025.

Meanwhile, the market moves on. Perhaps the best that can be said about this is that they will make some margin on the funded R&D.

In addition, the Group's important project to source certain entry level products, which are uneconomic to design and produce in Europe, from an existing Chinese partner also remains on track.

They previously manufactured in China, but had problems and moved to Poland. Surely at some point, they have to accept that the problem is with FireAngel, not the manufacturers?

Having passed certification, the production pilot is now complete, and the Company remains on target to launch these products as planned. The project is expected to be margin enhancing in FY22.

Prime People (PRP.L) - Delisting

Here's an interesting one Prime People are taking their ball home with them:

The Directors have conducted a comprehensive review of the benefits and disadvantages to the Company and its Shareholders in retaining its quotation on AIM and believe that the Cancellation is in the best interests of the Company and its Shareholders as a whole.

They mention costs, which is the usual reason for delisting plus:

The relatively poor performance of the share price since January 2020 has resulted in a market capitalisation of approximately £8.6 million, which the Directors believe no longer accurately reflects the Company's value. The Directors believe that this under-valuation negatively impacts on customer and supplier engagement.

Not sure we believe this. Being a listed company is often quoted as a reason for winning business, attracting talent and improving a reputation. We suspect they will find things harder as a private company. And, as for costs, these can often be kept very small by companies committed to this endeavour.

The reality for many delisting is that the management or major shareholders see a big potential upside, and want it all for themselves. This is why we often get a tender offer associated with the delisting:

a Tender Offer for up to a maximum of 2,282,628 Ordinary Shares representing approximately 18.78 per cent. of the Company's issued Ordinary Shares at the Tender Price of 87 pence per Ordinary Share.

With the share price trading at about 70p then the premium isn't too bad. However, the strange part is:

You should note that Shareholders holding in aggregate 53.06 per cent. of the issued Ordinary Shares have given Irrevocable Undertakings not to accept the Tender Offer. This means that should you wish to tender the whole or the majority of your shareholding, you can expect to have your tender accepted as to at least 40 per cent. of your current shareholding.

Just seems daft - surely the management doesn't want all these small shareholders trying to use the matched trading function via their nominees or certificating etc.?

With the price still above 70p then shareholders are surely better off selling in the market rather than getting 35p of the tender offer and the hassle of unlisted equity?

DX Group (DX.L) - Strategy Review

An interesting RNS this week from DX. This, of course, is the company that is about to be suspended for not publishing audited accounts on time.

Today's news is:

…the Board is commencing a wider review of the Group's growth strategy and capital allocation policy.

This is led by Liad Meidar who is a non-exec who was recently appointed by Gatemore, and is a managing partner there. So clearly Gatemore are flexing their muscles on this one. However, the review itself isn't exactly inspiring of confidence:

This review will build on the Group's existing investment plans, outlined in its preliminary results announcement made on 8 November 2021, which reported the launch of a three year £20-£25 million capital investment programme and focus on M&A opportunities. The review will consider the Group's total shareholder returns and capital allocation policy, including dividend policy and share-buy backs, and will only be capable of being concluded once the Group has published its 2021 audited Annual Report and Accounts.

This is usually code for a dividend cut. However, in this case, they don't pay a dividend so it is likely to be the forecast dividend that doesn't arrive. Which makes sense, because although the company has net cash, this is only due to a large negative working capital position, which combined with a lack of any real tangible asset backing to the business means that the balance sheet is quite weak.

They do generate about £10m of net operating cash flow pa once you adjust for lease payments, but given the weak balance sheet, it seems unlikely that they can afford £20-25m capital investment and engage in any significant M&A without coming to the market for more cash. But they have picked a poor time to do this with their shares about to be suspended. This is a sector where M&A has historically destroyed shareholder value too.

Still, it would be nice to see them pull this trick off since the fees to their broker finnCap from any acquisition & placing are likely to be significant. The chances of this outcome being beneficial to DX equity holders looks slim though.

Chamberlin (CMH.L) - Half-year Report

In other surprising news this week, Chamberlin report an operating profit:

H1 2021 operational performance significantly improved compared to prior year with the Group delivering a profit after tax for the first time in five years.

This is driven, not by their usual automotive business but their side hustles:

Revenue of £8.0m (H1 2020: £11.0m) reflects loss of revenue attributable to BorgWarner offset by strong growth at Russell Ductile Castings ("RDC") and Petrel, and initial revenues from new business to consumer E-commerce brands - Emba cookware ("Emba") and Iron Foundry Weights ("IFW").

Given the current focus on ESG, and logistics bottlenecks, it makes a lot of sense that heavy items such as cookware & gym weights be made locally, rather than shipped half way around the world.

The problem is that the balance sheet is incredibly weak. The current ratio is just 0.6. They really are being kept going by the suppliers who are getting paid on something like 180-day terms. On top of this, you have long term liabilities, provisions and a pension deficit. They say:

As announced on 16 September 2021, the Company commenced a review of the use of its substantial property assets with the objective of strengthening the balance sheet and improving operational and investment returns from Group resources. This review continues and ensuring that the Group has the necessary resources to deliver on its growth strategy remains a key focus for the Board.

But with just £2.5m of property, plant and equipment, even if this can be sold at a premium to book value, this barely makes a dent in the net liabilities. So despite a very welcome turnaround, the big beneficiaries of this new strategy are Chamberlain's suppliers, banks and pensioners. The equity remains uninvestable for us.

Capital Ltd. (CAPD.L) - Contract Award

The three-year contract will utilise five rigs from the existing fleet, together with the acquisition of one new rig during 2022, to continue provision of blast hole drilling services at the Geita mine…

The key word here is "continue" - this is effectively a contract extension with an expanded scope. How many extra rigs this includes is not determined, but is at least one. The interesting part is that they give the total number of operating rigs:

…bringing the total number of rigs operating on site to 25.

Whereas, in his contract tracking, Mark had just 14 rigs operating for the other Geita contracts from the previous contract extensions & expansion:

The underground contract will utilize nine rigs, including five from the existing fleet together with an additional four new rigs, which have been secured and are currently in transit to the site. The surface delineation contract will utilize the existing fleet of five rigs. Capital has been providing drilling services at the Geita Gold Mine since 2006.

We can't find any historical announcements on the number of rigs allocated to the Blast Hole part of the contracts. But it seems clear that in the last 6 months Capital have added at least 5 rigs into Geita, quietly expanding their operations there. This is typical of their strategy to win core long-term drilling services contracts and gradually expand the scope of their operations.

3-year contracts give good visibility over future revenue. The $33m quoted works out to be an ARPOR of around $150k which is lower than their current average, but these longer-term contracts often have higher gross margins which mean the profitability is similar to shorter-term exploration contracts on higher ARPOR.

Overall, the increase in rigs pushes Mark’s estimate for FY22 number of rigs utilised to around 90, and FY22 EBITDA estimate to around $88m. His mid-case fair value estimate (based on industry average multiples) moves up slightly to around £1.71 per share.

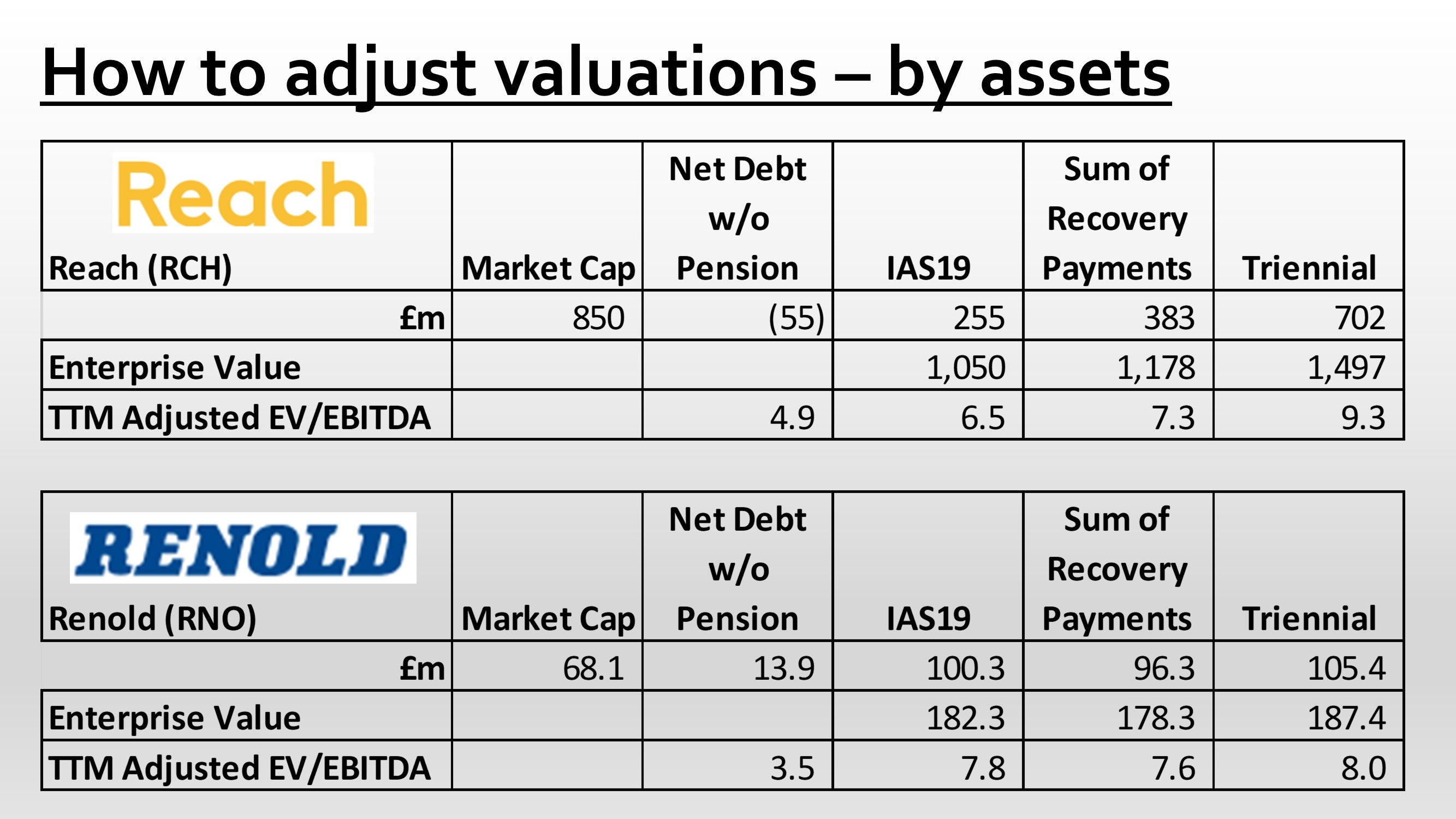

Reach (RCH.L) - Pension Deficit

Mark did a recent Mello Monday talk on Pension Deficits where Reach was one of the examples:

Eagle-eyed followers of Reach will have noted that their current payments are based on a 2016 triennial valuation. While the mathematicians amongst you will have calculated that the next one is as at 2019. A dip into various reports confirms the exact date to be 31st December 2019.

While it is usual for negotiations for triennial reviews to take at least six months and often a year, that was quite a long time ago now. On the 27th July in the interim report Reach commented:

The triennial valuation for funding of the defined benefit pension schemes as at 31 December 2019 would usually be completed by 31 March 2021. We have agreed the funding of the West Ferry Printers Pension Scheme (the 'WF Scheme') and the discussions with the remaining five schemes are ongoing, having been delayed by COVID-19.

Shareholders would have needed to take a view on the credibility of this statement. On the one hand, pension trustees are likely to be on the old side, but on the other hand, most of their compatriots seem to have managed to get to grips with Zoom all too well, and failing to do so would pretty much constitute a dereliction of duty at this stage. On 23th November, they said:

We have yet to reach agreement with regard to the triennial review of our pension commitments but we continue to engage in discussions and remain committed to working towards our objective of achieving funding of all schemes as agreed in our 2016 triennial review.

We didn't cover this at the time, but it does sound a bit more serious. This seems pretty disingenuous given that the Telegraph is reporting this week that the trustees are now involving the pensions regulator following a stalemate in negotiations:

Daily Mirror owner faces action over pension fund deficit

Reach's refusal to make bigger contributions to its retirement scheme leads trustee to seek intervention by the Pensions Regulator

Reach, which as well as the Mirror titles publishes the Express, the Star and dozens of regional newspapers and websites, has hit a stalemate in triennial negotiations with the trustee of its pension fund.

In a letter to scheme members last week, the trustee said it had “requested that The Pension Regulator now take a more active role to try to help reach a positive outcome for all stakeholders”.

This is why Leo subscribes to the national papers: you sometimes pick up some information companies don’t RNS.

The implication of the delay is surely that the Triennial assumptions are showing that Reach needs to pay more than the c.£50m pa they currently do in recovery payments. Otherwise, why would Reach management be happy to string things out with their current agreed annual payments?

Indeed, many argue that a pension deficit is the best kind of debt because it cannot be called, but this kind of thing shows that this is only true to a limited extent. Effectively the trustees will be wanting more of the payments upfront. The trustees are often willing to be understanding in times of business stress, but the flip side is that they want to have a first call on the cash during times when the business is doing well.

In retrospect Reach should have issued new shares to followers of high profile investors at around £4 earlier in the year, and used the cash to pay a lump sum into the pension:

Although the amounts required to remove the liability completely would likely dwarf the current market cap.

The only scheme they have agreed with trustees is the one where they have paid to have an annuity buyout:

As part of the decision to close the Luton print plant the Group reached agreement with the Trustees of the WF Scheme to make additional contributions of £5.0m in 2020 (included in the £53.9m of Group contributions) and a further payment of up to £15.0m by the end of June 2021 to enable the Trustees to purchase a bulk annuity policy which would match the remaining liabilities in the scheme in full. In February 2021 a payment of £9.6m was made and the Trustees purchased the bulk annuity policy. No further contributions are expected to the WF Scheme.

The WF scheme had a Triennial deficit of £6.5m at 31st December 2017 so the £14.6m paid is significantly greater than the last Triennial assessment. Applying a similar premium to the remaining £692m deficit shows why a quick resolution is not possible. And Reach are going to have to end up paying annual contributions of whatever the Pension Regulator steps in to determine.

That’s all folks. Happy Christmas!