Small Caps Live Weekly Summary

GLE MPAC PAY VNET

Here’s a selection of what we looked at this week.

(Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.) To avoid spam, the only way for new members to join the Discord server is via the Small Caps Live website. This will be instead of direct invites via Discord. All genuine investors are still very welcome to join in the discussions.

MJ Gleeson (GLE.L) - Update on Gleeson Land

It seems that teh company can’t get its land deals over the line by the end of the financial year. If it’s only a question of delays, it’s potentially a profit warning that doesn’t really matter. The market certainly appears to have mostly shrugged it off. However, they say

There is no doubt that housebuilders, in the south of England, are reviewing and reappraising their land buying strategies and we anticipate these conditions will continue through the next financial year.

It is possible that these deals will never be completed, or the price will be negotiated down. Their broker Cavendish confuse matters further by saying:

While this pushes earnings into FY27E, we leave FY27E and FY28E forecasts unchanged, consistent with broader market conditions and peer commentary around land buying.

It sounds like they are saying that even if the land deals are completed in 2027, it will only cover the profits that would have been missed in 2027.

This update sounds a lot like the reverse of the recent Henry Boot one: its housebuilder part is doing ok, but it can’t complete its land sales! Perhaps they should merge and be mediocre at everything!

Overall, though, this probably isn’t their fault. Many in the sector are trying to sell their land bank to shore up their balance sheets, and mostly finding no buyers. Those with cash are clearly stalling as they know they will get much better deals in 6 months, or they can simply complete at the point that interest rates fall or demand returns to the sector.

Bellway is usually one of the most aggressive, and they are also talking cautiously this week:

Land investment has remained disciplined and highly selective...In response, we are maintaining a sharp focus on the monetisation of our well-invested land bank and work-in-progress position through FY26 and beyond to support improvements in asset turn and cash generation.

The book value of many of these companies is providing support, but when a lot of that value is tied up in land, it certainly doesn’t appear realisable at the moment.

Mpac (MPAC.L) - Trading Update & Sale of Mpac Lambert

The Group continues to focus on maintaining appropriate liquidity and covenant headroom. This position will be materially improved by the proceeds from the sale of Lambert.

It seems the liquidity situation was far worse than we imagined. This is why they are having liquidity issues:

Since 21 April 2026, trading margins have continued to be impacted by delays in customer decision making on capital investments, heightened competitive pricing pressure, and lower operational leverage arising from reduced OE volumes. Accordingly, the Board now expects first half margins to be below the prior year, and FY 2026 underlying profit before tax to be substantially below current market expectations on a like-for-like basis.

A 43% cut in EPS by their broker, Panmure Liberum, is certainly “substantial”! This is despite removing the Lambert losses.

In light of this, the 15% drop in share price in response looks far too small. The Lambert sale does buy them some time, but on the current rating, this was not priced to go bust, which is still a possibility.

However, the sale of Lambert was clearly flagged in previous comments, but also by the move of HQ from Tadcaster back to Coventry. While we are not sure the strategic reasons for the sale make much sense, £20m for a loss-making company with only £2.1m of assets seems like a good deal. But haven’t exactly covered themselves in glory by buying this for £15m in 2019. Inflation means they have lost money.

Despite the cut, it is tempting to think that this is reasonable value on about 10x forward EPS, but this ignores the still sizable debt pile, no tangible asset backing and a current ratio of 0.9, even after the sale, which means there is still little in the way of downside protection.

Is it really a bargain, as buyers this week seem to think? Larger competitors can be bought on similar multiples with a good track record, net cash, a much better gross margin, and a much more diversified business. Where’s the discount to buy a low-quality microcap?

On top of this, the company often makes quite a few adjustments to get to their EPS figures. We are doubtful whether this is worth 10x real earnings if it were debt-free, let alone 10x adjusted earnings with debt.

Paypoint (PAY.L) - Record profits…

They seem to have mixed up the RNS title with the byline. The title should be “Results for the year ended 31 March 2026”. Also, profits are down in real terms, with sub-inflation rises. Only the combination of buybacks paid out of a 35-40% increase in debt drives EPS forward.

We get confirmation that Collect+ is now ex-growth with the number of sites falling, parcels little better than flat and revenue down 4.9%. Looks like them selling half was the right move.

However, the new structure demonstrates where the growth is now:

PayPoint are at the heart of efforts to break the Visa / Mastercard tyranny:

In Open Banking, we have made further progress in executing our strategy and leveraging our extensive capabilities. In PayPoint, we are focused on winning business with both new and existing clients delivering Open Banking services and payments channels, all enabled by obconnect and Aperidata, with 26 new client services live in the year, including the Department for Work and Pensions, AccessPay, Gousto and the Insolvency Service for Confirmation of Payee. ... In addition, as a founding member of the UK Payments Initiative, PayPoint is closely involved in the rollout of account‑to‑account (A2A) payments in the UK, including exploring how these services can be made available in‑store to support inclusive access for all customers.

If all goes well, Digital Payments & Open Banking will go from the smallest to the most significant segment in five years. Network Services revenue is already effectively £8m less than stated due to 49% disposal of Collect+, and at current shrink / growth rates, it will be overtaken in about 5 years.

We’re not sure what their business model for open payments is, but suspect there is some transaction fee element. While the point of Open Banking is to simplify the payment chain, reduce costs and remove the network effects that created the current duopoly, potentially this could get very interesting from a PayPoint investor perspective as well as for retailers and consumers.

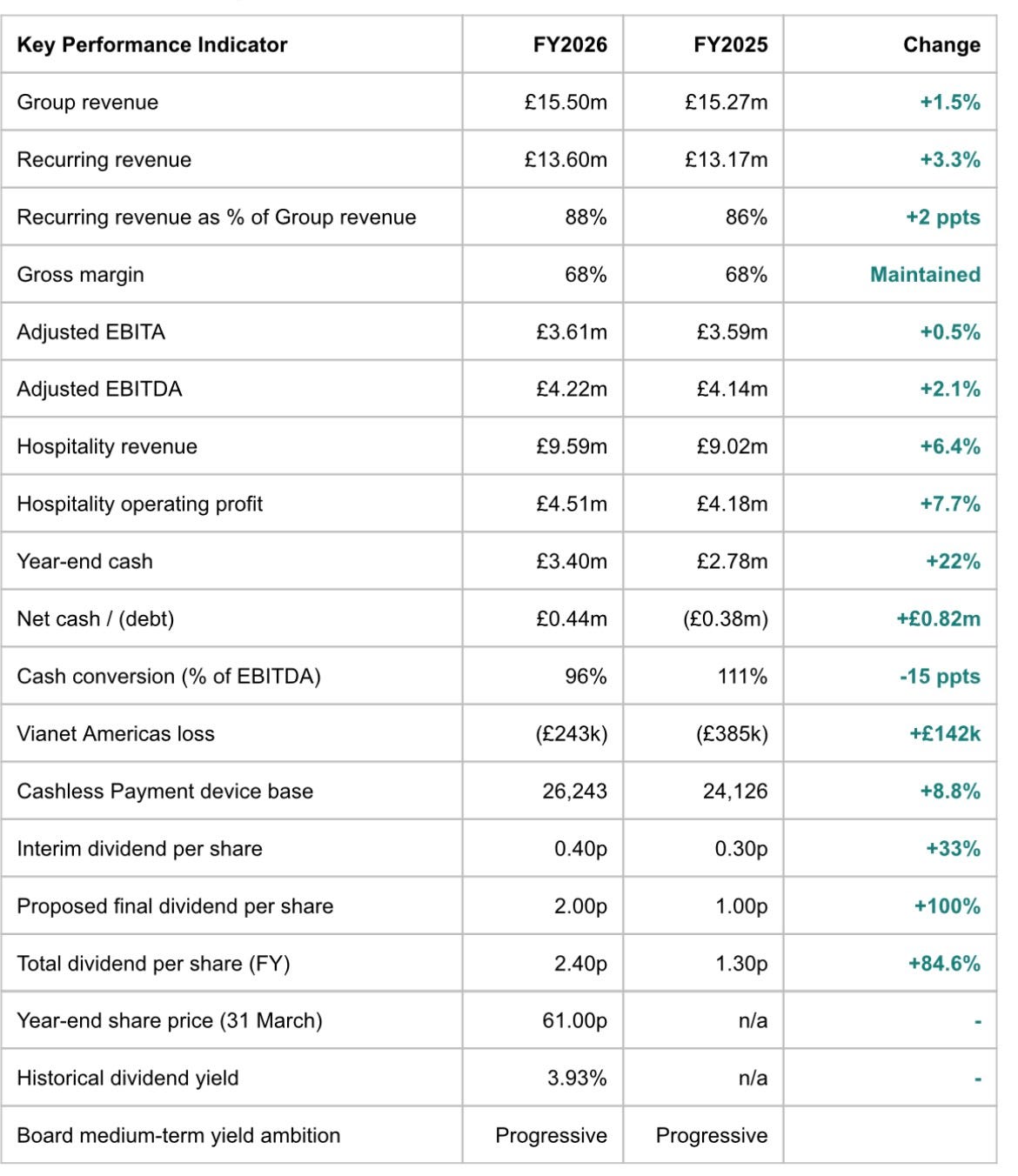

Vianet (VNET.L) - Final Results

A big summary table on Page 1 is normally a good thing. However, in this case, it's full of BS metrics. No EPS or PBT. Which are, of course, both down:

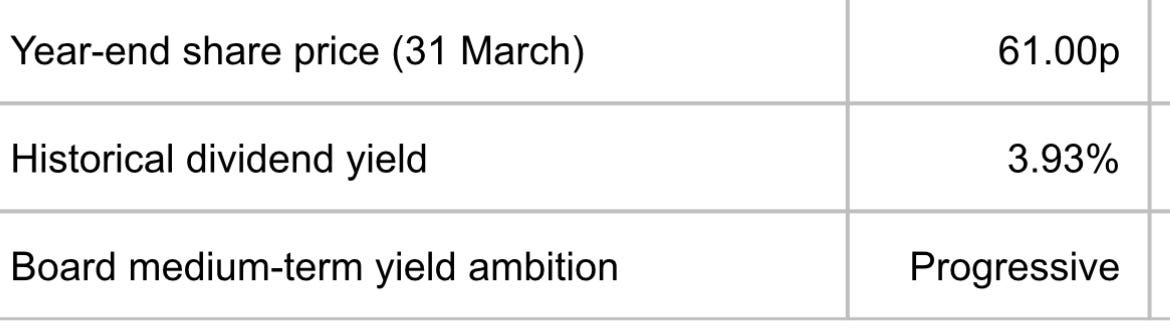

It's odd how they include the share price, but exclude the figure from last year. Perhaps, because it is flat.

We wonder whether they have only paid LSEG for one additional colour in the RNS, so they can pick only the metrics that have improved and leave out the ones that haven’t, to get an all-green table. Whatever the reason, Vianet appear committed to taking Partridgism to the next level.

On the plus side, they do appear to understand that their share price is only heading down by having a progressive yield expectation:

Because yield is obviously dividend over share price, a “progressive ambition” can be achieved with a declining share price, not just a rising payout.

These are supposed to be final results, but don't yet include a segment results table. Extracting the numbers from the narrative, it appears revenue is down in the vending machines division, despite all the talk of opportunity.

So we have a business with a poor track record that is on an Adj. PE of 20.8 (trailing) and a forward PE of 18.8. Normally, we like owner-operated businesses, but with a track record like this, we hope Mr Dickson gives his new CEO a free hand.

That’s it for this week. Have a great weekend!