Small Caps Live Weekly Summary

Share Picking Competitions SDG FCAP HTG K3C FUL

Another quieter week on SCL, WayneJ was recovering from an injury, and Mark discovered that some new things take up a lot more time than you expect:

As you can see, he is already a big fan of Sanderson Design Group!

Share Competitions

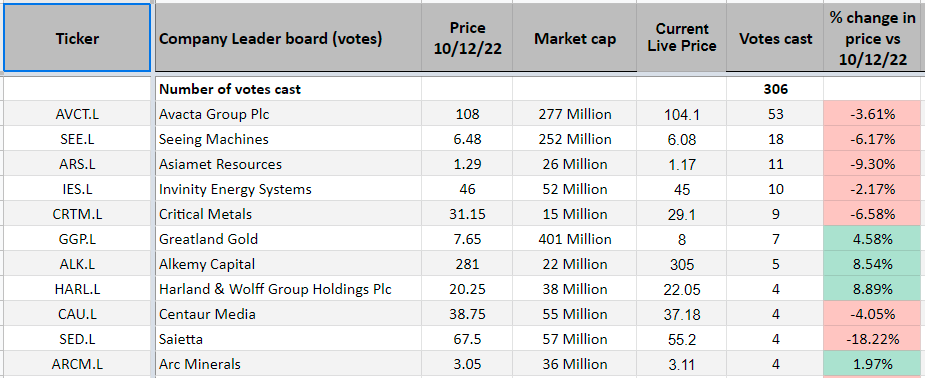

At this time of year, lots of people are running share competitions, such as this from Paul Hill:

Unfortunately, these normally end up a set of the worst possible stocks to invest in. Sometimes this is due to the structure of the competition. Normally, you need to choose something incredibly high risk that will multibag or be a zero to stand any chance of winning. However, this is different. There is no prize. So investors are incentivised to pick stocks they really believe in, and hold in size.

Paul points out that last year's list didn't perform any worse than AIM or the NASDAQ, on average, which seems reasonable. However, this is not a good measure of performance. If we picked 265 stocks at random and equal-weighted them, then it wouldn’t be unusual to track an index. The real test is how the most popular picks performed

Basically, terribly. If we take the top 25 stocks, all with ten or more picks they returned a 52% loss so far this year. Given that these are likly to be conviction holdings, many of these investors will have lost far more this year.

So it is worth paying attention to the most popular picks on these lists; they are almost certainly the ones to avoid next year. Here is where the avoid list looks like today:

Small Caps

finnCap (FCAP.L) - Interim Results

o finnCap Capital Markets revenue £9.3m (H122: £15.6m)

o finnCap Cavendish revenue £7.1m (H121: £16.1m) in line with 5 year average HY level

Both main parts of the business have seen revenue down on much tougher market conditions. One of the strengths of the finnCap business versus listed competitors recently has been the M&A part of the business, so it is a little bit disappointing that that has completely reverted to long-term averages. They end up with a small loss, unsurprising given market conditions:

o Adjusted PBT(1) of £(0.6)m (H1 22: Adjusted PBT of £7.2m); PBT of £(2.6)m (H1 22: PBT£6.3m)

o Adjusted basic EPS:(1) (0.30)p (H1 22: 3.54p); Basic EPS: (1.82)p (H1 22: 2.96p)

They say:

Controlling our costs

o Significant reduction in fixed cost base implemented from September 2022

o FY24 fixed cost base substantially reduced to c.£28m from c.£31.5m H123 run rate(2)

o Reduced discretionary spend and headcount reduction without impacting client service levels

o Marketing of surplus office space under way, further savings identified

However, we can’t help feeling they let these get out of control. Some of it is not their fault. For example, a new office building shortly before COVID hit and made flexible working the norm. However, they clearly mistook the 2021 boom times as more normal rather than a time of excess. (To be fair, we didn’t see how quickly sentiment would turn in the small cap markets either.) The average headcount is down slightly versus 31st March but up 19% on the last half year. They also spent £1.4m on fees related to their acquisition by Panmure Gordon, which was aborted. This seems excessive.

These factors are largely known, though, and the key unknown here is the outlook, and this doesn’t seem too bad:

Relative to H1, Q3 has begun well with the ECM team closing a number of equity fund raisings, including for Xeros Technologies and Surface Transforms, the completion of the acquisition of Attraqt PLC and private M&A transactions including the sale of Peach Pubs. Our pipeline of private M&A transactions remains good and we currently have over 36 mandates signed and in various stages of execution.

So perhaps we are past the nadir of trading and with a reduced cost base this will be profitable going forward. There are hints of this too, where they say that no interim dividend will be paid, but they will consider a FY dividend.

Despite the failure of the Panmure deal, M&A should be the game here as it does seem to be generally accepted that there are too many subscale operators for the current conditions. The problem is that in the current markets, acquirers may be looking at P/TBV rather than full-cycle earnings. And here, finnCap trades at a premium to peers. In the past, this has been worth paying up for, given the strength of finnCap Cavendish and the very long-term track record of the business under Sam Smith. With Smith no longer at the helm, the new CEO has a lot to prove.

Hunting (HTG.L) - Year-End Trading Update

They report 2022 in line, but 2023 management estimates increase by about 10% due to a strong order book:

upgraded EBITDA for 2023 from $80m to $85m—$90m.

However, this is still way off the level they delivered in 2018 & 2019:

Underlying EBITDA $139.7m (2018 - $142.3m)

Their broker, Arden, points to the US$500m order book, much of which falls in 2023, as underpinning financial expectations, but they maintain their 2023 EBITDA forecast behind company guidance, which seems strange. Previously they were at $70m versus $80m and now increase this 17% to $82m versus $85-$90m guidance.

However, with the DA part of EBITDA relatively fixed and "I" falling on higher cash, accounting profits increased 37% on this update giving EPS of 15.9p. Therefore on a PE of 18x, this remains a play on a more full recovery than currently forecast, albeit Arden is behind the consensus. They remain on a P/TBV of 0.9, so if those assets can be made productive again, there remains potential upside, although it is arriving more slowly than when oil prices were at this level in the past. This oil cycle is potentially much slower because of the lack of access to debt for drillers. But our understanding is that much of their kit is consumable, so the peak demand matters much less than the total demand.

As always, the bull and bear cases come down to whether investors believe this is a normal but slower oil cycle or whether the shift to renewables means that demand for oil field services is now in permanent decline.

K3 Capital (K3C.L) - Recommended Cash Acquisition

This was rumoured last week and the talks were confirmed by the company so this should come as little surprise.

For each K3 Share held 350 pence in cash

It seems many shareholders feel a little aggrieved at the premium paid:

a premium of approximately 16.7 per cent. to the Closing Price per K3 Share of 300 pence on 7 December 2022 (being the last Business Day prior to the commencement of the Offer Period);

However, the price had been rising on rumours. And they point out that it is:

a premium of 52.2 per cent. to the Closing Price of 230 pence per K3 Share on 13 September 2022, being the last Business Day before Sun and K3 commenced discussions about a possible offer by Sun for K3

And:

an implied enterprise value of 13.1 times FY22 adjusted EBITDA

Plus, they are flagging that the recent very strong trading conditions may not last:

Whilst being confident on the outlook for K3, we are mindful of the weakening macroeconomic environment in the UK and the pressures that this is likely to put on UK SMEs over the medium term and, therefore, it is the Independent Directors view that this offer represents an opportunity for shareholders to realise their entire investment, in cash, at an attractive valuation.

Mark agrees with the independent directors on this one. 13x adjusted EBITDA seems a very full price for a largely people business that has faced exceptionally strong market conditions recently, which are now abating.

It is via a scheme of arrangement, so it needs 75% acceptance. However, given that they have been in discussions with Sun since September, the chance of a higher competing offer seems very slim. With the price of £3.44 to buy, there doesn’t seem to be much of a merger arb either. Given the warning on outlook, if the bid was not accepted, the price would surely lose all of the takeover and rumour premia and be back below £2.50. For this reason, it looks like a done deal.

Fulham Shore (FUL) - Half-year Report

As with many companies at the moment, we turn to the outlook first:

Trading during the first two months of the second half of the financial year was well ahead of the comparable periods in 2019 and 2021, at 46% and 12% respectively.

They also waffle:

Furthermore, the Franco Manca loyalty programme continues to grow in user numbers with 350,000 users and over 50,000 loyalty pizzas enjoyed by our loyal customers.

And even this sounds OK, making it sound like a mere continuation of H1 trends:

Notwithstanding this momentum, the Board remains mindful that we continue to operate against an unstable political and economic backdrop, which in turn has impacted consumer confidence and driven up our costs as well as facing significant challenges from the ongoing transportation disruption.

But they are being negatively affected by reduced central London occupancy figures, which have been made even worse by the rail strikes, so they now say:

Due to these challenges, the Company expects that trade in the final quarter of the current financial year is likely to be behind any of the Group's first three quarters.

In some ways, that is to be expected given that Christmas falls in Q3, but the new year lull in Q4. But in any case, this is a multi-year profits and revenue warning:

given the pressures outlined above, the Board believes that it would be imprudent to aim to maintain this opening frequency in the next financial year

That means total restaurants will probably never catch up with earlier plans. Their broker, Singer, reduce EBITDA by 23% for the current year, which probably implies a loss in Q4.

Frankly, we find this impossible to value at the moment, but FWIW, Singer have slashed their target price from 24p to 15p on this update, which rather makes us think they were behind the curve on this one.

Zytronic (ZYT.L) - Final Results

So, Gaming & Vending are going great guns, but Financial dropped off a cliff. Overall they managed impressive growth in EPS and dividends:

§ Basic earnings per share increased by 87% to 5.6p (2021: 3.0p)

§ Proposed final dividend of 2.2p (2021: 1.5p), a 47% increase on the prior year

But this is off a small base, and they are not obviously cheap on earnings. However, the EPS should grow again due to the weighted share count effect, and they have 45% of the market cap in cash. The outlook is a bit weaker than we expected, though:

Whilst supply chain issues persist equally for Zytronic and its customer markets, and average order intake for the first two months is running at a level similar to the second half of the prior year, we are encouraged by the full return of our key face to face global business development and marketing. These activities provide the basis for progress, as we continue to accelerate the rebuilding of the opportunities pipeline.

However, the pipeline is £59m vs £28m this time last year, and the dividend increase indicates confidence too. The slowish first two months of trading doesn’t diminish that.

They have a very long sales cycle, though, since they have to be designed into customer products, and if customers can’t get chips, those revenues are deferred. If you’d asked Mark in early 2021, he’d have said that Zytronic was almost certain to be doing 20p+ EPS this year due to business bounce back, but many factors mean we will be way below that. 20p EPS still looks possible eventually, but only for the very patient investor.

CentralNic (CNIC.L) - Leadership Change

This is another red flag for this business that appears to have transitioned from a nice sticky domain-name business to producing auto-generated websites that make the internet worse for users:

…the appointment of Michael Riedl, currently Group CFO, as Group CEO with immediate effect. Michael succeeds Ben Crawford, who retires from the board today.

We could see no hint of this change when we watched the recent Investor Meet Company presentation. But if the quote that the now-CEO opened with on IMC is an indication, he very much sees himself as the Nelson Mandela of the auto-generated marketing website world! Perhaps today is the culmination of his long walk to freedom.

That’s all for this week, have a great weekend!