Small Caps Live Weekly Summary

Mark Minervini's loss aversion, LSXMA ACRL BSE SUP ZYT TGP DRV SMRT

One of the most memorable events this week was the appearance of well-known trader Mark Minervini on CNBC. Minervini was describing some recent successful trades, but when the interviewer asked what one of the companies did, this appeared to flummox Minervini:

We’ve all been there, caught out by a bad position. And as a trader, Minervini should have known what to do: take the loss. Indeed, Minervini tweets regularly about the importance of stop losses. If he’d simply said, “I don’t know, but as a trader, I don’t need to know to make money”, then that would have been it.

However, Minervini’s loss aversion kicked in, and he appeared to fake technical problems to avoid the question, which opened him up to the internet’s ridicule. And then to further questions such as, if his trading record was as good as he claimed, why would he still be trying to sell trading services to the general public, or why he appeared to be still using a stock photo taken decades ago?

At this point, Minervini had another decision to make. If he’d simply laughed it off, then that would have been it. However, again, his loss aversion kicked in, and in order to “take on the trolls”, he began a series of tweets that gave the appearance of a man having a major mid-life crisis. The moral of the story is, when things go wrong, always take the first loss.

If you think this story of escalating loss aversion is bad, wait until you hear this account from one of Mark’s investment talks:

And if you want to do a better job of overcoming loss aversion than Minervini did, pick up a copy of Mark’s book.

Large Caps Live Monday 18th October

I was intrigued by LSXMA as proposed by the Sunday Ideas Brunch Substack. The story here is that this is a Liberty holding co for Sirius XM (SIRI) and LiveNation (LYV – note that the substack has the ticker as LVY which is wrong).

Historically John Malone has various listed vehicles which hold stakes in other media companies. The key point, to me of the idea brunch substack is that he is moving towards 80% control of SIRI which then makes the tax position for upstreaming dividends more attractive.

I have been reading on Seeking Alpha a variety of articles on LSXMA and frankly, I think it is a lot more complex than a brief summary. Hence I would recommend anyone considering doing the trade to do their own homework.

John Malone is a past master at pulling rabbits out of hats and shuffling his deck of cards to benefit himself / his partners. There is a massive following of Malone in the value investor community however as he had generated a lot of wealth for himself and investors. So I am going to be measured in what I say:

(1) It does make sense that Malone may want 80% of SIRI to upstream cashflows / dividends

(2) The current sum of parts suggests that LSXMA is trading at a discount to its sum of parts of around 30%+

(3) The creeping control of SIRI means that the 80% threshold will occur probably in a limited time span. Back of an envelope, I think 2 years rather than the more bullish one-year estimates of some people

(4) The other way to look at this is that you get exposure to LiveNation for free. So I started also looking at LiveNation....

Looking at LiveNation I think one sees one of the most sensitive businesses to Covid recovery:

With a current market cap of £16bn LiveNation has a valuation that assumes a very dramatic recovery post Covid!

This is the bit of the story re LSXMA that I am a bit lost on currently. The sum of parts argument only really holds if you believe that in 2022 that Live Nation will be a $12.6bn revenue business.

So my conclusion is that:

(1) A lot of people like subscription businesses – especially in media post the success of Netflix

(2) Sirius Radio has been around for years; is a US-specific business but reflects the size of the country. I suspect that for investors in the US, who know the issues with long-distance driving, at some point SIRI looked like an ‘inevitable’.

(3) It generates great cashflow but I am not sure about the projected earnings bounce:

(4) I am obviously UK based and so used to the UK DAB network – I do not know if there is an equivalent in the US

(5) But more frequently I find that I am listening to previously downloaded podcasts from my phone (bluetoothed to the radio).

(6) Nevertheless it seems to me that at 18.9x PE for SIRI, with a discount for LSXMA there is a risk-reward trade here.

(7) I do think I need to do more research, especially given this:

Is the Google trend suggesting that Siri interest is drifting? On the other hand, fuel consumption/prices suggest that people in the US and elsewhere are driving more than ever?

(8) On the LiveNation side I think that there will be a bounce in concert / live show attendance as we unwind from Covid. However, I am not entirely sure how long it will last. But I would speculate that next year there are likely to be a lot of stadiums/concert venues filled and people will pay premiums.

---

So I don't know if anyone on LCL plays US stocks or sum of parts/event trades but LSXMA looks interesting but I feel is more complex than first meets the eye and one really needs to have a view on the future path of Livenation and Sirius.

Small Caps Live Wednesday 20th October

Accrol Group (ACRL.L) - Trading Update

In line with the wider market, pressures on the Group's raw material supply chains have been considerable with further tightening in recent weeks. Pulp and parent reel production costs have been impacted across the world by energy cost increases, input shortages, and general inflationary pressures. Whilst the Group's supply chain has shown significant resilience and supply shortages have been managed, considerable cost increases had to be absorbed in the short term. In addition, distribution pressures, notably the availability of HGV drivers, which served to increase costs further, have restricted revenue growth in FY22.

So, it shouldn't be a surprise that this sort of company producing bulky, close to commodity products is struggling at the moment. However, this has been a surprise to investors with the stock down 15% according to stockopedia.

These cost increases are successfully being passed on, albeit there will be a time lag in passing on the full impact, resulting in earnings in FY22 being lower than previously expected. Overall, operational efficiencies and integration synergies, together with the successful passing on of cost increases, will enable the Group to deliver FY22 percentage EBITDA1 margins in line with those achieved in FY21.

So being almost commodity means they can pass on the cost increases, but this takes time.

A big broker downgrade following this trading statement means that they look quite expensive, at least in the near term:

There would appear to be much better risk-reward opportunities than a near commodity producer in the current climate.

Base Resources (BSE.L) - Quarterly Production Report

This week we got a production update from Base Resources. These show production down slightly as they moved mining blocks but up on the September quarter the previous year:

Sales look disappointing, and if you do the maths then about 46.6kt of material seems to be unaccounted for. Mark asked the company about this and the reason is that they haven't mentioned stockpiles at the port, which after a small delay, will be shipped in the December Quarter. This is reiterated in the following management interview.

Production guidance is re-iterated and we can expect their sales to roughly match production over the year.

One of the advantages of being the commodity supplier, not the near commodity processor, as long as demand outstrips supply, which it does at current pricing. This is what the Proactive article has to say on pricing:

Zircon prices for the company’s September quarter contracts increased by about US$150 a tonne from the June quarter and prices agreed for the company’s December quarter contracts have increased by an additional US$600 a tonne, it said.

The average price for Zircon in the previous year was just short of $1300/t, so a $600/t move is a big percentage going forward.

So although this quarter is a little disappointing on the headlines, the delayed sales hitting the next quarter plus the potential for some big price increases could see some very large free cash flow from this company going forward.

Indeed, Mark has updated his 2022 FCF estimates from around $100m to c$140m following these price rises. This still compares favourably to a $225m market cap despite a short mine life in Kenya.

Supreme (SUP.L) - Trading Statement

We’ve not looked at this recent float before. Supreme seem to be even more entrepreneurial than UPGS, whom we often mention, but have also gone down the vertical integration via manufacturing route. This seems to have given them some protection against rising shipping costs, although of course they still need the raw materials.

This is a short trading statement, so let’s go through it in full:

The Board is pleased with the strong performance of the Group in the first half of the financial year and remains confident in achieving expectations for the full year.

Clearly good news, but no upgrade. The last update was 20th July and in some ways, this update is in lieu of the absent AGM update on the 30th of September.

Positive momentum in the Vaping division has continued alongside particularly strong growth in the Sports Nutrition and Wellness category.

As we've said before, Vaping has significant regulatory risks, as we have seen in the US. While vapes that taste of cigarettes are mostly for the cigarette substitution market, there is plenty of evidence that sweet fruit flavours and menthol attract virgins. It is also a strange juxtaposition to Sports Nutrition and Wellness.

Lighting has benefitted from some brought forward sales in addition to the expected organic growth and Batteries continues to be a defensive and predictable profit contributor for the Group.

This appears to be early evidence that distributors and retailers are stocking up early ahead of Christmas. Perhaps light bulbs aren't the most traditional of Christmas gifts, but it is certainly something you don't want to be running out of due to shipping delays.

As manufacturing in Supreme's key vaping and sports nutrition categories is in-house, the Group has been relatively unaffected by global supply chain issues affecting other areas of the economy.

Note that vaping is now "key". I think they talked in detail about the sourcing and manufacture of these products in a recent video. IIRC, disposable vape products are still filled in China from UK made "juice", but the majority of their sales here are refills.

In addition, active management in the Group's Batteries and Lighting divisions has also largely insulated Supreme from these issues.

Presumably, this involves some ordering early into speculative stock, some booking of ships early and some communication with customers to get them to order early too. I imagine there will be some working capital hit from this.

Management remain cognisant of supply chain and labour constraints but are confident of being able to manage these risks in-line with the growth the Group is delivering.

Leo won't invest in Supreme while vaping is a significant product line, but these comments bode very well for UPGS as they also are very good at managing things where it is possible to do so.

Supreme's working capital that their year-end is 31st March which is likely to be just after peak cash for them following Christmas. H1 end is likely to be lower as they bring in stock and November worse still. So worth having a look at the admissions document to see if there are any half-yearly results and disappointing they didn't state cash which could be under pressure.

Integration of Sci-Mx and Vendek was completed in the period and both are progressing well and management remain confident in the prospects for these businesses.

Honestly don't know what those are (see how easy that is Mark Minervini ;-) but sounds good.

Overall, group margins have been particularly strong with significant year-on-year growth in profitability. Whilst it is too early to draw conclusions about the full year, the Board is pleased with the performance of the Group and looks ahead with confidence.

Margin growth, which is again positive for Supreme and UPGS.

UPGS look better value in terms of lower P/E & higher forecast growth although they still trade above historical norms on rating. Supreme are more entrepreneurial and probably more aggressive than UPGS, giving a higher upside. Of course, Supreme being a new issue adds to the risk. UPGS had a massive wobble post listing and without a track record, was really punished for it. Hopefully, the same won’t befall Supreme.

Small Caps Live Friday 22nd October

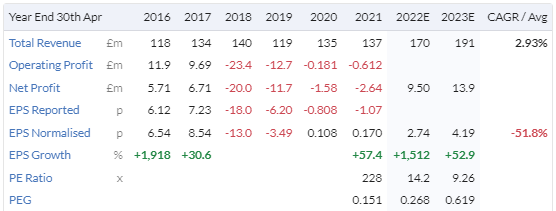

Zytronic (ZYT.L) – Trading Update

We last talked about this just over a month ago when they issued the following trading statement. Which caused a jump in the share price at the time, when they said:

We are pleased to report the continuation of an improvement in sales during the second half, currently running at more than 30% ahead of the first half, which has enabled a faster return to profitability and reversal of the first half loss.

This showed how low the expectations here were since this was actually below what Mark was assuming. Since this time, the share price had sold off somewhat, presumably on supply chain concerns. After all, they do rely on electronic components and export a lot of their products. Though the signs were good on revenue, as their Twitter feed showed a contract win, hiring of production operatives and a software engineer, plus being nominated for industry awards. (For companies who report infrequently, then a Twitter follow can be a good source of scuttlebutt.)

So in today's statement, comments on supply chain & margins would be key. On supply chain, they say:

Although the business continues to see COVID-19 related effects, both nationally and internationally, and particularly related to electronic component supply issues across our full range of touch controllers, we are pleased to announce a considerable turnaround and a return to profitability since the half year ended 31 March 2021.

So not exactly no effect, but the fact that the gross margins have increased by so much shows how that volume and production efficiency:

The improvement in trading in the second half of the financial year compared to the first half was significant, with sales increasing by 44% to £6.9m from £4.8m and gross margins increasing by six percentage points to 33.2%.

GM's are back close to FY19 levels, although that is a year they faced some challenges, and there is still some way to go to reach the 40%+ GM's of 2015-2018. On H2 profitability, they say:

EBITDA for the second half is expected to be around £1.3m

This significantly exceeds my expectations, both driven by the gross margins, but since it is unlikely they have made any savings in distribution costs, this implies that Admin costs have been managed downwards too, Zytronic is emerging from COVID as a much leaner machine.Perhaps the most pleasing part is this:

The improvement in trading since 31 March 2021 has also contributed positively to the net cash position which has increased by £1.4m since that date to £9.2m at 30 September 2021.

A lot of the positive cash flow during COVID was due to the unwind of working capital. And while this gave them the ability to make cost savings and do a tender offer, Mark was fully expecting cash to decline going forward as working capital increased again. To generate £1.4m cash from £1.3m EBITDA while revenue increased 44% means that working capital was very well managed and CAPEX restrained. Expecting this to remain low going forward into strong growth is perhaps overly optimistic. We will see the levers of this cash flow in action with results soon:

We expect to announce the results for the year ended 30 September 2021 in the week commencing 6 December 2021.

After the last trading statement, house broker N+1 Singer said:

We upgrade our forecasts accordingly in this note and will review forecasts in more detail in due course. Over the medium term, the recovery opportunity looks very attractive, given that Group PBT in the last full year pre-pandemic was >£3m.

And Mark commented:

I don't see why they won't be back to £3-4m FCF pa in time and a £3-4 share price.

Obviously, the faster they get back to such levels the better the returns, but I still see a potential valuation gap between what the market is pricing and what the eventual outcome will be.

With today's trading statement, that return appears to have been accelerated.

Tekmar (TGP.L) – Trading Update

The structure of today's update is interesting. They start with a "Strategic Update". Often this can be a way of diverting attention from the recent past and near future. They did similar in their last results. Although here we suspected that they had promised this to be released earlier and felt forced to put something in the results since they hadn't delivered it yet.

The Group continues to make encouraging progress in delivering on the plans to support the strategic ambition to double organic revenue growth over the next five years, and to deliver a sustainable mid-to high teen EBITDA margin in the later years of the five-year plan. Recent highlights supporting our strategic execution include:

We are not sure we’d call these "plans", more "aspirations". With the best will in the world, they can't plan what their revenues or margins will be in 5 years. (As an aside, Creightons use the term "aspiration" for their projections, and not "promises", whatever some Twitter commentators may say!)

Anyway, here are those highlights:

· contract award with Van Oord to supply Tekmar's Cable Protection System ("CPS") for the Baltic Eagle offshore wind farm in the Baltic Sea, Germany

· partnership agreement with DeepWater Buoyancy announced in August 2021, which supports Tekmar's ambition for the global floating wind market and the US fixed offshore wind market

· contract award from EPC contractor to design, build and supply an Emergency Pipeline Repair System for a subsea project in Qatar

· contract award from EPC contractor to manufacture and supply concrete mattresses for a subsea project in the UK

· various contract awards in support of Offshore Wind Operations and Maintenance projects.

We think these have already all been announced, but no monetary amounts have been given as far as we can see.

This activity has helped to support growth in the current enquiry book to £359 million, an increase of 31% on that reported on 1 June 2021 of £273 million, in addition to an increase in preferred bidder tenders from £4.5 million to £10.4 million in the same period.

Enquiry book? Not really the same as an order book is it? We can't help imagining that if the order book was good they'd tell us what it is.

Without any prior knowledge of the company, you'd expect current trading to be pretty good, with catch-up revenues following (albeit inexplicable) covid delays earlier in the year.

As has been widely experienced in many sectors, the dislocation to global trade flows has impacted Tekmar's operations including challenges with shipping goods for delivery, supply chain constraints and cost control pressures.

Yes, well everybody knew about those already, the lead times are very long and the margins very high, so surely this can't be that big a hit?

These headwinds impacted Tekmar's financial performance, particularly through cost pressure and reduced volume, such that the Company expects to report revenue of £46 million and an adjusted EBITDA loss in the region of £1.2 million for the extended financial period to 30 September 2021.

Reduced volume sounds like they failed to deliver stuff. That's hardly going to be popular with electricity from wind farms sold before they are built. And yes, they changed their accounting year. Rarely a good sign.

The Board expects the profitability from the size and nature of contract mix to improve in the current financial year to September 2022, albeit the financial impact of continued disruption to global trade remains harder to quantify at this time.

If "aspirations" are described as "plans" then presumably "hopes" have become "expectations" here?

Cash balance at the period end to 30 September 2021 was £3.5 million. The Group has extended its CBILs facility of £3.0 million for a further 12 months to October 2022 and has also worked with its relationship bank Barclays, together with UK Export Finance, to introduce an additional trade loan facility of £4.0 million, which is available at least to November 2022.

Quoting a cash balance without a net cash figure leaves a lot open to guesswork too. The assumption has to be that they have fully drawn down the trade loan, so they have £7m debt and £3.5m cash = £3.5m net debt. Also, we are not sure how far £3.5m of cash will go towards funding the working capital of the magnitude "strategic plans", especially as customers have been traditionally very slow at paying.

Plus, customers can't pay until they have been billed and historically this company had a large proportion of unbilled revenue in its receivables. Supply chain delays will hardly help with working capital either, with weak companies like Tekmar having to pay up in advance for supplies that might take months to arrive.

The summary doesn't say much, although this caught our eye:

We remain very energised about the opportunities we have ahead which is further reinforced by the recent pledge of £9.7 billion announced earlier this week at the Global Investment Summit in sectors including wind energy. The industry is at a major inflection point in terms of significant acceleration in offshore wind capacity investment. This combined with the broader energy transition aligned with the net zero by 2050 imperative and our initiatives to deepen and extend our capability across energy projects' life cycles provide clear drivers for sustained future growth.

Confusion/conflation between a massively growing wind energy market and Tekmar's ability to profit from it should provide some support for the share price, but has not been enough to stop it from falling 73% since IPO. This company is so bad that even Downing sold out after further investigation. But at maybe £25m EV, maybe it has some value as an acquisition for a large wind turbine supplier?

They are in a market that is growing strongly and at least used to have a high market share, and in a product that is a small part of a big overall project cost. If they sort out the balance sheet (via placing?) and can return to growth then they could be a good investment. They are far too risky in the short term though, and there will be plenty of time to get aboard if a turnaround starts to occur.

Driver Group (DRV.L) – Trading Update

We got a trading update from Driver group yesterday:

The Board can confirm that it expects to report underlying* PBT for the financial year in line with market forecasts and a healthy net cash position at 30 September 2021 of £6.5m.

Pretty short and sweet. Usefully, both N+1 Singer and Equity Development have the same forecasts as each other, so the consensus is for £2m PBT before share-based payments. This means H2 is similar to H1 in performance, which is not exactly earth-shattering. The momentum seems to be (finally) building here though:

…the overall result masks a material improvement in activity levels and in underlying* PBT during Q4, as a result of which Driver Group enters the new financial year with renewed positive momentum.

The trading statement was set to coincide with a management call, organised by Equity Development yesterday, which revealed a few further details:

Management are comfortable with ED forecasts of 4.7p EPS for 2022.

Asia Pacific exceeded expectations after the loss of a team in Singapore earlier in the year, they added several key personnel and are swamped with enquiries.

No other key losses of staff.

£4-5m was the minimum cash balance during the period.

Buybacks, not ruled out when things are more certain.

One of the key questions Mark asked was around how big a business can this be. The answer was that the previous move to a greater scale but low margin. However, in the last few years they have had a revised strategy: growing the core business, margin not revenue.

The CEO, Mark Wheeler, said that in 3 years’ time it won’t be two times larger in revenue but will be a fair bit bigger and margins potentially much higher. This lack of a significant sales runway won’t appeal to everyone, but they are positioning it to be the market leader & much more profitable.

Given that this is on a 9x cash-adjusted 2022E P/E with the potential for earnings to grow significantly in the next few years then this still looks much too cheap, despite the people business risk. The only real negative for Mark is that he would prefer them to be much more aggressive on buybacks while the stock is trading cheaply. Bringing in a buyback at say £1+/share if it becomes clear that covid is behind us and they are delivering high margin work at a high utilisation rate will be too late to add significant shareholder value.

Smartspace Software (SMRT.L) – Trading Update

Gordon Jones and Alan Charlton did a great presentation on one of the Mello Mondays about how this company was re-inventing itself. Basically, the previous business failed and so they switched model.

Leo was never quite convinced because his research showed their products an also-ran in a crowded market, and that locations were growing linearly rather than exponentially.

It took some time but a few months after the presentation it did indeed take off. However, by the time we reviewed its last trading statement in August 2021, then location growth was decelerating and ARPU growth looked less than impressive given that the number of locations per user had increased. Leo commented that:

Indeed, this looks like it could get quite nasty from a share price perspective, especially if they need to raise more money.

Which seems quite prescient:

Today we get a further trading update

In advance of the Company's Interim Results Statement which will be announced on Tuesday 26 October, the Board provides the following update on current trading.

Financial Highlights:

· Annual recurring revenue ("ARR") up 53% year on year to £3.78m at 31 July 2021 (FY21 H1: £2.46m). This momentum has continued in to H2 with ARR of £4.11m as at 30 September

On the face of it, these are fabulous growth rates, far in excess of what Leo thought was achievable back in December.

Gross margin on continuing operations continued to improve to 71% (FY21 H1: 51%), reflecting an increased mix of higher margin SaaS revenues, in-line with stated strategy

Also great news.

In the Mello presentation, Gordon and Alan made a big thing about ARPU and how the management had massively grown this in a previous company. Again Leo was doubtful this could be repeated here, but for their main product, SwipedOn:

Monthly average revenue per user ("ARPU") increased by 32% year on year to £56 at 31 July (FY21 H1: £43) and has advanced further to £61 at 30 September

However, our concern continues to be that they are failing to reach critical mindshare. To do this they need to quickly grow customers, not just revenues. Here things are very disappointing:

wipedOn locations increased to 7,061 at 30 September (FY21: 6,741) with customer numbers at 4,747 (FY21: 4,735) as SwipedOn targets higher value, multi-location customers

As you can see, something apparently went badly wrong and/or a wall was hit last Autumn:

Clearly, on a customer basis, things are even worse.

The question with subscale high margin, high growth companies is: When will profitability breakthrough occur and will it happen before the growth runs out?

Revenue for the year ended 31 January 2022 now expected to be not less than £5.2m (FY2021: £4.6m) with an adjusted EBITDA loss of not more than £2.7m (FY21 adjusted EBITDA loss: £2.1m)

The Group had net cash of £3.25m as at 20 October 2021 (31 July 2021: £3.37m)

Using EBITDA as a best-case approximation of cash flow it appears they are still cashflow negative and might not get through another year at this rate. Software development costs were down in FY 2021 (Jan 31st), but still £0.7m. Cash on 31st July was £3.4m. It was £4.5m on 31st January. The cash hasn't dropped much but with that EBITDA loss then there has to be significant working capital flows making up the difference.

But here's the obviously bad bit of the statement:

In particular, the Board had expected sales of Naso to accelerate in the autumn, however this has not been reflected in September sales or initial indications for October. Whilst Evoko remains optimistic regarding the future sales trajectory of Naso, the Board has decided to adopt a more cautious stance surrounding the Company's own forecasts, in light of a more gradual return to the office, as a result of the ongoing challenges of Covid-19.

So that's a profits warning. (already reflected in the figures above).

In Leo’s analysis, he only considered the SwipedOn product as Space Connect is not material and growth rates from such a low base are not meaningful. He certainly didn't consider sales of the Evoko Naso product. So problems with Naso don’t worry him.

We are worried that they may need to raise more cash at a disadvantageous price. So are not surprised they are down 20% today. It is still worth watching though, the story has been proven completely wrong yet.

Right, that’s it for this week. Thanks for reading this far. Have a great weekend!