Small Caps Live Weekly Summary

Value Trapped Podcast, Discord Improvements, CAPD MWE NWOR TGP TRMR

Mark has a new podcast out called Value Trapped with his friend Bruce Packard. The aim is to have a fairly irreverent monthly chat about topics and companies that will be of interest to the typical UK investor. Check out the first episode here, or on your favourite podcast app.

Leo has been beavering away behind the scenes on discord, creating a bot that automatically posts a summary of important regulatory news into individual company threads. If you follow a thread, you should get notifications on discord. His aim is to add reminders of company presentations and also track when companies are featured on a few key sites. This should make the SCL discord server the go-to place for tracking and discussing important company news.

Small Caps

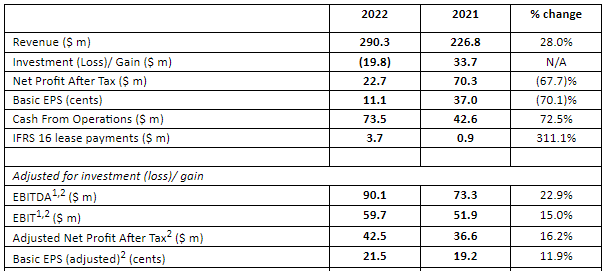

Capital Limited (CAPD.L) - Preliminary Results

Revenue was known here, but EBITDA appears to be a small beat versus Tamesis Partners’ $86.1m:

Adjusted EPS at 21.5c is an 11% beat versus the Stockopedia consensus, and there is a small beat on the dividend too. The outlook is positive too, with revenue guidance higher than Tamesis’ previous estimates of $319m:

Revenue guidance for 2023 of $320 to $340 million driven an improved contract portfolio, contract extensions and expansions from existing long-term contracts, the Sukari load & haul contract continuing at steady state and MSALABS continuing to grow through 2023;

So why did the initial increase in the share price get sold into, and the shares finish down on the day? Partly this may be because the company has developed a reputation for never responding to good news. But we think there are a couple of concerns market participants may have.

The first is the lack of operational gearing. The increases get less as we go down the income statement. Admin expenses, depreciation and finance charges have all increased faster then revenue:

Higher depreciation is due to the bigger fleet. The increase in admin expenses is particularly worrying, but we missed this on the first reading:

Part of the increase is bad debt and credit loss provision. The bad debt was described on the management call as a drill-for-equity where they decided the results were not promising, so they declined to continue drilling and didn’t receive equity. Expected credit loss is not ideal, but management describes this as a one-off.

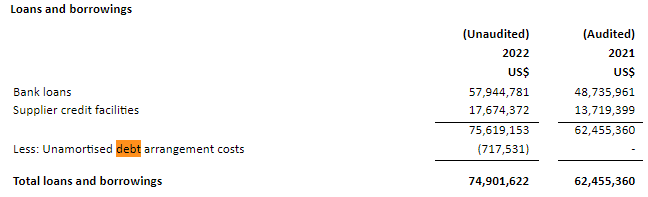

The interest costs reflect higher cost of debt and the increase in debt:

Which brings us to the second concern, which is that they show no slowdown in their capex plans:

Capital expenditure is expected to be $50-60 million in 2023. This will fund a more than typical replacement of the drilling fleet to ensure ongoing youth and productivity, the expansion of MSALABS, including a number of commercial labs, as well as sustaining capex on the enlarged drill fleet and the Sukari mining contract;

On the call, they said that about $10m of this was going into MSALABS for new lab facilities, but the rest is largely rig maintenance or renewal. The debt here is less than 1xEBITDA, so isn’t a worry from a solvency point of view. However, they are paying 10% interest rates. And we don’t believe this guidance includes any mining services contract wins. Of which, they seem pretty confident that they should be awarded at least one in the near future. On the plus side, the $25m of working capital build in 2022 is expected to reverse in 2023.

The company seems to be well aware the cycle will turn at some point, and while there appears to be no sign of this in the short term, they have been pursuing long-term contracts with inbuilt inflation clauses rather than taking higher rate short-term exploration contracts. Although one could argue that they are spending $50m to renew rigs to generate an additional $40m of revenue. That doesn’t sound like a great trade. The second risk is that they fail to spot the turn and keep investing into the downturn. However, this is an experienced management who have a good track record of acting countercyclically.

Anyway, at least one institutional holder doesn’t like the strategy expressed in these results since the share price has been weak since on some fairly chunky sales. However, it seems strange to be selling a growing company on a P/E of 5, trading at less than tangible book value, even if they are unconvinced that now is the time for large investments. At the end of the day, capex can be turned off pretty rapidly, and their suite of long-term contracts will throw off cash for at least the next three years, if not much longer.

MTI Wireless Edge (MWE.L) - Final Results

MTI say that:

MTI is a growth business operating in growth markets. Our products and services are in good demand across all three divisions. We continue to invest in innovation, product development and new companies when the opportunities arise, whilst always remaining focused on radio frequency communications which lies at the heart of our success.

Yet these results read differently:

· Delivered revenue growth of 7% to US$46.3m (2021: US$43.2m)

· A 12% increase in adjusted EBITDA to US$6.06m (2021: US$5.4m), helped by the economies of scale from the increasing size of the Group

· Profit from operations increased 4% to US$4.59m (2021: US$4.42m), including some one off costs related to the acquisition of PSK

· Net profit growth of 4% to US$3.85m (2021: US$3.7m)

· Earnings per share increased by 3% to 4.21 US cents (2021: 4.07 US cents)

So revenue growth, at best, is in line with inflation. EPS is only up 3%. Some of this will be their withdrawal from Russia, but then they also have a small acquisition made in this period. So, in reality, this is a 14xP/E for a company not growing.

The story is always good here, Water Management, 5G aerials - but they are on a c.30% gross margin, so this doesn't exactly scream competitive advantage. There's a 5% dividend yield, and they seem keen to keep buying back shares, although £200k is small beer. This appears to be another case of buybacks occurring at inflated prices to prevent management blushes on underlying performance.

National World (NWOR.L) - Results for the year ended 31 December 2022

National World continues to show the strength of its management compared to peers:

Continuing strong digital revenue bucked the trend compared with some peers in January and February with a 9% year on year increase matched by audience growth of 9%. This is before the benefit of acquired Scoopdragon and Newschain sites which are expected to add over 10% audience improvement.

But they are not immune to market conditions, at least on the revenue side:

Despite total revenue being down 9% year on year, due to economic conditions, we have met our EBITDA target for January and February. Trading is expected to remain challenging for the first half. However, management continues to innovate to address the headwinds faced across the industry, including revenue initiatives, while transitioning to a digital only operational model providing customers with quality and original content across all genres and platforms. The Group maintains its performance expectations for the year.

These are the forecasts:

So 2.5p EPS for this year. That is a P/E is more like 5, cash adjusted, since they have £27m cash. This makes them still cheaper than larger peer Reach on an EV-basis, despite the share price falls there. And unlike many cash-rich companies, they will use it to drive growth, which will not be in current forecasts. We see little reason to buy Reach when National World is cheaper and outperforming them.

Tekmar (TGP.L) - Final Results

They report the 18 months to 30th September this week, five and a half months later. That is a sizeable red flag in itself.

Statutory financial statements for 2021 have been delivered to the Registrar of Companies and those for 2022 will be delivered in due course. The auditors reported on those accounts; their reports were unqualified and did not contain a statement under either Section 498(2) or Section 498(3) of the Companies Act 2006. For the year ended 30 September 2022 and period to 30 September 2021 their report contains a material uncertainty in respect of going concern without modifying their report.

On the good news side, there is an operating cash inflow this year due to a reduction in trade and other receivables.

Over 30 days remain notably high, and the suspicion is that some (or possibly even most) are over a year. As we've seen elsewhere, statements like:

Trade and other receivables are all current and any fair value difference is not material.

...cannot be used to infer that the NPV of receivables is not lower than the book value due to an extended term.

Unfortunately, an improvement in receivables of this size is unlikely to be repeated. Given that underlying cash flow, EBITDA and profits are all heavily negative, cash should remain a concern. However, given that these results are now ancient history, what about the outlook?

We remain cautious, however, in the near-term on the likely lead times for project awards and starts in the offshore wind market and we expect this is likely to suppress the volume required to restore profitability for the current financial year.

We also recognise that it will take some time for improved contractual and commercial discipline to impact financial results, as the impact of existing legacy contracts diminishes over time.

Taking these factors into account, and anticipated business mix for the current financial year, the Board's expectation is for the business to break even at an Adjusted EBITDA level for the current financial year.

Well half of that year has already gone!

This is based on expected revenue for the current financial year to be in the region of £40m, of which approximately 70% is already secured. The Board expects the business to generate positive Adjusted EBITDA in FY24.

On liquidity, the net current ratio looks pretty good. The main concern here is how much of the current "trade and other receivables" are really current. Looking at note 6 from above, a conservative view would be that most of the "over 30 days" and "contract assets" are not, but that still leaves current assets > liabilities. We think investor madness for anything tech and green had a big part to play in destroying profitability here, but perhaps this has changed, and they can make money.

In this case, the balance sheet becomes relevant. Removing goodwill and £3m of receivables still leaves £15m net assets. The market cap is £7m. So perhaps now is the time to buy?

The trouble is that the debt facilities previously appeared insufficient to continue to break even, let alone take on large new contracts. This must also be affecting customer confidence. As a result, they are in a formal sales process. As a reminder, this has 14 days left to conclude an equity raise that would be "at or around the share price at the time exclusivity was granted in November 2022", i.e. around 9.25p. But things certainly look better with fresh eyes than we expected here.

Tremor (TRMR.L) - Response to Speculation

This is the speculation:

Adtech group Tremor screens interest from potential bidders

However, this is not new news. These stories run every time the share price takes a dip due to poor trading. Here’s the one from December 2022.

Sources said that Tremor's board, chaired by Chris Stibbs, had asked bankers at Goldman Sachs to review its options and evaluate a fair price for a formal offer.

We wouldn’t rule out the board themselves leaking the story to Sky. The story spiked the share price by 14%, but when the response to speculation came, it lost all of these gains:

The Board of Tremor notes the recent press speculation and confirms that it is in discussions with Goldman Sachs as an ongoing financial adviser. However, the Company also confirms that it is not currently in a sale process.

The only thing it appears to have done is make the company pay more for the shares it bought back on the day.

That’s it for this week. Have a great weekend!