Small Caps Live Weekly Summary

Inflation Semiconductors MRK ZTF

Another week of reduced discussion this week due to holidays, weather, and lack of news. WayneJ still managed an extensive Large Caps Live, though.

Large Caps Live

The question of the day - inflation and how to invest in such an environment. So:

(1) Do we risk a recession? One of the arguments re no recession is that we have strong employment and a tight labour market. I have been looking into this and it seems that if anything tight labour markets and low unemployment do NOT exclude a forthcoming recession. Perhaps the following chart helps here:

Another chart:

And this:

That is a very important point. The latest US employment survey shows an increase in jobs - but a lot of those jobs were part-time. And I suspect that means a lot of them are casual jobs eg home delivery. I think people are getting used to the convenience of home delivery and not thinking about the number of hands (ie people) that have to touch a product for home delivery vs purchase in a shop / retailer. By this I mean both direct (ie delivery staff) but also indirect eg billing, software development, logistics coordinators etc.

So the first point to take away is that unemployment is a poor indicator of recession as it tends to be backward facing. Indeed in 2001 unemployment initially fell as we went into a recession. I think we are also scared by memories of the 1980s / 1970s where recession was associated with high levels of unemployment.

(2) A recession is generally defined as two consecutive quarters of negative GDP growth but I would argue that one has to be pragmatic eg if one had GDP of -2% +0.1%, -2.3% I would argue that is a recession even if there was a slight positive in the second month. The significance of that is that the UK numbers for earlier this year were distorted by the Queen's Platinum Jubilee. Let me quote from the BoE MPC committee notes for August:

The May outturn had been weaker than Bank staff had expected, but there was still uncertainty around the scale of the upward impact on activity from the additional trading day in May associated with the timing of the Platinum Jubilee bank holiday period.

And further on:

Following a 0.8% quarterly increase in GDP in 2022 Q1, Bank staff now expected GDP to have fallen by 0.2% in Q2 as a whole, weaker than the 0.1% growth expected in the May Monetary Policy Report. Headline growth had been depressed by the run-down of NHS Test and Trace activity and by the impact of the Platinum Jubilee over the quarter as a whole. Bank staff had estimated that GDP growth excluding those factors was likely to have been around ½%, compared to around 1% in previous quarters

Now in this case the Jubilee perhaps led to a lower GDP number, though given that in the first quote they highlight an extra trading day it is rather confusing. So anyway though I like the simplicity of a two consecutive quarter slow down I think that one will have to be more pragmatic.

(3) I reckon that business investment is a good leading indicator. And hence I think that the following from the MPC August notes is interesting:

Business investment had fallen by 0.6% in 2022 Q1 and had been persistently lower than expected in previous Monetary Policy Report projections. Relative to its pre-pandemic level, that weakness had been particularly apparent in investment in transport equipment and buildings and structures. Official data for business investment had been subject to significant revision in the past. According to the Bank’s Agents, investment intentions had softened slightly recently but had remained positive. Current investment spending had continued to be held back by cost pressures and shortages, and a greater number of the Agents’ contacts had indicated that uncertainty about demand might curtail investment in future.

I think we are seeing that in big companies eg tech companies that are cutting back on additional staff growth. But I suspect we will see that throughout the economy.

(3) There is a 'jaws' effect on people drawing a wage.

If CPI is over 9% but AWE (average weekly earnings) are only growing 4 - 5% (according to the MPC) I think that will lead to a squeeze on many people. That in turn will lead to a change in consumer spending.

(4) The MPC focusses on core inflation e.g.

Twelve-month CPI inflation had risen to 9.4% in June, 0.3 percentage points above the May Report projection. In contrast, core CPI inflation, excluding food, beverages and tobacco and energy, had fallen to 5.8%, around ½ percentage point below the expectation at the time of the May Report. Relative to the May Report, there had been upside news in fuel, food and, to a lesser extent, services prices. The softening in core CPI inflation had been accounted for by a deceleration in core goods prices, in large part reflecting outright falls in used car prices. Services inflation, which was more closely associated with domestically generated inflation, had risen further, to 5.2%.

I find it fascinating that the MPC has 'core' inflation which excludes the cost of food. I was struck by what was missing in the MPC minutes. I think the three big Fs are food, fertilizer and fuel (=energy). There was no discussion on fertiliser, limited discussion on food and fuel. And there are two big Is - inflation and interest rates - and frankly I am not convinced that they have been properly considered.

(5) As investors I think part of what we have to do is consider BEHAVIOURS and likely behaviours. I think we are already seeing some behavioural changes, such as an increase in consumer credit / unsecured lending especially in the US. US credit card debt rose 13% in a year. To some extent I would expect that post Covid and post lockdown anyway. CNN inteprets this as “Americans are piling up credit card debt as they struggle to keep up with the high cost of living.”. Whereas CNBC takes the same story and translates it into 'consumer is strong'

So thinking about behaviours. I mentioned the other day somewhere that I had noted that graphics card prices were falling. The Semiconductor ETF that I traded for a decade:

This is one of the most important charts I'm watching. Semiconductor stocks are an important indicator for the REST of the market. So if $SMH breaks higher (above the downtrend line), it could signal the rest of the market still has room to run. And this:

Now - why should you all care re semiconductors?

(1) I think that the great semiconductor shortage is correcting itself faster than people expect due to three issues (a) debottlenecking and sorting out the supply chain (b) increased supply - the industry increases its capacity each year (c) a decline in demand

(2) The decline in demand I think is starting to show in white goods sales, PC sales etc

(3) We are starting to see this in second hand car prices falling. And our local car dealer has invited us to a 'special' sales promotion event.

So where does that lead us? I anticipate:

(1) We get low GDP growth or even declines in REAL terms. BUT maybe increases in NOMINAL terms.

(2) In order to tame inflation central banks will continue to raise rates. BUT as in previous generations there will come a point where the political pressure (even if central banks are independent) will be too high - so they will ease off. I think this happened to various extents in Germany in the Weimar Republic, in the US in the 1920s - 1930s, in the 1970s - 1980s etc.

(3) I would highly recommend reading Ackman’s slides on inflation. He mentions 'stagflation' and I think that is the right term ie slow or negative real GDP growth and high inflation. I know that different people have different impact from inflation. But I also think that the % increase in some utility bills will hit middle England. It will not surprise me if the average 68 year old Shires resident, Daily Telegraph reading couple living in a detached house and supporting Liz Truss face a £3 - 4 k pound increase in utility bills. If they are living on a (say) £60k per year pension they that is going to hurt. Remember that even pensions are taxed so their take home is probably say £45k per year.

I think that when central banks raise rates they are ultimately trying to slow demand and implicitly that means more unemployment UNTIL it becomes politically unacceptable.

Small Caps

Marks Electrical (MRK.L) - AGM Trading Update

We've started the year well despite a very tough market back-drop with the Group's sales for the first four months up 13.7% compared with the online MDA and CE markets being down over 20% in the first months of our FY23.

As a result, they have seen strong market share gains, going from 2.5% to 3.8% YoY (+50%) in their core market. Even at a modest 3.8% market share, this growth clearly cannot continue at this rate in the medium term. But 20% over 5 years would still leave them with under 10% share.

On cash costs, they are well invested in terms of vehicles and warehouse space. Leo had hoped that competitors such as AO would be forced to cut advertising, lowering rates across the industry, and to seek margins. However:

We've seen strong competitive activity both in pricing and marketing, with heavy discounting of headline prices and higher cost per click marketing expenses.

But overall everything seems to be fine:

Despite this, we have maintained our tight control on inventory, cost management and disciplined capital allocation, ensuring we are in a healthy cash position and remaining focused on profitable market share gains.

Broker Equity Development have a new note out, but with no changes to forecasts. Vox markets have an interview with the management team.

The share price has been weak here recently, and there appears to be an overhang from a large seller. The March 2024 forecast P/E is now 10.8x, which seems good value if they continue to deliver.

Zotefoams (ZTF.L) - Interim Results

Zotefoams has generated considerable debate on SCL. On the surface, investors are paying a very high multiple for a company that has not generated any profit growth in the last 5 years. They appear to have been engaging in a fools’ errand: pursuing revenue growth at declining margins in a capex-heavy industry. in doing so they have been racking up debt.

So the first thing we check is those debt levels. At £38m this has stopped increasing, which is good to see, however, ideally we’d like to see them generating free cash.

The high-level figures hide what is going on behind the scenes, though, which is 3 segments with very different recent performances. So the next thing we look at is the segmental reporting, this time for half-years:

Good to see HPP continuing to go from strength to strength. And all is not dead with Polyoefins, as it may have looked at the end of last year. MuCell still looks unproven to Mark and he wouldn’t attribute any value to this part of the business beyond net assets.

They now have a handle on their cost inflation issues:

We have delivered robust volume growth across both the HPP and Polyolefin Foam businesses in H1 2022. Alongside this, several rounds of price increases have been implemented across products and markets to catch up with persistent and unpredictable input cost inflation. As a result, we have been able to report stable gross margins, which has enabled strong first half operating profit growth.

And the result is that they expect to trade above market expectations:

Whilst remaining mindful of these risks we now expect full year underlying profit to be ahead of current market consensus expectations.

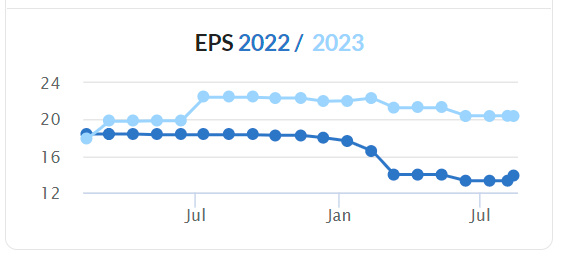

The consensus on Stockopedia shows that these are still significantly below where they were at the start of the year:

This means the current share price has dropped in proportion to EPS this year but there has been no de-rating. This shows the strength of belief that shareholders have in the company. At 23x forward earnings this isn’t cheap in current markets.

Despite growth continuing for HPP foams, and now good control of cost inflation issues, the dividend has only been increased 4%, and stands at just 2%, which suggests that the capital intensity of this business is not abating.

As described above, the valuation is more complex than this, since a sum of parts would ascribe significant value to the growing HPP foams, even if the Polyoefins & MuCell would be rated much less favourably. However, when buying shares in this business, shareholders are getting all three and there is little sign these will be separated. Also, given that Polyoefins foam segmental profits grew rapidly before declining. Mark thinks that we can’t rule out the same happening with HPP foams. The best investments are low-capex growth companies at value prices. This is a potential growth company, at least on the HPP foam side, but it is not low-capex and already at a growth company price.

That’s all for this week, enjoy the sun!