Small Caps Live Weekly Summary

Gordon Growth Model HUM CTG IGR TND SYS1 D4T4 SDG UPGS AO ARDN INCE CNKS WHI FCAP

It was a shaky start to the week, with Monday not a good day to be in any risk assets with Gold, Oil, Bitcoin etc. all down with the market indices. Although, this is really a dollar strength reaction so rationally UK listed stocks denominated in GBP should see a limited reaction. However, the market sentiment is what matters in the short term and early this week saw a plethora of weak small cap share prices.

The good news is that we have an in-person Mello event to look forward to in May

Large Caps Live

I was lecturing recently and talked about the Gordon Growth model. I want to flash up a sensitivity table and then highlight a couple of points:

As you can see the table was called 'Abusing the Gordon Growth Model’!

I have highlighted a square with 3% growth and a 5% discount rate which (if the base dividend is £1) means a business is worth £50 (ie 1 / (r-g) = 1 / (5% - 3%). So if the growth rate falls to 2% and the discount rate goes from 5% to 6% then r-g becomes 6% - 2% = 4% and the value growth to £25 ie halves.

Now, this may be trivial, but I was in a meeting last week where people were making comments on how the market was irrational etc and that valuations should not move far due to small changes in rates. I would suggest that interest rate rises have 3 effects on valuation:

a rate rise increases the risk-free

it impacts market sentiment and hence the equity risk premium as well; and

a rate rise reduces growth expectations so those fall at the same time

So as we saw above a 2% spread becomes a 4% spread and the valuation halves.

Usually, on SCL, we make the point that no equity investor should be using a discount rate below 10%. BUT remember the slide was on abusing the GGM!

But I would go further - the GGM should only be used when:

growth is stabilised

growth is significantly less than the discount rate

BUT in the height of a boom when animal instincts take over, people get overexcited and do not do that. For example, they try to pump into the GGM a growth rate of 15% and a discount rate of 16% or 18% and claim that their discount rate shows conservatism! These arguments rarely survive the bust that follows the boom.

Small Caps

Hummingbird Resources (HUM.L) - Q1 Operational & Trading Update

Hummingbird has been a persistent underperformer in the bull market for gold producers, and with these Q1 results you can see why:

As forecast at the start of that year, Q1 2022 production was a lower production quarter at 15,548 ounces ("oz") of gold (Q4 2021: 18,181oz)

The reduced production means they affectively make a loss for the quarter:

Increased AISC of US$2,235 per oz for Q1 2022 (Q4 2021: US$1,803 per oz)

…average realised price of US$1,837 per oz

They say that this is due to planned maintenance work:

…driven primarily by the planned essential maintenance work on the processing plant, and the gradual improvement in mining rates as extra excavators were added during the later end of the quarter, in particular.

However, it is really the low grade here that has caused the lower production:

The Q1 2022 grade profile was again relatively low primarily due to lower grade sections of the orebody accessed during the period and a run of mine ("ROM") pad not fully optimised to allow for more consistent better grade ore feed into the mill, resulting in lower grades being processed for the quarter.

However, they claim that this will improve going forward:

With improved mining rates and practices taking place, the quantity and quality of ore on our ROM pad is scheduled to improve, with expectations to then allow for better mill grade feed to be processed

And maintain their annual guidance:

Guidance: The Company maintains its 2022 guidance of 87,000 - 97,000 oz of gold, with an AISC of US$1,300 - US$1,450 per oz of gold with forecast improving trends in production and AISC as detailed above

But they will have to average 23.8koz per quarter for the rest of the year to hit even the low end of that range. Quite simply, the market doesn't believe them. If they can deliver this then the company looks incredibly good value. They have another mine, Kouroussa, in development, due to produce 100koz in 23Q2 and debt-funded to first pour. This would make them close to a 200koz producer in around a year’s time.

Comparing gold miners isn't all about production. Reserves, resources, AISC etc. are all big factors. But when you consider that something like Centamin produces 400-500koz and has a £1b market cap, the current c.£50m market cap of Hummingbird looks low.

And they also have a 51% interest in Dugbe:

Earn-in partner, Pasofino Gold Ltd ("Pasofino"), remains on track to release details of the Definitive Feasibility Study ("DFS") on the Dugbe gold mine in Liberia in Q2 2022. Once finalised this will be a significant milestone for the project and will complete its journey from being a pure exploration asset to a proven project with economic fundamentals of strategic value to Hummingbird

Here, they will likely swap their 51% interest for 51% of the equity of their partner, Pasofino Gold. This is listed in Canada with a market cap of around £23m, making the Hummingbird Enterprise Value something like:

£56m - £11m + £61m debt (including drawdown for Kouroussa construction ) = £106m.

If the management hit its targets this will easily be the cheapest EV/oz produced in 2023. However, this is also one of the biggest "if"s out there given the recent performance of Yanfolila. And, as such, is only for the brave.

Christie Group (CTG.L) - Final Results

This is a Lord Lee stock, so well worth looking at since it could be a place he puts some of his Air Partner winnings. Mark has avoided it it in the past due to the weak balance sheet, plus debt and a large pension deficit removing any superficial earnings cheapness when it is taken into account.

However, the balance sheet has strengthened recently. With the current ratio going from 1.17 at the HY to 1.35 at 31st Dec. The risk of this going bust in the short term is now significantly reduced.

Although the debt is now significantly reduced, this is not an asset play as net tangible assets are still negative and the company has significant provisions and the pension deficit remains, although at a reduced level as bond yields go up and asset prices have risen.

The EPS in these results looks pretty good:

Earnings per share rebounded back to 13.71p per share (2020: negative 19.32p per share)

Stockopedia has 6.62p as the forecast EPS so on the surface this is quite some beat.

House Broker Shore say:

FY Revenue rose by 45% to £61.3m and operating profit increased to £5.2m (vs Shore of £3.5m at H1 in September upgraded following the update in January 2022 to £5.0m)

I’d not seen these numbers, and neither, it appears, had Stockopedia’s data provider, so this is a beat but not as large as the stockopedia numbers would initially suggest. Still, 13.7p EPS works out to be a P/E of 8.6 which looks cheap in the current market.

The Professional & Financial Services business is the big driver of this outperformance with business sales up from 624 to 1069. Sales of hotels, holiday parks, dental practices and pharmacies all doing well during the year. There is clearly some momentum behind this part of the business, but as we see from the likes of finnCap & Numis, M&A transactions are viewed as very low-quality earnings by the market at the moment.

Stock & Inventory Systems & Services grew revenue vs 2020 but is still way below 2019:

Our Stock & Inventory Systems & Services (SISS) division achieved revenue of £17.5m (2020: £16.0m and 2019: £32.1m) including some £2.4m of furlough support. The year continued to be seriously affected by the pandemic, which resulted in a significant operating loss of £2.4m (2020: £3.2m operating loss).

The outlook is reasonable:

Our agencies' pipelines of deals in progress have grown to exceed those of the prior year.

Our stocktaking businesses from this point forward, should not put additional drain on our resources as their activity levels further recover.

But Shore have EPS declining in 2022 to 12.2p. Perhaps also taking into account that 2021 still contained £2.6m of government grants that won’t be repeated. Without these, the EPS would be much closer to the original Shore estimate of 6.7p.

Forecast EPS rises again in 2023 to 15p and 16p in 2024, again according to Shore, but this has the feel of a guess rather than an in-depth analysis - there is a large amount of uncertainty here.

The Dividend per share is increased to 3p but even with forecast rises this is a disappointment in our opinion. This sort of cheap people business should be yielding the 5-7% that brokers etc. trade on. Partly this is because they have been paying down debt, but also as one SCL discord contributor points out, the cash here often ends up going to the employees, not the owners.

And while the pension deficit is reducing, it is still requiring ongoing recovery payments. And as we know, Triennial funding can look very different to the IAS19 position.

Even if the 15p EPS is hit in 2023 then the Earnings Yield is around 10%, after accounting for the Pension Deficit. This isn't bad, but certainly isn't stand out for this sort of people business.

The 10% earnings yield includes the 15p EPS and the 120p offer. The P/E of 8 is flattered by a Pension Deficit that is a third of the market cap even after the recent reduction. Now the company is more profitable the trustee could well demand much more.

However, we can't see the "ongoing deficit repair plan costing approximately £1m per annum" in the cash flow statement. If this has already gone through the income statement then this will look more favourable (although does not mitigate the risk of increased demands in the future)

IG Design Group (IGR.L) - Post-Close Trading Update

We last looked at IG Design following its profit warning in January when the share prices was down 60% or so. We concluded:

Director sales at IG Design also tell a story. Since 2019, over £27m of shares have been sold by directors and just £60k bought. Perhaps one to consider only when it is clear that the business has stabilised and the directors finally see value again.

Since then the share price continued to drop down to the 60p level, before bouncing to 80p on the appointment of a well-regarded CFO, who then bought some shares. Although, he appears to have owned a few shares in them prior to his appointment so presumably knew the company already. However, a buy one day into the job suggests he's not making a particularly informed inside view.

The shares have dropped back down to 70p following this week’s update

In January, we also said that despite them reporting net cash:

…as with many companies, their year-end is a favourable time for working capital. Given their seasonality, IG have large working capital requirements peaking in October which will need to be debt-funded. As we're now being told that adjusted operating profit will be breakeven, there is a risk (depending on the calculations) of breaching the covenants and requiring a waiver. This looks unlikely to be a genuine going concern issue but requiring a covenant waiver is not a great look, and potentially adds significant debt costs.

This is now confirmed by the company:

The Group is in the process of finalising a facility waiver amendment in anticipation of the 2022 seasonal working capital requirements and an extension to March 2024 of the existing banking arrangements which run currently to June 2023. It is expected that these will be completed in the near term.

And that the current cash position is in no way a reflection of the typical situation for the rest of the year:

Average debt of the Group is expected to increase to c.$75-$80 million across the 12 months to 31 March 2023, compared to c.$15m in FY22 reflecting the expected higher working capital requirements of the Group throughout FY23.

We expect them to get the waiver but also for the banks to charge their pound of flesh. Indeed, they mention the subsequent impact on profitability going forward:

…with the adjusted loss before tax expected to be broadly flat on the Group's FY22 results, driven primarily by increased finance charges in the year ahead.

On discord, regular contributor Alistair provided a good summary of where we now are with IG Design:

They forecast a small loss before tax for the FY, but this involves a large loss in H2 (c. $19m). Curiously, although H2 includes Christmas it has been less profitable for them in FY19, FY20 and FY21 so some deterioration in H2 vs H1 was to be expected, but the outturn (as the company had guided) is much worse than previous years. This does mean that the apparently dull sounding outlook statement for FY23 (small loss) has some risks because they will have to improve considerably on H2 FY22.

The business has two main problems:

(i) it’s low gross margin and faces rising labour and high freight costs and negotiates with powerful buyers (Walmart is 24% of sales); and

(ii) it’s selling consumer discretionary products and discretionary spend is under pressure.

I suspect that customers like Walmart are willing to allow price increases to reflect additional costs actually incurred, but there has been a lag for container costs.

The short term bull case is:

(i) they’ve guided to a small loss for FY23 because they’re still fighting last year’s battle of costs rising out of control and lags in passing them through; but

(ii) they should already be getting respite on container costs (I’ve looked mainly at Asia to US) flattening and forward costs falling; and

(iii) my pet theory is that container costs will fall more quickly than the forward rates indicate because consumer demand for goods is falling on pressure on spend and shift to services and companies that are busy building and maintaining inventory will run down those inventories when they see freight rates falling rapidly which will then produce a virtuous circle of falling rates.

FWIW I don’t really buy this short term bull case because, as I said, the FY23 guidance is already baking in a significant improvement on H2 FY22, so it’s difficult to be confident that they’ll make it up and get ahead.

There are some reasons to be bullish longer term. They’ve increased sales by 10% in FY22, so have been growing ahead of inflation implying that they’re not being displaced by cheaper rivals and the business will potentially be there for them when and if the current squeeze dissipates. And they’ve hung out a carrot for investors who might not be inspired by loss before tax with another year of forecast loss before tax by publishing a longer term aspiration of 5-6% operating margin for their US business in FY25. Meeting that would obviously lead to a re-rating although, IMO, there is a risk of further pain in the meantime.

A new CEO might have different plans although I suspect the only real strategy open to them is to knuckle down with what they’ve got and turn the operating margin around. The board has been very savvy with their trading (especially the old CEO who sold all his shares towards the top and steadfastly resisted suggestions to buy) so it will be interesting to see any large buys.

So there doesn't appear to be a quick fix here, with FY25 being flagged as the target for the USA to return to acceptable margins and Mark thinks there is certainly scope for the new CFO to kitchen sink things and the outlook to get worse before it gets better.

One of the attractions may be that the Price to Tangible Book is only 0.33, the vast majority of which is inventory. If those assets can be made productive again then the upside is large. In an inflationary environment we are surprised there isn't a short term LIFO boost to accounting profits, or perhaps there has been, which flatters even the current poor results. However, in the short term, those assets are going to be even more unproductive as debt is taken on to build inventories which is going to yield no improvement in profitability.

So this looks too early to buy for any recovery to Mark, and as Studio Retail showed, things can go wrong quickly if banks get nervous about inventory builds. The big fall from grace, plus strong bull and bear arguments, will likely see this very volatile in the short term, making it a great trading share for those who are good at calling short-term sentiment.

Tandem (TND.L) - Resignation of CEO

Tandem reacted negatively this week to news that their CEO, Jim Shears is leaving:

Jim Shears, the Company's Chief Executive Officer, is due to leave the Company by mutual agreement and resign as a director of Tandem on 6 May 2022.

Given his 20 years with the business, the sudden departure and no words of thanks suggest this was neither a planned exit nor a happy one.

The company presented at Mello on Monday and it was an assured presentation from Phil Ratcliffe, Commercial Director, answering some of the more pressing questions around China sourcing and when investment into warehousing will pay off. You have to think that he is in the running to take the top job.

Probably the most important unanswered question, however, is will Jim Shears sell some or all of his 4.7% in the company? In these sorts of situations, where there is an unplanned exit, the leaving director tends to sell all their shares and go for a clean break from the company. Either through a loss of faith in the business under different stewardship or simply out of anger, it is very common for a leaving director to take a big haircut simply to get out. After he ceases to be a director he will no longer be required to inform the market of every sale and will only need to do so if he crosses the percentage thresholds.

Such selling doesn't change the long-term valuation, of course, but in the short term, a 4.7% overhang in a fairly illiquid stock could see quite a lot of selling pressure here.

System 1 (SYS1.L) - Trading Update

This looks to be reporting a further miss on expectations:

Profitability was stronger in H1 than H2 as the planned increase in H2 operating costs coincided with a reduction in revenue during the final quarter. We expect to report an adjusted profit before taxation (which excludes impairment, share-based payments, government support, bonuses, loan interest and certain provisions) of some £1.1m for the full year (FY21: £3.0m). Statutory profit before taxation is expected to be ca £0.8m, £1.1m before share-based payments. (FY21: £2.1m, £2.2m)

Revenue is only out by £0.1m vs the Stockopedia numbers but PBT of £1.1 vs the forecast of £1.4m PAT means a bigger miss here. And for this year they introduce the dreaded H2 weighting:

We intend to grow revenue and profits in the course of the new financial year and anticipate that the growth will be weighted to the second half of the year as expenditure flattens versus last year.

Without the buyback in place supporting the price, we were surprised that this didn’t sell off more strongly on this second profit warning in a row.

D4T4 Solutions - Follow up

Leo had an initial look at D4T4 Solutions last week. This week he took the time to dive into some more of the details, starting with the balance sheet:

I note goodwill back from the acquisition of what is now their main product line. Some of this was soon written down, but I am happy with the valuation of the rest. They amortise some IPR that likely comes with it, but exclude that from the adjusted profit figure. As they are not a serial acquirer and there is only 2 years left to go then I am happy with that treatment.

They have started capitalising software development costs and amortising them over 8 years. In principle, I am unhappy with that as I think 8 years is too long. But on the other hand, the amount is small and so can be ignored for the moment. Indeed, they are expensing quite a lot of costs for new products and you might even want to adjust more out to see the underlying picture.

I was concerned to see receivables blow out at the end of the last FY and it apparently in overdue 61-90 days. The commentary said that they had received payment immediately after year-end, but in H1 receivables were also elevated and this time there was no breakdown. They have massive direct customer concentration, with a single customer accounting for potentially 50% in 21H2 and 48% for the FY. I nearly stopped researching when I discovered that, but I since discovered that their integration partners act as principals. So it is not a single end customer that could cancel. But it is a single customer that could (in the abstract) become insolvent potentially leading to large credit losses and disruption. I would need to check the accounts of their major customers (which are known, albeit I am not certain which is number 1) before taking a major shareholding.

Also, nobody likes to see a growing deferred income liability on the balance sheet, but this a part of life for a SaaS company and can be used to verify claims about recurring revenue levels. Overall I was happy with the balance sheet.

Following this balance sheet check Leo then put together a detailed model of the company finances:

My models include my own opinion of an adjusted profit measure. In this case, this varies from their adjusted measure by including averaged restructuring costs (which recur most years) and averaged capitalised development costs (which will approximate to the non-acquisition park of the amortisation they exclude in the long term). At this stage, these numbers are not large enough to worry about, but I had to check them to know that, and this may change in future.

I also looked at the segment data provided. This underlined that this is effectively as US company with US customers and a US CEO. A relisting or corporate activity cannot be ruled out. I also looked at the SaaS metrics. Some of these are only available in presentations. As is often the case I had to reverse engineer a graph. The vast majority of their ARR is Support & Maintenance contracts which they have always offered against their perpetual license sales. To see the true SaaS part you need to concentrate on the "Products - Own IP" section. This is indeed growing strongly, albeit not exponentially:

The last year shown is to FY 2021 which was affected by covid. We don't have the breakdown for FY 2022 (just finished) yet, but we do have an estimate of the total. And this allows ARR coverage of forward revenue to be calculated:

That last bar is ARR at the end of FY 2022 versus forecasts for FY 2023. These are percentages which mathematically cannot exceed 100% for credible revenue forecasts. Yes, they can rise over time as revenue quality increases, but growth must slow as they get anywhere near 100%. That jump for 2022/23 just looks too high. I think revenue forecasts for FY 2023 are too low and can be beaten with relative ease.

However, I also think the company are quite right to guide conservatively and aim to beat, especially given their H2 (let's face it, Q4) weighting.

Having looked at the figures, Leo finally looks at the "story":

They have a very impressive customer list. Retention periods (checked with Wayback Machine) seem very good. I can see how their product is genuinely and increasingly valuable to customers. All indications are that they have limited competition.

Then there is the new product to do with fraud prevention. They are investing a lot in this, approximately $1.5m a year according to the US CEO. So far revenues are minimal. So without this uncapitalised investment EPS would be 2+p higher. Either this will go as expected and spending will reduce to $1.0m a year diluted by higher revenues, or it will not and there is lots of scope for cost savings, or it will go better and nobody will care. There appears to be nothing for this in the forecasts for 2022, but contract announcements may be imminent.

So I think the reasons for the historical investor excitement here are intact and the 26x PE is not quite as expensive as it seems with "underlying" profits higher and a likely beat.

Sanderson Design Group (SDG.L) - Full Year Results

Compared to the better comparator of 2020, revenue is flat but profits have increased significantly:

Mainly driven by decent increases in Gross margin:

Distribution costs are up, as one may expect, but this is offset by a reduction in Admin Expenses:

However, this is one of the companies where there is a big difference between adjusted and statutory profits so before looking at valuation, we need to take a view on the suitability of these adjustments:

Let’s go through these one by one:

The restructuring costs are high this year:

These relate to the reorganisation of the Group and comprise of the rationalisation of certain operational and support functions. The costs mainly comprise employee severance and professional fees associated with the closure of Sanderson Design Group Brands SARL in France of £1,100,000 and other reorganisation costs of £90,000 (2021: £171,000). See further details in the Chief Financial Officer's Review.

So the bulk of these are closing the French office and should be genuinely one-off. However, there does seem to be an ongoing restructuring charge that keeps occurring so this bears watching for in the future.

It is now normal for companies to exclude amortisation of acquired intangibles from their adjusted figure, which shows that this accounting standard now seems largely pointless. We have an issue when repeatedly acquisitive companies count all the gains in revenue and profit from acquisitions but exclude the acquisition costs and ongoing amortisation. However, this isn't the case here and it makes sense to adjust this out.

The LTIP accounting charge, again, is normal to adjust out. However, if you are going to do this then EPS really needs to be calculated on a fully diluted basis.

Adding back in the defined benefit pension charge is a little bit more controversial. Given that this is added back into the cash flow statement this is a non-cash charge. However, there is a large cash outflow in pension deficit recovery contributions of £2.209m. It may be tempting to view this as a one-off and exclude this. Particularly since the IAS19 valuation is in surplus.

Unfortunately, the triennial is in deficit and looks to remain so. They say:

The triennial valuation of the schemes, based on the position of the schemes on 5 April 2021, is in the process of being completed. Independent pension and actuarial specialists are supporting the Group through the valuation process.

But they have clearly been given a steer on the outcome as they say:

The Group's contributions to the schemes for the year beginning 1 February 2022 are expected to be £2,391,000.

So deficit recovery payments appear to be increasing not decreasing (although it is not clear if this figure includes some of the ongoing admin costs etc.)

So the "real" adjusted PBT is £10.3m. This means that the real EPS, by coincidence, turns out to be almost exactly the accounting EPS, which is 10.8p fully diluted.

£19m of cash is 26.5p per share, making the cash adjusted P/E 12.7. So potentially good value if they can continue to grow. The high gross margins mean that any sales growth will drop to the bottom line.

The outlook is perhaps better than one may have expected given the challenges in the world:

Trading in the first three months of the current financial year has performed in line with expectations, with continued demand for manufacturing and strong brand sales, particularly Morris & Co. and Sanderson. Licence income has also performed strongly. The simplification of the Group has continued with the closure of our French subsidiary, with business in France now managed directly from the UK.

However, a lot depends on high-end consumer discretionary spending bucking the trend of squeezed incomes. This seems logical, but then none of us really know what the impacts of higher inflation are going to be across the consumer discretionary sector. Perhaps Sanderson holders should now be standing outside John Lewis counting footfall to get the true picture.

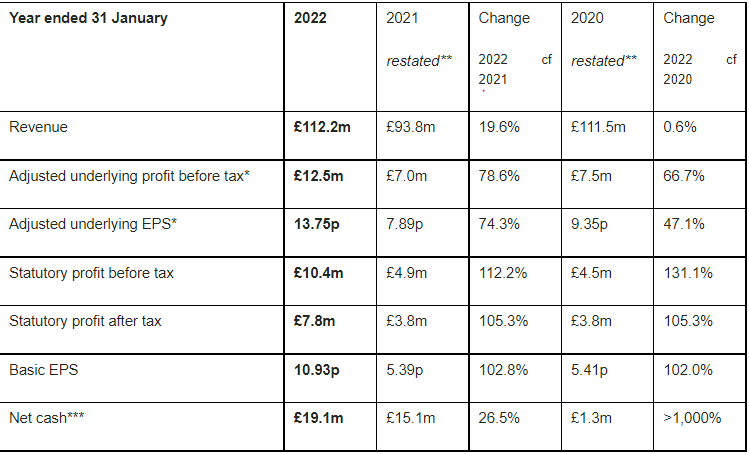

UP Global Sourcing (UPGS.L) - Interim Results

These read well with revenue up 13.7%, although this was only 2.6% organic growth. Profits look even better:

Profit before taxation up 36.4% to £9.8m (H1 FY 21: £7.2m)

Driven by higher gross margins:

Gross margin increased to 24.4 % (H1 FY 21: 22.8 %), driven by the benefits of the Salter acquisition, with the Salter licence royalty now no longer payable and the addition of the higher-margin scales business

Although they don’t provide a like-for-like figure for profits. On the outlook, they say:

The Board anticipates a full year performance in line with current market expectations.

These presumably being the £15.9m PBT from Equity Development.

The Group has so far been unimpacted by the recent lockdowns in China, but continues to monitor the situation closely. The Board is confident in the Group's ability to navigate its way through any further lockdowns in the region, having done so successfully at the beginning of the pandemic.

More broadly, the current cost of living crisis, partly arising from the war in Ukraine, together with increased personal taxation and reduced benefits is leading to a general fall in disposable income. The Board believes that the Group is well placed to respond to this given its relentless focus on delivering value to the consumer. We intend to carry on winning market share and through this continue to deliver growth despite the challenging market backdrop.

However, ED reduce their Price Target:

We modify our fair value / share from 275p to 250p to reflect exogenous factors such as higher interest rates and inflation but retain confidence in a fair value materially above the current share price

Using ED's figures, we note that the largest brands are growing faster than revenue as a whole. Should this continue the growth will naturally accelerate as these more successful brands become a greater part of the whole.

There is a major inventory build forecast for the FY and most of this was seen in H1. UPGS comment:

Higher inventories are attributable to the necessary rebuilding of the Group's stock position after being artificially depressed during FY 20 and FY 21 by the accelerated growth of online during lockdown, the strong demand for sales from stock as non-essential retailers reopened and reduced shipping capacity as a result of the CY 21 shipping crisis.

Of course, they have also acquired stock and a requirement to stock with Salter scales. Cashflow also now looks poor in 2023 due to further working capital build. We don't know how much reliance should be placed on these figures, however. Equity Development maintain their usual 6% growth in revenue for 2023, which may prove optimistic.

The UPGS balance sheet looks a little bit better than before with a current ratio of 1.27. Although, running with no cash and lots of short term debt means they are at the mercy of their banks somewhat. The ED forecast of £18.8m EBITDA means that the debt is only 1.5x forecast EBITDA, so quite manageable.

The gross margin here is low, indicating that they have little competitive advantage in the products they create. Their key skillset is the efficiency of their operations, keeping admin costs low as a proportion of sales.

The gross margin has increased as Salter is a higher-quality brand but this may be a key risk area in the current market since a gross margin drop back to 2021 levels would cut EBITDA forecasts by 20%.

It would be useful to know what the peak debt is during the year, not just the balance sheet date. But in general, this doesn’t seem to be a big risk given that the bulk of the facilities are invoice discounting:

The Group is funded by external bank facilities provided by HSBC comprising a revolving credit facility of £8.2 m, an invoice discounting facility of £23.5 m and a term loan of £9 m, all running to 2024, along with an import loan facility of £8.7 m which is subject to annual review.

So these are likely to be able to be increased if the receivables grow further and receivables are largely insured. 98% of them were at the year-end.

This issue is ongoing poor cash flow means that further earnings enhancing acquisitions are probably off the table and opportunities for returns to shareholders are limited.

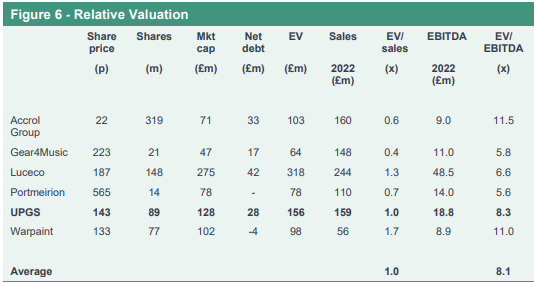

As such, and with significant uncertainty over the 2023 numbers, the current forecast of 8.5x EV/EBITDA doesn’t look particularly cheap given that most of the supply is from China and most of the forecast sales growth is from Germany. Even the (reduced) ED target of 250p at 13.4xEV/EBITDA feels more like picking a round number above the current share price than a considered valuation. Their relative valuation table shows that some higher quality businesses now trade a discount to UPGS not a premium:

AO World (AO.L) - Trading Statement

AO is the major competitor for Marks Electrical, who presented at our in-person SCl event. This week AO issued a trading statement:

Group Adjusted EBITDA is expected to be c. £8m, reflecting the impact of lower sales volumes and higher costs incurred in our UK logistics operations; driver shortages across the industry in H1; and significantly higher marketing costs in Germany.

AO’s logistics strategy looks weak in the current markets versus Marks who employ their own drivers and own their own vans and hence have better net promoter and TrustPilot scores.

In March, we were notified of higher warranty cancellations than average historical trends as customers responded to the escalating cost of living.

AO always came across as a warranty seller with a loss-making white goods seller attached. And warranties never seemed to be great value, hence higher warranty cancellations are good news for everyone…apart from AO.

could result in a reassessment of the carrying value of the contract asset, which could lead to a material impact on FY22 profits.

Perhaps it would be better if their accounting was more straightforward?

Competition in the German online market has remained intense, with digital marketing costs increasing significantly as a result, despite online penetration returning to pre-pandemic levels.

The strategic review is continuing...

Perhaps they should focus on execution in their core market?

In the coming year, we will focus on cash generation to strengthen the balance sheet whilst optimising our cost base to align with the expected lower levels of revenues.

Perhaps cash generation should have been a focus all along?

The outlook doesn’t look that bad, however:

In view of the volatile market conditions, inflationary cost pressures and logistical challenges in the supply chain, together with the escalating cost of living for consumers, we remain cautious about our revenue and profit outlook in the near term.

With the shares down 20%, these comments about liquidity are maybe doing the damage:

Available liquidity as at 31 March 2022 was c. £50m and, given the factors cited above and the seasonality of our cash flows, our liquidity has since reduced. However, we expect that this situation will improve as we move into Q2 driven by a range of actions that we are implementing. The Group's revolving credit facility of £80m was extended and now expires in April 2024. Net debt at the end of the financial year was £32.8m.

As we’ve said before, anyone wanting exposure to this sector should really be looking at Marks Electrical, which appears to be a much better run company and cheaper. Unfortunately, it still appears expensive on an absolute basis and hence isn’t for us at the moment at the current price.

Listed Brokers (ARDN.L, INCE.L, CNKS.L, WHI.L, FCAP.L)

With the Ince takeover of Arden completing this week and Ince failing to get approval to be a Nomad, many of Arden’s client list was left searching for new Nomads. There was a material risk that some of these would not get one appointed in time and would be delisted. In the end, they all managed it apart from Origo Partners who had announced their intention to delist anyway:

In our opinion, Strand Hanson is a kind of no-frills Nomad for those who aren’t interested in extensive research being published. The number which went to Strand Hanson perhaps suggests they took some Arden staff? Many companies went with their joint broker, understandably.

We were surprised to see that finnCap did not become a Nomad for any of the companies that were marooned by Arden. Although many were too small (and a couple perhaps too big), there were perhaps 10 within range that looked reasonably sensible. finnCap not taking any potentially suggests they are not actively looking for new Nomad clients.

Leo analysed changes to their Nomad client list over the last 6 months. Generally, they have been active with IPOs and taking business from other people, although mostly companies that had grown "too large" for the likes of Allenby or were/had become "too small" for Peel Hunt. Overall they won more than they actively lost, but not enough to compensate for the natural attrition from takeovers and delistings.

The quality or size of new customers is higher than customers lost, but of course, some of the losses are because quality/size had declined during their time as customer. So while they are still actively taking on new clients, there is no evidence of any concerted effort to grow them.

We don't actually think this matters much, as the public markets are likely to be more difficult for a few years and they seem to be focusing elsewhere, as suggested by this week’s announcement:

finnCap announces that it has, today, acquired a 50% interest in Energise Limited ("Energise") a net zero and sustainability consultancy, based near Cambridge…

Mark doesn’t know quite how to feel about this one. It is clearly a big growth area where reporting etc. is now mandatory due to the influence of larger shareholders. Many companies will be struggling with this and welcome the help. I can see finnCap with their contacts driving lots of business in this area for the JV. On the other hand, the price they've paid isn't obviously cheap, and not all shareholders or managements value this sort of reporting.

We don't like JVs in principal, but today's deal is not the typical arrangement where the other company has a continuing business not part of the JV. The main concern is the price paid. £1.1m revenue / £0.1m EBITDA indicates it is subscale, presumably due to being early stage. An EBITDA valuation doesn't make much sense. Assuming 25% EBITDA margins at scale, EBITDA would be £0.3m, they are still effectively 15x EBITDA for 50%. So, a lot of the cost is option value on this growing strongly and has a sufficiently good outlook such that 6-8x EBITDA for the other half is good value.

Still, it aligns with the finnCap core mission of doing the right thing and helping clients to do the right thing. And it potentially looks very cheap having retained (in some form) the exceptional profits of recent years on their balance sheet and are now looking to use this to expand into complementary areas. Companies that do this well often get earnings growth and a multiple re-rating. We really need to see some 2023 forecasts to make any further judgement on this, though.

That’s all for this week. Have a great weekend!