Small Caps Live Weekly Summary

ALU BKS DARK G4M HARL JSE LUCE SRC SLP

A fair amount of discussion this week, so straight into the results:

Alumasc (ALU.L) - Final Results

Ok, but not outstanding performance here:

§ Group revenues from continuing operations maintained at £89.1m (FY22: £89.4m)

§ Group underlying* profit before tax from continuing operations £11.2m (FY22: £12.7m)

However, this is enough to see a small reduction in net debt and a small increase in dividends. Given they operate in the building products sector, the outlook is probably the most important news:

§ Healthy order book; year started in line with management's expectations

§ Water Management expected to see positive impact from delayed Chek Lap Kok contract and contribution from ARP acquisition

§ Diversified businesses, innovative products and demand for sustainable building products provide resilience

§ The Board anticipate short-term market conditions will remain challenging, but are confident the Group has taken the right actions to manage these, while the Group remains well positioned to benefit when markets normalise.

Their house broker, finnCap, makes no change to operating profit forecasts, although FY24 forecasts fall by 5%, reflecting higher interest costs.

Unlike some companies we look at, we can't see anything specific in these results that the company might cite in a couple of months’ time as to why they are issuing a profits warning. You know the sort of thing: "As we highlighted in the results statement on 5th September, blar blar blar, the situation has worsened and profit expectations are halved".

The “progressive dividend policy [that] reflects Board's confidence in outlook” helps back this up as actions often speak louder than words when it comes to company results. So this looks pretty cheap on a PE of 6, with a good yield and growth potential in better times. Net cash is forecast by June 2024.

The badly run pension scheme is a bit of a problem:

As previously reported, our annual defined benefit pension scheme contributions have been reduced to £1.2 million (previously £2.3 million), reflecting an agreement with the trustees until 2025. Along with many other schemes, Alumasc's defined benefit pension scheme felt the effects of the financial markets turmoil following the September 2022 mini-budget. The pension scheme deficit was £4.3 million at 30 June 2023 (2022: £2.1 million).

Gross liabilities are £76m, versus Alumasc's market cap of £55m, which means this has scope to do some damage. However, if we take the £4.3m at face value, this is still only an adjusted forward P/E of 7.5.

Beeks Financial Cloud (BKS.L) - Trading Update

Beeks provide lots of details about how well they are doing:

Revenue for FY23 is expected to be over 20% higher than FY22, delivering underlying EBITDA growth of over 35% and underlying profit before tax growth of approximately 10% versus FY22.

But strangely, no clear guidance on whether this is in line with expectations or not. We are always a little sceptical of Beeks reporting, given their history of missing forecasts. And we are right to retain our scepticism as the title of the Canaccord note makes plain:

Small speed bump but the road ahead remains clear

They continue:

Expected adj. PBT growth of +10% implies ~£2.3m vs our £3.1m forecast.

From then on, it all gets a bit confusing. In the text, Canacord say they are reducing revenue to £22.5m but fail to update the table in their note for this change, nor a new EPS figure.

Paid for broker Progressive, don’t clear matters up either, saying:

Forecasts unchanged. We leave our estimates unaltered, as below, and will reflect FY23 results once fully detailed by the company in October.

So they retain a £24.5m revenue forecast. That's a big discrepancy on revenue for a period that is long over. Either Beeks don't really know the numbers or are unable to communicate them.

Given all this, you can see why some investors were confused by this and missed that it was a big profits warning and the shares opened up briefly on the morning.

We have said in the past that not only is the share overvalued and has underdelivered on EPS, but the cash flow is even worse. Analysis of the business model and accounts suggests that this would improve as soon as they stop growing, but today, we have the proof. They fail to make a few sales and:

[Beeks] generated around £1m in FCF in the second half, improving net cash to £4.4m, above our £3.5m estimate.

The other positive that we've said before, is that banks are willing lenders because what they are buying on behalf of clients is real IT kit that has other uses and can be repossessed if the company fails.

Assuming Canaccord have been accurately guided on revenue, we can imply that the EPS would be around 3.5p (although probably with some aggressive adjustments in there). It is a capex-heavy company and hence deserves a relatively low rating, but there is growth here, and they have now demonstrated they can make cash when they stop growing. Fair value is probably around a 10x P/E or 35p. Making it still significantly overvalued, despite the market eventually cottoning on that this was a profits warning.

Darktrace (DARK.L) - Final Results

It is beyond our pay grade to analyse this large cap cybersecurity started by former Autonomy executives in any detail. We will simply note that they managed to grow revenue by $130m during the year by spending $290m on sales and marketing. This dwarfed the $31.3m cash spent on R&D in the period. Readers can decide for themselves what this means for where the company’s strengths and weaknesses may lie.

Gear4music (G4M.L) - Trading Update

An in-line statement from this musical retailer, mainly due to a lot of cost-cutting:

we are prioritising increasing gross margins and cost base reduction to improve profitability, ahead of revenue growth.

Presumably, they have engaged in less promotional activity to improve gross margin and cost cutting to maintain profitability, such as:

…driving significant cost efficiencies in our software development unit.

Sounds a lot like making the most expensive staff redundant! Helpfully, they give us the consensus:

Gear4music believes that consensus market expectations for the year ending 31 March 2024 prior to release of this announcement were revenues of £161.2 million and EBITDA of £10.0 million.

So this is on a 4x EV/EBITDA rating, which isn’t crazy on the surface. The problem is that they don’t seem to want to mention profits or EPS in their guidance. This is a company that has £1-2m ongoing capex plus £5m+ a year of capitalised development expense. When you add these to the finance costs, free cash flow, excluding any working capital flows, will probably only be around £2m. Not great for a company that has now signalled prioritising profitability over revenue growth.

Harland & Wolff (HARL.L) - Half-Year Report

This is almost certainly the worst balance sheet we have ever seen:

Not just in how much current liabilities exceed current assets, with so little tangible asset backing in the non-current assets, but in the scale of the deterioration in balance sheet strength in such a short period of time. when things are this bad, we simply don’t have to read any further.

Jadestone Energy (JSE.L) - Montara Update

Good news again, all going to plan:

With further wells being brought back online in recent days, production has increased to c.8,000 bbls/d. This figure includes some flush production, and it is expected that average Montara production will return to pre-shutdown levels of c.6,000 bbls/d over the coming days.

This confirms what we thought, that the share price drop on suspension of production was a massive over-reaction.

Luceco (LUCE.L) - Interim Results

These are not bad results considering the RMI backdrop:

Drop in freight rates etc. is a clear tailwind for Gross Marginss as they say:

Adjusted Operating Profit: £10.8m (H1 2022: £11.5m) reflecting a return to strong gross margins, up over 5 percentage points versus H1 2022 to 39.4%

But as usual, you can drive a bus between statutory and adjusted results.

The adjustments are fairly standard: amortisation of acquired intangibles and related acquisition costs and the re-measurement to the fair value of the hedging portfolio. So no different to any other company would do, but as a serial acquirer, you have to question the exclusion of acquisition costs, which are cash costs, even if amortisation of acquired intangibles is not.

Last year, the rise in net debt scared some investors, so pleasing that they say:

Covenant Net Debt reduced by 30.2% year on year and Covenant Net Debt : EBITDA ratio remains at the lower end of the target range at 1.3x (H1 2022: 1.4x)

But this reduction occurred in H2 last year so is no new news. Most pleasingly, there is continued momentum in the business:

- Customer stocking has appeared to return to normal levels at the end of H1 2023 following post-pandemic destocking

- Non-residential demand continues its favourable trend

And several tailwinds:

- Despite economic headwinds, revenue decline has been less than expected

-Material and freight costs pressures have subsided

Leading to:

further progress since the July trading update and we now expect full year 2023 adjusted operating profit to show clear progress on last year. This is above the current range of market expectations.

Not sure exactly what this means, as Stockopedia already had higher EPS for 2023. However, these results have led brokers to upgrade forecasts:

They weren’t looking particularly cheap prior to this update. But the combination of this plus a small drop in price, presumably due to their caution on 2024:

We remain mindful of the uncertain macroeconomic environment and the potential impact it may have on our markets in 2024.

The results presentation was impressive. They always seem to have a deep understanding of their business and strategy without a lot of promotional BS that we often see from management teams. Net debt to EBITDA at the end of the year should be less than 1, which gives them around £35m to make acquisitions. They have a strong M&A pipeline with three workstreams currently in progress. One of these may give manufacturing geographic diversity, which is now a key focus.

They are confident that, over the long term, they have the runway to grow 10% CAGR organically and 10% CAGR through acquisitions (although both will be lumpy to some extent). Gross margins for H2 will be above 40%, and long term should be around the 40% level as they increasingly to a more favourable value-added mix. If the RMI market begins to show some strength again, then operating margins should be around 15%. The maths of this strategy make this a compelling investment opportunity if they can continue to deliver.

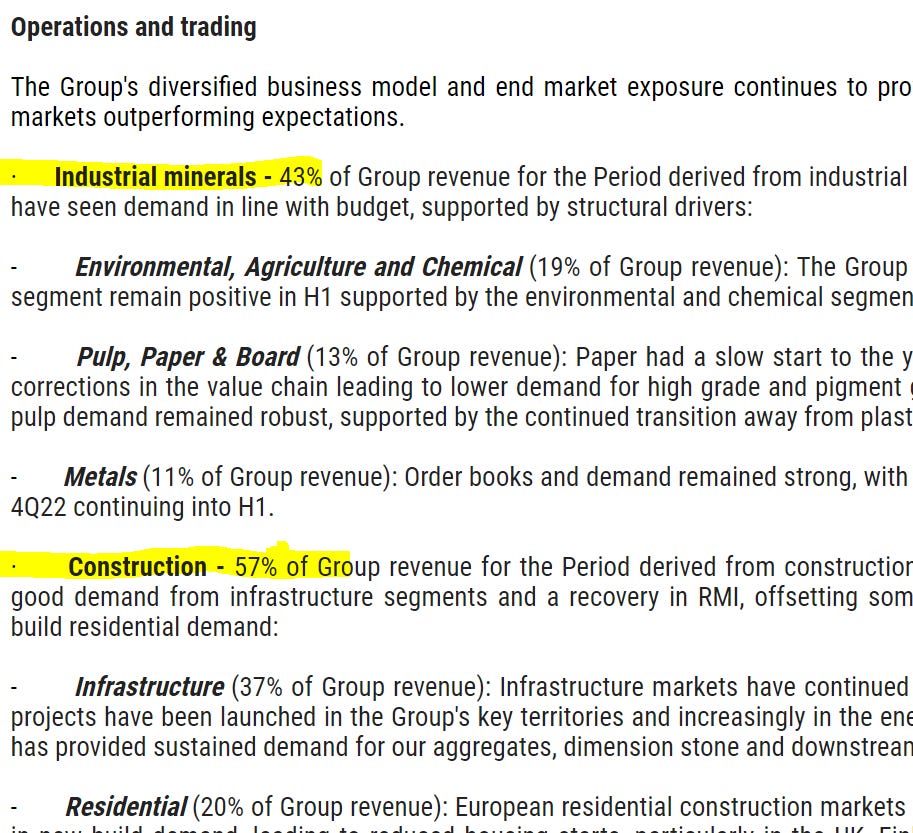

SigmaRoc (SRC.L) - Interim Results

As a company we haven’t followed closely in the past, it was pleasing to see that these results contain a nice breakdown of their markets and how these are performing:

You can see that Construction is the majority, and within that is infrastructure (including what sounds like wind turbines) and residential. Accordingly you would reasonably expect a profits warning with today's update, but instead:

H2 trading has started well, with continuing robust demand for infrastructure and quicklime products, alongside stabilised conditions in the paper, pulp & board market;

…While the Board is mindful that trading conditions are likely to remain challenging in several of the Group's markets, the Board expects that the Group's diversified end market exposure, geographic spread, and decentralised operating model will continue to deliver a resilient performance and accordingly the Board's expectations for the full year remain unchanged.

They continue to act as a consolidator in the sector:

SigmaRoc's vision is to become the leading European quarried materials group, seeking to create value by purchasing assets in fragmented materials markets and extracting efficiencies through active management and forming the assets into larger groups.

The forward PE of 7.2x on Stockopedia appears to be correct and is significantly lower than similar rollups are and/or have been in the past, including Sigmaroc itself, which was on 18x back in September 2021. However, there is significant net debt and adjusting for this makes the P/E closer to 10.

Steady-state forecasts from Liberum are for debt to be repaid at a rate of £50m pa, with elimination by FY 12/2026, although their forecast of net interest being flat throughout calls into question the credibility of their whole model. In practice, acquisitions are expected.

Debt structure is important in a company like this:

The Group’s Debt Facilities have a maturity date of 15 July 2026

So the debt term is OK for the moment, but they probably should be extending next time they make an acquisition. They have the freedom to stop acquiring and pay off the debt if they don't like the incremental ROE, which puts them in a far better position than a company forced to roll at any price. The failure to fix is probably reflected in the share price falls as interest rates have risen, and it is probably too late to fix now.

With trading this robust in difficult conditions, it is difficult not to be optimistic about how well they would do in better times, although the risk is there is a lag or that things will get worse still. If you trust management on capital allocation and you trust that debt would be repaid in 2026 without further acquisitions, then we can see the argument that this looks fair value now but with some good returns to come across the cycle.

Sylvania Platinum (SLP.L) - Annual Results

There's nothing new in the financial results due to the detailed quarterly reporting from the company. The market seems to have liked them, though, presumably because they are still paying out a decent dividend and are renewing the buyback.

However, the outlook doesn't mention the elephant in the room. Which is that current PGM pricing means they are on a forward P/E of around 23. Given the large cash balance, the forward EV/EBITDA is a more reasonable 7.4 (if you adjust for the $32m committed to the chrome JV). Not crazy, but this company is used to trading at an EV/EBITDA between 1 and 3, reflecting the risks of the operations and the limited life of the resource. So anyone buying or holding today, including the company with their buyback, is betting on a rapid increase in PGM prices happening fairly soon. The longer they stay at current levels, the more shareholders may be in for a rude awakening.

That’s it for this week. Have a great weekend!