Small Caps Live Weekly Summary

FLO GMS HERC LIKE MEGP PMP

A quiet week this week, as most of us were too busy enjoying ourselves at Mello. The standard of companies was particularly high this time, as was the turnout for many presentations. We take this as a positive sign for UK small caps; that quality companies feel they have a story to tell again, and investors have capital to deploy.

(Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.) To avoid spam, the only way for new members to join the Discord server is via the Small Caps Live website. This will be instead of direct invites via Discord. All genuine investors are still very welcome to join in the discussions.

Flowtech FluidPower (FLO.L) - Acquistion

The £0.4m consideration for the Acquisition has been financed from the Group’s own cash resources. It is expected that this cost will be fully recouped from customer receipts before the end of FY26.

...For FY27 the Acquisition is expected to deliver turnover of c.£4m and EBITDA of c.£0.5m.

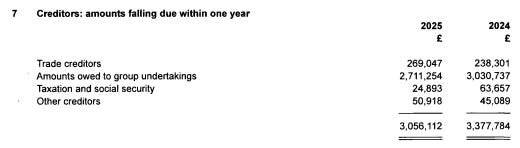

Small numbers, but on the face of it, a huge bargain. We are not sure why any business person would sell at this price. The only reasons we can come up with are severe financial distress or that they will still owe the (former) parent holdco a significant sum post acquistion. Here is what the last set of accounts to 31st March 2025 show:

It can’t be the full amount shown here, as they say they’ll be reporting as a bargain purchase gain, i.e. they are buying for less than the tangible book value. However, if there is anything outstanding, then management credibility is a serious concern here. Even if it really is only £400k paid, we think they owe shareholders an explanation as to why they have got such a good business with a great manager for an absolute pittance.

Gulf Marine Services (GMS.L) - Broker’s Note Update

Following Q1 Results, their broker Zeus said:

Full year EBITDA guidance again maintained. GMS has again maintained its existing 2026 EBITDA guidance of US$105-115m. This remains the company’s original guidance for the year, which did not include the Qatar downtime or the newly acquired vessel. As such, it looks like, while the actual 2026 full year outturn may move within this guidance range, overall the newly acquired vessel can be expected to significantly compensate for the Qatar downtime. We look for further confirmation of this going forward, including at the H1 results.

It seems confirmation was not forthcoming, as this week’s updated note showed them taking 33% out of adj. EPS and net debt estimates increase by $67m, partly due to the vessel acquistion.

This gives the appearance of a stealth profits warning via the brokers, rather than RNS guidance, with EBITDA going slightly below the bottom of the guidance range.

In only the way a broker can, Zeus manage to downgrade forward EPS by 33% yet keep an identical earnings-based valuation of 32p!

Hercules Site Services (HERC.L) - Interim Results

A 10 am results release on a Friday usually means bad news. Which is quickly confirmed on reading the headlines:

Underlying EBITDA* of £1.7m (H1 2025: £2.6m), reflecting planned investment in the Group’s future growth, including major technology enhancements, operational improvements and additional professional fees associated with the extended FY 2025 audit process

Underlying pre-tax profit of £0.6m (H1 2025: £1.7m) and underlying EPS of 0.67p (H1 2025: 2.11p) reflecting the impact of acquisition, extended audit and integration costs, as well as continued investment in strategic growth initiatives

On the plus side, they did show revenue growth:

Another period of growth and strategic progress, with revenue increasing 8% to a record £59.2m (H1 2025: £54.6m)

But then forget to mention that they bought two businesses in the meantime, one of which added £11.1m annualised revenue, and the other £1.4m. It seems organic revenue is likely down.

We have been highly critical in the past of the company’s unwillingness to provide the breakdown or details of the difference between statutory and adjusted figures in their Interim Results RNS.

Unsurprisingly, we are left yet again scrolling down to find that the real figures are an operating loss:

At least non-recurring costs have reduced. But they want us to ignore major investments again. It seems highly unlikely that they will treat any returns these major investments yield in the future as exceptional!

A quick look at the balance sheet shows £10.3m of net debt. They are guiding for an H2 weighting, and they better hope it arrives, as the leverage multiples look a bit high if we annualise H1 EBITDA, even if we take their slightly questionable definition of adjusted EBITDA.

Unsurprisingly, given the balance sheet, they say:

There will be no interim dividend in FY2026 (2025: 0.6p) as a result of our commitment to systems development and enhancements to support the continued growth of the business. The Board will keep the Company's dividend policy under review.

But strangely forget to mention the lack of distributable reserves that would prevent its payment anyway.

Likewise (LIKE.L) - Trading Update

We’re not entirely sure how they are doing this:

On a like for like basis, Total Group Revenue year to date 31 May 2026 has increased by 16.5%, with Sales in the month of May up by 19.1% against the corresponding period last year.

Order intake continues to be positive as the Group takes exponential gains in market share.

However they are managing it, it looks like the death knell for competitor Headlam. It is hard to understand how you can be so badly outcompeted in flooring distribution by a smaller competitor.

Perhaps the only saving grace would be that it now looks like a win-win for Likewise to acquire Headlam. The big questions are: what are the costs of rationalising Headlam’s network? Whether there has been enough churn in Headlam’s shareholder register that they’d capitulate for an offer below TBV? And whether the CMA would get involved?

ME Group (MEGP.L) - Trading Update

It’s bad news here:

While there has been an improvement in trading through May, the Board does not expect trading patterns to normalise while conflict in the Middle East and the subsequent uncertainty in the macroeconomic landscape continue. Consequently, the Board is taking a more cautious view to the full-year outlook, and it now expects FY 2026 profit before tax to be in the range of £69 million to £74 million.

They have had several recent missteps, and their business must be more fragile than we expected if a remote war can put people off washing their clothes.

The share price fell 25% in response, which seems large compared to the PBT downgrade (£79.9m to £69-74m), but then this is probably a partial reversal of recent misplaced optimism for the stock.

We still contend that the time to buy this is on the first ahead statement, and this looks like it’s at least 18 months away now. However, assuming the dividend forecasts are not changed by this update, they are on an 8% yield, and maybe an 8ishx P/E, so any further significant falls may start to make it interesting to income/recovery investors.

Portmeirion (PMP.L) - Placing

Our reliance on government initiatives to shore up the finances here looks misplaced as they announce a large placing to improve the balance sheet. They are raising £17m at 50p plus a £2m offer for existing retail shareholders.

We love British understatement as much as the next guy, but for those who are wondering, the actual figure is something over 200%!

The Group acknowledges that it is seeking to issue new Ordinary Shares significantly in excess of 10 per cent. of its existing issued share capital...

On the positive side, this seems excellent news for the people of Stoke, and I hope that it marks a turning point in the fortunes of their pottery industry. On the face of it, this recapitalisation, and the refinancing/sale-and-leaseback it enables, solve Portmeiron’s liquidity issues in the medium term, giving them the best possible opportunity to restructure into a profitable business.

Given the level of cash raised, the irrevocable undertakings for the GM, the risk level has materially reduced here. However, so has the upside of any recovery if/when it comes.

That’s it for this week. Have a great weekend!