Small Caps Live Weekly Summary

Property FRAS JOUL VTU VLX DRV SNWS GDP

Another interesting week. Many US large cap tech companies that were sold off last week on disappointing Q4 earnings outlooks made a big comeback this week. The catalyst for this was a lower-than-expected US CPI print. While this certainly helped UK market sentiment, any rises over here were a bit more haphazard. Higher-risk mid-caps were perhaps the main beneficiaries, although many smaller caps remained becalmed. This suggests that the big rises may be driven more by short-covering than large amounts of fresh capital. The biggest index rises tend to be the bear market rallies, so it is not yet clear whether this marks a more permanent change in sentiment. It seems the average small-cap investor is still a little shell-shocked by the markets in 2022 and it will take a more consistent wider market rally before small caps start to catch up.

Despite all the market excitement in the US, it was relatively quiet this week on the SCL discord, reflecting the lack of a lot of interesting small cap news. Next week is likely to be quiet too since many of the SCL contributors will be at Mello in London, including the three of us. Mark will be doing a talk that challenges one of the sacrosanct beliefs of UK investors, that dividend investing is a good idea.

This event is well worth making the effort to be there. And if you haven’t yet got tickets yet, use the code SCL50 to get a bargain discount.

Large Caps Live

This week on Large Caps Live, WayneJ takes a look at US property, the Japanese Yen, AT1 Bonds, and Frasers. Check out the full discussion on the discord thread.

Small Caps

Joules (JOUL.L) - Business Update

The poor trading continues:

Since its previous trading update, the Group has seen the continuation of the trends highlighted in the 19 August trading statement.

Not helped by the weather this time:

In addition, whilst dresses, menswear and more formal product categories have performed well, larger core categories such as outerwear, wellies and knitwear have been impacted, in part, by the milder than expected weather.

And Garden Trading joining the rout:

UK wholesale for the Joules brand has performed well and has been in line with expectations, however wholesale performance overall has been impacted by underperformance across Garden Trading and US wholesale.

We already knew they needed fresh equity, and now some form of CVA is in the mix too:

Furthermore, the Group is continuing to progress alternative options with the assistance of Interpath Advisory, including CVA planning, in conjunction with the equity raise referred to above.

They were already in dire straits but the above makes things even worse:

The trading underperformance mentioned above has resulted in the Company's working capital position being below expectations. Net debt at the end of October was £25.7m with headroom of £11.4m. However, this headroom is reduced by £5.6m of 'trapped cash' (i.e. cash held in transit by payment providers etc) and would also be reduced by repayment of the £5m short-term RCF ("STRCF"), due for repayment on 30 November 2022.

And now they have a deadline, which they won’t meet without bridging finance from Tom Joule:

The Company is currently in discussions with Tom Joule and its lender in regard to a bridge financing proposal in order to enable continued progress to be made with the re-financing plans referred to above. However, there can be no certainty that any bridge financing proposal will be agreed, nor as to its terms, in which case the Company expects it would be unable to repay the STRCF on its due date for repayment.

Given that it could be all over for the company in under three weeks unless Tom Joule stumps up the cash, we are surprised that the share price was not down further in response to this.

Vertu Motors (VTU.L) - Potential Acquisition

Following the announcement of a small acquisition last week, we said:

We strongly suspect that there is another acquisition in process since have yet to see any further share buybacks. On 1st July they announced the £3.5m acquisition of Wiper Blades and they bought back shares the previous day. Our hope is that the rationale behind this is more compelling (if it ends up being completed.) Or that they are the ones being acquired at a healthy premium to book value, of course.

This week sees some details of this more major acquisition:

Vertu Motors confirms that it is in advanced discussions regarding the potential acquisition of Helston Garages Group Limited, a privately owned predominantly premium manufacturer automotive retail group based in the Southwest of England. These discussions may or may not lead to a transaction. Funding for the transaction, were it to occur, would be from re-financed and new debt facilities, including long-term mortgage funding.

Helston did £31.1m EBIT last year, but the Vertu CEO, Robert Forrester, has said in interviews that they won’t pay up based on multiples of peak earnings. In a normal year, Helston does £12-14m EBIT. So the comparable valuation with the listed dealers who are on 5-6x normal EBIT at the moment would be £60-98m.

However, Helston’s accounting net assets are £136m with only tiny amounts of intangibles as yet accounted for. And Vertu has paid something for goodwill on acquisitions in the past. They can afford to pay a bit more due to the added scale and benefits of implementing their IT systems etc. The main uncertainty over the purchase price relates to what assets are included. Though they prefer owning (in this case likely with mortgage funding) strategic sites they could lease others from the sellers or sale and leaseback prior to completing the deal.

Vertu will take the bulk of the group but not all of the sites according to this article:

South west based Helston Garages Group is set to be broken up and sold to three dealer groups. Vertu is expected to take the majority of the dealerships with neighbouring Yeomans taking the Volkswagen Group franchises and Rybrook taking the Porsche operation.

Any debt-funded acquisition of this scale will be highly earnings-enhancing to an already cheaply-rated Vertu. We just hope they don't overpay when they could have bought back a shedload of their own shares at a very material discount to their own TBV recently, which may have been even more earnings-enhancing.

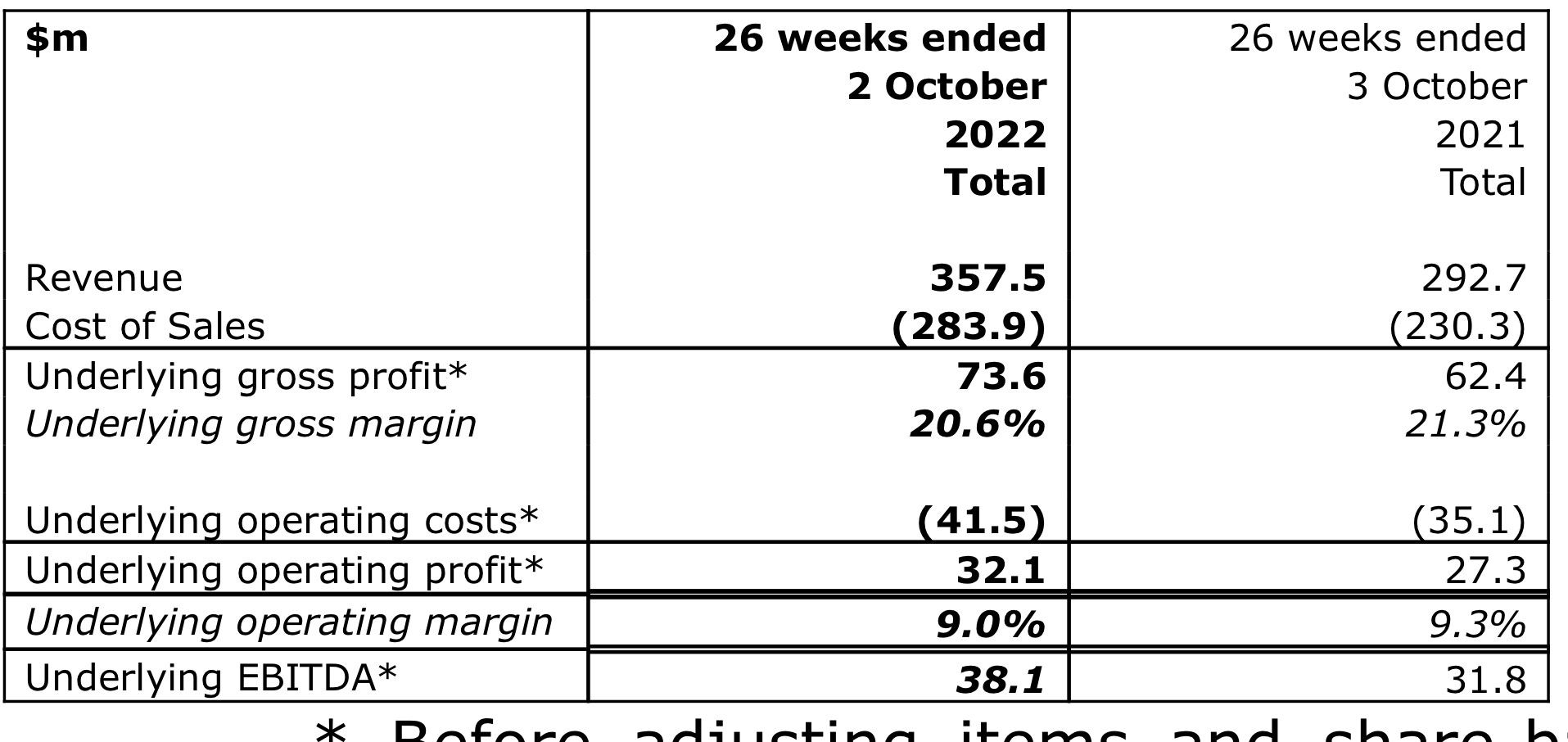

Volex (VLX.L) - Half-Year Results

This is a highly acquisitive group, so it is always best to look at organic growth rates. In this case, the 14% organic revenue growth sounds good, although this may just be their cost increases, given the inflationary environment. They don’t seem to share the organic profit growth figure which is perhaps more important. The underlying Gross Profit Margin falling suggests they have struggled with this:

There are big adjustments, but most of these are intangibles amortisation, not cash costs:

Adjusting items and share-based payments totalled $7.6 million in the period (H1 FY2022: $6.1 million). These costs are made up of $4.3 million (H1 FY2022: $5.0 million) of amortisation of acquisition-related intangible assets, $2.6 million (H1 FY2022: $2.6 million) of share-based payments expense and $0.7 million (H1 FY2022: $1.1 million) of acquisition costs mainly related to on-going activities to develop our acquisition pipeline.

This is a serial acquirer, so the cautious will want to add back cash acquisition costs and take the fully diluted share count for EPS. The cash flow isn’t great here, and net debt has gone from $40.1m to $117.0m. The comments on working capital suggest that of the inventory build, not all will unwind. And contingent consideration of around $60m eats up cash and is not included in Net Debt.

Going forward they say they are in line with expectations, but these expectations have been trending down for a while now:

Hitting these reduced expectations would put them on a forward P/E of 12. While not crazy, this isn’t exactly cheap when you adjust for dilution and the approximately $170m of debt and contingent consideration owed. Adjusting for these factors, the P/E would be closer to 20, which is high in the current markets.

Driver (DRV.L) - Trading Update

The full year is confirmed as loss-making:

The Board can confirm that it expects to report an underlying* loss before tax of £0.3m for the financial year to 30 September 2022, before one-off Middle East reorganisation costs of £0.6m due to the Middle East and APAC issues announced on 23 May 2022 (the "Middle East Update").

This is entirely down to the issues they have had in APAC & ME, since they also say:

The Group's UK, European and North American offices have had another strong and profitable year within management expectations, delivering an operating profit of £4.2m; group central costs were £2.4m. The UK team has successfully grown with a series of expert hires, and the expansion of the team in mainland Europe has contributed to the delivery of regional profits.

This business would clearly be worth a lot more if they only had the UK/EU/NA operations. They continue to take cost out:

Management have implemented plans to scale costs back further, to account for the lower revenue expected as a result of the Middle East and APAC reorganisation.

Which is having a positive impact:

Driver's management expect to see the business return to profit in Q1 of the new financial year, and to realise further performance enhancements in Q2, based on the prudent steps it has taken to identify and implement additional improvements.

And net cash is building again:

The Group had a healthy net cash position on 30 September 2022 of £4.8m, which reflected significantly improved collections in the year, particularly from the long-term debts in the Middle East, which are now markedly reduced.

If they can get APAC & ME back to break even, then the strong performance of the rest of the business, plus large net cash balance, perhaps more than justifies the current share price. Given the history of issues here, then the market wants to see it to believe it.

This is often described as a company that would make more sense as part of a larger consultancy business. There would be significant cost savings from not being listed. Plus, a business with existing scale can merge the APAC/ME into their existing operations and take the necessary action to either close, merge or rationalise these. This is a case of a business that should genuinely be worth much more to an acquirer than listed. So far, this logic has not led to any offers, so we are not holding our breath on this one.

Smiths News (SNWS.L) - FY Results

These read well:

Although, it perhaps makes sense to use the unadjusted figures. Bad debt from doing business in a declining industry could be considered normal business. This still trades on a cheap multiple even on the unadjusted figures though.

Net debt is down significantly but largely due to one-off factors. Average net debt is the more useful figure here given the negative working capital. This is down as well and now around £50m which does seem excessive.

Outlook is in-line with cost increases being well managed:

The new financial year has started well. Trading to date is in line with expectations, and in October 2022, contracts representing 35% of newspaper and magazine sales revenues, were renewed until 2029. Despite recent economic volatility, inflationary pressures continue to be consistent with planning assumptions and the combination of sustained margin mix and close cost control give us confidence in maintaining performance in FY2023.

So overall, a decent set of results, but at the end of the day, you either trust the managed decline will generate more than the current market cap or not. This business will decline to zero eventually. And nothing in these results will change opinions on the stock either way.

Goldplat (GDP.L) - Q1 Operating Results

Their operating profits doubled vs last year, although helped by FX movements:

The two recovery operations continued the strong combined operating performance of the previous quarter and achieved a combined operating profit for the quarter of £1,942,000 (excluding listing and head office costs and foreign exchange losses) which represents a 38% increase against Q1 in the previous period (Q1 2021: £1,403,000).

What didn’t help was the intermittent South African electricity grid supply and political events in West Africa. So given that this was a challenging period due to external factors, this is a great result.

They strengthened their relationship with DRDGold, through the ability to process material from DRD not just send their tails the other way for processing. This should provide a lot of stability of supply for the CIL circuits for many years. The Tailings facility being processed by DRD via pipeline is now officially confirmed by the company, although commercial terms are not yet signed and there has been a small delay to the permitting for the pipeline.

Their PGM circuits are taking a little longer to get going than planned, but the issues now look largely resolved.

Cash balances look strong despite some reasonable capex requirements in the quarter:

Cash balances in the group remained strong at £2,920,000 at the end of Q1 (Q1 2021: £2,340,000), (Q4 2022: £3,672,000).

Although they are quoting net cash not gross cash here, as they had £2.5m of debt at the start of 2022, which they took on to buy out their minority partner in South Africa. Some of this debt will have been paid down during the year, however. We are still waiting for audited results to 30th June to get more details. This reflects the complexity of the business plus the disruptions the audit industry has faced. They now say:

We are currently estimating to announce the Group's audited annual results towards the beginning of December 2022.

If the company performs similarly to Q1 for the rest of the year then they should deliver around 3p EPS. Perhaps higher, if some of the ongoing issues are resolved, and recent rises in the gold price stick. Even after recent share price rises, this still looks very cheap. Although, as ever, it remains a risky stock.

That’s all for this week. Have a great weekend and see you all at Mello next week!