Small Caps Live Weekly Summary

SBRY MKS UPGS TGP STAR MACF

It was another quiet week, and with most people making the most of some nice weather, share discussion was not always top of the list. Feels like the interest is starting to return to some small cap though, so maybe better times ahead.

Mark found the time to talk to Jon Kingston on the Capital Employed podcast. So check it out.

There will be no Large Caps Live on Monday due to the UK Bank Holiday.

Large Caps Live Monday 23rd August

Supermarkets (SBRY.L MKS.L)

Sainsbury is now in the frame for a bid. Morrison has agreed to be acquired and Asda has been sold by Walmart (albeit retaining a small stake). The key points about all three companies (and Tesco) is:

(1) They have large property assets – which are often not marked to market in their books.

(2) They have relatively stable top lines (at least on the food side - barring the upside from WFH / Covid)

(3) They are (I reckon) underleveraged in the eyes of private equity.

(4) They generate a lot of cash flow – which at the moment is ‘diverted’ into dividends. E.g. this morning, Sainsbury’s was on just under a 4% dividend yield.

(5) Supermarkets have large sites – if the supermarket is not viable then some of those sites are probably worth significantly more as land for housing (subject to change of use).

So I have been thinking about what I would do if I was ‘private equity’.

(1) Typically private equity starts by putting in 25% of the deal value and then does aggressive ‘equity extraction’ to take it down to 15% or so.

(2) Sell some assets to cut your ticket price. I believe that in one of the bids the buyers have already sold some of the distribution warehouses on a sale and leaseback basis.

(3) On 25% equity you get decent 10% plus returns for a decade.

(4) It is even higher if you assume 15% equity.

Obviously, the world was worried about online sales cannibalising supermarket sales. BUT my suspicion is that actually, it will allow supermarkets to reduce their physical footprint but serve the same number of customers ie rather than have 10 supermarkets serve a town cut them to 5 with lots of home delivery.

Ok so what else will private equity do?

(1) It will squeeze its suppliers. I was intrigued to find Sainsbury’s declares its marketing and advertising income. The following table also included the ‘fixed amounts’ that Sainsbury is paid to promote products in store. The advertising income line includes ads in the Argos Catalogue (no longer going to be printed) and Nectar related ads.

(2) I think advertising by the supermarkets themselves will be cut back. I tried to find how much Sainsbury’s spends on advertising today but could not. I suspect this has implications for TV etc

(3) I note that Sainsbury’s already has a supply chain finance arrangement for suppliers who want to be paid early. I assume supermarkets will hold onto cash longer.

(4) Sainsbury bank has £849M of equity as per the end of 2021. It will not surprise me if the bank is either sold or its balance sheet is used to help fund the acquisition.

For an investor, I think the key question is where else can I find hidden value and an attractive cash flow that hopefully PE will come along and buy. So which one next? I have mentioned M&S before. So what is the hidden value in M&S?

Today, 18th August 2021, M&S has launched an expansive range of M&S food products on worldwide export platform British Corner Shop, enabling customers in over 150 countries to buy their M&S favourites for the very first time.

I have no idea who owns British Corner Shop or if it will have significant sales volume but it does highlight a point of mind – I think the M&S brand has a degree of global appeal/reach that is underestimated by investors and even the company itself. Bear that point in mind as I think the appeal applies equally to M&S food and to M&S clothes.

Now one of the key differences between M&S and the big supermarkets is a lot more debt. The last results state £3.54bn or excluding leases we get £1.11bn. It is worth remembering (as I think I have mentioned before) that M&S sold a bunch of freehold on sale and leaseback to avoid hostile bidders early in this century.

Put another way M&S with a market cap of £3.19Bn has net non-lease debt of £1.1bn vs the £640 M we mentioned earlier for Sainsbury with about twice the market cap. I think that after Sainsbury’s, M&S has to be having an eye cast on it by private equity. The clothes mix might put them off but as I said above and previously, I think there is considerable opportunity here (especially going online, just in time and internationally).

Small Caps Live Wednesday 25th August

UP Global Sourcing (UPGS.L) - Trading Update

Compared to some of the recent updates this was relatively tame. FY 2021 revenues came in slightly ahead of expectations. There was only 2 weeks contribution from the Salter acquisition which we estimate to be £0.6m

They've clearly guided Equity Development higher on FY 2022 margins since they have raised their profit forecasts without raising revenue forecasts. Traditionally they have always forecasted just 6% revenue growth until the first trading update comes in. LFL their FY2022 forecast implies about 6.8% this time.

In the statement, UPGS say this for current trading/outlook:

· The FY22 order book for the core business, excluding the effect of the recent Salter acquisition, is ahead of this time last year

· Shipping availability continues to present challenges with forward orders from the Group's retail customers being prioritised ahead of stock purchases. Management expects that global shipping will remain disrupted until after Chinese New Year (February 2022)

· Current trading remains in line with expectations, with growth expected in FY22 both from the core business and through the acquisition of Salter

Order book "ahead" doesn't sound desperately strong. Not "materially ahead" or anything like that. And actually, an order book ahead could just mean that people are ordering earlier due to supply concerns. Well, as per the above, the order book is ahead of 2019 also. The best thing is probably reassurance on shipping. It is also too early to tell how well Salter is going.

Perhaps this line indicates further small acquisitions are still possible:

Net bank debt/underlying EBITDA ratio of 1.4x at 31 July 2021 (31 July 2020: 0.4x). The Group maintains comfortable levels of headroom within its bank facilities, with headroom at 31 July 2021 of £16.2m (31 July 2020: £21.3m)

Maybe it is a message to retail customers to get their orders in? They are always going to prioritise long-term customer relationships over D2C. Just like their suppliers prioritise them.

Anyway, the ED note is worth going into a bit more detail. The key line here is, I think, something I have pointed out many times before:

…it may be worth noting that this is based on an underlying organic sales growth expectation of just 6% which would be well beneath the 11.5% compound growth rate which the company achieved in the 5 years to FY2021.

That 5 years included a very nasty glitch. And again, I think Germany has much further to go:

Within the important growth driver of international, Germany remains the largest contributor and appears to have performed strongest.

Supermarkets probably benefited the most from covid, so that sector may be more of a challenge. So really, nothing changes here. The forward PE ratio is much higher than it has been in the past, but not as high as it was pre-Salter acquisition. Forecasts can be expected to be beaten, barring unexpected problems.

As the company gets larger and the time since the 2018 setback gets longer, I think a higher valuation will be justified. For the moment the 16.4x quoted by Stockopedia seems fair.

Small Caps Live Friday 27th August

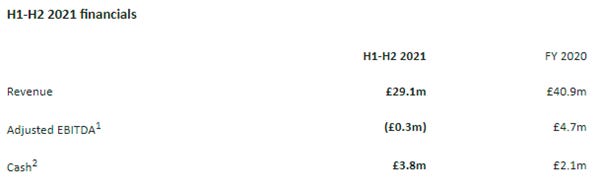

Tekmar (TGP.L) - Change of Auditor

With Tekmar, you have a very large Total Addressable Market (TAM) with wind farms predicted to grow 15% for the next decade, and Tekmar has a market-leading position in cable protection. So why is the share price close to all-time lows?

Well, on scl, we have been consistently worried by the state of the balance sheet. The proportion of receivables that were made up by unbilled revenue, which remained persistently high despite a drop in revenue, and the need to access CBILS finance, were just a few of the concerns we had.

On top of this was the news that there was an issue with the cable protection systems on one of their historical projects. It is not clear whether there is any liability here, but if there is, the sums involved are a major problem for Tekmar.

With this going on, it is perhaps not surprising there have been a number of board changes. The founder CEO left pretty suddenly. The Chairman gave up his non-exec role to become CEO, perhaps feeling a sense of responsibility to put the company on an even keel, but this is an unusual move for a non-exec. We felt that a strong CFO is key in these sorts of situations, and our impression was that this area may be lacking. So perhaps good news that in June we got a change.

However, with all this going on, today’s news – a change of auditor - doesn’t read well. It may just be a new CFO making his mark, but a shift from KPMG to Grant Thornton is rarely the direction you want from a company. GT will audit the results to 30th September.

A change of reporting period confuses matters somewhat, but given the last results, we doubt these will be great:

(That cash figure is really down to £0.8m on a net basis.)

We will definitely be watching with interest what the GT audited results look like when they are out. Before we have these, I’m not sure this can be considered investable. And if the figures start to show growth in line with the TAM, then there will be plenty of time to jump on this multi-year trend, with a much smaller chance of a nasty surprise on the downside.

Starcom (STAR.L) - Interim Results

Mark is never scared to look in the micro-cap bin for a bargain. Starcom recently came to his attention as it seems to be a real tech business trading close to all-time lows:

The years of persistent losses presumably being the cause:

These microcap loss-makers can make great investments just before the shift to profitability though, so forecasts matter. However, in this case, these 2021E numbers are clearly nonsense:

This shows why it’s always worth checking where forecasts come from before investing. Today’s results for the six months to 30th June don’t really give any hope of significant growth in the future:

COVID is the reason given:

I am delighted that despite the continuous challenges Starcom faced due to the COVID-19 pandemic we managed to show stable results with increased opportunities in the future. We now have several sales prospects we hope to convert when conditions permit, and I am confident that Starcom technology will continue to create value in this and following years.

This may well be true, but many companies have shown a significant recovery in 21H1. They do have some interesting technology though:

Further to the previous announcement regarding the cooperation with DHL, we can now update that DHL's proof of concept ("POC"), intended to ascertain Lokies's fit for DHL's monitoring of its fleets operation, is expected to be completed in the next couple of months.

DHL is a big potential client for such a small company and a big vote of confidence for their technology (assuming the contract gets signed.)

However, as usual, the balance sheet reveals the problems: Current Assets of $3.3m and current liabilities of $3.4m, cash and short term deposits are $476k, but short-term loans have gone from $137k to $958k. With no significant tangible asset backing, I don’t see how they can leverage themselves much further. So, it is unclear how they would fund the working capital of a large contract win.

Fundamentally, they just seem subscale to be listed. They haven’t generated any growth for years. Given the tough environment, they are focussing on costs control:

Starcom also continues to monitor and reduce the level of general expenses.

But this doesn’t get them out of it, at this stage, they need revenue growth, not cost-cutting. And DHL might provide that, but then it looks too late for their balance sheet to be able to support that growth without fresh equity. Starcom remains in the microcap bin.

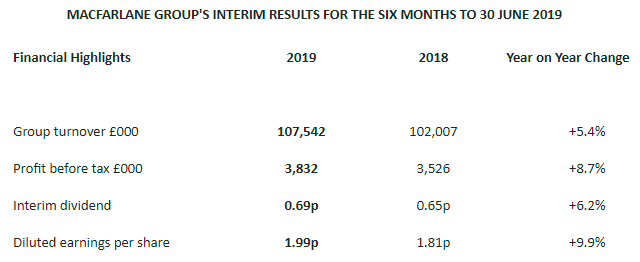

Macfarlane (MACF.L) - Half-Year Results

One of the best performers on Thursday was Macfarlane - the packaging company. Looking at the commentary on Twitter yesterday, following their results, Mark wondered why he didn’t own it.

Impressive growth rates there. These helped the shares push to all-time highs:

Although vs a period that was covided. But these read well vs 2018/19 too:

One of the things to be aware of is that there are acquisitions in here:

The acquisitions of GWP Holdings Limited ("GWP") and Carters Packaging (Cornwall) Limited ("Carters") in H1 2021 have contributed £8.1m of sales and £1.9m of operating profit before amortisation and impairment versus 2020.

So those growth rates are not really fully organic. The other reason that I have never considered investing in Macfarlane is the balance sheet. The current ratio has always been low but has dropped below 1 with this set of results. Part of this is the ramp-up in debt, due to acquisitions, but this raises the question of why fund acquisitions with short-term debt unless you are forced to.

Payables are greater than receivables. By my calculations, they are paying suppliers on an average of 122 days. I can't imagine their suppliers being too happy about that. If you normalised that to 90-day terms, then this would add another £15m or so to their debt. Which would blow through their debt facility:

So, yes, they are operating well within their facility, but only because they pay their suppliers much later than the typical terms you see for most companies.

Some good news is that they no longer have a pension deficit on an accounting basis:

The pension scheme was in surplus at 30 June 2021 compared to a deficit at 31 December 2020 of £1.5m. The improvement is due to continued contributions from Macfarlane Group and an increase in the discount rate, offset by lower investment returns during the period.

But this is partly due to their contributions (which go through the cash flow statement but not the income statement):

In their 2020 annual report they say:

Following the triennial actuarial valuation of the scheme at 1 May 2020, the Group agreed a new schedule of contributions with the Pension Scheme Trustees, which assumed a recovery plan period of 4 years. Annual contributions will reduce from the current level of £3.1 million to £1.3 million with effect from 1 May 2021. The next triennial actuarial valuation will be carried out at 1 May 2023.

So we can expect 3 more years of recovery payments. Assuming normal pension agreement terms, these don't just disappear because an accounting surplus has occurred. Given the debt, working capital features and weak balance sheet, the forecasts don’t exactly make this look cheap either:

But part of the bull case is that these are to be beaten. After all, they say:

· The Board expects that the Group's full year outlook for 2021 will be ahead of its previous expectations, despite the challenges we are expecting in H2 2021.

Fair play to the company, they quote basic EPS without doing extensive adjustments that more aggressive companies would do, and leave you to make your own adjustments. Again, this is from the cash flow statement:

Bullish commentators may like to exclude a lot of these costs. However, share-based payments really are a cost to shareholders, for example, so in my opinion, it is right to include them. There can be a lot of debate over whether amortisation of intangibles or goodwill impairments should be excluded. I think Goodwill as a one-off may make sense to exclude, but given that this company is a serial acquirer then including intangibles amortisation would seem sensible to me.

Personally, I would also make an adjustment the other way and subtract the pension payments from profits, as an effective cost borne by shareholders over the next three years.

To overcome the extra risk that shareholders take by investing in a company with such a weak balance sheet they’d typically want exceptional value to be on offer. And it doesn’t seem to be there unless one is very aggressive with one’s adjustments to EPS.

That’s it for this week, have a great long weekend!

Just really enjoying reading these weekly summaries. Found via a podcast on card. Thx