Small Caps Live Weekly Summary

MRW CAPD VTU MSI STAF JOUL RBN TND

Large Caps Live Monday 21st June

Morrisons (MRW.L) - Takeover

So over the weekend, we had a story about a takeover of Morrisons by Clayton, Dubilier & Rice – a PE shop out of NYC. The chart shows the impact today:

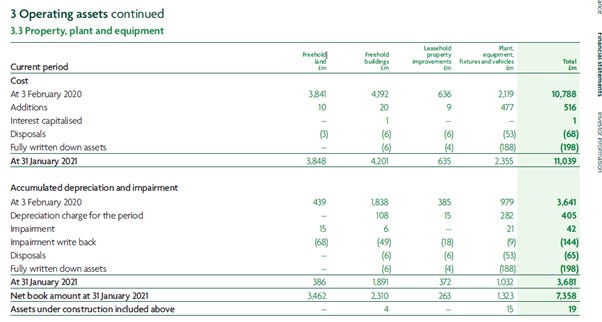

The market cap is currently £4.3bn with an EV of £7.47bn. At the weekend we touched on property within supermarkets in the #general chat. So let’s look at Morrisons. In the 2020 – 2021 accounts – page 79:

And from here we can see that the buildings are depreciated over 40 years but the land is not depreciated (which is normal):

If we look further we can see the cost of the property:

So we have the cost of freehold land of £3.8bn and buildings of £4.2bn giving us a total of £8bn. Now there is a massive issue with Supermarket property – which is that it is a big chunk of the balance sheet – and is not revalued annually (usually) into the accounts. So it is great to say that the depreciated net book value of the above property is £3.4 + £2.3 = £5.7bn. But what is the current market value?

Was the land bought last year – or 30 years ago in which case there is a massive valuation uplift. That of course also depends on the ability for change of use – eg take a 50k sqft supermarket and the associated car park (often the car park is the key point as it can be 2/3rd of the site) and get planning to convert the whole site to housing. And Bob – as they say is Hilda’s Uncle.

The lease liabilities will be offset substantially by the right to use. And the company has about £2bn of borrowing (long and short term). So putting this together I would add £2bn to the market cap of MRW to get an EV of about £6.3bn

The total equity is £4.2bn. However, as a rough guess, it would not surprise me if a bullish investor added 50% to the value of the land and property to get an additional £2- 2.5bn or so (total finger in the air) – which means that even with today’s rise in price the company is trading at about 1x price to tangible book.

[Lots more on the other supermarkets and interest rates on this week’s LCL, so check out the full discussion on discord if you are interested. A Discord server invite is here.]

Small Caps Live Wednesday 23rd June

Capital Ltd (CAPD.L) – Director Placing

It is a shame to see another founder sell some down at Capital Ltd. After all, the drip-drip selling of another founder, Craig Burton, effectively led to a poor price for the placing to fund a large contrcat win. At least this placing is done via the broker.

I suspect these will be easily placed but does remove some of the institutional demand in the market which is often key to seeing big upward moves in the market. The other things that moves the market are trading results. The price of gold, and therefore gold companies have been weak in the last week following the fed announcement we discussed on Large Caps Live. So, is Brian Rudd calling the top of the rig market?

I don’t think so, for these reasons:

The weakness in the gold price has been largely dollar strength rather than gold weakness. This affects sentiment but not so much the economics of companies operating in non-US countries and listed on UK exchanges.

Rig spend tends to lag the raising of money by 6 months to a year, and April 2021 was a record month for this activity:

On 15th June competitor Major Drilling said:

Looking ahead to fiscal 2022, we continue to see a noticeable increase in inquiries from all categories of customers, and if their plans progress as advertised, we expect to see utilization rates continue to improve as crews become available.

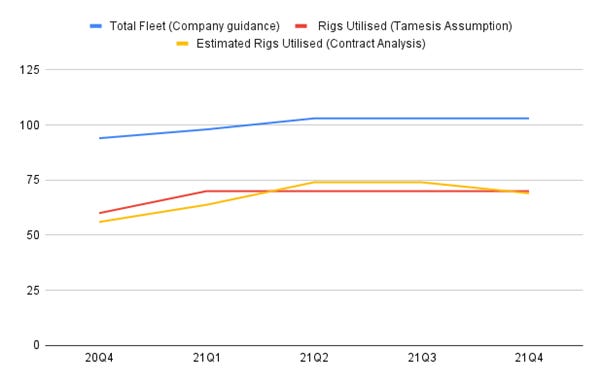

Examining the announced contracts and starts of drilling the company appears to be on target to at least meet, if not exceed, Tamesis projections for active rig numbers:

The Tamesis number for non-drilling services looks too low as well based on how we know the major contracts are performing.

So, although another director sell is not the next news we would have hoped for from Capital, I expect this is part of normal retirement planning, or the desire for a new house (which aren’t cheap in Australia!) rather than a specific call on the company’s future trading prospects.

Vertu Motors (VTU.L) - AGM Trading Update

Stock markets are supposed to look forward, but in the reopening trade, it seems that those companies that are already doing very well are currently valued less highly than those who might perhaps hopefully do well at some point sometime in the future.

In the former group airlines and pubs are trading at similar share prices to two years ago despite profitable reopening continuously being pushed back, long term structural issues, and in many cases significant new share issuance.

In the latter group, while the likes of ScS and Vertu have nominal share prices up over two years, that is from a cheap base, trading is booming, with little end in sight, they have made significant structural business improvements and they are much more likely to be buying back shares than issuing them.

According to Stockopedia Ryanair is now on a forward PE of 50x compared to 8x for Vertu. And both those forecasts are out of date, with the outlook for Ryanair now worse and the outlook for Vertu now better:

To date the Group has seen a continuation of the strong trading trends witnessed in March and April as explained in the year end results announcement released on 12 May 2021. If these trends continue, a strong first half financial performance is anticipated, however, there remain risks in relation to the remainder of the financial year concerning potential COVID-19 disruption and vehicle supply constraints.

Concerning the first risk, vehicle supply constraints is more than just a risk, it is a fact of life for car dealerships right now. They continue:

A tightening of new vehicle supply, largely reflecting component shortages flagged in the year end announcement, is increasingly apparent.

So it sounds like the well-publicised problems continue to worsen.

The expected time between order and delivery of new vehicles to customers for certain of the Group's franchises is now seeing elongation.

The analogy with ScS is interesting here. The question is what does a customer do when faced with increasing delays? Do they a) Buy from somewhere else, b) Delay their purchase, or c) Get in that queue ASAP?

Option (a) basically effectively means going down market in Vertu’s case, an unlikely choice for people with money in their pocket. I’m sure some people will go for (b). But the evidence from the great toilet roll shortage of 2020, and from ScS’s trading, is that most will go for (c).

But car dealerships have a particular advantage when supply is short:

The used car market remains very robust from a demand perspective. The reduction in new car supply is contributing to a reduced supply of used vehicles, with a resultant exceptional wholesale pricing environment.

Higher prices mean higher profits at a particular percentage margin, plus higher margins due to customers less able to negotiate, and a revaluation of cars on the forecourt (although this one-off profit will unwind later).

This leads to the following guidance:

In light of the strong trading performance to date, driven largely by the exceptional used car market environment, the Board now anticipates that the Group's full year adjusted profit before tax will be above current expectations and in the range of £28m - £32m.

How does this relate to EPS? Zeus Capital now forecast 6.2p EPS, commenting:

We have increased by 2022E EPS forecasts by 15.5% taking the mid-point of revised management guidance.

Remembering that Vertu have tangible net assets of 50p a share, this makes the current 46.5p share price look pretty cheap. But, in my opinion, here’s the best part of the note:

While we are just four months into the H1 period for Vertu, we would anticipate the H1/H2 split to be significantly ahead of the normalised c70/30% PBT split this year.

Given that they spent 25% of their H1 closed (except for click and collect), a split “significantly ahead” of the norm for H1 seems unlikely and I see a significant opportunity to beat implied H2 forecasts. So why would the guidance be so conservative? I see several reasons:

They don’t need to raise any money in the market, so why not?

Supply concerns

COVID disruption concerns.

Now while COVID may yet disrupt factories in anti-vax Germany, I just don’t see any disruption on the retail side. I think the psychology of CEO Robert Forrester is relevant here. As well as being very pro-car and the future of individual car ownership, he is also decidedly on the anti-lockdown side of the argument, though I should say not rabidly so. Both these positions strike me as wishful thinking (caused by him being a car dealer) and there is plenty of evidence the extension of restrictions came as a shock to him. For example, today's AGM was advertised as going ahead normally even when this looked unlikely, and he has restart mass meetings of managers today. In fact, attendees to today's AGM are/were actually allowed, with precautions, just not recommended. I don't think I've seen this for any other company.

So I don’t think the CEO understands why the end of restrictions was delayed and on that basis is cautious that he might be shut down again. However, my opinion is that the delay to relaxations virtually eliminated any chance of him being shut down again by preventing uncontrolled spread, and despite being broadly on the pro-lockdown side myself, I actually think his instinct that car showrooms are some of the safest places to be and that it is safe to hold an indoor maskless meeting of scores of senior (and therefore fully vaccinated) managers is right.

MS International (MSI.L) – Final Results

MS International released their results to 30th April yesterday:

Investing in MS International is a bit of a value investors right of passage, the cycle goes something like this:

Ooh this looks cheap, has net cash and is trading well. It is illiquid but I’ll risk it.

Hmm, that last trading update wasn’t great. And hang on, that balance sheet isn’t as good as I thought. This isn’t as cheap as I first thought.

They are now loss-making, they don’t respond to shareholders readily, the management are on £200k-£500k each despite the losses! And there is a pension deficit. This is uninvestable.

Ooh this looks cheap…

We are currently in stage 1:

The Company returned to profits with a pre-tax figure of £1.59m (2020 - loss £3.25m) on revenue of £61.54m (2020 - £61.15m).

Basic earnings per share amounted to 7.2p, (2020 - loss per share of 15.1p).

The balance sheet has strengthened, with total cash increased to £23.56m (2020 - £16.30m).

After a c.20% rise yesterday to 194p this puts them on a 27xP/E. At a £32m market cap with £23.6m in cash, this looks like the cash-adjusted P/E may be a lot lower.

However, I think that may be a mistake. With payables and contract liabilities totalling £33.6m and receivables, contract assets and prepayments totalling £13.4m. Then netting these off, the real cash that could be distributed to shareholders is looking more like £3.4m. Then there is a £7m pension deficit. This varies with the vagaries in interest rates but it is costing them £600k pa in recovery payments, which is a third of last year's pre-tax profit.

So it would seem wrong to cash-adjust that P/E at all and we have entered stage 2 of the MSI cycle!

The market is, of course, forward-looking, so the announcement of a US Navy win is perhaps why the market reacted so positively yesterday:

Pleasingly, a request from the US Navy, that we field our 'state of the art' 30mm MSI-DS naval weapon system for an evaluation trials programme resulted in a highly positive outcome. We have since been awarded a contract for the supply of seven systems, the first of which has now been delivered directly to the US Navy. We are hopeful that these sales may well lead to follow on production orders. In addition, following the award of that contract, we received an order from a US shipbuilder to supply eight similar weapon systems for a US government Foreign Military Sales Programme.

Plus, they are back paying a reasonable dividend:

All matters considered the Board recommends the payment of a reinstated final dividend of 6.5p per share (2020 - 1.75p) making a total for the year of 8.25p (2020 - 3.5p).

With no figures given for the defence orders and no forecasts in the market, then to buy now you are placing a lot of faith in the future earnings, which have proved to be very lumpy in the past. There is a risk that recent buyers will be entering stage 3 of the MSI cycle sometime soon.

Staffline (STAF.L) - 2020 Results

Staffline issued their delayed results on Tuesday. Looking at the accompanying going concern statement, it is likely they needed to get the recent fundraise away first to be able to publish these on a going concern basis.

With the raise completed, they can focus on future trading:

Trading across the first three months of 2021 was strong and underpins our confidence in meeting expectations for the full year. Having now strengthened our financial position through the recent fundraising and debt refinancing, we truly believe we have a platform from which to deliver meaningful growth as we are already seeing a stronger pipeline developing across all of our divisions.

So, basically no news on the outlook. But why would they big themselves up now? They've just refinanced. The objective now is to consistently hit and preferably beat broker forecasts, rebuilding a track record. (Oh, I should say that the results themselves were in line with well-trailed expectations.)

After we last talked about them they did dip back to the fundraising price and I picked up a few more, but I don't expect many fireworks in the short term. I supposed it is noteworthy that the H1 results are now due in only 10 weeks, but I don't expect a trading statement in the meantime.

The balance sheet still isn’t the strongest despite them raising their market cap again in fresh equity. The pro-forma current ratio is still only around 1 and they have negative tangible assets. This still makes them on the risky end of the spectrum.

Throughout these last 2 years of chaos, they have consistently emphasised their strong cash flow. Part of this may be due to recievables financing, though:

The new facility enabled the cancellation of the existing facilities, comprising the RCF of £20.0m and the RFF of £68.2m and also the non-recourse Receivables Purchase Facility of £25.0m.

Non-recourse receivables is a form of off-balance-sheet debt. Effectively, the receivables reduce by the about of the debt. So some of the cash would have gone / will over time go into increased working capital.

Joules (JOUL.L) – Pre-Close Trading Statement

Investors in Joules have done very well recently with the share price trebling in the last 9 months or so. Today we get to hear what all the fuss is about with a pre-close trading statement to 30th May:

The Group is pleased to report that revenue for the Period increased by 4% to approximately £199m (FY20: 190.8m)

This looks to be a miss on stockopedia figures, although you can rarely rely on these to be up to date. I think Liberum has £194m forecast, so this is above their estimate. On profits they say:

Profit before tax and exceptional items for the Period is anticipated to be in the range of £5.5m - £6.5m, slightly ahead of current market expectations.

This is vs £5.2-5.3m consensus. So why hasn't the share price responded to this beat? Perhaps because, even at the top end of that range, that is 5.4p EPS and this is on a P/E of around 30. And Liberum have not upgraded their FY 2022 and 2023 EPS forecasts. But they have been forecasting an increase to 18p EPS in FY 2023 from 12.5p in FY 2022, so prima facie this is a go-go growth stock.

They are clearly executing well, but in a very difficult area. When other multi-channel retailers are struggling, going bust and Joules themselves are closing stores to retain profitability, why pay up as if this is a structural growth area, rather than a company battling hard to swim against the tide?

Small Caps Live Friday 25th June

Robinson (RBN.L) – AGM Trading Update

Yesterday Robinson issued an AGM Trading Update which didn’t start well:

As we indicated in the 2020 full year results, published in March, sharp increases in resin prices, together with some lack of availability, have created volatility in 2021. As a result, margins to date are reduced.

Cost inflation is a big topic for a lot of companies at the moment as supply chains play catch up from a year of COVID disruption:

Since 1 January the market price of resins used in the Group have increased by on average 60%. There were numerous force majeure declarations by resin producers in the first quarter and no meaningful increase in imports into Europe, initially due to the large-scale, weather-related disruptions in the US and recently because of shipping container shortages from Asia. Whilst some convertors have been forced to shut down production lines, we have been successful in mitigating the substantial challenge of securing resin supply to continue to operate.

Being a 'substantial challenge' to even operate is rarely a good thing! While this seems to be particularly severe for plastics packing manufacturers such as Robinson, I don't think the rest of the industry will be immune. DS Smith was complaining about a lack of cardboard recycling. So I can see costs going up for cardboard packagers such as them and Macfarlane too. Particularly if people switch from plastics to cardboard due to lack of availability of plastic packaging.

The impact of all of this on Robinson is:

Group sales in the first five months of the year are 17% ahead of the same period in 2020, 2% excluding the impact of the recently acquired Schela Plast business. After adjusting for price changes, sales volumes in the underlying business are 1% higher than 2020, which included additional demand due to the Covid-19 pandemic. As a result of the short-term transitional impact of resin price increases on our Group, earnings for the year to date are well behind that achieved in the same period in 2020.

In their March 2021 note, House broker, finnCap had expected earnings to grow from 13.5p in 2020 to 14.2p in 2021 and 15.2p in 2022:

In their morning note yesterday finnCap say:

Robinson has provided a trading update with its AGM, covering the first five months of 2021. Revenues are tracking as expected but raw material cost increases, particularly polymers, are rising faster than assumed. Robinson can pass these cost increases through to customers (albeit with a lag) and has identified cost savings to offset loss of gross margin. As a result, we are not materially changing our FY2021 earnings forecast or target price.

Yes, there is some temporary effect in resin pricing and availability here, and over time they should be able to pass on the costs to customers. Are they really expecting them to have such a great H2 that they make up the shortfall? If they do hit finnCap’s figures they will be on a low P/E, which may attract some investors.

However, I don’t think they look good value for the following reason:

Including the acquisition, net debt has increased to £13.1m at 31 May 2021 (31 December 2020: £6.6m). This remains well within the Group's total facilities of £21.1m.

Even before today’s update, finnCap were forecasting a nominal amount of free cash flow, and net debt to continue to rise. When you adjust for this then the rating actually looks pretty demanding. The current market cap at £1.25 is c.£21m so with c.£15m net debt forecast, that is a £36m EV. £6m EBITDA gives 6x EV/EBITDA. Not crazy, but that is IF they hit those EBITDA forecasts, which I am doubting. Of course, large debt adds extra risk that should mean a lower rating too.

In general, they seem undercapitalised, so the cynic in me thinks that finnCap remaining positive may be because they will be given the task of selling any balance sheet shoring exercise to investors!

That said this is a family-owned business whose controlling shareholders like dividends and won’t like a placing so they may simply try to muddle through, as they have done in the past. I doubt I will be joining them on that muddling journey.

Tandem (TND.L) - AGM Trading Statement

Another AGM trading statement and this time from Tandem. Lots of details on growth rates of individual areas but the headline figures are what really matters:

I am pleased to report that it has continued to be a positive trading year so far for the Group, with revenue for the 25 weeks to 22 June 2021 approximately 14% ahead of the same period in the previous year…

The outlook for the remainder of 2021 remains positive. Our forward order books are at record levels with Group outstanding orders currently totalling £34.7 million compared to £10.7 million at the same point last year. Whilst this is very encouraging, it should be noted that our bicycle customers have ordered much further forward than usual, well into 2022, to ensure that they have ongoing supply in order to meet future predicted demand which may or may not materialise as envisaged. Currently, there are no signs of a slowing in demand in certain product categories such as bicycles, golf and outdoor.

All pretty good then. However, their last trading statement was only a few weeks ago and we looked at it in Small Caps Live then. Where they said:

Despite these challenges Group revenue to 31 May 2021 was approximately 24% ahead of the same period last year.

To go from +24% to +14% in six weeks suggests that this period is probably flat? This may be because last year the bike boom kicked off in May & June, or it may be due to the supply chain issues. This means my previous calculations of 85p EPS on 24% revenue growth are a little overcooked:

If 24% revenue growth is representative of the full year then this would be £45.9m revenue. With 30% gross margin this would be £13.8m, up 13% on 2020. So assuming the same £8.1m of operating expenses, due to the same reduction in travel, exhibitions etc. then we get an operating profit of £5.7m. With a normalised tax rate of 20% and 5.34m shares in issue we get an EPS of 85p and a P/E of just over 7.

This is what they say on supply challenges:

We continue, however, to face a number of unprecedented challenges. Global demand is high and containers are in short supply. Far East container ports are overloaded and in some cases have closed for a period or are operating at reduced capacity. Shipping lines persist with blank sailings of container ships. During June, the Malaysian Shimano factory has been closed due to COVID which has reduced the supply of cycle components. Input costs such as steel, oil, plastic and cardboard have risen significantly during the year. These issues have led to stock shortages, unparalleled freight rates, reduced freight capacity and large supplier cost increases which, in turn, put pressure on margins.

Which is similar to what they said in the last update. As a distributor, I expect them able to more readily pass costs on to customers than say Robinson, but perhaps 10% sales growth and 30% gross margin are more realistic for 2021. Doing some quick calcs, that would be £40.8m revenue, £12.2m Gross Profit, £4.1m PBT, £3.3m PAT =62p EPS. So this would be flat on 2020. At 9x P/E this isn't bad, but I can see why the price has been weak following this update.

Longer term you have to weigh the competing narratives of 2020/21 being exceptional years vs new warehousing and plans for continued growth. More efficient warehousing should drive down opex IF they can build the scale to use it efficiently. Increased sales and longer shipping cycles may drive the need for more working capital, but with c£4m net cash I don’t see this as an issue.

That’s it for this week. Have a great weekend!