Small Caps Live Weekly Summary

RFX RWA SFR TGP TIG

A bit of a boring week this week, with lots of uninspiring midcaps reporting but little in the way of material news from the type of stocks we follow. The political news more than made up for the lack of excitement in actual results, though. Here is a selection of what we did look at this week:

Ramsdens (RFX.L) - AGM Trading Update

The update here is a bit short for our liking:

The Group has continued to trade well across its key income streams during the first five months of the financial year from 1 October 2024 to 28 February 2025, with the purchase of precious metals segment continuing to benefit from the strong gold price.

The Group intends to announce a Trading Update for the six months ended 31 March 2025 in April 2025.

It is notably shorter than the AGM update last year. If this was H&T, we would now be expecting a closet downgrade via brokers’ notes. But given this is Ramsden’s, an upgrade is more likely.

The trading statement highlights that both H&T and Ramsdens benefit from high gold prices and should have had increased share prices to reflect this, although not to the same extent as a gold miner. Instead, the price has been weak since this update. Maybe the market was hoping for more, but at least nothing specific is identified as weak that might offset the gold benefit.

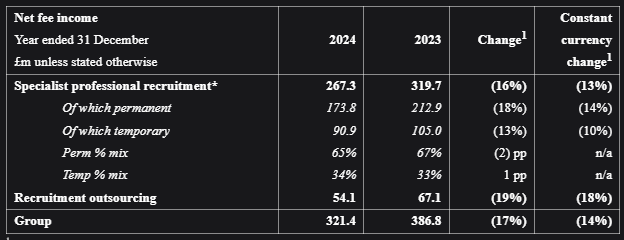

Robert Walters (RWA.L) - FY Results

As would be expected in these conditions, temporary recruitment outperforms permanent. Unfortunately, Robert Walters has a permanent bias:

The issue with perm income in these conditions is that it requires job turnover. Especially with many people living payday to payday with no savings, it is very risky for a candidate to give up a job with sick pay and protection against arbitrary dismissal for a new job with little to no protection for two years. The Employment Rights Bill currently going through parliament mostly addresses this issue. However, we are surprised by how much temp has fallen. Again, the provisions of the above bill are likely to affect this in the future.

The UK is only a small part, though:

The particular issue with candidate confidence is that it reduces productivity, with people passing interviews and then deciding it is too risky to accept. However, they are attempting to address this:

During the year we began to embed more robust behaviours on managing the sales funnel into our specialist professional recruitment business. This will ensure we are maximising the new job flow at the top of the funnel, and more actively influencing each key stage of the process such that we improve conversion into placements. The 5% decline in this volume productivity measure year-on-year reflected our decision not to let fee earner headcount fall further. Overall productivity, as measured by net fee income per fee earner, was up 1%* - underpinned by continued stable fee rates and benefits from wage inflation.

In terms of the bottom line, this pushes them into a loss, due to tax and financing charges:

They maintain the dividend, but for how long? Their capital allocation policy says:

The Group's capital allocation policy remains unchanged. The Board continues to recognise the value of a strong balance sheet, and therefore targets year-end net cash of at least £50m. Thereafter, the first allocation of capital continues to be on investment in those opportunities that enhance the Group's growth drivers and provide sufficient headroom above the Group's cost of capital. During the year investment continued into Zenith, the custom-built CRM system, as deployments were completed into the UK, Ireland, South Africa and North-East Asia.

Secondly, the Group's policy is to maintain a dividend cover ratio of 1.75-2.25x through the cycle. The Group also has the latitude to allow cover to fall outside this range at points in the cycle - as has been the case over the last two years - whilst seeking a clear route to return to the range. Looking ahead, the Board continues to be mindful of this aspect of the policy, particularly given the extended period of challenging market conditions whereby dividend cover has been outside the range.

With net cash now at £52.5m, it seems impossible that they can maintain £50m of net cash and pay out the uncovered dividend in the future. This knocks out perhaps the only remaining leg holding up the price.

Severfield (SFR.L) - Trading Update & Cancellation of Share Buyback

Before even reading the trading update, you know it is going to be bad when they are simultaneously cancelling a share buyback that is 93% complete!

This is the near-term warning:

the Group now expects underlying profit before tax for the full year to be in the range of £18m - £20m.

Here’s the multiyear part:

As such, underlying profit before tax for FY26 is now expected to be below our revised expectations for FY25.

Panmure Liberum says their net debt is in line, but then why cancel the buyback? It looks like a huge embarrassment for management here.

This is the original announcement of the share buyback:

The Company has entered into an irrevocable non-discretionary agreement with Liberum

As with Ultimate Products, it is important not to confuse the sequence of letters "irrevocable" with the English word "irrevocable" when found in the context of a buyback announcement!

Still, seems strange to revoke the share buyback instructions when it was 93% complete without a major cash crunch. Or lenders telling them to. Net debt may be the same, but if EBITDA is materially lower, the banking covenants will be tight for the same underlying cash flow. The benefit of lower trading is that it can release cash from working capital from this sort of business. The real crunch can come as they win new contracts and have to try to fund them.

This is another example of a buyback being conducted at price levels that now look daft. It looks expensive on medium-term forecasts, but presumably, the 0.7xTBV is now providing some support.

Tekmar (TGP.L) - Final Results

We have been warning about the cashflow/receivables here for years before the proverbial finally hit the fan. This week we note that they have taken a provision of £0.5m for "an aged debt balance". Does that mean the balance sheet now looks clean?

Hmm. So, receivables are up on reduced revenue despite a provision. It looks like the same old, same old. Net assets are maybe £1.5m after writing off the intangibles and half of the receivables.

We had hoped the founder leaving a few years back would resolve these issues with earnings quality. However, the problems appear to be on their third CEO, which suggests they are inherent to the business (or culture) and not easily fixed.

Team Internet (TIG.L) - No Offer

Their attempts to sell themselves at close to nil premium to the recent share price have failed. Almost immediately, Towerbrook announced they were out and this week Verdane joined them.

In their response, the company also included a trading statement, which doesn’t seem to say whether this is in line or not:

At this stage our best estimate of 2025 Search segment Adjusted EBITDA is between $20 million and $25 million (2024: $57 million). We expect 2025 Adjusted EBITDA of between $40 million and $43 million (2024: $36 million) from our DIS and Comparison segments, which is consistent with our previous estimates. That adds up to a range of between $60 million and $68 million for Group Adjusted EBITDA in 2025 before a return to double-digit earnings growth from 2026 onwards.

Given that the middle of the range for EBITDA is 30% below 2024, which in itself was down 4% on 2023, we are assuming not. The share price reaction backs this up:

That’s it for this week. Have a great weekend!

"it is important not to confuse the sequence of letters "irrevocable" with the English word "irrevocable" when found in the context of a buyback announcement!"

Brilliant 🤣