Small Caps Live Weekly Summary

50% off Mello ANG CCT LIKE MACF STAF VTU WIX

We are now within touching distance of Mello 2025, which is on the 3rd and 4th of June, back in Chiswick. The lineup is already looking excellent, and the organisers say it will be one of the busiest shows in terms of companies presenting. Here’s the current schedule:

Many SCLers will be attending for both days, and it is a great place to catch up with experienced investors and share ideas in a more informal setting. Tickets can be purchased here, and the organisers have given us a discount code M25Simpson50 to get 50% off ticket prices. See you there!

Here’s a selection of the news we looked at this week:

Angling Direct (ANG.L) - Final Results

They say:

Adjusted EBITDA2 increased 20.0% to £3.4m, slightly ahead of recently upgraded consensus market expectations

However, adjusted EBITDA isn’t a great measure for such a company. More realistically, EPS is up 17%, which is reasonable, but their growth is not all organic growth:

Like-for-like store sales3 increased by 6.0%, with improved customer footfall

Meaning the 22x P/E looks high, even compared to those growth rates.

The rating here looks better when you adjust for net cash, but this is now down to £12m and is about a third of the market cap, whereas it used to be well over half. Q1 sales up 17%, but again not all organic, and they will face cost headwinds from NI etc.

The other argument is that if EU losses were excluded, the results would look better. These are down to £0.8m from £1.0m. The problem is they are not dropping fast enough to look like they are on a path to being eliminated, but the company show no willingness to take the drastic action required to shut this down. So at 40p this looks fairly valued, at best.

The company are £1.5m into a £4m buyback, but by buying back shares on a high rating when the growth is all acquisition-led and even after adjusting for the dwindling cash pile, means this is unlikely to be adding shareholder value. They’d probably be better off using the money to shut down their perennially loss-making European operations.

Character (CCT.L) - Interim Results

Steady as she goes, at least on adjusted figures:

The significant conversion of working capital into cash YoY is particularly notable. However, things start to go wrong with the outlook:

The uncertainty flowing from the imposition of these tariffs has been felt in other parts of the world as customers have become increasingly cautious and are not committing to orders to our expectations. This is impacting sales in all our key territories. Despite this, the Board remains confident that the Group will be profitable in the current financial year as a whole, although it is too early to forecast short to medium term trading at this juncture.

An impact beyond the 20% US sales is disappointing. There was an interview from a US-based competitor on Radio 4 just now who said that orders were normally received in April, ready for Christmas, and these still haven't happened despite Trump partially caving.

We are disappointed that they haven't announced an extension to the share buyback amount which is nearly exhausted, and that there is no news on their excess property (it has not even moved to "Current Assets"). The dividend cut is disappointing given how much net cash and property they have:

Taking account of the current uncertainty, t he Board is declaring a reduced dividend at this interim stage of 3.0 p per share (HY 2024: 8.0p; final dividend 2024: 11.0p). The dividend is covered approximately 2.86 times by underlying earnings per share.

Shows they don’t think this is a short-term issue. It sounds like there's going to be blood on the streets and excellent opportunities for stronger players. This might explain the conservatism around the dividend and buybacks. However, it would be nice if they specifically said that. At the moment, the main inference is that they may need the cash to survive this upheaval.

Working capital tends to bounce around a lot at the year-end due to timing, but they said at the AGM that the H1 cash position was much cleaner. However, the reduction in YoY receivables is pretty extreme, one explanation being that sales fell off a cliff a month before year-end, well ahead of "Freedom Day". Indeed, the revenue miss of around £4.5m versus what would be expected to meet the (now withdrawn) forecasts is very similar to the reduction in receivables. Panmure Liberum say that the aim is to get inventory down by another £3m.

Likewise (LIKE.L) - Final Results

They are still significantly out-performing their markets (and Headlam):

Group Sales increased 7.4% to £149.8 million (FY23: £139.5 million). Sales in Likewise Floors increased 15.5%

· Gross margin increase of 0.4% to 30.7% in 2024 (2023: 30.3%)

· Underlying EBITDA of £8.8 million (FY23: £7.9 million)

· Adjusted Profit Before Tax was £2.0 million (FY23: £2.3 million) reflecting additional investment, particularly in H1 2024

· Positive cash generation from Operating Activities of £7.2m (2023: £6.1m)

However, buying back shares on a forward P/E of 16 looks like a stunt, and it sounds like they know this, with only £250k allocated.

Macfarlane (MACF.L) - AGM Trading Update

They say:

The Group expectations for the full year are unchanged.

However, it is an H2 weighting as they still face duplicate costs from the consolidation of one of their distribution centres. To be fair, the majority of companies would have classified this and acquisition-related costs as exceptional. No such shenanigans here.

There were a lot of questions about buybacks during the last management call, and they have responded:

The Group will commence a share buyback programme of up to £4m, details of which will be announced separately this week.

They never sounded particularly convinced by this course of action. However, it is clearly better to buy back shares at 5 x EBITDA than go and acquire smaller, lower quality, less diversified businesses at 6 x EBITDA. Given that these buybacks will probably be made at a historical low for the rating of the shares, this is a good move.

Staffline (STAF.L) - Contract Win

This is a relatively short update:

….pleased to announce it has secured a significant strategic partnership with one of the UK's leading food and drink supply chain management and logistics providers covering the whole of the UK and Ireland.

With a few details:

This new partnership comprises an initial two-year agreement with a one-year extension option to outsource to Staffline 100% of the agency labour services that are currently supplied by the wholly owned in-house labour supplier. This partnership will see the Group deliver flexible, temporary employment solutions in addition to managing second tier suppliers across the client's chilled and ambient business operations.

Our guess was that this was Wincanton, who have an in-house staffing operation but is being taken over by the existing Staffline customer, GXO, who do not. However, one of the brokers reports the client is Culina (Muller).

The contract is having an impact almost immediately:

The Contract is anticipated to further strengthen Staffline's leading market position in the logistics sector. The mobilisation of c3,000 temporary workers across driving, warehousing and security activities will begin no sooner than the end of Q2 2025 and is expected to continue during Q3 2025.

However, it is only by reading the brokers’ notes that the full scale is revealed. Here is Zeus:

Taking account of this phasing and of implementation costs, we increase FY25 revenue estimates by 4.4% to £1,071.5m, underlying EBIT by 8.8% to £11.7m and underlying PBT by 12.3% to £5.9m. With a full year of benefit in FY26 and FY27, we increase underlying PBT by 47% to £8.3m and 45% to £8.7m, respectively.

That’s a huge upgrade for future years. And while this is a time-limited contract, we know that if these are executed well, they tend to be extended. This makes the 15% or so rise in share price look a little light. Especially, as there is a chance of some Wincanton/GXO news after the CMA deadline to approve the deal on 25th June.

Vertu (VTU.L) - Final Results

These don’t look amazing, but are perhaps a little better than many expected. Especially on the outlook:

Trading in March and April has been stronger than the prior year, as the UK retail new car market improved from its lows and the Group continued to focus on operational excellence. Our high margin Aftersales business has sustained its robust performance.

March and April saw a significant increase in the UK new retail car market as Manufacturers rebalanced fleet and retail mix. The Group performed well, generating significantly more new car profit in the period than the prior year.

The narrative is fairly positive, although the lower dividend suggests they don’t feel confident enough to maintain this on reduced EPS. This is likley to simly be their policy. However, most companies bend this in weak years to smooth it and avoid cuts. After all, it’s still around 3x covered so should have been affordable.

Notable there are seven occurrences of the word "BYD", 15 for "Chinese":

As these brands are immature from an aftersales perspective, earnings and returns will take several years to develop to normalised rates as the vehicle parc is built up through sales.

There's quite a lot of detail about March / April trading , for example:

Core Group used vehicle gross margin improved slightly, by 0.1 percentage points to 7.8%, despite an increase in average selling prices of over £500 per unit. The Group was successful in managing inventory tightly and maximising margin due to high stock turn. As a result, gross profit from used vehicles was £0.9m ahead of the same period last year.

Annualised, that would be very material in the context of pre-tax profits of around £25m. Also, it is reassuring that reducing trading hours (admin costs) has not affected gross profits. As a reminder:

The Board has taken steps to fully mitigate the impact of rising costs announced in the Autumn Budget such as the National Minimum Wage and Employers' National Insurance.

They also claim that cash was ahead of expectations. So a lacklustre set of results on the surface look better the more you dig into them.

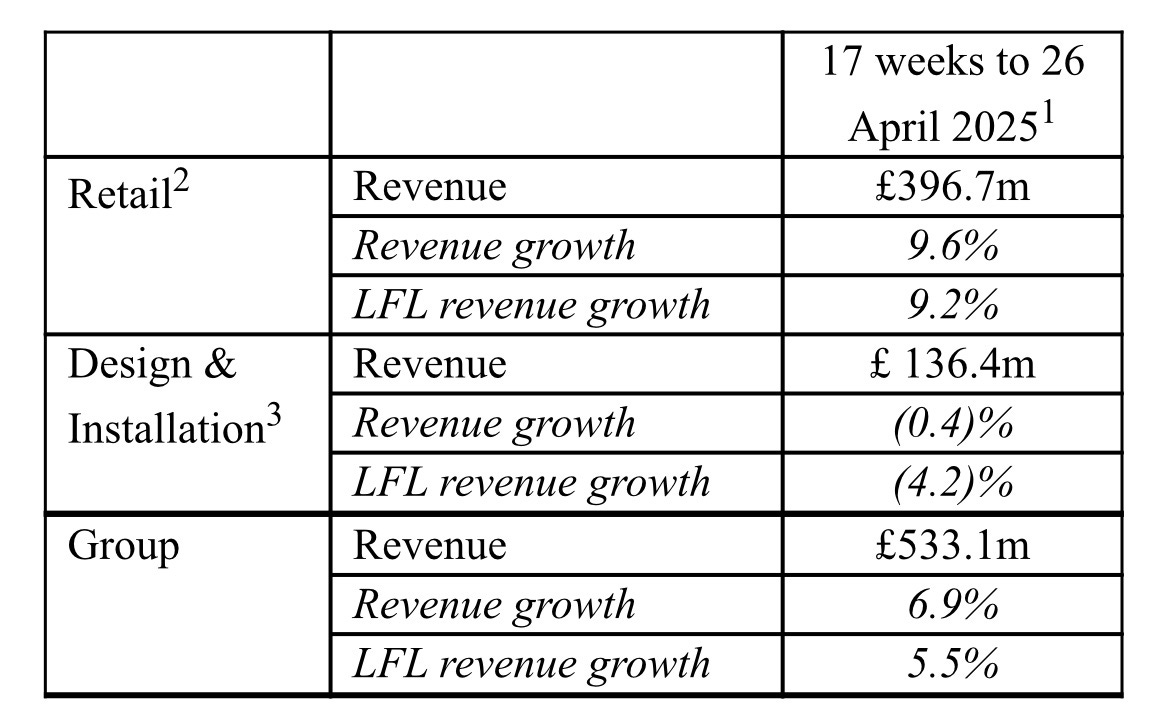

Wickes (WIX.L) - Trading Update

A very notable divergence between retail sales growth here and their installer business. Could have an interesting read across for the whole sector with DIY focussed RMI business performing much better than those that support the professional trade:

That’s it for this week. Have great weekend!

Reading between the lines of company and broker reports is always a fascinating aspect of these posts.