Small Caps Live Weekly Summary

UK HSBC SCS GDWN STAF

Another limited summary this weak as the Editor is away with limited network access. However, WayneJ was back with a Large Caps Live looking at the potential outlook for the UK and a UK bank.

Large Caps Live

So, where shall we start today? I was struck by Liz Truss challenging the economic orthodoxy in her leadership campaign. I thought I might try to dig up other leaders who have challenged the 'orthodoxy' and found a really interesting example. So before I go into details, let me tell you that this country is roughly the same size (in population) as the UK; it is a current example (i.e. not historical). The govt debt to GDP after a couple of decades of unconventional policies is 42%. (In comparison, the UK is 95.9%). Business confidence is 104 (vs (minus) -21 in the UK). Consumer confidence is 68 vs (minus) 41 in the UK. The corporate tax rate is 23%, and the personal income tax rate is 40% (vs 19% and 45%, respectively, in the UK.)

So what is this magical country? Turkey. And international confidence in the government's policies can be seen in the following:

One of the 'interesting' things done in Turkey is to reduce interest rates as inflation has gone up. The argument is that the orthodoxy is wrong and that high interest rates cause inflation. Additionally, the argument has been that lower interest rates increase exports and decrease imports and so allow the country to 'trade' its way to success. And Erdogan has had a refreshing approach to Central Bank independence - sack the Central Bank governor, and repeat until you find one that agrees with you.

He has a 'refreshing' approach to inflation - the official numbers are believed to be 'doctored' - and unofficial but credible numbers suggest inflation is running twice as high as the govt numbers. Estimate suggest as high as 175% (annualised) in June.

I will deftly sidestep any observations that Turkish / Italian trade has jumped dramatically since the bans on trading by EU countries with Russia began. And instead consider if it has any implications / readacross to the UK. My concern / expectation is:

(1) Truss is likely to be the next PM

(2) She is hellbent to ignore 'orthodoxy'.

(3) I have no issue with ignoring orthodoxy if you (a) understand what it is (b) what the flaws in it are (c) you have data / evidence / analysis as to why it is wrong and your plan is better (d) however just 'ignoring' it or seeking to overturn stuff without understanding verging on stupidity.

Now to be fair to Ergodan he has improved GDP / capita in USD over a number of years. For instance the following is GDP / capita on a PPP basis:

But in the UK we are facing the following:

(1) Change in the terms of trade (Brexit etc)

(2) Energy crisis - it is clear that the UK grid system has limited capacity and we also face significant primary energy supply issues in the coming winter

(3) The BoE has been slow to raise rates.

(4) The spend spend spend policies she is proposing will push govt debt to over 100% of GDP.

I think that short term this fiscal laxity and monetary looseness will lead to a boom in the UK but that longer term we risk a Turkey like scenario - but it could take 5 - 7 years to come through.

So how to play this? My thoughts are:

(1) The banking sector is a play on NOMINAL GDP growth - so if I am right about increased inflation for longer in the UK then the banks play well

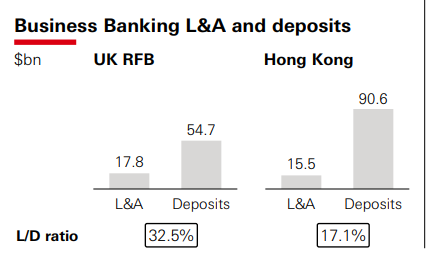

(2) It is clear that some banks have massive capacity to lend but have not been convinced it was the right thing to do eg have a look at the following slide:

The number to focus on is the L/D ratio. So the loan / deposit ratio (L/D) for the UK ring fenced business is 32.5% and in HK it is 17.1%. Admittedly in HK, HSBC is the de facto central bank so might be expected to have lower LD ratios but the above are nuts. Another bit of the results I found interesting (and relevant to the discussion on Turkification of the UK) is the following:

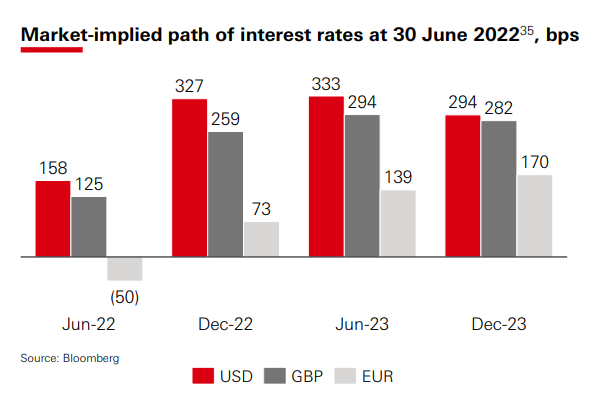

If I understand that right they are saying the market anticipated UK rates to be 259bps by y.e. and 294 bps in June next year. Now you might say so what - why is that bullish for banks? The following from the same slide shows the rationale:

As you can see HSBC's Net Interest Income (NII) mechanically increases as interest rates rise.

And u can also see that they benefit from volume growth.

Now can I be a bit 'unorthodox'?

(1) I think that credit creation by banks, especially in the UK, has been low due to the focus on improving balance sheets, shareholder returns and the vagaries of Brexit and our capital regime.

(2) Additionally on zero rates it is hard for banks to have sufficient spread to make money.

(3) What is perhaps getting less attention in the markets is that as well as raise rates the Bank of England is in quantitative tightening mode and I believe that will have massive positive impact on swap rates and margins for banks longer term.

The other point to note is that many UK banks are moving from 'personal banking' to wealth related service offerings. I am sure many people have heard of bank branches closing - there is a simple reason for that - most branches don't make money. However, wealth, premier and private banking are all attractive areas for banks as they tend to tie up less regulatory capital but give good returns with sticky revenues.

Both Lloyds and Natwest to me seem a tad 'lacklustre' with the only real structural growth being interest rates going up. Whereas, what has caught my attention with HSBC is that not only is it international but it is expanding / reinvesting in Asia and also in Wealth.

Small Caps

ScS (SCS.L) - Trading Update

We were expecting a profit warning here, however:

The board is pleased to announce that positive trading, strong margin, and effective cost management during the year means the Group now expects to report full year profit ahead of market expectations.

It seems Leo’s analysis matched orders but the deliveries is where the Trustpilot figures proved unreliable:

At 30 July 2022, the Group's order book was £71.7m (including VAT), £31.8m lower than at the same point in the prior year and £28.8m higher than at the same point in 2019.

This indicates far higher deliveries (= recognisable revenue) than Leo was seeing on Trustpilot. Impressive operationally for them to be able to deliver that order book profitably in this period. This has fed into profits:

After a challenging 12 months, the Board is pleased to be announcing profit ahead of market expectations for the year ended July 2022.

The Trustpilot figures have proven to be a much better guide of orders:

In recent months we have seen reduced in-store and online visitors resulting in a reduction in order levels, driven by the widely reported falling consumer confidence as a result of the cost of living pressures and economic uncertainty.

And, of course, the outlook is poor:

We expect the low consumer confidence will continue to adversely impact the Group in FY23.

Higher deliveries this year mean a lower order book entering FY 2023 than expected, but still:

However, the Group is in a strong position as we enter the new financial year, and strategic progress over the last 12 months means we are well positioned to take market share and maximise opportunities in a difficult environment.

So we continue to see a strong H1 weighting due to the order book with high uncertainty in H2. And their financial position means that have scope to survive where others fail. DFS, in particular, looks vulnerable, though it would be difficult for them to benefit from that as it would lead to an unwillingness on the part of consumers to pay deposits up front, and they probably wouldn't be allowed to buy them.

As ever, the thing to focus on here is the cash:

The Group's financial position remains robust, with cash at 30 July 2022 of £70.8m and no debt.

Here's the cash history pieced together from results statements:

27th July 2019: £57.7m

25th Jan 2020: £61.5m

25th July 2020: £82.3m

23rd Jan 2021: £91.8m

31st July 2021: £87.7m

29th Jan 2022: £87.9m

However, these figures are not much use without knowing how much of this cash is theirs and how much is customer deposits. Broker Shore put this as £43m net cash and we expect they have been given this by the company not calculated it. ScS have also spent a small amount on share buybacks.

Could it be we are at the same point in the cost of living crisis as we were with covid in March 2020? We now know it is going to be really bad, that government (and BOE in this case) have no plans to effectively tackle it and we have very little idea how long it will go on for. If so, then the bottom may be in on the share price, but one thing is for certain, FY 2023 is going to be pretty hairy.

Shore have cut 2022 revenue to £347.5m from £358m. FY 2023 forecasts have been cut from £375m to £349m. Perhaps the beat on profitability is due to the cost of living crisis that made advertising spend uneconomic. Profits are still likely in 2023 due to that order book, but FY 2024 could be loss-making. Shore FY 2024 forecasts look wildly optimistic with revenue of £359m versus £317m pre-covid.

However, Shore also “note the potential” for further buybacks next year. A business that is reducng share count by 10% a year and still remains capable paying a yield of c.9% will be attractive valuation for many.

Goodwin PLC (GDWN.L) - Final Results

They don’t do forecasts or trading statements so this is the first inkling we get as to how they have been trading. Despite the lack of shareholder communication, this company has quite a following. They did very well over the last couple of decades growing EPS. However, over the last five years the EPS has been up and down with little discernible trend. The bull case is that they have been heavily investing and that growth will return.

These results don’t exactly inspire confidence in that view though:

The "Trading" pre-tax profit for the Group for the twelve month period ended 30th April, 2022, was £17.2 million (2021: £16.5 million) an increase of 4% despite the Group having to contend with £3.8 million of additional energy costs versus the prior year. The revenue was £144 million (2021: £131 million).

Another flat EPS year. Although energy costs have played a big part. The outlook is quite positive for a number of the parts of the business though, particularly for the radar systems business and this perhaps explains the 11% rise in SP in repsonse to these reuslts despite ongoing energy headwinds.

However, the company themselves say this may not be visible in revenue for another year, and this sounds a lot like post-covid catch-up work. Elsewhere the market puts almost no value on this sort of short-term boom having been burnt on so many cases of this in 2021.

If this was on a P/E of sub-10 we’d say this was a nice bonus on top of a core business that has good potential despite energy & inflation headwinds. Unfortunately, this is a largely discovered gem amongst the PI community and the valuation reflects that.

Staffline (STAF.L) - Interim Results

Revenue is down 2.8%, well over double digits in real terms. Is the wage inflation in the sectors Staffline serve somehow far lower than ever other temporary staffing sector? Or have volumes (hours worked) fallen significantly? Figures are for 21.4m hours versus 26.1m, a 18% fall which is indeed very significant. The risk is that hiding behind the commentary about weak markets is a loss of market share, which in turn could be due to some underlying competitive or service issue. They do remind us that "The strategic exit from a significant high volume, low margin contract during 2021 further reduced revenues." so there probably has been some loss of market share, but not something that will hopefully continue.

Gross margins at the core Recruitment GB unit are up to are up to 7.1% from 6.8% which is pretty impressive given the pass-though nature of the revenue. Falls in operating profits are put down to investment ahead of growth. And the implication is that their staff are costing them much more even if wages of the staff they place have not. These are a poor results at the interim stage and their excuse is basically that their markets are in a transitionary phase - sectors benefitting from covid (food, online distribution) have slowed while some of those hit (automotive, aerospace) are only just starting to recover.

The only really bright spot has been Recruitment Ireland which is focused on permanent recruitment. They were lucky not to be forced into selling this last year (or perhaps lucky no offers were forthcoming) and have consistently said it has a long runway ahead.

For such bad interim results the outlook is strong:

· The Group has made a solid start to the year and continues to trade in line with expectations

· Continued strong demand for white collar recruitment across the UK

· A strong pipeline of new business opportunities and a robust balance sheet underpins confidence in the second half of 2022

· The full year outlook is subject to any adverse changes in the current macroeconomic headwinds of inflation, the associated cost of living challenge and global supply chain issues

But as is often the case, there are two outlook statements and the above is the wrong one. No actually there are three. Here's the bit from the shareholder perspective which reads like a deferred profits warning:

The Group expects performance to be second half weighted, with an increase in revenues from business wins secured in H1 2022, expected returns from PeoplePlus' Restart contracts, and increased seasonal retail trading volumes in Q4. Accordingly, management remains confident that FY 2022 results will be in line with expectations.

Who doesn't love a Q4 weighting?

On cashflow, things initially look bad due to the repayment of deferred VAT. Negative movement in working capital is less than half the VAT repaid. So are they stretching working capital elsewhere?

The IMC presentation gave more details on financial position:

In those terms it looks very comfortable. Leo found the presentation arguments over why H2 will be better fairly convincing so while the Q4-weighting remains a risk, this may not be as bad as it first appears. This has proven a good trading share in the past, perhaps due to the takeover potential, and it doesn't seem overpriced on an EPS basis, if they do indeed meet targets.

That’s all for this week. Enjoy the nice weekend weather.