Small Caps Live Weekly Summary

Ukraine LDG CAPD SYS1 TON SNX MACF TGP

Small cap markets this week have been rather overshadowed by political events with, of course, a terrible and rather unnecessary all-out invasion of Ukraine by Russia ongoing.

Hopefully, our current leaders will be able to look beyond the mountains of Russian cash they have been accepting as political donations over the last few years and agree to some sanctions with real bite. However, this is unlikely to be pain-free for UK businesses and consumers with energy and food prices set to rise further. In the UK, we have a long history of being willing to sacrifice our short term interests for the greater good and it is only right that we do so once again. It is worth bearing in mind what this further inflationary pain may mean for your investments, though.

There was no Large Caps Live this week.

Small Caps

Logistics Development Group (LDG.L) - Share Buyback

We last looked at this in detail in November last year when Mark said:

Although the presence of such cheap shares in the market today is perhaps an argument to both hold LDG and not. Why take the risk on an unknown acquisition when you can buy stocks where the value proposition is so compelling, without paying the takeover premium?

Since then, the valuation of a number of stocks has become even more compelling, and the LDG share price is flat so this would appear to be even less compelling. However, as we covered in the SCL summary email last week, one of the only things moving stocks at the moment is buybacks. And LDG are about to begin a buyback program.

The original announcement in mid-January was in an RNS with the, not exactly compelling, title of:

Publication of Circular and Notice of General Meeting

This is a cash shell after the sale of all trading assets and they said:

Following the Disposal, trading in the Ordinary Shares has been at a significantly discounted level to the amount of available cash per Ordinary Share, thus the Company is seeking shareholder approval to acquire up to 20 per cent. of the Voting Share Capital (the "Share Buyback"), to reduce the observed discount to net asset value per Ordinary Share and provide an exit opportunity for shareholders who do not wish to retain their investment in the Company following the change of the Company's investing policy.

Quite rare for a company to say that they are specifically targeting a share price with a buyback since that can often be considered market manipulation. However, investment trusts are able to conduct discount management exercises and this is similar here.

The discount is significant too. With the shares available to buy earlier in the week at 13.5p vs 19.12p/share cash balance as of 8th November. If the company eliminated the discount via buybacks then that would represent a 42% return on investment. We can probably expect them to stop some way short of completely eliminating the discount, but still, this is a reasonable upside, given that most of us probably target a c.20% annual compound return.

But as always it depends on how quickly that discount will be eliminated. And there was no sign of the buybacks yet, despite this being announced in mid-January. This is because doing the buybacks required a capital re-organisation:

The Share Buyback is to be financed by the cancellation of the entire creditable amount in the Company's share premium account, which will also create flexibility to make future distributions of profits in cash or in specie to shareholders and/or make future purchases of its own Ordinary Shares.

This was passed as a resolution on 31st January and this week we got the announcement that this was approved by the court, followed by the confirmation that a buyback will begin.

There are three major risks - the first is that existing holders are so desperate to get out that they sell to the company at the current price and exhaust the 20% buyback without moving the price. However, in this case, the discount to cash would actually widen, and sure the company would look to extend the buyback?

The second, and biggest risk is that the company does a daft acquisition. Thus negating the buyback and leading to the discount being wiped out.

Thirdly, as an AIM cash shell, there may be a deadline for delisting if they don’t invest the money. They have options, however, not least seeking a main-market listing. And in the buyback announcement, they say:

The Share Buyback will end no later than 7 July 2023 and the Ordinary Shares purchased under the Share Buyback will be cancelled.

They clearly expect to still be listed in 2023. And the other thing that happened in the GM is a change of investing policy:

Following completion of the Disposal, the Company, in conjunction with its investment manager, DBAY Advisors Limited ("DBAY"), has reviewed the investment opportunities currently available to the Company and believes that there will be more attractive opportunities to create shareholder value outside the parameters of the Company's existing investing policy.

The changes in the investment policy allow them not just to look at logistics companies but also:

a broader range of sectors, including logistics, distribution, technology services, security and manufacturing;

And they can invest up to 50% into DBAY funds, which is a little incestuous given that a lot of the company's shares are held by....DBAY funds. There are provisions to prevent them from double charging performance fees, though. And in Mark’s opinion, DBAY are very savvy operators. They have a habit of spotting undervalued companies, taking larger positions over time and then making an offer at a relatively low premium that gets voted through. Harvey Nash is the one that comes to mind.

As far as we can recall, we don't think they have ever treated the shareholders of their takeover targets unfairly, but also have never significantly overpaid. If they had intentions to delist LDG, or stuff it with poor performing investments, then why bother with the discount management exercise?

So in summary, this could be a good source of modest, uncorrelated short term returns in a difficult market.

Capital Ltd (CAPD.L) - Completion of Buyback

Capital picked a bad day to complete their buyback! (Of course, this was pure chance on timing and was driven by them reaching the monetary amount they set.) Without the buyback in place, we can perhaps expect higher share price volatility in the near term.

As well as the completion of the buyback they announced their results will be out slightly earlier than last year. We doubt results timing makes a big difference, although this sounds bullish:

Capital remains focused on growth and shareholder returns, and this Buyback Programme reflects the Company's balanced capital allocation approach as well as the Board's significant confidence in the business and its ongoing development strategy.

We’ll have to wait until the 10th of March to see what “significant confidence” looks like in actual numbers.

Eve Sleep

Eve Sleep nearly doubled on Wednesday on this announcement. Quite some move for an EQS (which is the new name for RNSNON - announcements that have an insignificant impact on company financials.)

This had come back onto Mark’s radar since, up until this week, it appeared to be a net net again. What put him off was the 20%+ spread and that the last trading statement had significant ongoing losses and big drop in net cash. This meant that they weren't actually a net net anymore once you pro-forma-ed the accounts for the drop in net cash.

This week’s excitement is that they will be on the DFS website, with plans:

...to extend the partnership to the DFS showroom estate later in the year. DFS will stock a range of eve mattresses

This perhaps indicates how much DFS are looking to push beds rather than just sofas in light of their ongoing supply chain challenges, as well as how the EVE model of online-only appears to have failed.

Unlisted, competitor Emma also announced a move to collaborate with a physical retail chain this week too. In this case, JYSK.

Overall, it shows how little differentiation there is in the market, and that those buying EVE on today's excitement are likely to be disappointed sellers when they see the next set of hard figures from the company arrive.

System 1 (SYS1.L) - Trading Update

System 1 dropped 40% on Tuesday in response to this trading update:

..total revenues in the final quarter ending 31 March 2022 are now expected to be over £1m short of management's previous expectations.

This drops straight off the bottom line:

As a consequence of the lower consultancy revenues, we now expect profit before tax for the final quarter and the year as a whole to be about £1m below the current market expectations.

The reason given is:

This is due to a sudden and unanticipated reduction in the forecast for bespoke consultancy project sales in the US.

Management is taking rapid action to address the consultancy sales performance in the US.

Not great that project sales can drop off so quickly. Perhaps there was an element of travelling hopefully here. £1m off forecasts is a big drop when the Net profit forecast is £1.4m. However, there are reasons for optimism here. Although they clearly have very little revenue visibility, having given an in-line trading statement 13 days ago, net cash was £8.1m at the end of December and £9m at the end of January.

Given that they have been buyers of their shares as high as £4.20, they will perhaps view the current fall as a gift horse, and a reason to be even more aggressive in their buybacks. And many investors hold this for the data products potential rather than the consultancy side, and here they re-iterate:

The Company is now well into its transition from a marketing agency to a decision-making platform. Automated Data products in the US region, and overall, continue to perform well, attracting over 200 new customers since launching in 2020. In the nine months to 31 December 2021, 39% of revenue came from Data and 60% of that revenue originated from those new customers.

The rating here means that this isn’t Mark’s sort of stock unless there are signs of the consultancy side returning to its more profitable ways, or the data side of the business scaling significantly. However, with the buyback in place and a strongly growing part of the business, this could enjoy a short term bounce, macro events permitting!

Titon Holdings (TON.L) - Trading Update

The other profit warning on Tuesday was from Titon:

...these supply chain issues have had a negative impact on our results in the financial year to date and we expect this to continue.

They are struggling to source components in the higher-margin ventilation business and the impact is flat sales, lower margins, and difficulty passing on costs:

We will seek to apply further price increases in the current financial year to recover higher input costs, but markets remain competitive.

Sounds like they are having to hire in some places while "restructuring" i.e. letting people go, from other areas of the business, all while paying more:

We will increase wages due to the very tight labour market and the increase in the National Living Wage in April 2022.

Since they are being hit on all sides, the result is fairly predictable:

As a result of these items our results for the financial year will be significantly lower than our prior expectations.

Their previously highly profitable Korean subsidiary is also struggling:

It is expected that Titon Korea will incur a loss for the full year.

Unlike System1 which opened down 20% and kept falling to 40% down, Titon opened at 60-65 before recovering to 75-85 (again note the large spread that makes trading this difficult). This is still down some 20%, but perhaps this is a case of the balance sheet providing a floor.

The Group has consistently maintained a strong financial position with a rigorous focus on working capital management and various cost initiatives. At 31 January 2022, the Group had cash balances of approximately £4.2m and no indebtedness.

Net cash at 30th September was £4.79, so this is being eroded slightly by these issues, but only slowly. At the same date, Titon had Net Working Capital of £4.7m and, although this may have been eroded somewhat as well, this compares favourably to an £8-9m market cap. The problem is that there doesn't seem to be a clear path to these assets being productive again. They are still minus a CEO:

The Group's process to recruit a new CEO is also making progress and the Company will update shareholders on these appointments as soon as the respective processes are complete.

With the previous one only lasting 8 months! So despite Mark being the kind of investor who likes unloved asset plays, the lack of strategic progress means that any turnaround here looks too far in the future to be of interest.

Synetics (SNX.L) - Final Results

Synetics is a Downing Strategic holding that Judith MacKenzie mentioned on Monday’s Mello event. It actually spiked up about 20% on Monday as punters clearly thought that the results due to be announced on Tuesday were going to be good and would knock the company out of its recent funk:

So were they?

Mark doesn't know this business well enough to know if there is, or should be, seasonality, and the last few years are going to be overshadowed by covid & lockdown effects. However, a £0.2m PAT for H2 on revenue that is slightly reduced vs H1 is not exactly something to write home about compared to the £18m market cap. The order book is down slightly on the £30.3m value at the half-year too:

Order book at 30 November 2021: £28.4 million (2020: £25.4 million)

They are however paying a dividend, despite the losses, which is often a strong sign that management expects things to improve. This is the outlook comments from the CEO:

"The second half of the year saw the Company return to profit, on a restructured cost base, delivering a significant reduction in losses. The Board is confident that the Company's excellent customer relationships in attractive markets, coupled with its talented and committed teams, provide sound foundations for a strong recovery and sustained growth. "

So positive, but very much driven by cost-cutting rather than top-line growth. The bull case is, of course, that they can return to their pre-covid days of £70m revenue and 16p EPS.

House broker, Shore, has cut revenue forecasts but maintained profit forecasts this week. They are expecting a return to former glories by FY23, with 15.6p EPS forecast for 2023 and 20.8p for 2024.

This makes them good value if you think that these forecasts are in the bag. However, a lot can happen between now and then and, as such, not one Mark would be willing to value on these figures today.

Macfarlane (MACF.L) - Final Results

These are a beat according to management:

I am pleased to report that Macfarlane Group has performed strongly in the year ended 31 December 2021. Our results are well ahead of the previous year and better than market expectations.

The continuing operations growth is certainly impressive. Less so on a statutory basis:

Statutory EPS makes them look expensive, but this is really because they don't provide their own adjusted EPS figure. Despite, clearly thinking that this isn’t a real cost, management don’t strip out acquired intangibles.

We turn to their house broker, Shore, who give us the adjusted 10.7p EPS figure and that is a beat on the 10.5p forecast. That also includes one-off costs regarding selling labels business, which could also have been stripped out.

The issue with Macfarlane, however, has always been the balance sheet. At the Half-Year, Mark calculated that the payables figure implied that they were paying suppliers later than would be normal and if they were on normal terms that could cause issues. Since then, others have pointed out that a chunk of those payables were contingent consideration for acquisitions and hence trade payables were likely to be on normal terms. So while that removes one risk, it changes a possible debt (change in supplier terms) to an almost definite debt - payments for acquisition.

What we really want to see is how those payables are broken down and it looks like we are going to have to wait for the AR for this since this isn’t in today’s announcement.

The current ratio of 1.16 isn't terrible but isn't great either. They have received most of the payment for selling the labels business too in these numbers so we can't count on that to strengthen the balance sheet further.

Management must clearly be happy with this though since they otherwise wouldn't have done the acquisitions they did. Excluding lease liabilities, they now have net cash which helps, but this is definitely a risk for a company whose turnover is large compared to profits, such as a distributor.

They've operated for over 15 years, most of the time with a much weaker balance sheet than today. However, it would seem daft not to consider it a risk, especially after the number of companies recently that have got themselves into trouble with working capital. It would seem sensible to position size accordingly.

There is good news on the pension front too, which is now in an accounting surplus. Of course, this doesn't eliminate recovery payments or even ensure that the triennial valuation won't be a big deficit. We’ve not looked into the details here, but gut feeling is that the next triennial will be ok, and if anything, recovery payments will be reduced or eliminated when the next one is due.

Following the triennial actuarial valuation of the Scheme at 1 May 2020, the Company agreed a new schedule of contributions with the Pension Scheme Trustees, which assumed a recovery plan period of 4 years. The next triennial actuarial valuation is due at 1 May 2023.

So, perhaps we can expect a couple more years of payments and this should be considered something like a £4m debt rather than adjusting EPS.

The outlook is for further growth despite challenges:

We expect to deliver further growth in sales and profit in 2022.

Shore have forecast 11.3p for 2022 showing a 6% EPS growth & flat for 2023. Bulls will suggest that these forecasts are made for beating. Bears will point out that they do warn of continuing inflationary pressures. Shore suggests that this trades at a discount to peers and that their price target of 150p is more reasonable. However, given that this is only some 15% above where share price currently is and brokers are paid to put a positive spin on things, Mark sees better value elsewhere.

Tekmar (TGP.L) - Final Results & Placing

We think it is important to highlight that Tekmar is an example of one of the ways that a previously successful founder-led company can go wrong when it comes to market. When you are private company with limited access to funding you have to run a tight ship, ideally being profitable and cash-flow positive every year, and quickly adjusting expenditure in the event of a downturn. Tekmar were successful for many years, but they raised money at IPO which they used to splurge on acquisitions and allowed them to completely lose control of their receivables. They were like the lottery winner that managed their finances fine before, but comes close to bankruptcy a few years after their win.

This resulted in the CEO losing control of the company they founded in October 2020. In December 2020 they issued their H1 results, stressing how strong their balance sheet was, but we kept stressing how weak it was. When the CFO eventually left in June 2021. Leo said:

In my view the only winners in the short term are likely to be brokers N+1 Singer and Berenberg, which doesn't help us much as they're not quoted.

Yet still no fund raise. In May they confirmed a dispute with customer Orsted. In August they changed their auditor. Yet still no fund raise. Perhaps there was no fund raise because institutions were wise enough to agree with Mark when he said:

I will definitely be watching with interest what the Grant Thornton audited results look like when they are out. Given the previous concerns we had with this company and the flux within the business, I’m not sure this can be considered investable until we see the GT audited results.

This week we get the announcement of the Results an clearly the first thing to look at in today's results is the going concern statement:

For the period ended 30 September 2021 their [the auditors] report contains a material uncertainty in respect of going concern without modifying their report.

And:

as the renewal of the two facilities in October and November 2022 are yet to be formally agreed and the Group's forecasts rely on their renewal, these events or conditions indicate that a material uncertainty exists that may cast significant doubt on the Group's and parent company's ability to continue as a going concern.

So, however much the directors say things like:

the Directors are satisfied that, taking account of reasonably foreseeable changes in trading performance and on the basis that the bank facilities are renewed, these forecasts and projections show that the Group is expected to have a sufficient level of financial resources available through current facilities to continue in operational existence and meet its liabilities as they fall due for at least the next 12 months

...be in no doubt that this is a company that was in serious financial difficulty. Accordingly a rescue fundraise was also announced today. The price of 45p was presumably agreed conditional on the audited results with institutions some time ago and is thus a premium on yesterday's price. The reasons given for the raise are:

The net proceeds will be used to:

o provide working capital headroom to support new contract deployment;

o invest in operational efficiency improvements;

o support the Company's R&D and technology roadmap; and

o strengthen the Company's balance sheet.

But in our opinion, this is a rescue fund raise.

"provide working capital headroom to support new contract deployment" means they couldn't continue working on contracts without it.

"support the Company's R&D and technology roadmap" means they would have to abandon all R&D without it. Which would kill the company - they are already on version 10 of the cable protection system and pretty much need a new one each year to remain competitive.

In the past their balance sheet has indicated very serious contract problems. Has the situation improved in this week’s results?

The unbilled contract assets were the biggest concern and so it is great news that these have reduced. The question is whether they have been billed or written off? Again, this looks like good news because there are no exceptional costs this year.

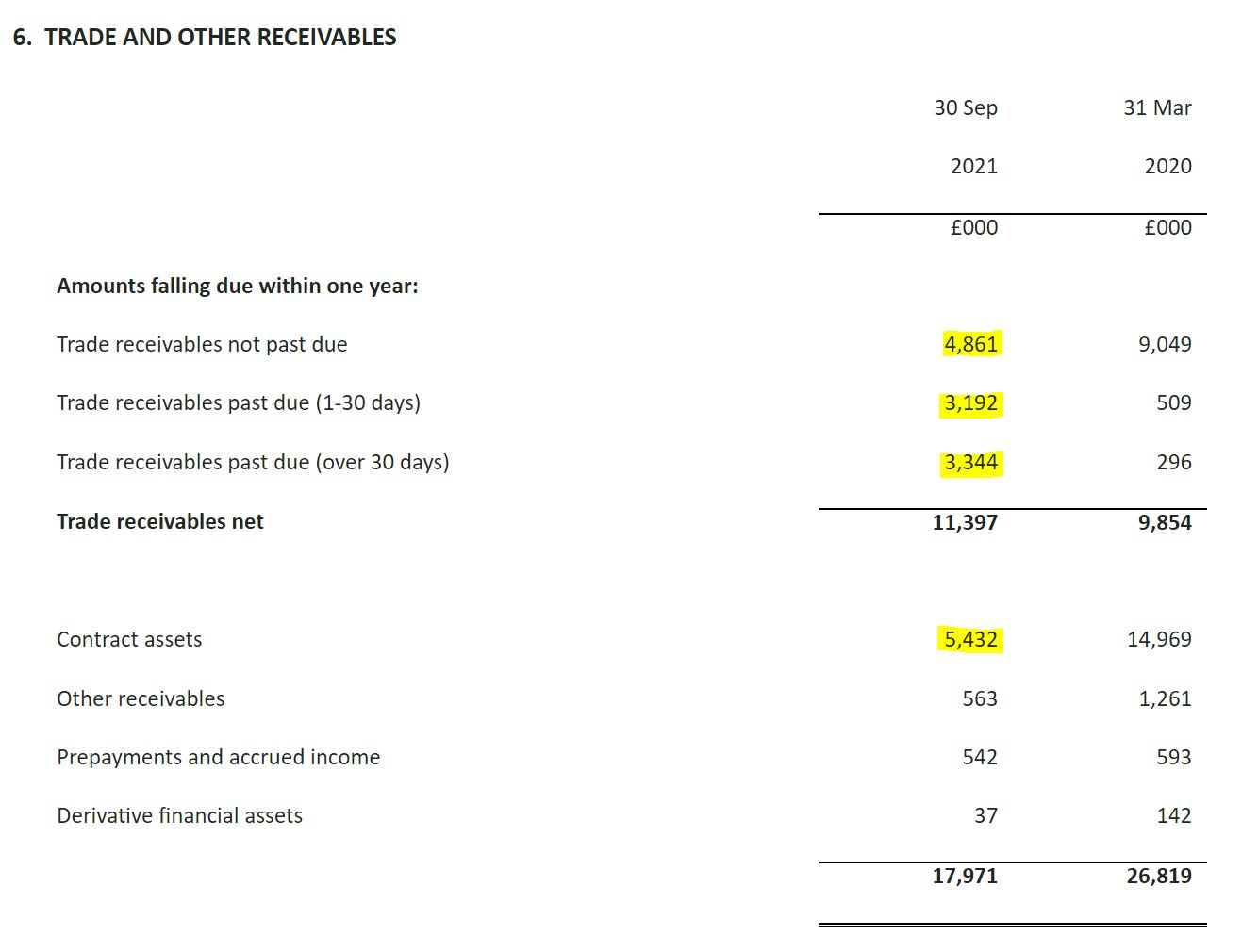

So they have billed these contract assets now. They bad news is that customers are apparently refusing to pay some of these bills with a massive increase in overdue receivables. Overall receivables have fallen, which is good in the context of revenue quality, but there are two problems here:

1) This is NOT a like for like comparison because they changed their year end. And I interpret their reasons as being with the explicit aim of flattering the figures. And they have conspicuously chosen not to provide like for like figures in the table above.

2) Half of the "improvement" is in "trade receivables not past due" which is definitely not what you want to be falling as it suggests a collapse in sales in the final month of the period. So, based on these figures we still have very serious concerns about revenue recognition.

Another part of balance sheet worth looking at is provisions. We know there has been a claim from one of their customers, and in principal they need some level of warranty provision as they have said they do not have insurance. Unfortunately, this information is missing from today's results. We might expect to see it in non-current other payables, but this figure is in line with last year. Given that warrantied installations are up on 18 months prior it appears they have not provided for claims.

Current trade and other payables are down inline with trade receivables, providing further evidence of a collapse in final month sales, although to re-iterate they have deliberately chosen not to provide comparable figures for September 2020.

So, based on the information disclosed on the balance sheet and notes today, we would still be extremely concerned about revenue recognition. Maybe there is some explanation in the commentary? Reading through the Chairman's and CEO's part, Leo is very concerned to see a complete failure to admit that this is a company that has made some very serious mistakes, which could yet prove terminal, and which leave real questions over whether its fundamental business model is even viable. The CFO says:

Trade and other receivables fell to £18.0m (FY20: £26.8m) due largely to the fall in revenue levels discussed earlier in this review.

But in fact revenue was not meaningfully discussed, with no relevant LFLs given. But anyway, they seem to be saying that there is no fundamental improvement in high receivable levels. The high levels of debtors and accrued income relative to revenue reflects the large number of contracts across the Group, including in Offshore Energy into China, plus the major contracts within the Marine Civils division where project milestones were towards the end of the reporting period, or the projects were not yet due for invoicing. But they claimed to have changed the year end precisely to avoid this kind of timing effect!!

They give no explanation of why overdue receivables have jumped while confirming that falls are about lower business. So it seems that indeed most of that reduction in contract assets has moved into invoiced revenue that customers slow to pay.

You'll notice that we haven't looked at revenue or profitability or anything like that. This is pretty much irrelevant because of the truly extraordinary red flags over revenue recognition. Based on these figures there is little evidence there are doing anything of any commercial value to their customers.

The other thing that is missing from the results statement is anything concrete since 30th September 2021, which was almost 5 months ago now.

Just to take the other side of the argument for a moment: It could be that management are just exceptionally bad at communicating and also that if we went back and found / calculated the missing like-for-like figures then things wouldn't look so abysmal. What kind of valuation would justify that kind of work on the off-chance that would uncover some hidden value?

At the moment you’d have to argue that it would be significantly below today’s price. However, wind power is a growth area so it may be worth re-assessing if the company returns to profitability, customers are paying their bills on time and we are sure there is no Orsted liability.

That’s all for this week. Hopefully better news next week.