Small Caps Live Weekly Summary

Crypto NSPN HUR MWE ESC GDP SHOE STAF CARD GATC SCS NCYT

[A Discord server invite, to see all this week’s discussions, is here.]

Large Caps Live Monday 17th May

Crypto Currencies

The big story in Crypto world is that tether has been forced to reveal the backing of the Tethers issued:

For those not fully aware, Tether is meant to be a "stable coin" - people transacting in the cryptoworld struggle to access the traditional banking system since no bank will accept payments in and out of dollars without passing KYC, AML etc.

A lot of people can't or won't subject themselves to this scrutiny. So, into this void stepped Tether, who offer a cryptocurrency that can be freely converted to other cryptocurrencies but is meant to be pegged to the dollar. Crypto exchanges are issued Tether in return for dollars from customer deposits. Each Tether is meant to be backed by these dollar holdings so if a customer wants to convert their crypto back to dollars they can convert it to tethers and then the exchange will return tethers in return for dollars to give to customers. And in the past, this has been subject to some scrutiny, with some people pointing out, for example, that Tether's claimed holdings in a tax haven bank exceed the banking assets of that jurisdiction. A lot of the increase in the value of BTC has been due to funds flowing in via Tethers being issued. So if Tethers are being issued without the backing of US dollars then this is fractional reserve banking, to the benefit of those who can issue Tethers for free (i.e. the owners of Tether) and presages a bank run, at least in the crypto world, if people all ask for their money back in dollars at the same time!

The suspicious mind may think that there was a strong incentive for Tether to issue Tethers to the Crypto exchanges, not in return for customer dollars but in the form of IOU's from the exchanges i.e. commercial paper. Indeed it could all be from related entity Bitfinex, we just don’t know. However, it is hard to believe that all these assets are mainstream financial assets.

If this does unwind, as many suspect, then this is probably the end of the crypto bubble. The real question though is, given the widespread speculation on cryptocurrencies, would this even presage a financial crisis in the real world?!

Naspers (NSPN.L)

This is a £65bn market cap in London and no one realises it is there! Obviously, the London listing is as illiquid as anything and has a wide bid-offer spread. Naspers has traded for years at a discount to its holding of Tencent. So a few years ago they decided to spin out a partially owned subsidiary onto the Dutch market to hold their internet investments - Prosus:

Naspers trades at a big discount to its holding in Tencent.

Prosus trades at a discount (not as big) to its assets.

Prosus is partially owned by Naspers.

So now Prosus is buying 45% of Naspers in exchange for its own shares.

Ultimately that will mean that Prosus owns 49.5% of Naspers.

And the free float of Prosus will increase to circa $100bn - and de facto become Europe's biggest internet play.

I still need to work through the numbers but roughly I think historically Naspers traded at 40 - 45% discount to Tencent, and Prosus about a 20-30% discount to Tencent. And I am thinking the key point will be how Prosus is treated by the index providers eg the Eurostoxx / Stoxx - could it lead to a lot of index buying. Or is this a clever way to get money out of South Africa (I always felt that currency controls were partially an explanation for the discount)?

Small Caps Live Wednesday 19th May

Hurricane Energy (HUR.L) – Requisition of GM

When we looked at Hurricane following its announcement of a debt for equity swap. We believed that the market was still overvaluing the stock, given the level of dilution shareholders faced.

The stock continued to decline as the maths of what was happening sank in…until today, when HUR is one of the largest risers on the announcement that Crystal Amber are looking to remove all the non-execs and put their own choices in.

When they have a new board they will clearly try to cancel the D4E swap.

In their statement, Crystal Amber do make some good points, such as:

The Fund believes that the emergency legislation upon which the Hurricane board is seeking to exploit with the Restructuring plan is intended to be applied for emergency fund raises where there is insufficient time to obtain shareholder approval, in order to ensure a company's immediate survival. It is concerning that the Hurricane board believes it is appropriate to apply Covid 19 legislation in order to circumvent the sacrosanct right of the owners of a business to vote on, and if thought necessary, approve a financial restructuring.

Although they still seem to be hanging on to the past, talking about past CPR estimates & valuations.

They question why the D4E is occurring now:

The Hurricane bonds are not repayable until July 2022. All interest has been paid and at 31 March 2021, Hurricane had $127 million of net free cash, with cash having increased by $10 million per month since 30 November 2020. The Hurricane board has said in clearest terms that Hurricane will have no difficulties servicing the future interest payments on the bonds. The Fund does not currently understand how the Board can say now, more than 12 months from the repayment date and having made almost no effort to find alternatives, that Hurricane will not be able to repay the bonds.

But I think the directors have a duty not to trade while insolvent, and if their internal models show that they are unable to pay the bonds when due, they may have a duty to act now. In the last operational update, the water cut was increasing further so the continuation of $10m FCF per month may be optimistic.

Hurricane are already indicating the alternative would be insolvent liquidation:

Shareholders and Bondholders are reminded that in the event the Restructuring Plan is not approved by Bondholders at the Plan Meeting, or if it is approved by Bondholders but not sanctioned by the Court, the Restructuring will not be capable of being implemented. In that scenario, it is likely that there would be a controlled wind-down of the Group's operations followed by an insolvent liquidation of the company.

The Hurricane presentation gives more details as to why they think bond repayment isn’t possible:

To be sure of this course of action, I think the board will need to have shown that larger shareholders were not supportive of say a large rights issue, which would have got them out of their duty not to trade while insolvent. In the plan documents, Hurricane don’t name the parties but it is easy to work out who is who. It appears that, when approached, Kerogan were not supportive of a further raise and Crystal Amber refused to be taken inside to have these discussions. Crystal Amber appear to have shot themselves in the foot with that one.

I think the key problem for Crystal Amber’s plan to wait it out and hope the oil price allows Hurricane to scrape the repayment is this statement:

As a result of entering into the Lock-up Agreement, an Event of Default (as defined in the trust deed dated 24 July 2017 in relation to the Convertible Bonds (the "Trust Deed")) has occurred. However, as explained further below, the company expects that the Ad Hoc Committee will not take further action in relation to such Event of Default whilst the Lock-up Agreement is in effect.

So they may sue the directors, company and whoever, after the outcome. But if an Event of Default has occurred, I don’t see any way back from this. The board have announced the General Meeting but given no further response so far. When they do, I’d expect them to point out their fiduciary duty and re-iterate that an event of default has occurred.

I’m sure other annoyed shareholders will vote for anything. A change of board composition is unlikely to change the long-term outcome, though, and may actually strengthen Bond Holders hands since change of control conditions often make such instruments repayable on demand.

The bonds are trading at 50, but were at 30 prior to the D4E, which suggests bondholders are still not sure they will get paid even when they own 95% of the equity.

As I see it, the only way out for Crystal Amber would be to negotiate with the Bond Holders – if they paid them face value for the full $230m tomorrow, then I can see Bond Holders walking away happy. If Crystal Amber can’t do that, I think they are, in technical parlance, screwed.

As usual, the market price reaction on the Hurricane equity seems bonkers - as I can't see Crystal Amber's actions making any difference to the long-term outcome for most shareholders which is very severe dilution.

MTI Wireless (MWE.L) – Q1 Trading

MTI Wireless released their Q1 Trading Statement this morning. Revenue growth is a little muted:

· Solid revenue growth, up by 4% to $9.95m (2020: $9.55m)

However, cost control & operational gearing means the profit numbers look better:

· Increase in profit from operations, up 14% to $0.96m (2020: $0.84m), reflecting the benefit of increasing scale on profit margins

· Significant increase in profit before tax, up 25% to $0.9m (2020: $0.72m)

· Earnings per share increased by 20% to 0.80 US cents ( 2020 : 0.67 US cents)

This has always been a cash-generative business and this quarter is no different:

· Strong cash generation with net cash up 10% to $9.5m on 31 March 2021 (31 March 2020: $8.6m), despite having paid a 2020 dividend of $2.2m in March 2021 (compared to payment of the 2019 dividend in April 2020).

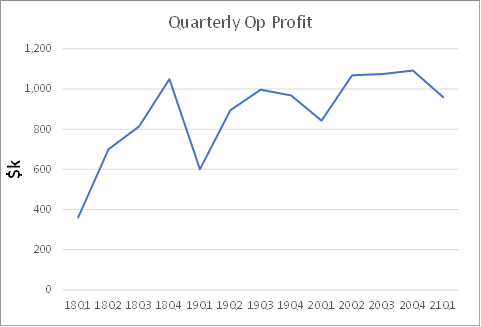

Comparing Q1 to Q1 isn’t particularly useful, though, particularly given recent upheavals in markets. Here’s what you get when you do a quarterly comparison:

Q1 has often been the weakest quarter, however, Q1 here is down significantly on Q4 and in line with Q2-Q3. This is reflected in quarterly operating profit:

The EBITDA picture is slightly better, reflecting the good cost control:

Management are indicating that their trading conditions are largely back to normal, so this reflects real underlying trading performance:

We have enjoyed a good start to the year. The majority of our markets are functioning well, with our home market, Israel, largely back to normal as far as COVID-19 is concerned. Trading is still likely to be disrupted in some areas but overall, given the experience gained last year when operating under the Covid-19 restrictions, we are confident in the ability of our teams to trade effectively.

The company operates in some good niche areas: 5G antennas, wireless irrigation solutions. And these are good places to be long term. However, I see little evidence that these are leading to high levels of growth in revenue or profits.

Again, the outlook statement reflects steady growth:

Looking ahead, we believe the Company's clear focus on providing radio frequency solutions coupled to being diversified across several markets positions us well to continue to grow and expand through a mix of acquisition led and organic growth.

So what about valuation? At 71p, this is on a historical P/E of 24 & an EV/EBITDA of 15.4. If Q1 trends continue, I can see that being a forward P/E of around 20 and an EV/EBITDA of around 14. This is hardly cheap for a company growing at 5-10%, even in current markets. They say they are targeting low-teens revenue growth a few years out but this acceleration would appear to already be priced in. Although this is a family-run company with a long history, there are additional risks of being a foreign domiciled AIM-listed stock.

I’d expect this to trade at a discount to the market, not the premium it currently does. It is a stable, well-run company but the current price is pricing in significant growth that has yet to materialise in the numbers - whereas periodically the market worries about its domicile and it can be bought pretty cheaply. I don't see the point of buying/holding when all of that potential future growth has already been priced in.

Escape Hunt (ESC.L) – Final Results

These are FY results to 31st December 2020 and the company continue with their highly successful policy of putting the best possible spin on things:

Group Adjusted EBITDA loss reduced to £1.4m (2019: loss £1.7m) despite COVID-19 restrictions

Or as I would put it:

Group Adjusted EBITDA loss reduced to £1.4m (2019: loss £1.7m), helped by the receipt of £0.8m of furlough payments.

I have previously explained how flexible furlough has particularly helped companies that normally (i.e. pre-covid) struggle to be profitable throughout the week and they go into some detail themselves:

Importantly, the 'flexible furlough' version of the scheme was critical in ensuring that sites were able to make a positive contribution when they re-opened but remained subject to restrictions. This flexibility led us to re-examine our service contracts to ensure that the business will be able to manage fluctuations in revenue better in future, when the scheme will no longer be in place. In November we implemented changes which have enabled us to convert over 80% of what were previously fixed costs to variable costs. This change will result in lower break-even points at all our UK sites and ultimately should lead to higher operating margins as a result of the better flexibility the changes afford.

Basically, they like only paying people when they're on-site and giving them an hour or two's notice of whether they are working or not and hope to continue this!

The results themselves were reasonably well trailed and are in any case historical. What investors are presumably interested in here is prospects for future trading, which means: new sites/pipeline, digital offering and most importantly reopening bookings.

Most of their recent new sites were opened late, missing the start of school holidays etc., but they managed to get the new Kingston site open for May 17th so hopefully, execution is improving here. There is also a disclosed pipeline of two more sites, but this hardly seems large in proportion to the existing 15.

There’s been a lot of noise about digital, but this only contributed £90k in the three months to 31st March. Assuming this will continue now they are open physically (doubtful), that’s £360k, up from £230k in FY 2020 (when they were mostly open), versus £5m total revenue in a normal year.

On current trading/bookings they say nothing, but never mind because I have the data...Let's start with Monday 17th:

They don't normally open on a Monday, but they did on the August bank holiday, and they did in October half-term just before the November lockdown. So this isn't really a fair comparison, but you can see broadly that there was some booking excitement early on, but the momentum didn't hold up. There's no indication that they will be viable on a Monday once the flexible furlough finishes. (Note the dots for 50% capacity on the right - they are nowhere near that.)

A similar pattern for yesterday:

So, far below half term, but better than a typical Wednesday:

Thursday looks worse for a couple of reasons. Firstly bookings are building a little ahead of a typical Thursday. Secondly, this is despite very significant increases in capacity - see the red dot on the right. Some of these increases in capacity are from new sites, others from more slots enabled by flexible furlough.

Friday looks better, provided you don't adjust for new sites etc

Saturday started very strongly. Note it is far ahead of the last Saturday they were open, but perhaps some Saturday trading was displaced into earlier in the week as it was a half-term holiday back then. However, early indications are that bookings have tailed off.

And weekends were always profitable. Surely, the hope was that people working from home would spread demand over the week. People get used to having to book pubs, national trust properties etc in advance I guess so also book ESC more in advance? Pre-opening publicity will have led to more booking further in advance. But they have been 100% advance bookings as long as these charts go back.

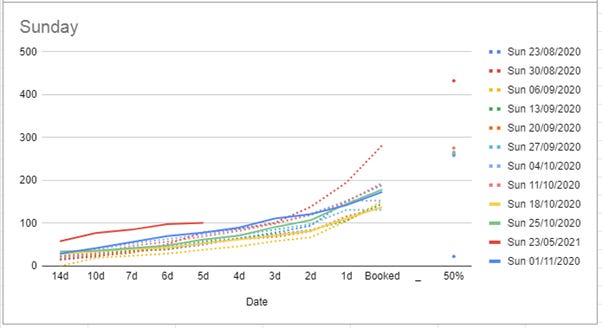

Sunday bookings also look strong...so far.

And remember the weather has been bad too, which normally helps them. Utilisation has always been terrible except for Friday-Sunday and even then not great. This is the fundamental issue with the business model. In my view, they were crazily overvalued in 2019, got below fair value in 2020 and are now back to the crazy level again. I don't think it is even worth doing the sums at a share price of more than 20p. Remember also that they have issued more equity in the meantime.

Goldplat (GDP.L) – Q3 Update

Goldplat released their Q3 update this week:

Not much that we haven’t said already on this one in past scl’s. Ghana is performing well, with regular batches of materials to process from clients. South Africa has struggled somewhat, processing lower-grade material that has been less profitable. Although the recent increase in the gold price probably starts to make this look much better. Kilimapesa finally sold for $1.5m. No definitive decision on processing their tailings dump but moving closer, slowly.

Overall they say:

The recovery operations achieved a combined operating profit for the nine months ended 31 March 2021 of £4,220,000 (31 March 2020: £3,802,000) and a combined operating profit in the 3rd Quarter of £1,165,000 (3rd Quarter - 2020: £1,053,000).

Net cash is £2.1m and they should receive either cash or cash & shares for Kilimapesa in July. If we assume similar performance for Q4, which may prove conservative given the move in the gold price then we have a P/E of 4.7, EV/EBITDA of 1.6. Which still looks good value, despite the inherent country risk.

It will be interesting what they do with the cash for Kili. Management comments indicate an intention to pay dividends:

I am pleased to report that with our two profitable recovery operations, in South Africa and Ghana, we are getting closer to our strategic initiatives of building long term visibility of earnings and being in a position to return value to shareholders through dividends.

If these are of a size that reflects the underlying FCF, then this could start to drive a re-rating. A long history of challenges here, though, and having to correct their last set of results twice, including not getting the EPS figure right, still shows a company that is struggling to get a good handle on all aspects of their disparate business.

Shoe Zone (SHOE.L) - Interim Results

These are H1 to 3rd April, issued pretty quickly:

Revenue of £40.4m (2020 H1: £68.9m)

Store revenue £22.8m (2020 H1: £63.3m)

Digital revenue £17.6m (2020 H1: £5.5m)

Digital contribution of £5.3m (2020 H1: £1.9m)

Digital conversion rate 6.43% (2020 H1: 3.47%)

Over 1.0 million engaged users in shoezone.com database

The thing that strikes me here is the growth and scale of digital relative to Escape Hunt. Unlike Escape Hunt it is a serious contributor.

Cash is holding up:

Net cash balance of £4.1m (2020 H1: £3.6m)

But how much is theirs?

CLBILS loan of £15m in place and drawn down. £4.6m repaid…

Majority of staff furloughed and we have used the Government business support schemes including grants, rates and VAT….

The company ended the period with a net cash balance of £4.1m (2020 £3.6m). The increase in cash balance has been achieved through the measures taken by the business over the last 12 months, which restricted cash out of the business but also took advantage of the Government furlough scheme, the business rates holiday, retail grants and the ability to delay VAT. We should state that, compared to last year, we are behind on rental payments as we continue to negotiate better terms with Landlords.

They don't quantify the rent arrears and I can't tell from the balance sheet, which seems a bit confused in this area. Ongoing negotiations with Landlords and suppliers may even imply they're delaying paying suppliers. Here's the recent trading:

Trading started strongly but has settled down to a more mixed picture of good High Street and retail park sales but weaker shopping centre performance.

It looks like they need more capital here, which should be a nice set of fees for their broker finnCap. It is surprising that they didn’t do a large raise in March when the markets and their share price was strong. There could be two reasons for delaying. The first is that appearing financially weak strengthens their negotiations with landlords. The second is that the Smith brothers, who are Chairman & CEO don’t want to be diluted and they think they can scrape through without additional equity. Indeed, they have been adding to their holdings this week. History says that this is often a dangerous strategy, though, and raising while capital markets are strong is often the wisest move.

Small Caps Live Friday 21st May

Staffline (STAF.L) - Proposed Placing

Staffline is down 17% today on the following news:

Staffline announces its intention to raise £44 million by way of a placing of 87,249,500 new ordinary shares and a direct subscription of 750,500 new ordinary shares both at a price of 50 pence per share…

In addition, in order to provide all Qualifying Shareholders with an opportunity to participate in the fundraise, the company also announces its intention to launch an Open Offer of up to 8,837,242 new ordinary shares at the Issue Price to raise up to a further £4.4 million.

Shareholders perhaps surprised at the size of the raise, which totals £48.4m and adds 97m shares to the 148m currently in issue. Readers of Small Caps Life will not be surprised, of course, since Leo called this on 28th April, saying:

My initial analysis showed at least £10m, preferably £15m, but they have a nasty in their books. As understand it they have off-balance sheet funding of £25m in the form of non-recourse invoice financing….Worse, the uncommitted part of this facility can be removed at any time, and of course it naturally rolls off. Worse still, some of the other funding is conditional on that £25m remaining in place and seems to be callable should it be removed. So they really need £35m.

Also bad is that their working capital varies enormously through the year. For example, they previously said that as at 30th Dec they had 9m net debt, but the average over the 12m was 38m. And in today's update they said the average in Q1 was £54.9m (including VAT deferral), only £15m better than a year before. The closing Q1 net debt wasn't given, but at the end of H2 last year it was £90m!

So really, they need a little more than that. Liberum note that mid January is the worst point in their cash cycle and that's when they need to make the final VAT payment. Therefore they need £40m.

He was out by £8m, but we will give him that, particularly since there are placing costs and debt fees to consider, plus the open offer is not guaranteed.

Leo also thought they could get this away at 60p, but it seems they had to go for 50p, in the end. The open offer part of the raise is small, but the size of the raise means that the price heads to the open offer price anyway.

Pretty much the last thing Leo said about Staffline was that they were effectively playing chicken with the market. So today's timing and price is interesting as it comes after a bit of a wobble in equity markets over the last few days and at a relatively high discount given the share price has been consistently over 60-70p for months, and the broker target was just raised from 60 to 90p. They needed the discount, in the end, to get this size away.

Perhaps indicative of the shareholder base they have:

If HRNet said no in preliminary discussions, then they're already short. The same goes with Henry Spain. Then there's a lot of PI investors there, which they can't canvass.

So what does a raise of this size mean for valuation? Over to Leo again:

One way to look at this is that in December 2018, net assets were £83m, and after this raise, I think they will be £64m. But the market cap was £280m then and after this will be £100m (at current market price). And the quality of the assets is much higher, with far less intangibles. And the quality of the company is much better, with competent management in charge and significant cost savings / higher margins. But of course, they were wildly overvalued in 2018.

Another way is to look at earnings. I haven't done a sensitivity analysis on this, but broker forecasts are for EBIT of £11m on 2022 and £14m in 2023. They were forecasting £7m of debt costs. Of course, they knew there would be a fundraise, but they can't factor that in until it happens. I reckon that now reduces to £5.7m pa.

Of course, the share count is higher. So I get EPS of 2.6p for 2022 and 4p for 2023 based on the last broker forecasts.

But I think the key thing here is their dominant market position. This allows economies of scale that justify a higher rating than competitors. I'd also argue that they shouldn't be valued on the same basis as a people-business recruiter, but more like a company that can leverage technology.

The ways these things work means that even for non-shareholders who don't have the Open Offer, there is a high chance of picking up shares around the 50p level in the next few weeks, but even at that level 13x P/E on 2023 numbers doesn't seem a compelling value opportunity unless they can really prove themselves as a tech company rather than just a recruiter.

Card Factory (CARD.L) - Trading Update

In another sign that the sheer volume of demands for fresh cash from shareholders may be dampening market sentiment slightly, Card Factory is down around 13% on their trading update. Part of the fall may be due to this:

Initial store sales performance exceeded both our expectations and the sales performance realised after reopening following the first and second lockdowns. Initial strong demand has been satisfied, with store like-for-like sales for the first 5 weeks marginally down compared to the same period in 2019.

It seems that at least some of the exceptional demand was catch up, and perhaps the novelty of being able to go into stores again. Viewed in context, today's fall has only really undone the exuberance from their last trading update on 30 April, when they said:

The Company is pleased to report that its performance following the reopening of stores in England and Wales from 12 April 2021 has exceeded its expectations.

However, I expect the following statement has also dampened the spirits somewhat:

The facilities are structured to incentivise an early reduction of overall debt with fees of up to £5m payable if pre-payments are not made in line with specified dates from 30 November 2021 through until 30 July 2022. Subject to prevailing market conditions and upon taking independent advice, the company intends to use its best efforts to raise net equity proceeds of £70m to facilitate these prepayments.

Like Staffline, Card Factory are trailing a placing prior to it being done which can often weigh on sentiment. At least they have quantified the amount, and a failure to raise will simply mean more expensive debt. I can't help feeling that with extra dilution on its way and a challenging high street environment, the recovery has now largely been priced in here.

So there are tentative signs that investor fatigue may be setting in with regard to equity raisings, and this may explain the recent weakness we are seeing in some of the small-cap brokers, such as finnCap, Cenkos and Numis. I'm not sure this is logical, though. These companies don't care what price the raise gets away at, just that the raise gets away. And I think we are a long way away from the point where decent IPOs or necessary placings get pulled. As always, shareholders can track these transactions directly via the RNS system which don’t really seem to be slowing that much.

Gattaca (GATC.L) - Trading Update

Recruiter Gattaca also released a trading statement this morning:

Since we announced our half year results on 31 March we have seen a faster rate of recovery in NFI than originally expected. In Q3 we are pleased to have delivered quarter-on-quarter UK NFI growth of 13% across a broad range of segments.

Sounds good.

In addition, the changes arising from the introduction of new tax legislation (IR35) had less of an impact on the company than we anticipated. We now expect NFI in H2 to be in the order of 10% up on H1 2021….

Whilst there remains uncertainty around Covid-19, our current expectation is that this rate of recovery will continue, and we therefore expect our underlying continuing profit before tax for the year to 31 July 2021 will be significantly ahead of market expectations.

Even better. But what does this mean?

21H1 results had NFI down 33.7% from 20H1 to £21.1m. So 21H2 NFI will be £23.2m, essentially flat on the £22.5m for 20H2. H2 is January to July so in 2020 a period that faced the absolute worst of COVID-19 impact.

On PBT, Equity Development has a new note out where they raise their estimates from £750k to £2.7m. This is a decent increase, but given they broke even in 21H1 then the PBT for 21H2 is greater than the increase in NFI, this seems to be largely driven by cost-cutting. Which seems strange in a people business that is allegedly growing again.

Also strange is that Equity Development have raised their price target to 280p on the back of this update, however with little real justification on how they got there. They do say:

In fact, even after the recent price appreciation the shares at 150p still trade on frugal FY22 multiples of 7.4x EV/EBIT & 11.3x PER vs 12.8x & 20.9x for peers (see below).

So they seem to be valuing this at around 15x 2022 EV/EBITDA based on comparators with much larger recruiters that have always had higher margins and have been more highly rated.

If you applied the same multiples to something like finnCap you'd end up with a price target of 150p or more! I wouldn't pay 15x 2022 EV/EBITDA for any people business, let alone one with such a chequered past as Gattaca!

One of the bull cases is that this may be a sector where M&A takes place. We note that MMGG Acquisition, who are part of Morson, have recently upped their stake to 20%. They have held for a while, however, and nothing has come of it, so it would be a brave move to own on this alone.

SCS (SCS.L) – Retail Sales

We've talked several times about how footfall is relatively weak, but that people are buying more. The ONS choose to compare with February 2020 rather than April 2019 here, but this is very visible:

Volume bought AND value is significantly up. But where is this spend going? Surely the homeware sales boom is over?

Again, according to the last column apparently not. It is still the strongest category. I think this bodes very well for SCS and, to a lesser extent, UP Global Sourcing.

Novacyt (NCYT.L) - DHSC Dispute

Holders reading the subject of the RNS will have been hoping it is all resolved. However, the company said:

On 9 April 2021, Novacyt announced that it was in dispute with the DHSC in relation to its second supply contract and that this may have a material impact on Q4 2020 revenues. In the same announcement it was also noted that approximately 50% of Q1 2021 revenue was driven by sales to the DHSC. The dispute may now have a material impact on these Q1 2021 revenues from the DHSC.

I don't think this should be a surprise. In my mind, there was no doubt that Q1 would be affected. Ideally, they would know their FY 2020 revenue by now, since potentially they could start running up against the 6-month deadline to produce audited results.

This has taken the share price back to the lows following the initial "bombshell", but no lower. They have previously given enough information to have a stab at guessing the ongoing profit impact, and when I tried previously it was clear they are now overvalued. If they fall below 300p, however, I might take another look.

That’s it for another week in the markets, have a great weekend all.