Small Caps Live Weekly Summary

TND DRV FA. PGH EBQ PRES AUK BAR IDP GATC NUM PEEL

Some readers may not have realised that what we send out here is largely a summary of what we have discussed on the SmallCapsLive discord server. Here is an invite if you want to join the debate.

Small Caps

Tandem (TND.L) - Final Results

The shares were down 17% on these results on Monday. The results themselves don't read badly:

Ø Revenue increased approximately 10.4% to £40,917,000 (2020 - £37,056,000)

Ø Gross profit increased to £12,051,000 (2020 - £11,018,000)

Ø Increase in operating profit to £4,939,000 (2020 - £4,095,000)

Ø Profit before tax after non-underlying items was £4,732,000 (2020 - £4,004,000)

Ø Net profit for the period was £3,826,000 (2020 - £3,458,000)

Ø Basic earnings per share 73.8p (2020 - 68.5p)

Net cash was down:

Net cash as at 31 December 2021 of £2,326,000 (2020 - £3,779,000) following land purchase and construction

But, as they say, this is largely due to expansionary capex, of around £3m.

They've played around a bit with which products are in which categories, but generally, it is bicycles that are the problem child, with the rest of the business increasing revenue:

The big issue is with getting stock:

Stock availability proved to be a significant problem throughout the year, both for independent bicycle dealers with our Dawes and Claud Butler ranges and also national retailer customers with our Falcon, Boss, Elswick, Townsend and Zombie brands.

Although price rises seem to start to perhaps dampen demand as well?

Licensed character bicycles, which were also reclassified from Toys, Sports & Leisure in the year end accounts, were approximately 30% behind the prior year and this was due to a supply chain issue which has subsequently been rectified by re-sourcing supply to alternative factories. Cost price increases also had a greater impact due to the price sensitivity of junior licensed bikes.

It is the outlook that is doing the real damage here though:

Unsurprisingly, given the significant global uncertainty and prevailing economic conditions currently in play, the year has started more slowly than we would have wanted. In the 11 weeks to 20 March 2022 Group revenue was £4,432,000 which was approximately 43% behind the same 11 week period in the prior year which was exceptionally high as back orders for 2020 were fulfilled.

43% reduction in group revenue is huge! The do say:

However, it was still 7% ahead of the comparative period in 2020.

This doesn't exactly inspire confidence since at the start of 2020, pre-pandemic, the share price was around £2, with 2019 EPS of around 40p. Cenkos now produce research coverage on Tandem so we get to see what this outlook is expected to do to EPS going forward:

We note they apply adjustments differently to stockopedia and have 48.8p EPS for 2019 and 56.7p for 2022E. This means the forward P/E is around 7.5 following today's share price fall.

So on one side, you have one of the cheapest ratings in the current market, at least for non-resource stocks. But countering this you have declining EPS, a risk that Cenkos haven't cut EPS enough given the outlook, further cash outflow in 2022, and the fact that in 2019 it was trading at an even lower multiple than this and at times, at a discount to tangible book value.

Then on the other side, surely this weak outlook should have been expected by shareholders, and if they can generate the growth from their expansionary capex eventually, this will look even cheaper. Management changes in recent years have also improved the perception of the business and partly explain why the rating is now much higher than in 2019.

A quick check on advfn reveals that they have a fairly wealthy and fanatical PI holder base. People like this can certainly move the price on their own if they wanted to. Conversely, if this is just the first of many profit warnings and the larger holders lose faith then they will probably be capitulating below £2.

Despite the modest rating, Mark doesn’t don't see much reason to rush in now. The share price may bounce slightly off the current lows but with the short term outlook even more uncertain, it is unlikely to soar again anytime soon and there is always the risk of further profit warnings if supply chain issues and inflation persist.

Driver Group (DRV.L) - Trading Update

This is one of the biggest fallers this week, with this trading update doing the damage, plus a sell recommendation from the Investor’s Chronicle adding to the woes.

Mark’s thesis on Driver group has been that there were lots of construction contracts delayed by COVID, lots of disputes, and that these would all be litigated over the next few years leading to a lot of work for the group. Sadly, this has been proven wrong so far, with today's statement saying:

Driver Group has had a difficult second quarter (ending 31 March) with results during the period impacted by a combination of a problematic loss-making contract in the APAC region and an unexpected drop in revenues in the Middle East region.

It is not all doom & gloom though:

The EuAm region has continued to perform well and provides a solid platform upon which to build for the future

Both revenue and margins have been improving here over the last few years:

But this is perhaps an example of where valuing a business as a sum of parts and ignoring the loss-making bits is not the right thing to do:

the drag effect from the APAC and Middle East regions means that underlying* Group profit before tax for the half year is expected to be between £300,000 and £500,000 against £1.0m in the corresponding period last year.

They are taking action to address these issues, though:

Given the historic underperformance of these regions, the Board instructed an operational review of both regions, with independent external support, and has identified a near term opportunity to reduce annual operating costs by in excess of £1.0m through a reconfiguration of the Group's operating footprint in both regions, including the closure of marginal locations.

We’re not sure history books will be written about this loss, so perhaps they meant "historical" rather than "historic"? Anyway:

Implementation of the key findings of the review will commence immediately and is expected to support a significant improvement in profitability in the second half.

£400k PBT for H1 plus say £900k H2 would give £1.3m PBT for the full year. This would be about 1.9p EPS vs 3.74p forecast. So this is a big reduction, but with the share price now at just below 30p to buy, the rating isn't crazy expensive considering the problems they faced in H1.

Net cash balances currently stand at £3.9m with available bank facilities of a further £5.0m, reflecting a significant increase in trade and working capital receivables, particularly in the Middle East regions and dividend payments.

So this is a third of the market cap in cash, making the cash adjusted P/E about 11. If the full £1m of cost-saving comes through in FY23, then they should be on a cash-adjusted P/E of 5. Less if the current working capital build reverses and the cash balance increases again.

The problem is that the market has lost all confidence that the current management team can deliver the required changes. The CFO has fallen on his sword:

The Group also announces that David Kilgour has tendered his resignation as Chief Financial Officer and will leave the Group to pursue other ventures. The recruitment process will commence immediately to identify a suitable replacement to ensure a smooth transition.

So clearly the blame has been put on a lack of financial control or reporting. Though it is notable that he isn't leaving immediately. The last time their CEO left they ended up paying a massive amount to buy out his contract. So hopefully, learnt their lesson on that one.

This isn’t the board change we would like to see though. However bad the CFO might be, a resignation announced with a negative update is never good news. A new CFO almost always wants to make changes and the temptation can be to “kitchen-sink” the first set of results when they come in.

Steven Norris is Chairman of this and 6 other companies. He also runs his own personal company and is involved with 4 more. Even if he is able to commit the time required to lead Driver Group, he doesn’t appear to have done a great job of it so far. Under his watch, the company appeared to have established a culture of only reporting problems when they are forced to, rather than updating shareholders in a timely fashion.

The company has improved in its willingness to be open about problems more recently, however. The risk to H1 was highlighted by CEO Mark Wheeler during the last results, where he said:

The consolidated budget for the 2022 financial year is heavily second-half weighted as usual but also reflects the Board's expectation of some level of Covid-related disruption during the first half and the typical lag between new strategic hiring decisions and revenue generation.

However, management information for the first quarter shows an estimated result which is slightly behind both the budgeted result and the outcome for the same period last year. The Board remains optimistic that the underlying result for the year as a whole will show significant year-on-year improvement, but this will require monthly revenues during the remainder of the financial year consistently higher than the c£4.0m monthly run rate recorded across the first quarter.

With the share price already weak and looking cheap on a number of metrics the price didn’t react strongly at the time.

Equity Development have suspended their financial estimates and Singer say;

We withdraw our forecasts and place our recommendation under review.

Which won’t help confidence. Our gut says that the trading performance is likely to improve markedly in H2 and the company will advance from there, although it will take much longer or further management changes to rebuild investor trust.

Later this week we get the news that the non-execs have put their hand in their pockets at 27p per share:

We are not convinced these are particularly material to any of these people, but they may have been constrained by the relatively low liquidity. Such buys are unlikely to sway the investment case either way, which rests on a successful restructuring of Asia and the Middle East.

FireAngel Safety Technology (FA.L) - Final Results

Underlying operating loss £3.4 million (2020: underlying operating loss2 £5.4 million)

Manufacturing in Poland, they should have been a major beneficiary of competitors struggling to get goods from China, right?

Demand, especially for connected products, was much higher than the Company's ability to supply, which has continued in the first few months of 2022

Apparently not then. And we’ve been left slightly unsure of whether the company think this is a bad thing or something to be proud of. Running out of cash and having to raise more is definitely seen as a good thing, though:

Our team has done an excellent job of navigating a difficult year. Our steadfast focus on our strategic initiatives, the significant deals signed and our successful fundraising of £9.8m, (before expenses), in April have provided us with a strong platform for further improvement.

So how is that cash?

Operating cash flow before movements in working capital is minus £2.3m.

An inability to supply customers helped reduce inventories, but their payables were reduced by twice that, as apparently their contract manufacturers and suppliers refused to prioritise them until they sorted out their payment terms:

Average creditor days reduced significantly to 21 days (2020: 72 days) due to the increased pressure to support our manufacturing partners with extended working capital exposure from longer component lead times resulting in increased credit exposure in addition to purchasing components on the open market with minimal credit terms.

So cash used by operations was £3.4m. Capitalised development costs burnt another £1.5m. Historically most such development expense has been wasted. Although they say:

In April 2021 the Group signed a long-term partnership agreement with, Techem, to provide a fully funded research and development programme for a new generation smoke alarm.

Describing the above £1.5m as fully funded doesn’t work for us because Techam own the results. This is more like contract engineering. So total cash burn for the year was £4.7m. This included the benefit of £0.6m tax refunds due to losses. With only £3.2m of cash left from the fundraising, they will apparently be reliant on increasing debt facilities during FY 2022. This could be funded from undrawn invoicing discounting and receivables financing of £8m and so there appears to be no immediate risk, however.

Provisions for warranty claims continue to be a concern. While there was an underspend of £0.3m on provisions of £1.5m at the start of the year, previous research and current reviews suggest they are saving money by not consistently honouring the warranty, for example:

Although the trend in warranty utilisation is downwards, the provision for FY 2022 is lower than claims in 2021 and the provision for future years is negligible. This is despite it being manifest in recent reviews that the battery and manufacturing issues are far from over.

Here's the outlook:

We are confident that the middle part of this year will see a step change in gross margin performance, as planned. We have recently begun to ship our new entry level products, a project we initiated in 2020, which will add to the gross margin performance of the overall business beginning Q2 2022.

They have been talking about improvements to gross margins for 3 years now.

We are excited to have begun the second and major phase of our partnership with Techem. This is a transformational opportunity, from which I expect the Company and its shareholders will derive significant value. We will continue to update investors on this project's progress as we cross key milestones.

With a proven inability to execute in design, manufacturing, sales or support, this partnership is an accident waiting to happen in our view.

So how are the forecasts? Shore have 2.4p EPS in 2024 and Singer have 3.0p. Given their terrible track record, a PE of 6x would be the most Leo would be willing to pay that far out. So a possible valuation of 18p. That FireAngel are still trading at 13.4p shows how much confidence there is in these forecasts.

Forecasts show cash burn continuing for another year, plus presumably inventory rebuild, before turning around in 2023. If it does not then they'll be back to the market for more cash.

Looking at the chart this could be a speculative buy as history shows investors frequently get sucked into believing these forecasts. We've got 18-24 months before the next financial crunch, probably 12 months before a warranty provisions crunch, and who knows how long before the Germans realise who they're in bed with. Plenty of time for madness in the interim. Speculators could consider buying with a 19p target and 11p stop loss. But that's no excuse for not reading the news - either good or bad might well be ignored.

Personal Group (PGH.L) - Preliminary Results

Group revenue of £74.5m (2020: £71.5m)

Looks great right? Recovered from covid. All happy? Well, no. Revenue is a completely irrelevant metric for the company due to the high and increasing level of passthrough revenues.

Adjusted EBITDA* of £6.1m, in line with market expectations, (2020: £10.1m)

Most of their profits come from the core business of selling simple but overpriced products that payout if you get ill and somehow manage to find space in a hospital.

If you view the National Lottery (payout ratio 53%) as a "tax on stupidity", then you'll take a dim view of the customers of a product with a payout ratio of under 25%. But at least most customers aren't so stupid as to go online a buy it themselves. No, these products need to be sold, in person, on the back of a recommendation from their employer. This sales activity stopped during much of covid, while attrition continued, albeit at reduced levels. The result is a fall in policies in force that will take years to recover.

Operational gearing deals with the rest. The key metric here is:

93,147 insurance payers (2020: 103,497)

Unfortunately, that was almost 3 months ago now and no update has been provided. The most we have is:

Post-Period Trading and Outlook

· Continued strong trading in line with market expectations, including good momentum in insurance policy sales

Although major client wins during the period do bode well:

Record number of new client wins in a single year, including goods retailer Homebase, Avanti West Coast and The Royal Mint

Profitability and cash were ahead of Cenkos forecasts but they downgrade FY2022 on fears that the NHS might get around to treating people, triggering higher payments. Without current customer numbers, it is difficult to estimate their run-rate and verify their forecasts, but this will have stabilised now and increased EPS forecasts are credible.

Still, with 2023E EPS still only 16.7p (versus 28.4p pre-covid) recovery is expected to be slow as the insurance book is rebuilt. For some reason though the share price has already recovered to pre-covid levels resulting in some crazy PE Ratios.

Like with Driver, Leo is fussier about who he does business with nowadays and this is not a company he feels comfortable holding at any price. But FWIW they currently look wildly overvalued.

Ebiquity (EBQ.L) - Final Results

This is a small cap that very few people have heard about. It is an advertising analytics business with an impressive client list. However, its performance over the last few years has been less impressive as it is transitioning to being a more digitally focused business. This week we got their Final Results:

So reasonable revenue growth there, but comparisons to 2020 don't really give us much of an idea of true performance. Too many businesses have been bid up recently on the idea that they are growth stocks, whereas the reality is they simple benefited from covid or the recovery out of covid and are now returning to type.

Here is the table from the 2019FY results:

So these figures are perhaps less impressive in this context. The company always seems to have a big gap between underlying and statutory figures so we really need to take a look at these adjustments next:

The statutory operating loss of £5.1 million (2020: £2.9 million) is calculated after highlighted items including the accrual for the post-date renumeration relating to the acquisition of Digital Decisions BV, as detailed below.

· £7.9 million charge to accrue for post-date remuneration payable in 2023 relating to Digital Decisions BV, acquired in January 2020

· £0.5 million charge relating to share-based payments

· £1.1 million charge for amortisation of purchased intangibles (2020: £1.1 million)

· £0.3 million charge for professional costs relating to acquisition and bank facility agreements

· £0.4 million tax credit on highlighted items.

It seems right to remove deferred consideration as a cost from the income statement, but this needs to be accounted for as debt:

The contingent consideration relating to Digital Decisions BV is being accounted for as post-date remuneration as payment is dependent upon the principal vendor remaining in employment with the group. This will be payable in 2023 and the amount due will be calculated as six times the average profit generated in the two years ended 31 December 2022, from digital media solutions developed by the Digital Innovation Centre, less the initial consideration of £700,000 paid in January 2020. The current estimate of the deferred consideration payable is £12.5 million.

So that's £12.5m that really should be accounted for as debt. This can be paid as shares but of course, that dilutes existing holders and doesn't change the capital structure. Share-based payments can only be adjusted out, in our opinion, if you take the fully diluted share count. Amortisation of intangibles is normal to adjust out, but this is a company that has grown by acquisition and almost all its assets are intangible so this is perhaps less reasonable than many other companies. Still, these are no cash.

Free Cash Flow after accounting for leases is about £3.5m, so this is nicely cash-generative. Although a good chunk of that has come from releasing working capital.

Net Working Capital including contract liabilities is now negative £3.9m so there is a limit to how much they can push this going forward. Net Bank Debt is down:

Strong financial position at 31 December 2021 with net bank debt of £4.8 million (2020: £7.8 million) comprising cash balances of £13.1 million and bank debt of £17.9 million. The Company had undrawn bank facilities of a further £5.0 million

And also today they announce two extra acquisitions on top of a small one they did earlier in the year: MediaPath and Media Management

So they are paying £6.1m for MML and £15.5m for MediaPath and raising £15m before costs via a placing at 53p. This is probably about £14m after costs. And a large dilution:

The Placing will comprise a minimum of 28,301,886 Placing Shares, representing approximately 34.0% of the existing issued share capital of the Company.

However, they say that:

the Transaction is expected to be accretive to earnings per share prior to the realisation of any synergies for the current financial year to 31 December 2022 and beyond.

Plus:

Ebiquity believes that it will be able to generate meaningful synergies from the acquisitions and that there will be benefits to the Ebiquity Group of integrating MediaPath and MML simultaneously into the existing business.

Handily they give us some figures:

On a pro forma basis, the Enlarged Group would have had FY2021 revenues of £74.8 million and operating profit of £7.3 million.

The operating profit from the current Ebiquity was £4.7m so this is a meaningful increase of more than 50%.

The pro-forma balance sheet would be £12.5m net debt as they say they will be using £7.7m cash to finance the acquisitions. Add in the £3.9m of negative working capital, £12.5m existing deferred consideration + £3m MML deferred consideration and we have £31.9m total.

Here is the proforma market cap:

Using the proforma EBIT figures given we can calculate pro-forma valuation metrics:

Sadly, we can't see the Panmure Gordon note that provides future forecasts, although prior to today's acquisitions they were forecasting a 40% growth in EPS for FY22. If we assume similar growth rates in the acquisitions then this could be on an EV/EBIT of around 10. Not crazy if you expect them to generate good synergies from the acquisition. However, not obviously cheap either, given that almost all of the growth is coming from acquisitions and the performance of the company was largely static even prior to the covid impact.

This may give some pause for thought too:

Rob Woodward, Nick Waters, Alan Newman and Richard Nichols intend to commit a total of £75,000 to the Placing.

£75k out of a £15m raise for an entire management team isn't exactly a big vote of confidence.

Those who like roll-ups and are willing to take a risk on this management team may be keen to jump on board. Personally, Mark prefers to wait and see how these things go, or wait for a more compelling valuation. He likes the story here, he’s just not willing to pay upfront for what is largely an unproven narrative at this stage.

Pressure Technologies (PRES.L) - Trading Update

When we last looked at this following prelims in January, we said:

Perhaps more by fortune rather than any good judgement by management, Pressure may find itself in a favourable position in the next few years with hydrogen, defence and oil & gas all in strong cyclical up-trends.

However, with the dreaded H2-weighting already being flagged for 2022 and no meaningful hydrogen revenues until 2023, the wait and see approach remains the best option here.

It is perhaps no surprise that the company majors on these trends in the trading update:

In Chesterfield Special Cylinders, the overall order book has reached its highest level for over five years, as order intake for high-value defence contracts increased during the first half of the year, with manufacturing scheduled to commence as expected in the second half…

As expected, during the first half of the year, the pipeline of opportunities for static and mobile hydrogen storage systems for delivery in the remainder of FY22 and FY23 grew significantly…

In Precision Machined Components, following a prolonged period of challenging oil and gas market conditions and Covid-19 disruptions, steadily improving enquiry and order intake levels are encouraging

However, these only end up as an inline statement overall:

…the Board remains confident in meeting full-year market expectations.

These expectations are for 2.95p of EPS and the company had previously flagged an H2-weighting. This makes the current forward P/E around 30. So not exactly a bargain, then. 2023 estimates are for 6.44p EPS which would make the company look better value. However, with years of underperformance, this perhaps isn't a company you should give the benefit of the doubt.

Still, maybe we should have realised that this is exactly the sort of company where the market will buy the narrative and sell the numbers. As such, we've missed out on an almost 40%+ rise in less than a month. Although, the price is only back up to where it was 6 months ago.

Mark is not inclined to chase it now, particularly since the next news is likely to be the relatively poor H1 numbers and the valuation looks stretched in the short term.

Aukett Swanke (AUK.L) - Final Results

Note that these are for 30th September, not 31st December, so basically the day before they would have got suspended for not filing accounts. When these are your highlights, you can see why they may wish investors ignore them:

Revenue (less sub consultant costs) decreased by 22% to £8,822k (2020: £11,336k) primarily due to the continuing impact of COVID leading to uncertainty in decision making and inevitable delays.

Businesses in both the UK and the Middle East were loss-making however Continental Europe made a profit (excluding Group management charges) of £330k.

The overall loss for the year was £1,136k (2020: loss £20k), largely due to sup-optimal group plc costs and a one-off impairment of £249k.

Even the outlook doesn't really manage to put much of a brave face on it:

I fully expect our management team to continue to steer the Company around the current difficulties, always looking for suitable business opportunities.

Unfortunately, with nothing in the way of tangible assets and a current ratio of just 1.05, this doesn't have a lot of time or flexibility to turn things around. They required a bank covenant waiver last month:

In February 2022 the Group received a 3 month covenant waiver to avoid the risk of a breach on the net gearing covenant from February to April 2022. The Group will then attend the scheduled 6 monthly review with Coutts & Co in May 2022 to discuss the Groups' financing needs. The Group is therefore currently reliant on the ongoing support of Coutts & Co.

The scrape doing their accounts as a going concern by claiming that they have some, as yet unspecified, actions they will take:

The Directors are considering a range of options regarding our strategy for the Group structure and geographic footprint to stabilise and improve the Groups' underlying financial position. With this in mind, the board has a reasonable expectation that the Group will have adequate resources to operate for the foreseeable future, however we face the usual uncertainties that occur in our market regarding the future levels and timing of work that are made by client decisions which are beyond our control, which could result in the Group requiring additional external financing.

Despite a market cap of just £2.3m, it still looks overvalued. It is the sort of business where the most humane option would be to put it down.

Brand Architekts (BAR.L) - H1 Results & Merger with InnovaDerma (IDP.L)

Unlike Aukett Swanke who are actual architects, Brand Architekts is a consumer healthcare product company. They are similar to Creightons, except Brand Architekts sold off their production operations for a big chunk of cash a few years ago to focus only on the brand side of the business. That they have lost money ever since perhaps shows the strength of those brands!

As well as the proposed merger with InnovaDerma, Brand Architekts released their H1 results today, where the losses continue:

Loss before tax of £1.1m (H1 2021: profit before tax of £0.4m) absorbing additional freight charges and also increased marketing spend for theunexpektedstore.com marketplace launch.

And the cash is dwindling, although at a slow pace:

Net cash position as at the period end was £17.3m reflecting an additional £1.0m contribution to the Group's defined benefit pension scheme and planned capex investment in the new DTC marketplace.

Prior to today's offer for InnovaDerma, Brand Architekts traded at just a small premium to their net cash. The InnovaDerma takeover is described as a merger, since just 7p of the offer is in cash or about £1.2m. The cash part of the deal was 7p leaving 40.7p, at least at yesterday's Brand Architekts price, to be met from the issue of Brand Architekts shares.

When Brand Architekts themselves have £17.3m worth of net cash on the balance sheet, being willing to issue this many shares suggests that they themselves don't value their own business above net cash value. Given that BAR have £10.2m of Intangible Assets on the balance sheet, which will largely be the brands they already own, and they prefer to issue shares close to net cash value rather than utilise that cash, perhaps they should be writing down these intangibles to zero?

The alternative explanation is that perhaps the larger current shareholders of InnovaDerma want to own a stake in the larger business rather than take the cash:

Following Completion, InnovaDerma Shareholders will own approximately 38.7 per cent. and Brand Architekts Shareholders will own approximately 61.3 per cent. of the enlarged issued ordinary share capital of Brand Architekts.

However, if this is the case, why not offer all cash, or a higher proportion of cash, to smaller shareholders who want it and all shares to the larger holders who want to own the larger business. InnovaDerma has pretty much has no institutional holders though:

So perhaps the outcome would be the same anyway. In any case, it shows how little value InnovaDerma holders place on Brand Architekts shares when they want a 70% premium for InnovaDerma largely in Brand Architekts shares that are trading only just above net cash!

The Brand Architekts shares have not reacted well to this announcement, falling 20% to 85.5p. This makes the current offer worth 39.6p.

As of Thursday lunchtime, InnovaDerma trades are going through at 36.4p so there is a decent arb here if you think it is a done deal. Realistically, you won't get the borrow on Brand Architekts so this is only worth doing if a) you already held Brand Architekts, b) think the deal is certain to go through and c) like the combined entity.

The benefits of this merger are given as:

Value creation for both sets of shareholders, underpinned by cost and revenue synergies. The Merger is expected to result in recurring run-rate pre-tax cost synergies of c. £1.5 million - £1.75 million per annum, primarily driven by:

o the harmonisation of the Combined Group's supply chain and DTC business relationships;

o a reduction in staff costs across the Combined Group; and

o a reduction in duplicated public quoted company costs and certain operational costs and overheads.

Which is perhaps a tacit admission that Brand Architekts was subscale and if left alone was going to simply waste their cash pile on continued losses.

The other factor that may affect the Brand Architekts valuation is that when they sold their operations they kept the pension deficit, and while the IAS19 value is down to £9.2m in the results released today, the Triennial is likely to be significantly higher and require ongoing payments. Perhaps another reason that InnovaDerma holders seem less than keen to take Brand Architekts equity.

The current commitments from shareholders look weak:

Brand Architekts has therefore received irrevocable undertakings in respect of a total number of 6,479,973 InnovaDerma Shares representing, in aggregate, approximately 23.1 per cent. of InnovaDerma's issued ordinary share capital as at the close of business on the Latest Practicable Date…

Brand Architekts has therefore received irrevocable undertakings and letters of support to vote in favour of the Brand Architekts Resolution in respect of a total of 3,134,425 Brand Architekts Shares representing, in aggregate, approximately 18.2 per cent. of Brand Architekts's issued ordinary share capital as at the close of business on the Latest Practicable Date.

So not exactly high committed percentages. But again the almost complete lack of institutional holding in InnovaDerma may explain the low numbers there. Brand Architekts has more institutional holders so will be interesting to see which way they vote. A 20% drop in a Brand Architekts share price that was already trading close to net cash (excluding the pension deficit) perhaps won't help matters.

So this definitely doesn't look like a done deal at this stage.

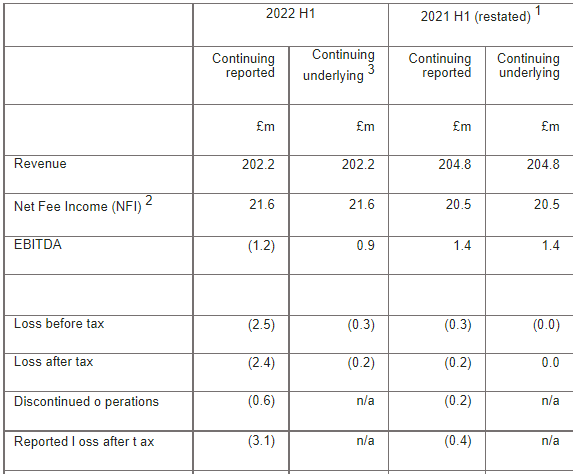

Gattaca (GATC.L) - H1 Results

We already know they will be a loss given the previous profit warning where they said that underlying PBT will be breakeven for the full year. The issue isn't so much their Net Fee Income, although not being able to grow this at all at a time when other recruiters are performing well is not good, it is that costs have increased:

One of the advantages of these sorts of recruiters is that in a downturn they throw off cash as the working capital unwinds. The flip side is that they suck in working capital as business improves. This means net cash has reduced significantly:

Compared to the same time last year it is the increase in receivables that accounts for the difference, yet compared to the year ended 31st July it is the reduction of payables. A lot of this was deferred VAT. This does mean that the company now trades at a discount to TBV. And a lot of these assets are liquid working capital. The problem is that unless these assets become productive they will remain "busy fools". Equity Development are forecasting this to happen as soon as next year:

However, the analyst here is Paul Hill - a man who has the power to remain impressively optimistic even in the direst of circumstances. And certainly doesn't have a great track record here by putting a £3.50 price target a short time ago when the share price was trading at an inexplicable £2.80 per share.

Still, everything has a price, and if the shares were trading at a very significant discount to tangible book value, they could certainly be worth a punt. Especially given the track record for this to attract excitable investors. However, with net cash reduced and likely to fall further as business picks up, no dividend declared in these results and an outlook of break-even at best then we’re not sure 0.87 x TBV has a sufficient margin of safety to tempt the bargain asset buyer yet.

Numis (NUM.L) & Peel Hunt (PEEL.L) - Trading Updates

A tale of two updates on Friday. Numis’ has not been particularly well-received as they say:

Overall, revenue for first half is expected to be in the region of £74m, approximately 36% below the record six month performance achieved in the comparative period.

In contrast, Peel Hunt say:

Following on from the trading update issued on 23 February 2022, the Group's trading performance has been ahead of revised analyst expectations, following a strong end to the year from our Execution & Trading business. As a result, revenue for the full year is expected to be around £131m.

Of course, the Peel update comes 2 months after they said:

[The] Company now expects full year revenue to be marginally below the bottom of the previously guided range and accordingly earnings will be commensurately lower than current market expectations.

So this is a bit like the UP Global Sourcing forecast beats of 2021, where the analysts slashed forecasts by far too much and then the company repeatedly beat them but the overall level was below where they were forecasting previously!

Peel say:

Our pipeline of Investment Banking deals remains strong, albeit there is heightened execution and timing risk in the current environment. The number of retained corporate clients continues to grow, with 19 new clients added during the financial year.

The client growth adds to future business potential. And:

We continue to benefit from our diversified business model, demonstrated by the increase in Execution & Trading revenues during periods of higher market volatility. In addition, our broad range of Investment Banking services and increased institutional commission market share leaves us well placed to benefit from any ongoing market dislocation.

Whereas for Numis the volatility seems to have hurt them:

Within our Equities division, Institutional income delivered a robust performance in line with the second half of FY21, whilst the challenging market conditions in recent weeks adversely impacted the profitability of our trading book…

….our trading profit has been negatively impacted by the extreme market volatility of the last eight weeks of the period.

Perhaps they had taken blocks of client stock prior to the war in Ukraine breaking out and had yet to clear these. Numis highlight that M&A remains their stand out in current markets:

M&A continues to be positive with a large number of announced but ongoing transactions, and a strong pipeline of future business.

We expect these trends to continue in the short term, with a potential read-through for others where M&A is a large part of their business.

That’s it for this week, enjoy your weekend!