Small Caps Live Weekly Summary

SCL Meet BOO SOM CAPD FCAP GTC

Not long to go now until the SCL Investor Meet on 23rd March and the good news is that an additional high-quality company has agreed to present - Conor Rowley, Corporate Development & Strategy Manager from Capital Limited (CAPD.L), will present the company’s future strategy.

This is in addition to a presentation from Mark’s Electrical (MRK.L); very relevant investor presentations on Investing in an Inflationary World and Staying Rational in Irrational Times; and an interview with Glee Club founder and active value investor Mark Tughan. There will also be plenty of time to socialise, catch up with old friends and make new ones.

This in-person event is free to attend and easily accessible by Train and Car. Make sure you register here to get full details.

The terrible news from Ukraine continues, and although the Russian military appears to be taking heavy losses, it is the intentional targeting of the civilian population of Ukraine by the Russian army that is the most shocking. In response to this, Western democracies are increasing sanctioning Russia and freezing the assets of those who prop up the dictatorship. World powers are aligning themselves with or against Russian aggression with the consequence that global supply chains are under threat and commodity price inflation is here to stay. In these times, investors need to look for not just primary effects (don’t invest in Russia) but secondary ones as well (whose business is reliant on global supply chains that are now breaking down.)

Small cap markets rarely apply these principles rationally though. Earlier this week many small cap stocks fell significantly, not because they were the most badly affected by the war, but simply because they were popular PI stocks. Presumably, investors were either panicking or this was the consequence of over-leveraged investors receiving margin calls and having to meet these buy selling illiquid stocks into a weak market. Many of the most sold off names recovered later in the week, as liquidity returned to the market. In an uncertain world, one thing is certain - now is not the time to be leveraged, particularly in popular small cap names.

Large Caps

BooHoo (BOO.L) - Trading Update

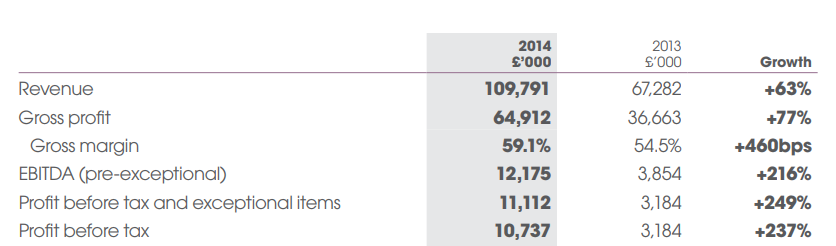

A quite incredible chart here:

On Tuesday afternoon they bottomed out at under 66p. Before bouncing strongly on this week’s results. This compares to the IPO price in 2014 of 50p. This is what the accounts looked like back then:

Compared with £1.7bn of revenue and £91m of net profit in FY2021. That's well over 10x what they did in the annualised figures immediately pre-float and their reported FY 2014 figures. So you might have expected the share price to be up by more than 30% in that time.

Shareholders, however, have been panicking that the growth might be over and that margins might be falling. And seemingly, the more the share price falls, the more concern there is over sourcing and the trustworthiness of the founding Kumani family. In this context, this week’s trading update seems to have reassured:

Boohoo provides an update for the three and twelve months ended 28 February 2022. The Group has delivered net sales growth in the fourth quarter of 7% (2 Year growth: 48%), and over the full year of 14% (2 Year growth: 61%), in line with guidance.

By quoting 2-year figures they seem to be positioning 2021 as exceptional. Certainly it was in terms of profitability, which was partly driven by the "loungewear" lockdown trend of clothing that was much more likely to fit first time.

In the fourth quarter, gross sales growth was strong (+26% vs. last year and +57% vs. two years ago). As expected, net sales growth in the quarter was impacted by higher returns rates year on year due to product mix. This is expected to continue in the first half of FY23.

The other thing that made 2021 exceptional in retrospect was that they were efficiently delivering large quantities of goods directly from the UK to customers in the EU and US:

The USA had grown particularly quickly:

But the pandemic (and likely Brexit) has increased overseas delivery times dramatically, to the point of threatening its entire viability. Today they say:

In the UK, the Group continues to deliver a strong trading performance with our leading proposition resonating with customers. International performance continues to be impacted by longer customer delivery times as a result of pandemic-related supply chain pressures. However, in the fourth quarter, the Group saw a return to growth in ROW due to the positive contribution from wholesale.

It would have been nice to get some news on the US distribution centre. But, given there has been no update since mid-December and that the share price had almost halved since then the following was certain to reassure:

The Group expects, subject to audit, to report adjusted EBITDA for the financial year ended 28 February 2022 of approximately £125 million, in line with prior guidance issued in December and market expectations (company-compiled consensus adjusted EBITDA for FY22 of £125 million).

The 15% rise on these results puts the total gain from Tuesday's lows at +40%. While unlikely to repeat this rate of recovery, they continue to look sensibly valued and Leo is happy to hold a small amount in the tail end of his portfolio. The situation with sourcing is now no worse than other similar companies and unlike UP Global Sourcing, for example, they have suppliers across the world, and while many are in China, Pakistan and India who support the Russian genocide to various degrees, they also have a diversity of suppliers in friendly countries. There is a small exposure to Moldovan sourcing which would be a problem in the case of a Russian invasion.

Small Caps

Somero (SOM.L) - Final Results

Although these were great results, these were largely expected as the numbers were in line with what we knew already. Indeed, the title of the finnCap note is "FY21 extraordinary growth, no change to forecast". 2022 is expected to be a year of consolidation. Although they said that at this time last year and then proceeded to continually upgrade expectations throughout the year.

It is worth noting the difference between the CEO & non-exec Chairman’s outlook comments. Jack Cooney says:

Following what has been an exceptional year, we expect to deliver modest growth in revenue and consequently profitability in FY 2022, on top of what has been an exceptional year.

And also mentions their expansion:

In H2 2021, we started a US$ 9.5m project to add 35% more operating capacity to our Houghton, Michigan Operations and Support Offices, adequate to support a business with US$ 175m in revenues, that we expect to complete in H2 2022.

Whereas Larry Horsch mentions:

With these planned investments, primarily in the form of staffing additions, we expect an increase in 2022 operating costs that will exceed our traditionally targeted US$ 2.0m.

And then:

Following an extraordinary year in 2021, with remarkable growth and record revenues and profits, 2022 revenues are expected to grow at a modest rate, and with the investments for future growth being made, 2022 EBITDA is expected to be comparable to 2021.

We doubt there is a significant shift in the ITDA part of EBITDA which makes these statements slightly incongruous! The mismatch would perhaps suggest varying levels of caution. Jack comes across as always optimistic, although he's been right to be so in 2021.

However, 2020 was a weak comparator, with H1 particularly bad as coronavirus hit just as customers would have been buying ahead of better spring weather. And not only was 2020 down on 2019, but 2019 was very weak too, purportedly on bad weather. So the revenue CAGR has only been 12% since 2018. Nevertheless, 51% growth in one year is organisationally quite difficult even in normal times. As they say:

Underpinning these remarkable results was our ability to reliably meet customer equipment delivery requirements so that our customers could continue work on their projects. This was critical to achieving the growth we experienced and is an accomplishment that set us apart from many other companies. Our team faced many challenges in 2021, not the least of which were supply chain delays and the COVID impact on the labor force, yet through the resilience of our employees, we overcame each obstacle and we met our customers' needs.

So it sounds like they met all of the customer demands...but only just. However, this is not reflected in the inventory. They comment:

higher level of inventory in 2021 due in part to new products launches.

An inventory build is not consistent with a company that only just managed to deliver customers’ requirements. Yes, some of that will be inflation, some is a larger business, some is normalisation and some is new products, but in no way did they sell out of stock. So where did the growth come from? The subheading of today's results is:

Healthy North American market drives strong finish to 2021

And North America is pretty much all that matters at the moment, with 80% of revenues from there. Europe is severely unrepresented on a comparative population basis and is falling behind further. They have failed in the China market and it seems they are only maintaining a presence there going forward to monitor the market.

There is a bright spot in Australia where switching to direct sales (or, more likely, associated publicity/promotions) resulted in a large percentage increase on a very small base. If similar absolute increases in sales continue for another 4-5 years then it will start to become significant.

For all the new products, then dependence on boomed screeds has also increased:

There are two ways of looking at this - either the failure of other regions to get traction is a weakness, or an opportunity if those regions take off as NA has, but with some delay. We really don't know which way to lean on this.

Looking forward, we know that concrete costs have increased due to rising energy costs. But, working capital movements on accounts receivable and especially accounts payable suggest a strong end to the year. In the CEO review we have:

The outlook for North America is positive supported by expected continuation of an active US non-residential construction market and supported by customer feedback indicating project backlogs extend well into 2022.

We have revenues from relatively new products that they couldn't previously demonstrate on-site and also brand new products now being produced. The US is much less affected by higher energy costs than the rest of the world. Commodity inflation is both a blessing and a curse - it may impact the demand for infrastructure but we know it is spilling over into labour inflation which means increased demand for automation on both the end customer side (more flat floors) and the immediate customer (labour-saving Somero machines). And there is a lot of optimisation still to go on distribution warehouses, even if total capacity requirements stall. So the situation is quite balanced.

Still, the 11%+ Earnings Yield with all new product development costs expensed looks very good value for such a high-quality company with great cash generation and commitment to shareholder returns. The heavy reliance on boomed screeds in the US means that it is not without risks, however, or opportunities, depending on your viewpoint.

Capital Limited (CAPD.L) - Full Year Results

We knew revenue and rig numbers/ARPOR already, so starting with what we didn't know - gross profit is way above where Mark had estimated, coming in at $106.3m vs c$97m. 47% Gross Margin is phenomenal for a mining services business, particularly given the increase in typically lower margin mining services revenue. This shows how strong the market is and good on-the-ground cost control. On the conference call, management mainly put this down to fewer large-scale rig moves and better maintenance on newer assets.

Admin expenses are up more than Mark expected though and had increased further in H2 vs H1. But the overall result is EBITDA some 7% above where he expected, and about 20% above analysts’ consensus. 2021 EBITDA was even above analysts’ previous consensus for FY22.

Depreciation, Tax, Finance are roughly in line with what he expected, giving a Profit After Tax of $36.6m or some 20% above Mark’s expectations. So a decent beat on earnings.

As expected, there was little Free Cash Flow since they invested heavily in capex to support new contracts plus there was some working capital build. The working capital is not expected to increase further in FY22, and net debt reduced slightly in H2 showing that they are likely to be past the peak in terms of investment exceeding operating cash flow. Looking forward they say:

Revenue guidance for 2022 of $270 to $280 million driven by an increased drill rig count, contract extensions and expansions from existing long-term contracts, load and haul waste stripping contract at Sukari, Egypt running for the whole year at full capacity and MSALABS continuing to grow through 2022;

Again from the call, it was explained that this revenue guidance range was based on a $170-180k ARPOR. Given this was $184k in Q4 there seems some scope to beat this range. The last year has shown that the management team have definitely under-promised and over-delivered so could well do again. The macro environment is strong even without the recent gold price strength and verbally the management said:

We can't emphasise enough how supportive the current macro environment is for a mining services company.

They are unlikely to face significant inflation impacts either. Fuel is less than 5% of their cost-base and is often provided by clients. Labour inflation may be more significant but all their long-term contracts have rise and fall clauses in there. Parts availability is tighter than in the past but they are not seeing and meaningful impact on their business. Rig procurement timescales have moved out from 3 months to about 6 months but they have the scale and financial strength to book slots and pay deposits to mitigate this.

The standout performer is again MSALABS, and although it is a smaller part of the business, its growth rates are making it increasingly significant. Good to see management listening to shareholders on this and providing specific guidance on this in their presentations:

The guidance of $30m revenue is significantly above Mark’s previous assumption. His expectation was that growth would start to slow with scale but there seems little sign of that. The Annual Report shows MSALABS making a loss for the full year, however, management have stated that this is now profitable, which is impressive for a company growing revenue 100% pa.

It is the roll-out of the Chrysos technology is driving that forward growth, but management were keen to point out that not much of FY21 growth was Chrysos-related. The Chrysos units that are being commissioned this year will further drive revenue growth. And they are in advanced discussions for further Chrysos units to be deployed in 2023-24 so there is plenty of scope for further growth in future years. Although they don’t own the Chrysos IP, Capital have a first-mover advantage on this tech outside of Australia. Chrysos are being strategic in their roll-out and don’t want geographic overlap in regions so they are unlikely to face competition with the same tech, at least in the short and medium term.

Looking forward to 2022 as a whole, we now have the revenue guidance of $270-$280m, and if we go for the midpoint of that and an ARPOR of $177k that implies $191m of rig revenue, $54m for mining services and $30m for MSALABS. Assuming the Gross Margins drop a couple of percentage points in FY22, then we get $122.8m Gross Profit for FY22. This could be beaten since they say their ARPOR assumptions in the revenue guidance are for a reduction, which perhaps seems conservative for where we are in the cycle.

If we say $37m Admin costs, which is closer to the annualised 21H2 run rate than FY21 then we get about $86m EBITDA. Perhaps more, if MSALABS starts to contribute significantly to EBITDA going forward. There is also scope for EBITDA to be higher if they win further mining services contracts, although this may increase capex above their $45m guidance for FY22. So base case, a 17% rise on FY21.

So where does that leave us on valuation? One of the differences between us and the mainstream analysts is that we separate out MSALABS. In their latest note, Tamesis do say:

The laboratories business in particularly is growing at an extraordinary pace and we suspect sooner or later may warrant its own separate valuation as part of a SOTP analysis.

Perhaps this is because they haven’t been given enough details by the company to be comfortable with a valuation. Regardless of the reason, this means that all brokers currently value MSALABS at close to zero (since they apply a small multiple to the small amount of EBITDA this produces which is co-mingled with the consolidated results).

A negligible value is, of course, daft. Growth stocks tend to be valued on sales multiples and despite growth stocks facing a significant derating recently, we don’t think it is unreasonable to apply something like a 5x TTM Sales multiple as a mid-case to a business growing revenue at 100% pa. This would make it worth c$60m.

For the rest of the more mature businesses then applying an EBITDA multiple is more valid. Tamesis say:

Surely a business such as this should be trading near 5x EV/EBITDA for 2022?

However, we prefer to be a bit more conservative, separating out Capital Drilling from Capital Mining and applying the industry average multiples to these. Thankfully we don’t have to calculate these ourselves since Capital provides these in the appendix to their presentations. These multiples have tempered somewhat recently due to good results from competitors and perhaps the market anticipating that we are slightly closer to cycle peak, plus general equity market weakness and they now stand at 4.1x EV/EBITDA for drillers and 3.2x for mining services.

Using these multiples and assuming a pro-rata split on admin costs, we get a $70m valuation for Capital Mining and $263m for Capital Drilling. In terms of Capital Investments, applying a 10% discount to valuation to reflect illiquidity would seem wise.

Putting this all together generates a fair value mid-case valuation of £1.65 per share or some 70% above the current share price. It could be argued that Capital should trade at a 20% or so premium to the average company in its market sector since it has higher margins and longer contracts than the industry average. In this case, a valuation of around £2.35/share would be more reasonable. All of these figures would increase if the $270-280m revenue range does prove conservative for 2022.

This means that Capital remains at a large discount to similar listed competitors, and that discount has increased since the share price didn’t respond to this week’s earnings beat.

Tamesis retain their £1.40 price target, although their preferred metric of 5x EV/EBITDA would imply a price target of around £1.75. Berenberg increased their price target to 138p from 134p and retain their Buy rating, although without seeing the note then we can’t judge the rationale behind this. These price targets perhaps reflect more about how brokers’ targets tend to work, being chosen largely by applying an acceptable premium to the current share price, than driven by absolute valuation. As such, Capital remains a company where it pays to do your own research.

finnCap (FCAP.L) - Trading Update

We have been saying for some time that finnCap’s revenue guidance looked too low based on our analysis of their public deals and this week they confirmed it:

…pleased to confirm that unaudited revenue for the year to date has now exceeded the top end of its £45-£50m guidance range.

Questions remain over the outlook for FY23, however. Given the current market conditions, IPO's are understandably dead in the short term. However, finnCap is a more diversified business than in the past with M&A advisory still going strong and ESG advisory being in demand. Even on the equity raising side, we were pleasantly surprised to see them get three placings away this week for Destiny Pharma, SRT and Parsley Box. Although the amounts are only in mid-single-digit millions and required a 25%+ discount in most cases.

We also expect the company to report significant cash balances at the year-end, which gives them a lot of flexibility to take advantage of any short-term weakness.

Getech (GTC.L) - Agreement with the Highlands Council

In light of the ongoing issues with oil and gas from Russia, increasing focus is being placed on renewable energy sources, including hydrogen. Getech are continuing their green energy transformation:

The Highland Council and H2 Green have agreed a vision to create a regional network of green hydrogen hubs across the Scottish Highlands. This infrastructure will accelerate the decarbonisation of the Highlands council area, the largest administrative unit in the United Kingdom covering almost a third of Scotland.

While this all sounds great, the reality may be more mundane. Hydrogen hubs are really just petrol stations for Hydrogen cars or trains. So this is a refuelling project for a product that doesn't exist yet, at least on the car side.

In line with these goals, we have already announced agreements with Eversholt Rail to accelerate the wide-scale deployment of their hydrogen-powered trains on the Far North and West Highland Lines of Scotland.

Eversholt do have a Hydrogen train operational in Germany. However, the highlands of Scotland is one of the most uneconomic areas for transport given the large distances and relatively low population. So this really should be the last place to adopt hydrogen cars.

The problem is that Getech’s history, and still core business, is as a provider of seismic data and analysis tools to oil and gas companies. They have no history of successfully delivering large scale construction projects in a regulated industry, and certainly not ones featuring new technology and significant safety hazards. Nor are they currently capitalised to do so. Complex construction projects have a habit of over-running, sucking in capital and causing problems for even large companies.

This is perhaps why this is just a Memorandum of Understanding at the moment and why the best news is that:

The Highland Council will contribute £100,000 to the cost of this initial work.

Which will delay the next Getech placing by at least a month!

That’s all for this week, enjoy your weekend.