Small Caps Live Weekly Summary

Mello WIX CAPD CARR MTEC GDP NWOR ZYT

A shorter summary this week due to UK bank holidays. As always, if you think we are missing something, then join us on Discord to have your say.

Don’t forget to get your tickets to the Mello investing conference that we will all be attending. And, with the early bird discount expiring, we have our own discount code: Simpson50 gives 50% off tickets to Mello 2023. Tickets can be bought here:

https://melloevents.com/mello2023tickets/

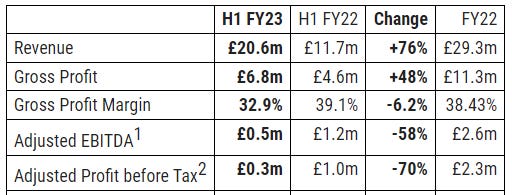

Wickes (WIX.L) - Q1 Trading Update

A steady but unexciting Q1 update from Wickes:

Wickes has made an encouraging start to the year with performance in line with our expectations and the prior year. For the first 16 weeks of the year, Group LFL sales were down (0.6)%. Delivered DIFM sales were ahead by 9.3%, with Core LFL sales down (3.6)%. Both periods include Easter trading.

They say it is weather impacted in core:

Core sales have been affected by adverse weather in 2023 to date, affecting outdoor and weather-related categories. Storms in the prior year also drove significant sales uplifts in fencing in the comparative period. Sales trends have improved towards the end of the period as the weather has started to normalise.

We are not sure the lack of storms is a big impact, but the cold weather certainly is. For example, Mark is only just beginning to buy gardening items such as plants, so he will be clicking & collecting things like compost from Wickes shortly. Last year these would have been bought much earlier in the year.

On the Wickes thread on Discord, contributor SamG has written up their extensive research on Wickes, and that is well worth checking out.

Capital Ltd. (CAPD.L) - Direct Investment Update

It seems investors may have been asking them to clarify exactly how much Allied Gold they currently hold! This is the reason:

It is presently expected that Allied Gold will become a public company and list in North America on or before August 31, 2023…

The planned pre-money valuation is expected to be discounted to net asset value, and expected to be in the amount of US$1.2 billion.

On the face of it, this is excellent news because we have:

Hard backstop date for the float (aka "the becoming of a public company"): 31/8/2023.

Hard valuation of at least $1.2bn for the existing shares and an indication this is still below net assets.

The language here is a little unfamiliar to UK investors, but if the pre-raise valuation is $1.2b, then that means the $18.6m for CAPD's stake, with maybe more to come if the stock ends up trading at a premium to NAV in the short term.

This could easily see a paper gain of at least $10m. But we’d really like them to crystalise some of that gain soon. With debt costing them 10%, the ability to buy back shares at an EV/EBITDA less than 3, or deploy capital to win more long-term contracts, they potentially have better use for the capital. There should be little worry that selling their stake would impact their contracts. That they were willing to support Allied financially in more difficult times, we suspect buys them a far stronger working relationship than holding around 1% of the listed company.

Carr’s Group (CARR.L) - Interim Results

Anyone interested in Wynnstay should probably be following this too. However, with a Price / TBV of 1.3x, and a forward PE of 14.0x, this is more expensive on the metrics that most attract us to Wynnstay, albeit not that expensive and with a somewhat higher dividend.

The Speciality Agriculture division manufactures and supplies feed blocks, minerals and boluses containing trace elements and minerals for livestock.

The Engineering division manufactures vessels, precision components and remote handling systems, and provides specialist engineering services, for the nuclear, defence and oil & gas industries.

So the first part has similar drivers to Wynnstay, and we will focus on that for read-across.

The increase in revenue in the period follows an increase of 35% in average feed block selling prices to pass through substantial raw material cost increases, impacting total volumes by 13% (excluding joint ventures) compared to prior year.

So looks like demand is quite elastic here. It could be that farmers stockpile feed blocks, and so reduce buying when prices are high, but it seems more likely that the product simply increases, e.g. milk yield at the margins, and the optimal amount varies with relative prices. A bit like fertilizer inputs for arable. As ever with farming, the weather will also play a part.

They go into this in some detail in the following paragraphs. The US situation looks particularly poor in the short term. But there are signs of improvement:

In the UK and Ireland, farm input prices, particularly for feed and fertiliser, are coming down, easing the pressure on customer spending budgets. At the same time, farmgate prices for dairy, beef and lamb are strong, particularly when compared to 10-year historic averages, such that investment in the quality of inputs will be repaid by the marginal gain in revenue-related traits of daily liveweight gain and milk yield. In the USA, the area affected by drought is markedly reduced from 12 months previously, whilst the cyclical outlook specifically for beef will improve as herds rebuild over the next five years.

So, compared to Wynnstay, it appears they are just exposed to livestock (feed) rather than a mixture of livestock (feed), arable (seed, fertiliser) and retail / capex. And unlike with Wynnstay, inflationary inventory gains don't even compensate for the loss of volumes and pressure on margins on a P&L basis, let from cash flow.

The engineering side is significantly smaller, with revenue looking to be typically around half that of agricultural and margins lower even in a good year. This was not a good six months. However, they are optimistic for the future on this side. As this is a small unit providing capital goods, performance will always be lumpy.

On cashflow, this was poor for the reasons you'd expect:

The working capital outflow in the period was £1.6m (H1 2022: £5.6m) driven by a reduction in inventory levels since year end, offset by an increase in accounts receivable, due in part to the continued high selling prices in Speciality Agriculture.

Overall, this looks like the kind of confusing mess that might easily get undervalued from time to time, but we see little evidence of that being the case right now, at least relative to the rest of the market.

Made Tech (MTEC.L) - Trading Update

We’ve seen many an "enthusiastic" commentator about this one on Twitter, so not surprising that this profits warning has been punished this week. This is a late 2021 IPO that disappointed early - could now be the final profits warning?

Revenue forecasts were for £43m with £5.97m Net Profit, which presumably is house broker Singer's previous forecast. Now they say

the expected adjusted EBITDA3 outcome for FY23, which is now estimated to be at least £1.5 million.

At the half-year, they said:

Market expectations for FY23 as published on Bloomberg: Revenue £43m and Adjusted EBITDA £3.9m

So don't think those Stockopedia PAT figures can have been up to date. This is HY:

So perhaps they will do £1m PBT on an adjusted basis. A loss once you exclude large exceptionals (again, this is HY):

Despite the drop in response to these results, the EV here is £25m which is an EV/EBITDA of around 16. This suggests that this is still significantly overvalued on current performance.

They trumpet an increasing backlog:

We have our strongest ever Contracted Backlog at £61 million (30 November 2022: £47.8 million), an increase of 130% in Sales Bookings to a record £75 million (30 November 2022: £32.6 million), and a portfolio of new and existing clients, who are positive advocates for our business.

Which, all things considered, should see them grow, perhaps into a more reasonable valuation. However, it would be a brave bet that this can be delivered profitably, given their recent track record. Net assets are £15.244m at the last B/S date, of which £3.373m is intangible. So TBV of £11.871m or 7.7p per share, which should provide some downside protection, eventually.

Goldplat (GDP.L) - Q3 Operating Results

This company has been facing lots of challenges, not least problems with SA electricity supply:

The South African operation lost a total of 19 operating days, 20% of the total days available in the quarter, due to electricity cuts and infrastructure related issues during Q3. We expect that the current electricity situation will continue during the next 12 months.

So in light of this, SA performed very well during the quarter:

The operating profit for the period did improve from the previous quarter by £356,000 to £1,175,000 as a result of good supply from by-products towards the end of Q2 and during Q3.

There are no quick solutions to this one, but it looks like the higher gold price and lower oil price is going to make diesel generation economic.

To add to the woes. Ghana hasn’t been able to export and, therefore, book revenue.

During Q3, GRG production remained in line with previous quarters, however, we have experienced delays to the export of product as a result of the finalisation of the renewal of our Gold Licence, which is required for export.

But the gold is ready to go to refineries, so we can expect the usual £1m operating profit per quarter when they get the final signature on the license. This may have actually done them a favour, given the recent gold price strength. Obviously, there is a cashflow impact, but they are relatively well capitalised:

Our cash balances in the group remained strong at £2,750,000 at the end of Q3, with significant balances invested in inventory and debtors with our main exposures to smelters in Europe and South Africa.

Overall, they say in line with expectations for the year. But these have been reduced previously.

National World (NWOR.L) - Acquisitions

National World continues executing its strategy of rolling up local news and digitising publishing assets. However, we are not sure they really give enough details to decide if these are good acquisitions or not. All they say is that they will more than overcome weak advertising markets. So, they will perhaps start to grow EPS again via these acquisitions?

The valuation looked fairly cheap even if you assume they largely waste their cash balance, so acquisitive action here is probably good news, although it is very hard to say for certain.

Zytronic (ZYT.L) - Trading Update

Not good. A £0.5m TBV hit and major profits warning. Revenue guidance £8.0-£8.8m versus £13.5m forecast in December. This is for the year ending September, so things deteriorated quickly. It sounds like the bigger part of the hit is from the collapse of AGA, which is permanent rather than the temporary satiation of another customer.

Basically, a major shareholder in the parent of Aruze is accused of corruption, and this is being used as a reason (justified or not) to squeeze them out. Underlying it all is a feud between two one-time associates. This has evidently escalated into claims against Aruze. As we understand it, Aruze is continuing to trade fairly normally. The issues are who is owed what and how it is shared out. You could easily see judgements reversed etc., and that £0.5m being written back, and we would imagine a creditor delivering physical goods required for the business has a better position in practice than a legal claimant. This is speculation, but perhaps Zytronic will continue to receive orders on a cash-on-delivery basis. It doesn't appear to be in anybody's interest that Aruze is forced out of business by this.

So there are several reasons why the company is now worth less than we thought yesterday:

1) Loss of confidence they will report negative developments to the market in a timely fashion

2) Likely loss of £0.5m, albeit some may be clawed back through higher prices / better terms for future sales even if none of the original debt is originally recovered.

3) Loss of 6-9 months of orders from an unknown customer

4) Deferral of 6-12 months of orders for Aruze

5) Risk of further problems from Aruze, including the bankruptcy of Aruze and/or part of the supply chain or extended disruption, however, this is balanced by the possibility of a bounceback.

6) Possible restructuring/redundancy costs.

On balance, the risk of holding is now less than yesterday due to the greater TBV cover (currently a discount to cash and property) and track record of a flexible cost base. However, there doesn’t seem to be a quick way back for the company and any recovery is pushed back by at least a year.

That’s it for this week, have a great long weekend!