Small Caps Live Weekly Summary

XAR STAF PMP CCT TND ZYT FKE CMCX GAW

This week, Wayne takes a look at the pros and cons of investing in Uranium.

Meanwhile, in small cap land, there was a rush of Half Year Results. We did our best to look through as many as possible.

It is also shaping up to be a busy week next. However, both Leo & Mark are away so there will be no live small cap live events on discord. We will attempt to comment on the general channel though.

Large Caps Live Monday 13th September

Hypothesis: Increasing demand for Uranium and insufficient supply leading to a pending crunch

Idea: Long Uranium and uranium miners

Summary:

There is a pending shortage of uranium as nuclear plants have consumed stockpiles and new plants coming online:

a. The world consumes 180M lbs of uranium / year

b. Production from primary sources is roughly 125M lbs

c. 25 M lbs from secondary sources

d. So deficit of 30M lbs / yr

As we switch to zero / low emissions we need a base load electricity supplier. Wind and solar are not 'dispatchable'. Hydro is; as is coal and gas. But there is insufficient hydro to replace all gas / coal so need nuclear.

One of the candidates for Japanese PM (a front runner) has changed his stance on nuclear. The issue is that he is happy to restart existing nukes but not clear that he wants to have new nukes

Various funds - in particular UU - which has been taken over by Sprott - are buying Uranium leading to a squeeze

The 'Apes' ie WSB are getting on the trade

To 'load' a nuclear power station with fuel to start up requires 3x more fuel than that required annually for operations.

We have got to the end of the cold war conversion of nuclear weapons from Russian into civilian use nuclear fuel (the megatons to megawatts program)

The end of Japanese uranium dumping on the market post-Fukushima:

“Because of the flood of Japanese stockpiles, the spot market became more active. But that is now starting to change. This anomaly appears to have started to reverse, which is good news for the price of uranium. Both prices are well below the industry’s average cost of production.”

From a Katusa Research report - July 2018 - 'Special Feature: Uranium Royalty Corp'

The Japanese dumping led to utilities contracting on the spot market rather than long term contracts. This appears to have been particularly so with the US reactors. As prices rise they are likely to switch to long term contracts to lock in prices.

Most nuclear miners are not viable until $50 / lbs vs $38 currently - so many mines are on 'care and maintenance' (eg Paladin Energy)

Illinois has extended the life-time of two power plants -

High LNG will drive pressure on Japan

In Dec 2020 US senate Committee approved bill for strategic uranium reserve -

Chance of a take-off of SMRs = small modular reactors

Kazatomprom considering making purchases to rebuild inventory

Japan reactor reboots

Potential Issues:

Even with a change in PM in Japan it is not clear how quickly nuclear ramp-up will commence in Japan

Not clear to me whether the Chinese will buy spot uranium or from their own mines eg Husab uranium operations (China General Nuclear Power) and Rossing (China National Nuclear Corporation (CNNC)). Paladin's Langer Heinrich Mine is a JV with CNNC.

The national policy is to obtain about one-third of uranium supply domestically, one-third from Chinese equity in foreign mines, and one-third on the open market. Increasingly, other stages of the fuel cycle will be indigenous. Uranium demand in 2020 is expected to be over 11,000 tU (with 58 reactors operating), in 2025 about 18,500 tU (for 100 reactors) and in 2030 about 24,000 tU (for 130 reactors). UxC reports that China imported over 115,000 tU over 2009-14, notably 25,000 tU in 2014 and 10,400 tU to July in 2015. With annual consumption currently about 9000 tU, much of this will be stockpiled.

How much is being driven by the current energy demand ie. the reason why Thungela is at a high.

When will mines go back on? Kuppy reckons 3 years for mines to come back on

The risk is when the governments will step in?

Where is it stored and can the capacity be restricted

Risk of Thorium reactors in time?

Old reactors being retired

Solar and wind can reduce costs further

Cost of storage

Japanese reactor reboot - many are not coming back

Small Caps Live Wednesday 15th September

Xaar (XAR.L) - Interim Results

One widely loved stock in recent times has been Xaar. This was a net net, trading at sub-20p in the depth of the COVID-19 sell-off, as the market took fright at the lack of turnaround and their cash burn.

Since then, the pattern over the last few set of results has been clear: Shareholders get their hopes up and the stock rises before the results, perhaps helped by some bullish commentators and a large holding by Schroders. Then when the results come out they are disappointing, and despite a bullish management commentary, the numbers show very little in the way of real traction on the turnaround. The share price falls on the disappointment before the bullish commentators claim it is just a flesh wound and start to pick up the “exciting” turnaround narrative again and push it to their followers.

In the most recent cycle of this game, the shares rose 76% from 146p on the morning of the last set of results, peaking at 258p before these results:

Given that 20H1 was a period severely affected by the COVID-19 slowdown, for revenue to only be up 11%, and posting a loss, then these are simply poor. The only bright spot is that the cash burn seems to remain low:

This is likely to be bolstered soon by the sale of Xaar 3D, about which they say:

Negotiations to divest Xaar's interest in Xaar 3D are at an advanced stage, and although have taken longer than expected, we believe we are close to conclusion.

But it should be noted that this sale is coming from a position of weakness not strength:

The 3D business unit, with operations in Nottingham, UK, and Copenhagen, Denmark, has continued to experience some delays in the beta programme, testing and commercialisation of the 3D printers in the first half of 2021 as a result of COVID-19 restrictions.

It is these delays and the requirement to put more cash into the JV, which they are unwilling to do, which has led them to seek a sale to the JV partner. When they last divested some of this subsidiary, they put in place a call option for the JV partner to buy the rest for the maximum of $33m or 2 x Revenues. Since the revenue is small, and the JV partner isn’t just exercising their call option, then it is clear that the price they will receive will be lower than $33m. How low remains to be seen, but given the delays, I think something IRO £15m would be a reasonable expectation.

They acquired FFEI for £3.7m + £5.4m deferred consideration post-balance sheet date, so this would put their pro-forma cash balance at just less than £30m.

Despite the share price falling to the current 190p, this still has a market cap of c£150m. So, the ongoing business is being valued at £120m. Since they are loss-making, the outlook really matters:

Whilst the COVID-19 pandemic continues to cause business disruption, the Group is concentrated on securing continuity of supply of components to eliminate any interruption to the supply of printheads in 2022. The ongoing pandemic makes it difficult to provide reliable guidance on the outlook for the remainder of 2021 and beyond, however the short-term outlook remains positive with a healthy order book across the business. The success we have had in the first half of 2021, and the strength of the Group's balance sheet and cash position, means the business is well-positioned to withstand further volatility caused by the pandemic. We remain confident our full year 2021 results will be in line with expectations.

Those expectations are for a 3p EPS loss, so H2 should be better than H1 but still loss-making. 2022 estimates are for effectively break-even. So, despite the share price fall in response to these results, there seems to be a large amount of hope still built into the price. And buyers of hope in persistent under-performers rarely do well in the long term.

Staffline (STAF.L) - Half Year Results

Note that they disposed of their apprenticeships business, partly because the government keeps dicking about and partly because they could do without the distraction. Thus comparatives are restated. But clearly, there has been a significant turnaround in profitability.

The turnaround in profitability is mainly due to cost-cutting though, which while clearly welcome & necessary, is not as good as a rise due to improved topline performance or margin.

More importantly, there has been a big turnaround in their finances. Leo considers them to be now well-financed. Mark still has a few issues with the balance sheet:

a) the negative TBV despite an almost endless series of capital raises

b) payables, short-term borrowings and provisions exceed the cash + receivables.

I would expect the likes of Tesco are paying on 90-day terms and if you work for them in the Tesco warehouse you want paying monthly, if not weekly. So how can this be a negative working capital business? Likely only one way: VAT & payroll taxes timing arbitrage. This may cause them issues in a downturn, but in a growing market, they should be fine, aided by the big fundraises they’ve done over the last few years.

But, after the 37% EPS upgrade in late July and well-publicised very strong labour markets and ongoing momentum, clearly many market participants were looking for a stronger outlook statement:

· The Group continues to benefit from increased levels of client activity across the UK and Ireland. However, the Board remains mindful of the economic uncertainty and risks to the economy represented by the pandemic and sector-specific labour shortages

· The Group is trading in line with the revised, increased market expectations (further to the July trading update) for the full year 2021

· The Board remains confident in the Group's prospects after a period of transformation and restructuring to streamline operations in 2020, followed by the recent refinancing which materially strengthened the platform for future growth.

So, definitely no further upgrade, and a very uncertain outlook. They also comment:

Looking ahead, whilst we expect to see continued sector-specific labour shortages, we believe Staffline is well placed to capitalise on its position as the clear leader in many markets. In addition, our recent refinancing has transformed the Company's balance sheet providing a strong platform for growth in the medium term. The Group is trading in line with the revised, increased market expectations for the full year 2021.

This market positioning is why Leo is so keen on the company. They are the go-to company to fill labour gaps in many blue-collar industries.

So, on to the brokers note from Liberum, who say

In line results and demand is strong

No change to forecasts. A dip in EPS is still forecast for FY 2022 before growth resumes. That will be due to an increased share count. Prior to the June fundraise, their financing was unsustainable but cheap. 18% EPS growth 22 to 23. So a PEG of 1 => P/E ratio of 18. So, a 95p valuation.

Liberum have a target price of 100p, which we doubt is a coincidence.

Our TP of 100p represents an FY 23 P/E of 18x, which is attractive given the recovery potential and positive momentum.

But then a 23% return in two years if everything goes to plan probably isn’t what most small cap investors consider an acceptable risk-reward.

Portmerion (PMP.L) - Interim Results

This sounds great:

Portmeirion experienced excellent trading in the first half with year-on-year sales growth of 35%. Furthermore, the business has not only recovered to its pre-pandemic levels but is now exceeding them with sales up 24% compared to two years ago in H1 2019.

However:

Like-for-like sales in constant currency up 7% against 2019 ("YO2Y"), ahead of pre Covid-19 levels despite ongoing disruptions, showing the strength of consumer demand and progress with our online strategy.

7% over two years is about inflation? Maybe less? Furthermore, the Nambe acquisition seems to be very H1 weighted. Again, we already knew these figures. So what about the outlook?

We are delighted with our excellent results in the first half of the financial year. Since the period end trading has continued that trend into the first two months of the second half. Looking forward we have a strong order book across our key markets for the rest of the year. We are cognisant of the ongoing, widely reported disruption and volatility in global supply chains, including labour shortages, container shipping delays and significant market price rises in container shipping rates all of which impact our business. We have taken and will continue to take mitigating action where possible, expediting stock shipments, building additional raw material and finished goods stock contingency, reviewing our own selling prices and continuing to offer added protection and flexibility to our staff to protect them from Covid-19 and related absence.

We remain confident of achieving market expectations1, and the accelerated strategic investments we are making across our business will enable a strong path of growth in the next few years.

1 Current consensus market expectations for 2021 are revenue of £90 million and profit before tax of £6.4 million, and for 2022 are revenue of £99.5 million and profit before tax of £10.0 million.

So, again, no upgrade. However, Leo has modelled this and, despite the caveats above, £90m looks significantly too low. It perhaps should be £103m on conservative assumptions. That's the good news.

The bad news is that the level of cash costs and margin is disappointing. Brokers are forecasting dramatic improvements in margin going forward, but we can’t see this from the H1 figures. Leo’s modelled EPS actually comes in below broker forecasts.

But, they are on the right side of fashion trends. And the Korean issue seems to be resolved:

Strong growth (57% against 2020, 4% YO2Y) in key South Korean market following successful period of management action and focus on stabilisation of stock levels. Growth expected to continue in H2.

Forecast EPS for 2021 onwards is 37p, 57p, 67p. If you believe that margins will improve and meet these forecasts then they look reasonable but not outstanding value. And also, if broker margin assumptions are right, and Leo is right about revenue (which is easier to forecast), then there's a significant beat on the way for FY 2021.

Apparently, the market wasn't expecting a forecast upgrade before these H1 results, but now is:

Character Group (CCT.L) - Trading Statement

One of the biggest fallers this week is Character Group, in response to a trading statement. With this bit doing the damage:

Consequently, there has been limited downside and we expect the Group's underlying profit before tax for the year ended 31 August 2021 to decrease by no more than 10% of market expectations*.

Helpfully, they give the expectations:

*Current market consensus compiled by the Company for the year ended 31 August 2021, prior to the release of this announcement, is revenue of c.£140m and underlying profit before tax of c.£12.0m

So new expectations should be for PBT of £10.8m. The reasons for the miss are, perhaps, as we would expect:

…several factors that we identified at the time of our interim results announcement in April 2021, which have since deteriorated further. Like many companies, the global logistical challenges (such as the ongoing delays at ports, shipping and container shortages, exponential increases in freight rates, and increased costs of inland transportation in China and the UK), coupled with the pressure on the costs of production in China due to higher raw material and labour costs, has had an impact on profitability.

With no clear resolution in sight:

The immediate outlook for an early improvement in supply chain efficiency to ensure timely fulfilment is currently unclear.

Today’s c.20% fall takes the shine off but the price remains above the level before the release of the good H1 results, when they said:

Building further on the substantial increase in Group sales in the first half, we have continued to see a strong performance in sales of our product portfolio in all our territories from the commencement of the second half of the year. This growth is forecast to continue through to and beyond Christmas 2021 and we are on target to deliver the best sales performance in any calendar year in the Group's history. Accordingly, we expect the 2021 full financial year's underlying profit before tax will be materially ahead of the published market consensus of £10.5m.

So it appears this materially ahead statement didn’t actually materialise and we are back where we started. Christmas is always the strongest period for Character, so even with these issues, H2 should deliver £4.7m PBT. Last year they did £2.5m in the same period, although it was £5.5m in 19H2 when the share price was at similar levels.

Forecasts were for 44.1p so assuming a 10% reduction this would be 39.7p.

They do have significant cash balances of about 20% of their market cap and intend to do a tender offer to reduce the share count:

Prior to the date of this announcement, the Company has not effected any share buybacks pursuant to the Authority and currently has a capacity under the Authority to buyback up to 3,200,000 issued Ordinary Shares (constituting approximately 15% of the current, issued, voting share capital of the Company).

Assuming they do reduce the share count by 15% then this is a pro-forma market cap of £102m, given a P/E of around 11.7. Not crazy in the current market, but there are reasons we are not rushing to buy:

1. They have rarely traded above a P/E of 10 in the past. Investors tend to look at this as a low-quality business given that they licence rather than own the vast majority of their most popular brands. Plus, the management rewards themselves very handsomely.

2. Given that estimates have gone up and back down again, there is a lot of uncertainty and hence you would expect them to trade below where they started the year at c.420p.

3. The issues don’t seem to be easily resolvable so there is a high risk that the key Christmas trading period will be affected and 2022 EPS is much below that of 2021.

In light of these, the risk still looks to the downside.

Tandem (TND.L) - Half Year Results

The theme of supply disruption will be one that runs for the rest of the year, at least. But some companies seem to be navigating this better than others. Such as Tandem, who released their HY results to 30th June this week. On the topic-du-jour they say:

The challenges previously reported have continued over the last two months since our AGM update. Global demand remains high with shipping containers still in short supply. Input costs, having risen significantly during the year to date, have yet to return to more reasonable levels.

We continue to manage these challenges well, where necessary deferring shipments and seeking alternative shipping routes to minimise cost whilst seeking to maintain timely supply of product.

Generally, they are trading well -

- Revenue increased approximately 14% to £ 19,262,000 (2020 - £16,927,000)

- Gross profit increased to £ 6,066,000 (2020 - £5,556,000)

- Increase in operating profit to £2,003,000 (2020 - £1,478,000)

- Profit before tax after non-underlying items was £1,907,000 (2020 - £1,409,000)

- Net profit for the period was £1,602,000 (2020 - £1,141,000)

- Earnings per share 31.2p (2020 - 22.7p)

- Net assets increased to £ 18,568,000 (2020 - £15,266,000)

- Cash and cash equivalents as at 30 June 2021 of £5,850,000 (2020 - £6,322,000)

But historically, there has been no forecasts in the market....until now...enter Cenkos initiation note.

These seem quite optimistic, but you must think that the company have been guiding these figures. And the narrative in the results reads well. Despite the price now above £6 again, these figures imply a forward earnings yield of c.13% making them much cheaper than everything else we've discussed.

The risk, of course, is that supply chain issues get worse and affect the key Christmas selling period.

The only issue in the note that I spot is that the strong earnings are not appearing in the FCF:

Partly due to WC but partly due to high ongoing capex:

Working capital

We assume a working capital cash outflow of -£1.5m in FY21E, resulting from the expected ramp up in sales this year, followed by a -£1.0m outflow in FY22E.

Capex

Capex is forecast to jump significantly in FY21E (we forecast £3.4m) due to the cost of purchasing the freehold land in Birmingham and remain high in FY22E (£3.6m) as the warehouse is constructed and fitted out.

And the revenue growth isn't in the forecasts for FY22, so you could argue that this is an issue, or that as investors are expecting with Staffline or Portmerion, this is a beat that is on its way.

So, despite the risk that these forecast are overly bullish, there is potentially additional upside for 2022. It is an illiquid stock though, and I can't help feeling that there is a supply chain worry on the way at some point even if it just affects sentiment rather than the reality for Tandem.

Zytronic (ZYT.L) - Trading Statement

This trading statement caused a 20% share price rise:

We are pleased to report the continuation of an improvement in sales during the second half, currently running at more than 30% ahead of the first half, which has enabled a faster return to profitability and reversal of the first half loss.

It shows how poor expectations here were, since the 30% improvement is actually slightly behind what I was forecasting. But it seems the market was pricing as if this would never recover, which doesn't seem to be the case, hence the rise. As house broker N+1 Singer say:

We upgrade our forecasts accordingly in this note and will review forecasts in more detail in due course. Over the medium term, the recovery opportunity looks very attractive, given that Group PBT in the last full year pre-pandemic was >£3m.

I don't see why they won't be back to £3-4m FCF per annum in time and a £3-4 share price. Obviously, the faster they get back to such levels the better the returns, but there is still a potential valuation gap between what the market is pricing and what the eventual outcome will likely be.

Small Caps Live Friday 17th September

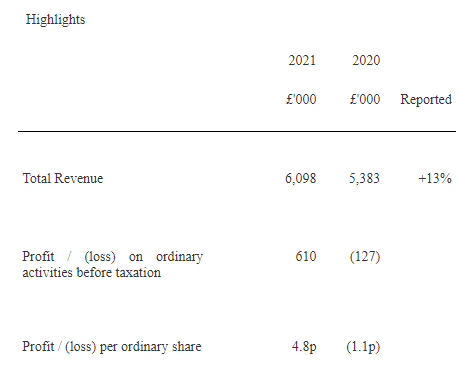

Fiske (FKE.L) - Final Results

Mark thought it was worth taking a look at this microcap fund manager that reported earlier in the week, partly because we’ve never looked at it before and partly because there was little that interested him in the second part of the week.

Not the most expansive of summaries there, but a welcome return to profitability.

They seem to be growing, but from a small base:

After the Covid-19 lock-down induced fall in market values in March 2020, a hesitant recovery promptly began but only really took hold in October 2020. Overall, portfolio values took until the latter part of our trading year to recover past their late 2019 values which was an impediment to our management fee income. Nevertheless, both commissions on trading and management fees each increased, even after a strong performance last year. We continue to attract new clients and to migrate clients from advisory to discretionary services.

The actual AUM is just £63m:

At 31 May 2021 amounts held by the Company on behalf of clients in accordance with the Client Money Rules of the Financial Conduct Authority amounted to £63,153,533 (2020: £56,624,640). The Company has no beneficial interest in these amounts and accordingly they are not included in the consolidated statement of financial position.

Given the fee income is almost 10% of AUM then they presumably charge quite a high admin fee, performance fee, or both.

Almost all of the profit was made in H2:

After reporting a pre-tax loss of £27,000 in the first half-year, we have made a profit of £637,000 in the second half which has resulted in a full year pre-tax profit of £610,000 (2020: loss £127,000). The second half of the year benefitted from increased commission revenues and increases in management fees as markets rose.

And looks like the run rate is similar but not quite that at the moment:

We have had a good start to our new financial year. Whilst the first few months have seen trading volumes soften a little, in line with more traditional summer levels, portfolio values are rising with markets which will enhance our fee revenues.

So that 4.8p EPS could easily be 8-10p going forward. On top of that, you have £3.6m of Euroclear shares and £3.5m cash (not all of which is free cash since there will be reg cap requirements. A £10.6m market cap perhaps then belies quite a lot of value.

The problem is that although they have been growing the top line, profitability and FCF has been patchy:

From this, you would conclude that they are highly geared to market conditions. Which makes sense considering the high fee income as a percentage of AUM.

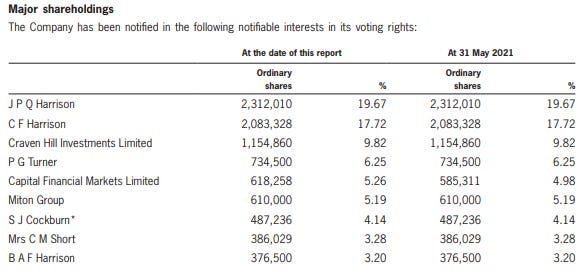

They are tightly held, too:

And haven't paid a dividend since 2015. So an investment in Fiske is very much hitching your ride to the Harrison family. I think if they paid out a large amount of their profits as dividends then I'd be tempted here, but given the illiquidity, only very slight growth and lack of communication then I just don't see the catalyst for a significant re-rating.

CMC Markets (CMCX.L) - Client Base Transition

We didn't see it flagged up anywhere in advance, so this came as a bit of a surprise:

CMC Markets Plc ("CMC" or the "Group"), a leading global provider of online trading and institutional ("B2B") platform solutions, today announces the transition of Australia and New Zealand Banking Group Limited's ("ANZ") Share Investing client base to CMC for a sum of AUD$25m (the "Transaction").

With this Transaction, the existing white label technology partnership, which has seen CMC's trading technology power ANZ's share investing business since 2018, will come to an end.

This doesn't seem the best news. With the current arrangement ANZ do all the marketing and CMCX just take the money, and presumably benefit from trading flows. It had been growing consistently each year. What will happen now is uncertain. Plus they've paid AUD$25m (whatever that is) for revenues they mostly already had.

However, this is likely to be good medium-term news. Firstly, although they already had the revenues, it would be far too big a stretch to say they had the AUM, and as I said above, on that basis this is very cheap. I believe these are "traditional" stockbroking accounts rather than spread betting where there has been a regulatory change in Australia and where AUM is much less meaningful.

But the main reason is that CMCX is more agile than ANZ and having established a good base of customers should be able to provide more services and continue to grow customer without ANZ:

The CMC platform will offer clients a wide range of additional benefits currently unavailable with ANZ. These include access to enhanced, market-leading mobile apps and complementary education tools and resources. Following transition, ANZ Share Investing clients will benefit from lower brokerage charges across four major international markets and the local Australian market and will give CMC the opportunity to drive greater value from its enlarged client base.

However, when they talk about "The CMC platform", they are unfortunately not talking about something that already exists for stockbroking as opposed to spread betting. This is the platform they are currently developing to break through into stockbroking in the UK and elsewhere. Thus:

The Transaction is expected to take 12 to 18 months to fully transition clients.

Or perhaps the delay is due to regulatory issues or slowness with ANZ. But either way, that appears to mean growth in this business will stall during the transition. So, overall I think this is good news, but it still leaves the question why this wasn't flagged up before and why ANZ are selling.

Games Workshop (GAW.L) - Trading Update

This is not, of course, a small cap anymore, but we cover it since it has a large following in the private investor community. They issued their September trading update yesterday:

Games Workshop Group PLC announces today that trading for the three months to 29 August 2021 was in line with the Board's expectations. Sales continue to grow but, as with other businesses, we have seen pressure on freight costs and currency exchange rates.

And that's about it. That doesn’t seem the strongest update. There is a real risk here that the same thing is happening here as has happened with Best of the Best and CMC Markets: conservative management consistently behind the curve in guidance on the way up means that when trading turns there is still plenty of contingency left in forecasts, allowing them to restate that trading is inline. Even when trading turns down further, management doesn’t want to believe it and want to keep their reputations for hitting or beating forecasts so they say little. When the reduced guidance comes in, it is brutal. As is the share price reaction. It turns out their conservatism is more about being slow to adjusting forecasts to changing reality, both on the way up and on the way down.

However, there were clear hints in both BOTB and CMCX’s earlier statements. Is there any hint in the above? Different companies communicate in different ways. Compare with last year’s equivalent update:

Current estimates show sales of c. £90 million in the Period against a prior year of £78 million for the same period. Operating profit for the Period before royalty income is estimated to be c. £45 million (2019: £28 million) and royalty income is estimated to be c. £3 million (2019: £2 million).

Much more specific. But in September 2019:

Games Workshop Group PLC announces today that trading is in line with the Board's expectations. Cash generation also remains strong.

Many companies disclosed additional details in 2020 due to coronavirus so I see nothing concerning about them failing to repeat this. Yesterday's statement is basically the same as 2019, but without the statement on cash, of which more later. Games Workshop issues trading statements multiple times a year, so is there a hint of this in the other ones? Let’s start with a year ago.

September 2020:

The Board recognises that this performance is better than the prior year but is also aware that it is still early in the financial year. A further update will be given as appropriate.

November 2020:

The Group announces today that trading since the last update in September 2020 is ahead of the Board's expectations. Given this, the Board's estimate of the results for the six months to 29 November 2020 is profit before tax of not less than £80 million (2019: £58.6 million)

Result: Significant broker upgrades.

December 2020:

Following the update in early November 2020, the Company announces that our preliminary estimates for the six months to 29 November 2020 indicate sales of c. £185 million (2019: £148 million) and profit before tax of not less than £90 million (2019: £59 million).

Result: Significant broker upgrades.

January 2021:

Like every other company we have our internal plans as to our future performance, which show a range of outcomes which are not shared with the stock market: predicting the future is always a risky business. To help inform shareholders and followers of Games Workshop as best we can we will continue to provide regular updates of our trading in each current year (much as we do already).

Result: Minor upgrade from what looks like one broker.

March 2021:

The Company also announces that trading in the three months to the end of February 2021 has been in line with expectations, notwithstanding t he majority of our UK and European retail stores were subject to Covid-19 closures and distribution disruption during the period.

May 2021:

For the year to 30 May 2021, we estimate the Group's sales to be not less than £350 million (2019/20: £270 million) and the Group's profit before tax to be not less than £150 million (2019/20: £89 million). This includes royalties receivable from licensing which are estimated to be approximately £15 million (2019/20: £17 million).

Result: Broker consensus downgrade for FY 2023, minor cut for 2022.

September 2021:

Games Workshop Group PLC announces today that trading for the three months to 29 August 2021 was in line with the Board's expectations. Sales continue to grow but, as with other businesses, we have seen pressure on freight costs and currency exchange rates.

Result: Significant downgrade for FY 2024 already visible on Koyfin.

However, nothing is shown for FY 2022 or 2023. Edison say:

Revenue growth against a tough comparative…Our forecasts for FY22 and FY23 are unchanged.

(They don't forecast 2024)

However, it looks like Jeffries downgraded:

Andrew Wade, an analyst with Jefferies, said the language of the statement suggested there had been an impact on margins, which would potentially lead to a small downgrade in consensus profit expectations.

So, while there's nothing really in yesterday's statement to worry about, the last upgrade that stuck was now in February. There does seem to be a loss of momentum here. The other thing that may be losing momentum is the dividend payout

Although dividend growth investing is a poor strategy overall, it doesn't mean that dividends don't contain a lot of information. When a cautious management team gives a big dividend increase, it often gives more information than their commentary.

In this case, the reverse seems to be in play. Games Workshop has declared a 25p dividend vs 50p at the same time in 2020 and 35p in 2019. But they do pay dividends multiple times a year, which muddies the picture.

From that Times article:

House broker Peel Hunt said the firm’s margins this year would be lower because of reinvestment in the business

So, lower dividend + lack of statement on strong cashflow + reinvestment in the business. That does seem to be telling a story about cash, at least. The Forward PE is 30, the share price has gone nowhere this calendar year (well, down and then up again), growth or at least outperformance seems to have stalled. Looking at the history of trading statements above, I think November is the one to really look out for.

It is probably too uncertain to make any real predictions since three months in is a bit early, but if they don't upgrade in November then it starts becoming likely they won't ever do, and a lot of people value it on the basis they always beat forecasts. Giving potential downside? After all, buying any large cap on greater than 10x sales tends to be a high-risk investment.

That’s it for this week, have a great weekend.