Small Caps Live Weekly Summary

BARC SCS JHD QRT CAPD GDP

Although Mark is back from Honeymoon it was still a disjointed week this week, not that that seemed to matter with only a few bits of news. In addition, most small cap moves in this period appear to be almost completely random. Tipsters seem to have more of an effect at the moment. As Leo commented on the General channel this week:

It is easy to forget how illiquid some of these companies are. It is worth having alerts on and important not be find yourself a forced seller.

Perhaps one of the advantages of acting countercyclically - if you are following the markets when no one else is, you often get a bargain.

Large Caps Live Monday 2nd August

Barclays (BARC.L) - HY Report

In the results, Barclays reversed £0.7bn (ie £700M) of impairments driven by ‘improved macroeconomic outlook’. And they still hold an impairment allowance of £7.2bn. This confirms my suspicion that banks overprovisioned due to Covid. I also think that the government schemes to support companies and employees (ie the furlough schemes) in both the UK and the US, plus the jump in house prices has helped a lot of bank balance sheets.

In H1 the group PBT was £5bn and the eps was 22.2p. Now before we go on I want to emphasise that that was the eps for H1. (For reference in H1 2021 the eps was 4.0p) Now let’s have a brief look at Stockopedia estimates for eps:

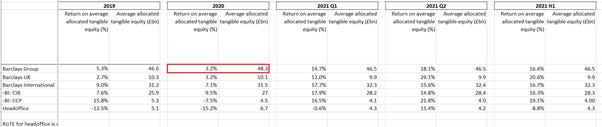

I could clearly discuss H1 vs H2 split of eps etc but whichever way you run it, it is pretty clear that the 2021 eps estimate looks low. (Remember that in 2020 they did 4p in H1 and so about 21p in H2; this year they have already done 22.2p in H1). Obviously, with banks ‘normalised’ and reported can be quite complex. However whichever way you look at it (and you can argue it was due to one-offs due to reversal of provisions etc) but the jump in eps is positive. This is my tracker of ROTE by division for Barclays:

The key thing to note in these numbers is that in Q2 2021 every unit was delivering over 10% ROTE. And the UK business was hitting 29.1% (note that the ROTEs are annualised numbers based on the quarterly result x 4) was at 29%.

The other area that I really watch is the CCP (consumer, cards and payments) which hit 21.8%. I really like the CCP business as it has a degree of differentiation vs a run of the mill bank, and potentially is a high ROTE business. Indeed, I could go all 'investment banker mode' and argue that the CCP business is probably a 20x P/E or 2 x P/TB business in its own right.

For the ROTEs in the above table, the quarterly returns are taken and multiplied by 4. The main point is that the group has gone from earning 3 – 5% ROTE to double-digit. I appreciate that this could be a one-off and it could revert to single-digit ROTE. However, I think the pressure that the management has been under and the ending of PPI etc should give some improvement.

Given that the group is on about half P/TB (ok 51% but half makes the maths easier) it means that 15% ROTE over the year (say) means as an investor I am getting 30% return on my investment which frankly is modestly satisfactory.-

Barclays is trying to also show that it is a fast-growing ‘fintech’ / ‘payments’ company. Personally, I think what is more relevant is the credit card business ie both the consumer credit cards (Barclaycard) and the merchant acquirer business. I have always been unconvinced that we know the full profitability of the credit card business due to the spread of it between the UK and the international division.

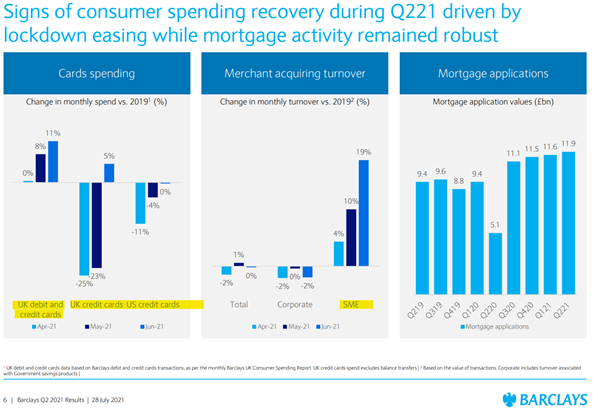

Part of my hypothesis on Barclays is that as Covid restrictions drop away we will see a rebound in consumer spending – often by credit card. Also currently consumer balances (/unsecured overdrafts) are low but that as we normalise the credit card companies will benefit. I think we can see some sign of that in slide 6:

The key way a bank like Barclays makes money on credit cards is due to net receivables – as many people fail to pay off the entire credit card amount at the end of the month. So, net receivables are an important number to track. We can see what is happening to them from slide 14 – the relevant part is here:

What is really interesting about this slide, in my view, is how US net receivables increased in Q2 over Q1 2021l whilst UK fell (a little). Here are HSBC numbers from today’s results on the same topic:

I think the key point in that HSBC slide is the 61% increase in card spend in 2Q21 vs 2Q20.

The other key points to highlight are the CIB (commercial/investment banking) returns – that is definitely a volatile area. But looking at Barclays I think the following slide is interesting:

Firstly this slide shows that only 1/3 or so of Barclay’s income is due to net interest income (ie ‘spread business’) whilst 2/3 is fees/commissions and other income. Secondly that 58% is ‘wholesale business. And thirdly that just under half is non-UK – all of these are interesting characteristics.

To get an idea of how significantly skewed Barclays is to fees/commissions and other income we can compare with slide 21 of HSBC results from today - you can see that for HSBC over half its income (remember for a bank 'income' means revenue) is from NII (=net interest income):

The area that usually excites UK investors is shareholder returns – both dividends and share buybacks. In the case of Barclays, they completed a £700M buyback in April. They will now be paying a 2p dividend (17th Sep 2021) and intend to do a further £500M buyback. Currently, Barclays has a market cap of £29.95bn so we will basically see 4% of the company having been bought back this year (1.2 / 30). In addition, we have a rolling dividend forecast (Stockopedia) of 3.93%. So total return this year if the shareprice stays the same is about 8%.

So if we put all that together we have:

1. A bank on 51% of price to tangible book;

2. Generating double-digit returns on tangible equity (over 15% in the last two quarters);

3. So for a new shareholder the effective internal return by the bank on the shareholder's investment is 30%.;

4. And a dividend of 4%

5. Plus a share buyback of 4% - but crucially this is at a 50% discount to tangible book value so is accretive to shareholders.

Small Caps Live

SCS (SCS.L) - Trading Update

Before looking into the details it is worth reiterating what they said in June:

As at 12 June 2021, the Group's order book was £116.6m (including VAT), £39.0m larger than at the same point in the prior year.

The Group has maintained a robust balance sheet, with cash at 12 June 2021 of £101.3m and no debt. Further liquidity is available through the three year £20.0m CLBILS revolving credit facility (RCF) granted on 25 August 2020.

The Board is encouraged by the Group's strong trading performance since reopening. Whilst some uncertainty persists relating to the end to all Covid restrictions, the Board believes the Group is well positioned to maximise opportunities for growth. The Group has a robust balance sheet and the re-introduction of dividends today reflects the Board's confidence in the business going forward. As such, and given the strength of the current order book, the Board's outlook for FY22 is substantially better than current market forecasts.

So, looking at how much order book has converted, whether people have kept ordering despite delays, a use for that grossly excessive liquidity and an improvement in outlook due to the reduced likelihood of further restrictions. So, since the last update, order intake is up 23% LFL. That's good. But not as strong as the 79% reported for the period up to the last trading update.

At 31 July 2021, the Group's order book was £103.5m (including VAT)

So that's down from the June update, meaning they have been catching up on deliveries rather than getting behind. Apparently, UK manufacturing of fabric sofas and Far-Eastern imports of leather have not been too badly affected by well-known issues.

The Group's financial position remains robust, with cash at 31 July 2021 of £87.7m and no debt.

A 3p/share dividend was paid on 24th July. That's just £1.1m, so the drop in SCS cash is likely to be mainly due to order book dropping by £13m due to order catch up.

Outlook:

The Board is encouraged by the strong trading performance since reopening and therefore believes that the Group is in a strong position as we enter the new financial year. The next few months still hold a level of uncertainty, with the tone of government messaging at present being one of caution.

The second paragraph seems unduly cautious to me. Everything seems certain to be full-steam ahead throughout the peak of people buying ready for delivery at Christmas. What is pointedly missing here is any mention of any issues with manufacturing or shipping. This is the next best thing to them saying there is no problem.

We were very optimistic here and was never likely to have been surprised on the upside, but this is useful:

However, given recent trading and the strength of the current order book, the Board's expectations for FY21 and FY22 are ahead of current market forecasts.

One thing to highlight is that prices soft furnishings were strong in the last inflation figures:

The contribution from furniture, household equipment and maintenance has risen from a downward pull of 0.03 percentage points in December 2020 to an upward push of 0.17 percentage points in June 2021. This reflects a 12-month rate of 3.3% in June, the highest since February 2018. The contributions from all groups within this division have increased since the end of 2020, with the largest change coming from furniture and furnishings.

So it seems that the industry have been able to pass on any price increases.

Brokers: Previous consensus was £318m revenue / 27p EPS for 2021. Revenue was forecast to progressively increase from there, but an EPS set-back was forecast for FY 2022. Given they made 37.5p EPS in H1 these don't seem especially credible.

The last full brokers note we can read is from Shore on 16th March after the H1 results. At that time, they forecast 23.5p EPS and net cash of £43.2m. So that cash beat is over £1 a share.

Followers of the company will be aware that while they cite closing order book levels, they do not give absolute order intake values, only LFL percentage changes. Except, that is, in this update at the beginning of the coronavirus epidemic.

So Shore has upgraded to 32.2p EPS and £323m "revenue" for FY 2021. Either way, this is a significant upgrade, but not as good as the 40p we thought may be possible. For FY 2022 the upgrade is from 26.3p in July to 30.8p now.

"Shareholders cash" ie. net of provisions and -ve working capital was just shy of £40m or 98p per share at last balance sheet date of 23/1/2021 which makes the valuation look even better.

There are also a few complications around the modelling. Firstly, when Shore says “Revenue”, they mean what ScS calls “Gross Sales”, whereas what Scs calls “Revenue” excludes the cost of providing interest-free credit.

Secondly, there are a lot of costs that can be expected to vary directly with sales that are taken as admin expenses, particularly distribution and sales commissions. Furthermore, sales are very much driven by what they describe as “call to action” sales campaigns, mostly in TV and newspapers. Although of course there is some brand recognition and passing trade, without advertising sales would drop off much faster than other companies. Therefore the gross margins of over 40% are rather misleading and 25% is probably closer to the economic truth.

So anyway, Leo had £333m Gross Sales vs £324m likely outcome and that immediately takes H2 EPS down from 7p to breakeven. H2 was affected by the repayment of furlough, a decision made after the H1 accounts were published.

Shore last published their model on 29/9/2020 when, coincidentally, their forecast Gross Sales were the same as they are now. They assumed a lower gross profit margin than me, but a normalisation of distribution costs that perhaps now look rather optimistic, and business rates relief lower than we now know it to be. Adjusting for the business rates relief gives FY EPS of 29.6p.

So, fundamentally, we were a little optimistic on how much order book would convert to sales and our gross margin estimate was about as over-optimistic as Shores was under- optimistic. In summary, Shore's estimate gone from 23.5p to 32.2p EPS in little over a month and we've gone from 40p to 32.2p in about two. So forecasts are very sensitive to assumptions right now. Although, either way, a cash-adjusted P/E of c.7 still looks good value.

James Halstead (JHD.L) - Trading Update

Early indications in February that international freight was showing signs of improving, in terms of cost and availability, was short lived and the chaos of the closure of the Suez canal has been matched by the turmoil in China and in particular the port of Yantain which handles vast amounts of international freight. Consequently, there have been delays in the supply of goods and ongoing adverse shipping costs.

In the UK, the availability of basic raw materials has continued to threaten smooth production but more disruptive has been the effect of employee shortages due to absenteeism mostly a result of the self-isolation of employees exposed to the virus. The Radcliffe production site has consequently struggled to achieve full output for many months. Teesside production has fared much better and third-party sourced finished goods have performed admirably.

Lots to unpack there. We expected higher shipping costs to be ongoing. Hopes they might abate about now are surely slipping away. Employee shortages were less clear. We know it is a problem in refrigerated facilities and now more widely due to people being exposed outside work. However, the variation between sites is interesting. Radcliffe probably refers to Bury, Manchester. Resilience from third-party suppliers is reassuring for the likes of ScS. But despite this, Halstead are doing well:

the Company expects to report both turnover and pre-tax profit at record levels for the period.

A lot of this seems to be about executing better than the competition at a difficult time:

the entire market has faced production issues and several of our competitors have had to suspend production due to material shortages. To date, we have not curtailed output and we believe this has helped us gain market share.

Investors might think Halstead, as primarily commercial flooring, would be especially hit by a lack of office/hospitality use, but there's been an unexpected (and I would say, unforeseeable) effect:

In addition, it seems clear to us that while flooring retailers were closed, due to lockdown restrictions, our commercial flooring offerings (particularly in luxury vinyl tile) were used increasingly and significantly in domestic settings.

Where contractors are used and domestic customers can't get into the shop to chose, then they make suggestions. Also with the move to home/garden offices and home gyms

WH Ireland only upgrades EPS by 2.2%, and only in the current year. Therefore the Stockopedia data showing a forward P/E is still current. A PE of 30 seems too high given the forecast pedestrian growth, despite them having proven themselves well through the crisis and being larger than many companies we cover here.

Quarto (QRT.L) - Interim Results

Quarto, the book publisher, produced interim results this week. This has been a tough sector and the balance sheet here looked far too weak for a long time, however, a board room bust up led to CK Lau taking the helm and a placing underwritten by him rebuilding the balance sheet. The H1 results to 30th June look much better too:

$2.1m PAT for the weaker 6 months (illustrated book sales tend to be Christmas items) vs a £32m market cap makes this look reasonable value. [Although on first reading I thought this looked much better value, since the googlefinance function in google sheets was returning the wrong share count - shows the value of double-checking with original sources!]

There are no forecasts on stockopedia, but a very naive extrapolation would imply that the P/E here would be below 10. P/E isn't the best metric to use when a company has large debts, or pension deficits though. Quarto has $16.4m of net debt, but having reduced significantly via operating cashflow and the placing this looks under control. And in the current market, these things largely get ignored. See Mpac or Reach for examples where a pension deficit, despite costing large cash payments is ignored by investors in their valuations because it is now viewed as under control.

Quarto's debt has always been very visible, but it has also always had prodigious operating cashflow. One of the historical issues though has been that it has tended to end up invested back into pre-production costs, and from what I had heard, cost control was rarely top of their to do list. So it is pleasing to see some cost control here and them spending less than they are amortising. Obviously, this doesn’t work if they are simply eating their own tail, but these results show little sign of that issue.

However, not everything is rosy:

We are now focused on the critical second half as we expect the trading environment to be particularly challenging, especially with the volatility in freight, regarding capacity issues and freight costs. That said, we have the right plans in place to capture all possible opportunities and ensure a satisfactory year-end.

The Board remains focused on continuing its efforts to keep costs under control, drive sales, whilst maintaining the debt reduction and defining further growth strategies for 2022 and beyond.

If the outlook was stronger here, I would be tempted to invest in Quarto, but the freight issues they are facing, due to printing large books in the Far East, give me pause for thought. Like Tandem, which we’ve looked at in the past, without a lot of pricing power, Quarto are disproportionally affected by these sort of freight issues. If we see freight costs start to normalise though, these could look good value.

Capital Limited (CAPD.L) - Customer Newsflow

While there has been no direct news, given out previous coverage here, it is worth going over some of the recent customer newsflow.

The following announcement from Cora Gold caused a 33% rise in their share price this week:

49m @ 15.55g/t Au and 32m @ 7.83g/t Au in first Selin P2 drill results

The grades reported over these sort of strikes likely make this a very economic resource. Capital Ltd. undertook most of this drilling:

● 277 holes drilled totalling over 30,923m from the start of the campaign to 31 July 2021.

● The Capital Drilling Deep RC rig has been moved, following completion of the P2 deeper holes at Selin, to target follow-up on the high-grade intercepts reported at Zones A, B1 and C, and as part of the completion of the P2 resource consolidation process.

● The GEODRILL KL600 RC rig will complete the southward progression of the Selin P2 shallow resource consolidation drilling.

● The Capital Diamond Drill ('DD') rig has moved south to complete geotech-metallurgical programmes at Zones A, B and C prospects.

It is unclear if Capital still hold their Cora equity stake since they went below the notifiable threshold last year, and the absolute amount is less than £1m so not particularly material to Capital anyway. What seems certain is that the success here is likely to lead to much more work for Capital in the future.

Centamin produced financial results yesterday, and, as usual, were highly complementary of Capital’s performance as an earthmoving contractor:

A total 2Mt was contributed by Capital Ltd, our waste contract-miner, who also outperformed their budget having mobilised equipment and personnel significantly ahead of schedule and delivering productivity ahead of schedule.

So we knew they performed well, but good to have them continue to be praised by their customer.

Hummingbird Resources also released drilling results. While not as impressive as Cora, these have the advantage of being an extension to a producing mine:

The drill programme has been a success and has showed that mineralisation continues to plunge to the north and is open down dip from these current holes. Drill planning has already commenced for 2022 which will be designed to test for further extension to the high-grade zones below the current level of drilling with a view to add further mineral resources that can be exploited by the future underground operation.

So good results leading to a 2022 drilling campaign - Capital do the delineation drilling at Yanfolila (but perhaps not production drilling IIRC) so this is a good campaign/future revenue visibility for them.

Finally, it is worth noting the continued strength of Predictive Discovery on the back of their recent drilling results:

The Capital 11% stake in PDI hit $20m in value at the peak. So about 10% of the market cap of Capital on its own. Capital, of course, bought in the placing at AUD8c and AUD7.5c in the market in July. Looks like they are better investors than me!

Goldplat (GDP.L) - Quarterly Update

Goldplat’s quarterly ops also include some key operating financials:

The recovery operations achieved a combined operating profit for the twelve months ended 30 June 2021 of £5,300,000 (30 June 2020: £6,350,000) and a combined operating profit in the 4th Quarter of the financial year of £1,080,000 (4th Quarter - 2020: £2,546,000).

The 4th Quarter was a little disappointing there compared to the previous year, not helped by the last Q4 being exceptionally strong for gold prices in the wake of the pandemic. The drop is really only in South Africa, though:

The Ghana operations continue to perform well as a result of steady supply of material and achieved an operating profit for the 4th Quarter of £729,000 (4th Quarter - 2020: £366,000 ). The South African operation achieved an operating profit for the 4th Quarter of £350,000 (4th Quarter - 2020: £2,180,000).

A lot of this seems to be timing, with £700k higher produced gold on hand at the year-end than last year. With the costs of production already incurred, then the operating profit would be c£1m which is a fairly normal level for this operation.

Although, water and electricity are the usual challenges that comes with operating in South Africa:

Operating profitability, year on year, continue to be impacted by higher electricity prices and increased water usage from the local municipality due to poor water quality from one of the Group's other water sources.

Putting this together with taxes, minority interests and finance costs, then they should have delivered c1.5p EPS for FY21, giving a P/E of c.5. This remains cheap, particularly given that a third of the current market cap is covered by cash & soon to be issued shares in Papillion (which now holds their former Kenyan mine.) Perhaps even eclipsing SCS for the crown of cheapness, although with a much higher risk profile.

Going forward that net cash will be reduced by the £3.35m net that they are paying to increase their stake in the South African operations to above 90%. [We commented recently that the read-through valuation of this transaction placed a valuation for the South African operations alone that is 50% above the current market cap.]

For 2022, if we assume a fairly conservative quarterly operating profit of £1m for SA and £600k for Ghana, then I get an EPS forecast of c2.2p for a forward P/E of 3.7 and a small net cash position. In addition, there is the $1.5m stake in Papillion.

As we commented on that other cheap South African miner, Sylvania Platinum all this cash flow doesn’t matter if it is never returned to shareholders. In a previous announcement, the Goldplat management has been explicit about their desire to restart dividends:

…it is the Group's intention to distribute to shareholders cash surplus to its expected operational and development requirements and additionally, the Group intends to pay as dividend any royalties received from Kilimapesa Gold on the royalty agreement signed.

It is not clear if a dividend will be declared with the FY21 results, and in what size, but they surely can’t be far away. With 2p+ EPS it is certainly possible that this could eventually be as high as 1p/share, although probably not initially. As the last few years of Goldplat have shown, this is not without risks, however, if they can return to large, and more importantly sustainable dividends in the future, then it is hard not to see some level of re-rating occur.

Have a great weekend all!