Small Caps Live Weekly Summary

Takeovers HOME LOAD K3C PEN VTU GMS ARGO QUIZ

A reduced service this week, not due to snow and ice, industrial action or staffing issues, but simply lots going on in real life.

Takeovers

Perhaps the biggest news of the week is that takeovers continue to be in full swing, with offers for Crestchic and K3 Capital being announced. Some investors may feel a little peeved at the low premiums being offered. However, these are companies whose price has been bid up prior to their offer being received, either because news has leaked or simply because they had short-term momentum that was being bought by investors. Management are usually fairly savvy with these things. They usually recommend an offer when the company is trading well (particularly for cyclicals such as Crestchic) and the acquirer offers a reasonable premium over a longer period of time. Optimistic bids which appear to offer a decent premium in the short term but take advantage of weak market conditions, tend to be much less successful.

But not every takeover is being rejected by shareholders. Sometimes the acquirer is pulling out, as happened with Pendragon. This is what the offerer, Hedin, had to say:

Given the challenging market conditions and uncertain economic outlook, Hedin confirms that it does not intend to make an offer for Pendragon.

It is possible Hedin had been hoping for a higher bid (they say they'd consider bids above 31p) for some time and have been messing shareholders around for months.

Pendragon comment:

The economic backdrop remains challenging, however the Board continues to expect to deliver group underlying profit before tax in line with expectations for the current financial year.

If anything, we would suggest that concerns over the agency model killed this, not the short-term outlook, which remains exceptionally strong.

Large Caps Live

WayneJ welcomed Boatman Capital to a brief LCL to discuss their open letter to the Home REIT board. Here is WayneJ’s summary of what was discussed:

(1) Investment company buys property from a developer

(2) But only on condition developer gives money to a charity for a year's rent

(3) The charity is then the tenant of the investment company for 25 years

(4) The charity then rents the property - usually (I think) on a room-by-room or individual basis to a Local Authority for homeless people, so they get Exempt Housing Benefit

(5) The charity is also meant to ensure rehab/support/mentoring/care etc

(6) There are lots of issues raised about the capacity of the charities to scale up to go from zero to 500 - 1000 beds

(7) And whether they have robust balance sheets

(8) And then there is the issue of whether these charities can be considered quality long-term inflation-linked tenants. This is ultimately important as the capitalisation rate drives the valuation.

(9) Of course, there is the issue of alternative use - and it is not clear whether the houses have the necessary EPC certificates for future use as HMOs

(10) And the debt position is apparently 15% net leverage, but clearly, this assumes no massive spending on refurb to improve EPCs.

(11) And the true valuation depends on how much overpayment there was upfront.

Small Caps

Vertu Motors (VTU.L) - Acquisition of Helston Motors

We’ve covered most of the details in the past, so we won’t go over old ground. 6.8x EBITDA looks steep compared to buying back their own shares, but then is double-digit EPS accretive, and the market liked the deal after a slow start.

This is what broker Zeus had to say:

Vertu has announced the acquisition of Helston, subject to completion, which we anticipate will enhance our FY24 and FY25 EPS forecasts by 18.7% and 24.7%, respectively.

The estimated acquisition ROCE (incremental EBIT / consideration) of 11.9% in FY24 and 14.9% in FY25 is in excess of the Group WACC of 8.5%.

Based on current forecasts, Vertu trades on only 5.7x FY23 P/E. The forecast EPS accretion in FY24 and FY25, post-completion, will reduce Vertu’s P/E multiples in these years (all else being equal FY24 P/E of 5.5x falling to 4.7x). We think this is materially undervalued. Our 104.7p valuation estimate from our 5 October note will be updated post completion, but we anticipate the Helston acquisition will drive further creation of shareholder value.

Note how Zeus avoid commenting on Vertu's own EV/EBITDA, which may well be 2.6x pre-deal as Stockopedia claim. From the RNS, but also mirrored by Zeus:

Post completion, the Group expects net debt at year-end 28 February 2023 to be £100-110m, with net debt/EBITDA5 below 1.4x. Due to the ongoing strong cash generative nature of the Group, net debt/EBITDA is expected to be around 1.0x by year-end 28 February 2025.

To us, this suggests they currently have no other material deals in the works that would prevent the buyback from a regulatory perspective, but perhaps this and the relatively short-term nature of much of the debt facilities/interest rates fixes could indicate the priority will be for debt repayment over share buybacks.

Gulf Marine Services (GMS.L) - Trading Update

EBITDA for the year to 31 December 2022 is expected to be between US$70‐US$72m, which is within the previous guidance range given.

In the H1 results, they said:

EBITDA guidance for 2022 remains at US$ 70 - 80 million

So not great. Also today:

Vessel utilization for 2022 is projected to be 87%, up from 85% in 2021, and day rates are on average up 7% versus last year.

vs September:

increased utilisation for H1 2022 to 89%...forecasted utilisation of 86% for H2

They comment today:

The increase in utilization is despite some unfavorable weather conditions and options on contracts not having been exercised.

They announced a number of new contracts since we covered the interims, and today they say:

increased our backlog to US$378 million

vs September:

Secured backlog was US$ 163.3 million at 30 June 2022 (30 June 2021: US$ 215.4 million)

It is difficult to know whether "backlog" and "secured backlog" are the same thing, but I think it is safe to say from the commentary that the June 2022 backlog was particularly low, and it has significantly improved since.

However, the rates are the key thing here, since utilisation is pretty much maxed out, and they can’t afford the capex to expand the fleet. In light of this, a 7% increase in day rates is not good. Rates really need to triple from here to make this look good value, despite the large discount to tangible book. Unless day rates soar from here these assets will remain unproductive until they are eventually scrapped.

Fans of the stock always point out that the cash flow against equity looks great. However, this will always look good because they have large depreciation. But this will be a real cost eventually since their vessels gradually rust. And they have a massive debt that needs servicing with the cash flow.

Argo Blockchain (ARB.L) - Operational Update

You don't hear much about blockchain nowadays, but we understand that bitcoin at least is still going.

During the month of November, Argo mined 198 Bitcoin or Bitcoin Equivalents (together, BTC) compared to 204 BTC in October 2022. The decrease in BTC mined was primarily due to an increase in the Bitcoin network difficulty in November compared to October.

Still, never mind, perhaps the value of each bitcoin increased when the mining difficulty got harder? Inexplicably though, bitcoins were £17,868 each at the end of October versus £14,217 at the end of November. The good news is perhaps then that they cash them in fairly quickly:

As of 30 November 2022, the Company held 126 Bitcoin, of which 116 were BTC Equivalents.

As everybody knows, the advantage of bitcoin over normal transactions is that everything is instant and free of any cost. This is presumably why it takes 9 days to say how many bitcoins you have mined and how many you have.

Argo generated this income at a Bitcoin and Bitcoin Equivalent Mining Margin of 29% for the month of November (October 2022: 32%).

Investors would be sensible to check whether this includes all costs, or indeed, any of the major costs in mining crypto, which are electricity and depreciation.

Argo continues to engage in financing discussions, as announced on 31 October 2022, to provide the Company with working capital sufficient for its present requirements.

Or to put it another way, Argo doesn't currently have sufficient working capital for its present requirements.

Should Argo be unsuccessful in completing any further financing, Argo would become cash flow negative in the near term and would need to curtail or cease operations.

But never mind, they do assure us that they are "endeavouring" not to collapse.

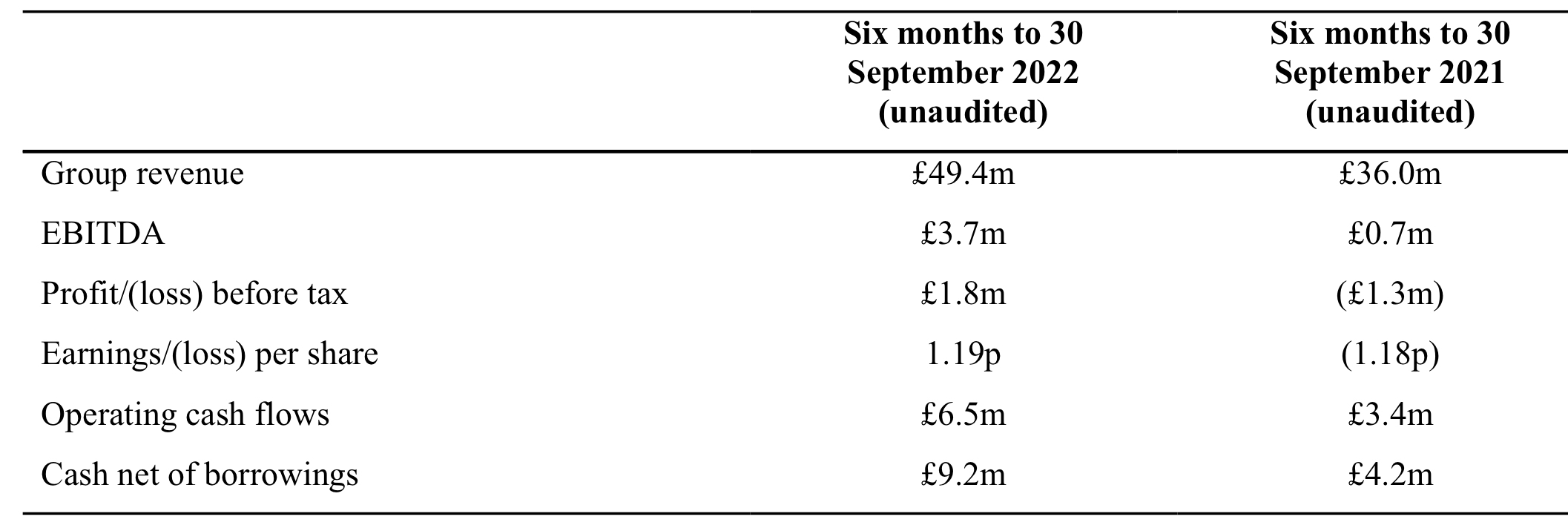

Quiz (QUIZ.L) - Interim Results

Strong results from Quiz:

Cash is likely to be a seasonal high, but is still up significantly on last year. However, the outlook is a bit mixed. First, they say:

Sales for the two months to 30 November 2022, including the Black Friday sales period, totalled £16.0 million (2022: £16.2 million) and were broadly in-line with management expectations with demand in recent weeks helping to offset weaker than anticipated revenues in October

Broadly, meaning slightly below, of course. But then later:

Notwithstanding, the recent volatility in demand and that QUIZ's important Christmas trading and January sales periods are still to come, the Board continues to anticipate delivering a full year outcome which will be at least in line with market expectations

This pattern of a weak October and then a bounce back in November seems to be a pattern in a lot of retail stocks. It appears to have caught out a lot of investors who sold into the weak sector outlook in October.

That’s it for this week. Check out the discord server for other discussions from this week.