Small Caps Live weekly Summary

Inflation D4T4 BSE CAPD CBOX VLX

Large caps live was back this week with a look at inflationary impacts. In small cap land, we mainly looked at new news from some old favs.

We are all excited about the upcoming Mello 2022 in London on 25-26th May. For those who haven’t attended before this event is well worth travelling/taking time off work/etc. for the opportunity to meet companies in-person plus listen to some great talks. You can book tickets here. Currently, tickets are half-price using the code “TwitMM50”.

Large Caps Live

I thought I would discuss inflation today. So we all know that inflation is going up but reading an article in the FT made me think about it in a slightly different way. Frankly, all you need is the title - 'UK households cancel streaming subscriptions in record numbers'. When I was a lad we used to split consumer companies into consumer discretionary and non-discretionary companies. Clearly (?) it appears that streaming services are 'discretionary'. So what occurred to me was the following:

(1) The focus is on the inflation rate

(2) But I would suggest we should be looking at the fall in cash available for discretionary spending - ie as fuel/taxes/mortgage or rent goes up then the fall in discretionary spend will be significantly more than the rise in the inflation rate.

(3) So as always let’s start with some data - I found this which is interesting:

I am going to focus on the monthly spend column. I have assumed that transport costs have gone up 20%, housing has gone up 10% and utilities have gone up 30%. This means that the 'non-discretionary' spend has gone to £2182.

Originally, the non-discretionary spend was £2035 - so the increase (ie 2181 over 2035) is about 7.2% which is roughly where it is believed that CPI is (I think the last quote I saw was 7.5%). But perhaps more importantly it means, assuming that the household budget remains circa £2548, that the discretionary spend has fallen from £512 per month to £365 ie a fall of 28.7%.

Now there are a lot of 'ifs and buts' in all the above - amongst others that the numbers above rely on a 2020 ONS survey. And I have 'eyeballed' transport, utilities and housing increases, and also ignored any increases in costs for package holidays etc due to fuel. And as we used to say - everyone's personal inflation rate is different.

But the point remains - that the impact on discretionary budgets due to inflation, all other things being equal, can be a multiple of the inflation rate - but with a negative number rather than a positive number.

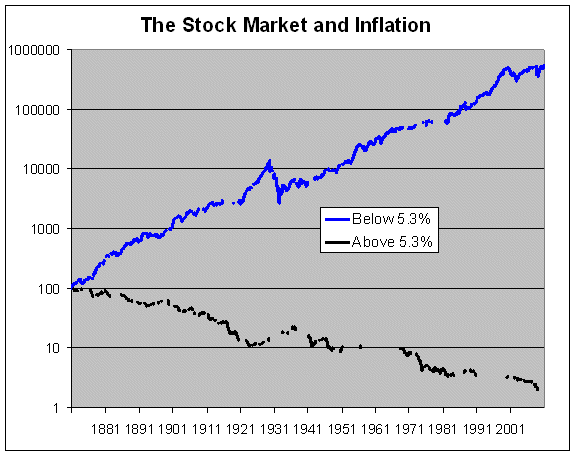

So the next question for me is what happens to stock market performance when we have high inflation. The problem with the question is that the performance of the markets depends not just on inflation, but also on GDP growth (real and nominal), debt levels, the mix of sectors etc. Nevertheless, we need to start somewhere.

I found this chart interesting:

However, I think more interesting is the question of 'balanced portfolios'. Let me take a step back and explain. Over the previous 3 - 4 decades, typical advice of financial advisors has been a 'balanced portfolio' which typically was a 40:60 portfolio - ie 40% bonds and 60% equities. I would suggest that to some extent that was a 'lazy' allocation that benefitted brilliantly from falling rates:

- long bonds have benefitted from an increase in capital value due to rates falling

- corporate bonds have benefitted from an improvement in credit quality due to rates falling (lower rates imply the ability to leverage more so a 3x debt to EBTIDA at 15% rates looks foolish but looks safer at 0.5% rates)

- equities have benefitted from falling discount rates and rising growth expectations as a result (this second-order impact is often ignored but I would argue that a shift in interest rates also impacts growth expectations)

The question is what happens in an inflationary environment:

I would argue that in an inflationary environment the longer end of your bond portfolio suffers the most in decline in capital values. However, certain customers (eg insurance companies/pension funds) only care about the return at maturity so it is not an issue for everyone - but is certainly for some.

Therefore I would expect that rationally, as inflation expectations rise you want to sell your long-duration bonds and buy short-duration so you can roll into higher rates faster - I would argue that probably has a significant impact on yield curve inversion and is often ignored.

Therefore, I would expect that, rationally, as inflation expectations rise you want to sell your long-duration bonds and buy short duration so you can roll into higher rates faster - I would argue that probably has a significant impact on yield curve inversion and is often ignored.

Small Caps

D4T4 Solutions (D4T4.L) - Trading Update

Mark has been pretty bearish on D4T4 in the past. SaaS has been a buzzword since Microsoft switched to their Office 365 model. A lot of investors hadn't clocked that the first year or so of Office 365 would see big drops in high-margin revenue before the ARR stream comes through. Buying Microsoft when the market worried about the initial drop in revenue proved to be a great move. Since then, every software company has been going after this holy grail of Annually Recurring Revenue, since it is sticky and predictable. And the narrative for many has been, don't worry about short term revenue hits - this is a sign the SaaS is working.

D4T4 have presented this narrative too. The problem is that they have been talking about a Saas transition for several years now, while their revenue looked like this:

And EPS like this:

So little sign that their years of attempted SaaS transition have really gained any traction. However, the share price has been weak this year and the stock has almost halved, making the valuation less stretched, so this week’s trading update is worth reading:

The Group performed strongly in the second half of the financial year, and consequently the Group Revenues are expected to be in line with market expectations, whilst the Adjusted Profit Before Tax* is expected to be at the upper end of the range of market expectations.

For these expectations we turn to house broker finnCap:

Adj. PBT will be at the upper end of expectations, and we raise our FY22 earnings forecasts by +23% from £2.6m to £3.2m.

That works out to be 6.9p EPS which is a decent beat. Although still below where forecasts were 9 months ago:

For 2023, finnCap say:

We also make no changes to FY23 forecasts until we have greater detail in the results.

Simplistically, there is evidence that finnCap are (being guided) on the conservative side. A similar EPS beat for the full year would give 12p and a PE of under 20 and a PEG under 0.4. This would be good value if this really is the start of the long-awaited SaaS growth. There are some encouraging signs on this front:

Moreover, during the year the Group increased annual recurring revenue (ARR**) significantly by 32% to £14.0 million (2021: £10.6 million).

Although the company still relies on large one-off license deals to hit its revenue forecasts. This is a small company and can’t simply demand that customers transition to SaaS deals in the same way that Microsoft can.

A lot depends on their new FDP product being successful and they certainly are expecting this in their outlook:

The Board remains highly confident in the Group's strategy, and we start the new financial year with a strengthened management team, good revenue visibility, and a strong pipeline of opportunities across both the Celebrus Customer Data Platform (CDP) and Fraud Data Platform (FDP) products. We expect to announce further contract wins in the coming months.

But we really need to know what FY24 will be like to make any judgement on valuation here. If the current forecast EPS trend continues the current price will look good value. However, if EPS in FY24 is flat then this looks expensive. The issue Mark has with investing now is that, given how reliant they still are on lumpy licence revenue, he doubts even the management have any idea what FY24 is going to look like, making this a gamble on a highly uncertain future. Leo thinks that the current momentum in the business means that this is a gamble worth taking, however.

Base Resources (BSE.L) - Quarterly Activities Report

In this quarter, the tonnes mined were down due to a couple of shutdowns - one planned and one unplanned. Production remained consistent with previous quarters, however, due to grade and stockpiling.

Perhaps the biggest news is how strong the pricing is at $740/t. The mix between the different Heavy Mineral Sand products helped here, but this is not just due to this effect. They are seeing even further price increases for the June quarter due to global demand outstripping supply.

One of the good things about Base is that their quarterly figures give enough information to roughly work out the financials. Revenue for the quarter is likely to be around $80m, driven largely by the pricing increase:

Net Profit looks to be around $34m:

Again these are recent highs for quarterly performance.

Free Cash Flow from Kwale is probably around $48m due to the large non-cash depreciation. Net cash has only gone from $37.1m to $41.5m, however. $26.1m has been paid as a dividend. There are c$2m of corporate costs and $1m spent on Toliara and $0.2m on exploration. This means around $14m has gone into working capital. Not a crazy amount, given the turnover here, but it is something to watch for in future announcements.

Looking forward, Q4 is likely to be equally cash-generative and at current pricing, Kwale is set to produce more than the current market cap in Free Cash Flow over the next couple of years, despite a short mine life.

Unfortunately, progress on the next mine Toliara remains stalled, waiting for approval from the Madagascan government and the share price is unlikely to make big moves upwards until this approval is granted.

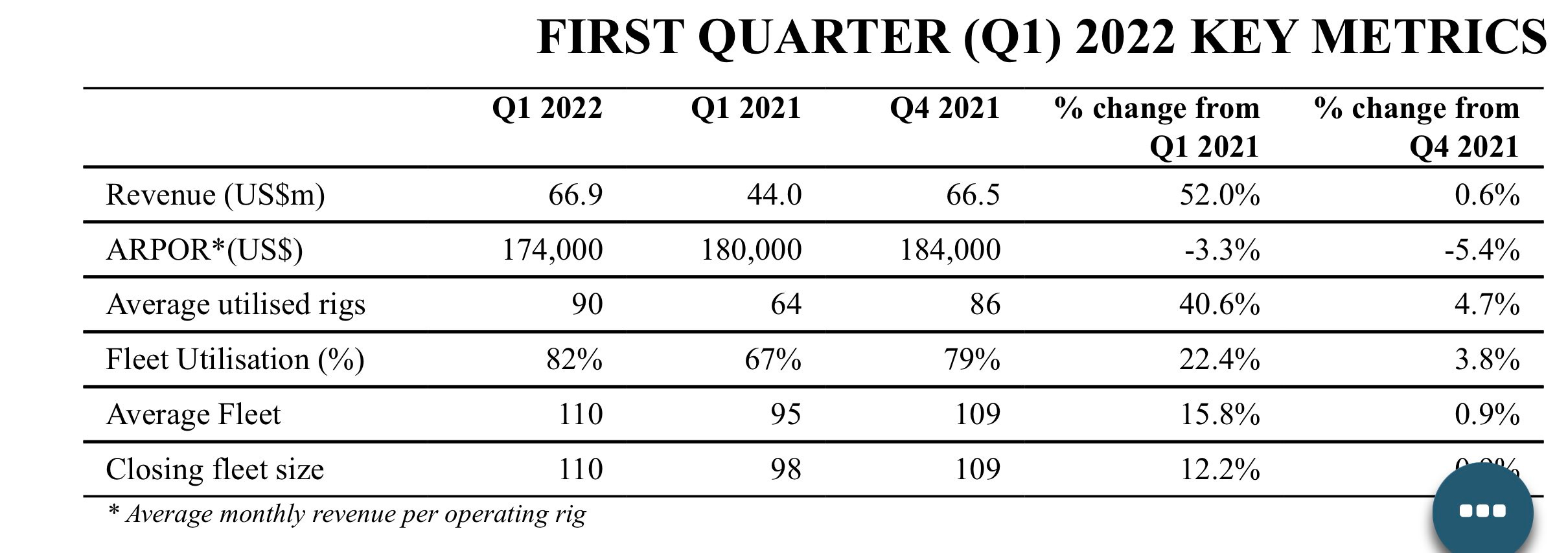

Capital Limited (CAPD.L) - Q1 Trading Update

As predicted, the Capital Q1 Trading Update was released on Thursday this week.

The number of rigs utilised is slightly above our expectations for this point in the year. However, ARPOR is below what we were expecting. These are the reasons given:

ARPOR in the quarter was impacted by increased rig movement within each region and also a higher proportion of revenue at Geita coming from the underground;

The reduced ARPOR on more underground rigs makes sense - the ARPOR on these is quite a bit lower than surface rigs but the margins are higher which means the EBITDA per rig is similar. Unfortunately, we don’t get EBITDA figures with the quarterly reports so we have to wait for H1 results to see the impact of this.

Leo is less convinced by the argument that increased rig movement caused a drop in ARPOR, since this hasn’t happened in recent quarters when utilisation rates have been increasing. Mark thinks that this is still a reasonable explanation, however, since additional rigs into existing mines will see greater initial productivity whereas rig moves to new mines will require bedding-in, so absolute changes in rig numbers are not necessarily a useful comparison. Still, it is a shame not to see this number increasing rather than decreasing in what we are assured is a tight rig market and the net effect of this is that drilling revenue was down around 5% quarter on quarter. This is the first such fall since Q4 2020 (the only fall in 2020).

Non-drilling revenue was also a little lower than we expected but they reiterate their full-year guidance so this only appears to be a timing issue, perhaps around the rollout of Chrysos machines. Here there is good news, with a second client for their Val D’Or lab:

Awarded a 12-month contract with New Found Gold for processing 20,000 samples per month through our new Val d'Or PhotonAssay facility commencing in Q2 2022.

Broker Tamesis viewed this quarter similarly, with utilisation above and ARPOR below their expectations and overall revenue in-line:

They retain their 160p Price Target:

With the current strong macro background of high gold prices and increasing mining activity in Africa we see this growth lasting well into 2024. Despite the shares being up 50% over the last 12 months we believe that they continue to look extremely undervalued; trading on a 2022E EV/EBITDA and P/E of 2.9x and 7.0x respectively – see Block Model. We remain confident in our recently set PT of 160p.

We have few details from the other brokers but it is worth noting that this Q1 update was well-received by Berenberg who nudged their Price Target up to 154p from 150p.

A final thing that stood out to us in this update was that the equity stakes continue to be a great business development tool. Three out of the four new contract wins announced this week are with companies where Capital owns an equity stake:

§ An extension of the exploration and delineation drilling contract with Predictive Discovery at its Bankan Project in Guinea, initially expanding from 2 to 5 rigs;

§ An exploration drilling contract with WIA Gold at its Bouaflé project in Côte d'Ivoire;

§ An extension of the exploration drilling contract with Golden Rim at the Kada Gold mine in Guinea;

§ An extension of the exploration drilling contract with Perseus Mining at the Yaouré Gold mine in in Côte d'Ivoire;

We expect lots more work for Capital to come from these relationships in the future as they progress their projects.

Cakebox Holdings (CBOX.L) - Full Year Trading Update

When we last looked at CakeBox, we commented that they didn't appear to have had a post-IPO stumble. Well, they have now! The H1 results in November turned out to be the high point:

This is why we are cautious of new IPOs!

The fall here seemed to come in three stages:

Sales by founders

Concerns were raised by Maynard Paton.

The Russian invasion of Ukraine lowered people’s risk appetite, particularly hitting stocks they didn't have full confidence in.

Risk appetite may have reduced, but has the appetite for egg-free cakes? They commented in January:

The Board confirms that, since the Company updated the market with its half year results in November, trading in H2 has continued strongly and in line with expectations for the full year.

This week they say:

Trading during the second half has continued to be strong across the Group's store estate and online delivery channels. Accordingly, the Group expects to report revenues for the year as up c.50% year-on-year, with adjusted profit before tax in line with market expectations.

2021 revenues were reported as £21.9m. So up 50% would be £32.9. In line with the Shore £32.8m forecast for the full year.

In terms of growth, +50% isn't a useful comparison as there were fewer lockdowns and more stores.

Revenues for the ten months to 31 March 2022, excluding the impact of the March 2020 lockdown and associated store closures from the comparative period, are expected to have increased c.32%, with total franchisee sales increasing 12% on a like-for-like* basis.

Normally, Leo would say 12% LFL is outstanding where the focus is on fast-growing store numbers with a capital-light franchise model, but there are two problems:

*Like-for-like: Stores trading for at least one full financial year prior to 31 March 2022.

That's easy to read as mature stores open for at least a year in the comparable period, but that's not what it says. Indeed, it is not clear what it means. It appears to include a store that opened on 31st March 2021 and therefore had zero revenue in the comparable period. Presumably, that's not right? So let's assume they mean simply stores that were open for both the whole 12 months to March 2021 and the whole 12 months to March 2022, excluding lockdowns. That means some of the LFLs started on stores that were only 2 months old at the start of the period. Add to this the usual caveat with LFLs that they exclude failed shops which closed and therefore have a survivorship bias.

The other issue is that June 2020 to March 2021 was not LFL with June 2021 to March 2022 in terms of lockdowns. The precise details of consumer spending are difficult to unravel, but just because cake shops were open did not mean footfall was the same or birthdays etc. were allowed to the same extent.

LFL numbers are super important because they tell you whether the cake shops are still "fashionable", and whether they getting close to saturation where new shops will cannibalise existing ones.

There's enough noise and confusion there which means we basically have no idea what the LFL figures are.

Our online delivery and Click & Collect options continue to expand the Group's customer base, and franchisee online sales increased c.41% during the year and c.27% on a ten-month basis.

Of course, these include new stores for the click and collect part.

The Group opened 11 new franchise stores in the second half (excluding kiosk openings), bringing the total number of stores opened in the full year to 31 (FY 2021: 24), and leaving the total number of Cake Box stores at period end at 185. New locations opened in the second half include Tottenham, Plymouth and Sunderland.

That's hardly massive growth. 20% in a year. We noted previously that their target was 250.

There continues to be a high level of interest in Cake Box's differentiated franchise proposition, with both strong demand for new stores from existing franchisees and a pipeline of new franchisee applicants representing 53 holding deposits held at the period end.

That seems very positive. Although hardly comparable years, last year they had 52 deposits.

The successful trial of Cake Box kiosks with Asda has continued to expand, with ten new kiosks opened during the year, taking the total number of Asda kiosks to 15 in addition to the Group's 20 shopping centre kiosks.

Also very positive. As is:

The Group's balance sheet remains strong, with a significant increase in the Group's net cash position, which stands at £5.2m at period end (FY 2021: £3.6m).

But that's not a good cash conversion on £4.8m profits, even accounting for dividends.

The CFO resigned with immediate effect in March and a COO appointed. There is no further mention of progress on improved controls etc. today.

Conclusion:

Before investing, Leo would want to wait for the full audited results and go through them very carefully, get clear answers on LFL figures and visit a variety of stores in person. Given the relatively limited/uncertain runway and likely higher admin costs from the larger management team, they don't look stunning cheap and at this price, it isn't immediately clear whether it is worth the effort. Investors in franchise businesses may also wish to take the time to visit a franchise show sometime, too.

Volex (VLX.L) - Trading Update

If you just looked at the chart here you’d expect that trading was getting worse:

However, the analyst consensus tells a slightly different story:

So, unsurprising this week’s update was well-received by the market:

Results ahead of expectations

The Group expects, subject to finalisation of the accounts and audit, revenues to be in excess of $605 million (FY2021: $443 million) and underlying operating profit2 to be in excess of $55.0 million (FY2021: $42.9 million).

Broker singer says:

[results] are ahead of consensus FY22E expectations of $581m

Singer now forecasts FY22 adjusted, fully diluted EPS as 26.4p, versus 25.9p in January. So this is a rather small EPS beat given that three months have passed. Still, a good performance, so how have they achieved it?

Volex has continued to trade strongly, delivering robust organic revenue growth, including a significant contribution from the Electric Vehicles sector, where revenue has almost doubled…

In a global inflationary environment, our ability to pass through increased costs to customers, protecting profitability while maintaining competitiveness, has been important. Our global teams have deep relationships with customers, enabling efficient and regular mechanisms to modify costs as required.

But of course, it is the outlook that is the most important. A beat from Q4 usually implies strong momentum, but they also say:

Demand has increased during the year with greater visibility of forward orders as customers look to secure manufacturing capacity.

The Group is well positioned to navigate the challenges of a dynamic macro-environment, underpinned by its diverse markets, capabilities and global manufacturing footprint.

As planned, during the year we have made strategic, targeted investment in production facilities, equipment, IT and people to support our long-term growth objectives. The strategic diversification achieved in recent years has positioned the Group well, with capital investment supporting organic revenue initiatives and vertical integration opportunities in growth areas.

They don't tell us how recent acquisitions have been doing, but clearly, contributions will annualise next year. On further acquisitions they say:

The Group continues to maintain a disciplined approach when assessing potential acquisition opportunities and enjoys a high degree of financial flexibility thanks to the new, enlarged debt facilities, secured in February 2022, which support Volex's ongoing growth plans.

Nat Rothschild comments:

We continue to pursue a number of exciting organic growth opportunities, while successfully acquiring and integrating compelling acquisitions, leaving us well placed for the future.

So no explicit outlook statement or guidance. Not much to go on at all. But that chart and the pre-update forward PE of 11, mean that this was received well. This is also an opportunity for guidance to be updated to include the benefit of a $13m acquisition completed just before the year-end. This is one advantage of acquisitive companies with debt facilities - forecasts don't include acquisitions that haven't happened but probably will. The acquisition combined with a positive outlook results in significant revenue and operating profit upgrades. That's the good news.

The bad news is that Singer sees little improvement in PBT, presumably on higher interest costs. At the EPS level, they actually cut slightly, perhaps due to higher UK corporation tax. In neither case is this explained or comparables given, leading us to question transparency. They have also cut their Price Target "reflecting the change in sector multiples".

So the bull case here is that they can continue acquiring by expanding their debt facilities ad infinitum and that they'll expand margins to their target 10% through sheer force of will despite inflationary pressures.

The bear case is that there's a shedload of exceptionals about to be dumped on shareholders and cash flow will collapse under the weight of maintenance CAPEX and debt servicing.

The FY results will probably be worth a good look, but this is NOT another opportunity like October 2019 when they had just finished sorting out all low margin business acquired in the previous acquisition spree.

That’s all for this week. Have a great weekend!