Small Caps Live Weekly Summary

AFRN AUTG BMS BSE CBOX CNC DX. LTHM PRES RBGP TND VTU

We often receive follow-up communication to these weekly summaries. They usually fall into two camps. The first are notes of appreciation. Some investors even suggest they would be willing to pay for this substack. However, our aim here is not to create a subscription model. Instead, if you do want to support us, there are a few ways you can do so:

Buy Mark’s book, Excellent Investing.

The book is packed full of wisdom and tackles complex topics, such as investing styles, overcoming behavioural biases and portfolio construction, in a practical and easy-to-read way. If you have already got a copy, please leave a review, or even buy an extra copy for a friend/enemy.

The Fund Your Retirement Podcast, which Mark features on, will shortly have a premium subscription option. More details to follow when it goes live, but consider subscribing to this great source of investing information when it arrives.

Leo has a referral link for one of the services we regularly use to analyse stocks: Research Tree. So if you are considering signing up for this service too, doing so via this link will give you a 10% annual discount, and Leo a free month.

Finally, for the charitably-minded, our friend Damian Cannon is raising money for the childbirth charity Tommy’s. Please sponsor him for this upcoming challenge and help him reach his target.

The second type of communication we get is when investors disagree with our summary. It is worth reminding everyone that these summaries are an attempt to take multiple viewpoints from many Discord contributors and create a pithy precis, with varying degrees of success. We don’t know every company well, so if you think we have missed something, or dissed your favourite share, the best thing to do is to hop onto the Discord server and join in the debate. The real value of SCL is the diversity of opinion. While we don’t always achieve it perfectly, the aim is for diverse, well-informed opinions to be cultivated. This is the main way investors can support us. Since this is the real value of SCL to us - sharing detailed analysis on UK small and mid-cap shares while avoiding groupthink.

Small Caps

Aferian (AFRN.L) - Trading Statement

We knew things were going wrong here, but here we see the actual figures. Device revenue has collapsed:

Device revenues in the first half are expected to be c.$9.4m, representing a decrease of 71% year-on-year.

That is quite some drop for a manufacturing business. However, the software side is doing ok:

Higher margin software and services revenue for the period is expected to be c.$13.7m (H1 2022: $12.0m), an increase of 14% versus the prior year, or 16% on a constant currency basis.

The company confirms that it will be EBITDA positive after cost reductions. However, net debt is still significant. They say they remain in compliance with covenants for the moment, but there is no update on amending future covenants, putting this at the very risky end of the investing spectrum.

What is interesting is that despite the uncertainty, broker Progressive are willing to re-introduce forecasts. This suggests that the company are confident enough to guide them, and the broker believes them. This is the outcome of that trust exercise:

Loss-making into 2024 isn't a great start. However, they are forecasting an almost elimination of the net debt over the next 18 months. If this is realistic, the free cash flow yield looks very good on a now much-reduced share price, even if the earnings yield isn’t positive.

Autins (AUTG.L) - Interim Results

The company is still loss-making, has net debt and trades at a premium to TBV, making them an unattractive investment at current share price levels:

· Loss per share of 1.65p (H1 22: loss of 2.83p)

· Net debt excluding IFRS16 lease liabilities increased to £2.42m (H1 22: £1.03m)

In the commentary, the CEO says:

"I am pleased to report that we have seen a significant improvement in margins and a return to EBITDA profitability, during the first half of 2023.

But then the going concern statement says:

UK sales volumes in H1 23 remained marginally below these forecasts, although EBITDA and cash performance remained above the targets presented to the UK lenders. The Board has assumed a slight improvement in revenues for H2 23, with further improvement and new wins expected in FY24. However, there remains uncertainty on the exact timing and sales improvement for the automotive market against the current backdrop of global supply chain considerations and continuously evolving vehicle platforms for which the technical specifications and likely production quantities are still to be reliably communicated.

So these results appear to be a miss, too.

Braemar (BMS.L) - Publication of Results, Investigation & Trading Update

The company confirms that they will be suspended from 30th June. Here is the issue:

During the past two years, in addition to establishing and developing the Group's growth strategy, the board has focused on ensuring that proper procedures are in place to deliver good practice throughout the business as it scales. As part of this work, the board and the Group's auditors have been carrying out an investigation into a particular transaction of circa $3m, which originated in 2013, and involves payments being made through to 2017.

The board is not presently comfortable with the manner in which the transaction has been historically represented and the remaining liability recorded in the Company's balance sheet. Upon conclusion of the investigation, should this liability be released, it would not affect the underlying trading profit or cash position of the Company for FY23.

We are not quite sure how a 2013-2017 revenue transaction leads to a liability in 2023 accounts. However, surely the maximum liability is $3m and the reputational damage?

The shares were down 24% initially on this news but bounced to down around 17%. This could be interesting for anyone not concerned with a period of indeterminate suspension.

Base Resources (BSE.L) - Production Guidance

The market didn’t like this update, with FY24 Production Guidance nearly halved on FY23. This should have been expected, given the move to lower-grade North Dune, although it comes in at the bottom end of what Mark was expecting.

However, the big disappointment here is not production numbers which are still highly cash-generative at current prices, but the lack of any future news on either Kenya or Madagascar. The company should still generate at least the current market cap in cash from Kwale operations before they cease. However, any production beyond that point is now looking increasingly uncertain.

CakeBox (CBOX.L) - Final Results

Not a great year, with revenue up less than inflation and profits down:

As always, the outlook perhaps matters most and here revenue continues to fall in real terms.

The Board is optimistic about the prospects for the year and the sales performance continues to be robust, with franchise sales up 5.4% like-for-like in the last 11 weeks.

But admin costs rise in real terms. Some of this is higher professional fees apparently relating to a GDPR etc. breach, adjusting that out and exceptionals admin costs still rose 20%.

The biggest problem appears to be the increased number of staff, but energy was also clearly an issue. Investors will want to satisfy themselves that the business can scale in the future. Otherwise, a forward P/E of 13 is unattractive.

Concurrent Technologies (CNC.L) - Final Results

Good news for holders here as they get their results released on the last day to avoid suspension. They say they are slightly ahead of market expectations, but these are still very poor compared to the prior year:

· Gross profit at £8.9m (2021: £11.4m)

· Gross margin at 48.6% (2021: 55.9%)

· EBITDA at £2.1m (2021 restated: £4.9m)

· Profit before Tax at £0.4m (2021 restated: Profit £3.5m)

However, the drop in cash is very significant:

Cash in the business at year end £4.5m (2021: £11.8m)

They give two reasons for this:

Deliberate use of cash for (i) increased component inventory to mitigate supply chain issues, and (ii) increased cost base to create more products and grow the business.

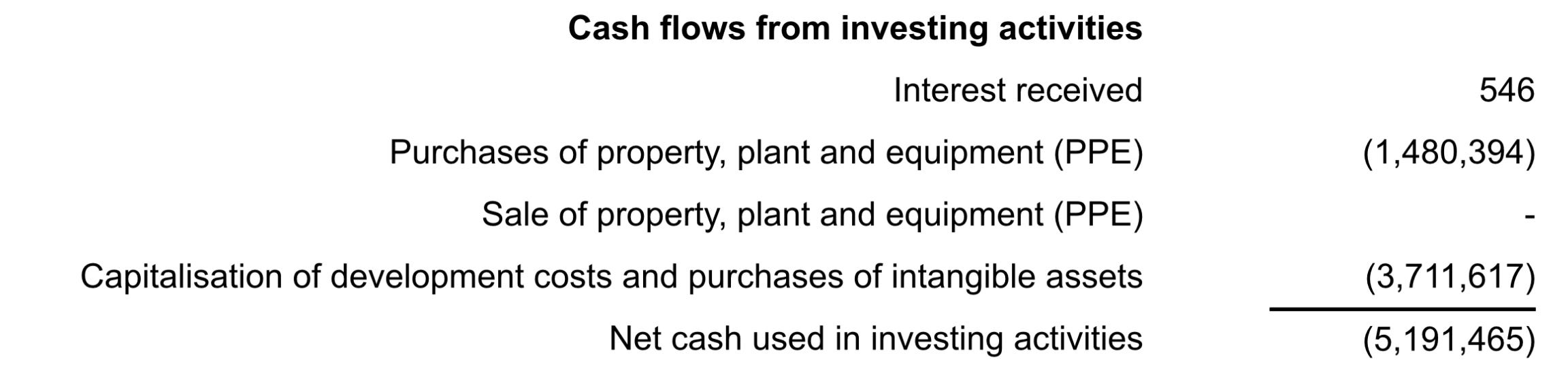

£3.7m has gone into inventories, so it may reverse over time. However, £1.5m has gone into PP&E, and £3.7m has gone into intangibles. Significantly above D&A:

So this is a bold move by the new management team, ramping up spending to try to grow again. It’s not a strategy that has worked out so far, but it may do in the future. You have to assume capitalised intangibles are wages in R&D, so if this is the new normal for cash spend, it better prove itself soon. With the market already pricing in a significant recovery/growth at the current share price, this needs to deliver and deliver it quickly. There’s a small rally in the shares in response to this release. But, presumably, relief at avoiding suspension rather than a response to the results themselves.

DX Group (DX.L) - Agreement regarding Tuffnells sites

This seems good news. Adding 15 former Tuffnells sites expands their network by about 30%. They also gain 250 employees, and 550 customers are added.

DX has signed an agreement with Interpath Advisory, the Administrator of Tuffnells, for an initial licence-to-occupy 13 former Tuffnells sites and agreed terms to purchase for £1 million cash the freehold of a further site. The initial licences are a precursor to entering into direct lease agreements. The Company has also agreed terms directly with a landlord for a long lease over a fifteenth site.

One site is freehold which is bought for £1m. We assume the "license to occupy" is for leased sites, and DX don't want to take on the leases at current rates or duration, apart from the 15th site. We are not entirely sure how it works with administrators who sub-lease property, but I expect new deals to be in place for some more of these sites at some point in the future.

This remains a very significant positive for DX, who look to be gaining significant business and experienced staff from this. This may not be fully reflected in the share price despite recent rises. The trading statement in July will help clarify this.

Jadestone Energy (JSE.L) - Result of Open Offer

Unsurprisingly, this open offer was not well supported due to the share price trading significantly below the offer price for the whole time:

This represents approximately 0.49% of the aggregate number of shares offered to Qualifying Shareholders pursuant to the Open Offer.

The surprising thing is that they got any takers at all. Who paid 45p for shares that could be bought in the market for 35-38p? And can they be our regular counterparty?

We do wonder if the price trading so far below the placing and open offer reflects a capitulation on behalf of other holders. When this happened to Hummingbird Resources recently, the post-raise dip was actually the nadir.

Latham (James) (LTHM.L) - Preliminary Results

This looks like a significant beat: 5% on revenue and perhaps 20% on EPS. However, it is difficult to be sure that the later forecasts are on the same basis as reported. The further good news is that they've also managed to free up cash:

Inventory levels have reduced to £67.5m from £74.2m last year as the easing of supply chain conditions meant we could reduce the investment we made last year in additional inventories.

This is despite cost-price product inflation of 6.5%. Even accepting that their strong cash position allowed them to take full advantage of the conditions in their FY 2022 in particular, they now appear to have significant excess cash.

The Board has declared a final dividend of 20.8p per Ordinary Share (2022: 19.0p) plus a special dividend of 8.0p (2022: 8.0p) to reflect the exceptional performances both this year and the previous year.

So there could be more to come here in the way of cash returns as surplus cash appears to be well in excess of £1/share.

Of course, there is also a detailed outlook statement which concludes:

The board is therefore very aware that the results for the last two years have been exceptional, and far beyond the profits earned before the start of the COVID-19 pandemic. The board's challenge is to navigate the business towards what is a more normal and realistic profit achievement which takes into account the market conditions we are operating in and the inflationary overhead pressures that all companies are facing.

Those "inflationary overhead pressures" are, of course, the wage part of the now well-embedded wage-price spiral. Commodities like wood (or technically "lumber") are likely to fall in price.

However, Leo’s guess is that FY 2024 EPS will be raised to around 170p, putting them on a PE of 7x. Adjusting for excess cash, that is more like 6-6.5x. This seems cheap for a company of such high quality, even in today's market. However, commodity deflation may hit their nominal gross profits at some point, so investors need to be prepared for a bumpy ride.

Pressure Technologies (PRES.L) - Interim Results

Obviously, these are poor:

● Adjusted operating loss of £0.5 million (2022: loss of £2.1 million)

● Reported loss before tax of £1.4 million (2022: loss of £2.3 million)

● Reported basic loss per share of 3.9p (2022: loss per share of 6.0p) and Adjusted basic loss per share3 of 2.3p (2022: loss per share of 5.7p)

● Net debt of £3.7 million (2022: £5.4 million; 1 October 2022: £3.5 million);

However, they reckon they will do £2m EBITDA in H2, which could be about £1m PBT. And now the balance sheet isn't terrible anymore after multiple equity raises. So this could be starting to look cheap again with a £15m market cap if that sort of profitability is just the start of the recovery. The problem is that trading is massively lumpy and cyclical. So the strong H2 is equally likely to be a one-off rather than something to base a long-term recovery on.

RBG Holdings (RBGH.L) - Press Article

If anyone has missed why this share price keeps on falling, then this article gives a good summary. We have nothing really to add, but needless to say, we are watching from the sidelines.

Tandem (TND.L) - AGM Statement

This statement was hard to decipher. This reads like a profits warning:

Trading conditions to 23 June 2023 have remained persistently challenging, however, we were pleased with performance in the second quarter particularly in bicycles and eMobility. The prevailing economic landscape, exacerbated by high interest rates and the impact of the ongoing cost of living crisis on the retail sector, has further compounded the obstacles we face.

As does this:

Overall, our sales have experienced a 26% decrease compared to the prior year. Notably, our Toys, Sports, and Leisure division has been particularly affected, with a 46% decline.

But then they say that this is due to FOB changes:

We have also experienced a shift in the buying habits of national retailers who are transitioning from Free On Board (FOB) purchases to Direct Delivery (DD).

This hit UP Global Sourcing a few years ago, so it is not a new trend. However, perhaps the lesson from that experience is to trust that the revenues will come through eventually.

And they say:

We therefore remain cautiously optimistic as the year progresses, anticipating a recovery in this segment.

But then, how bad was Q1 for bikes when they can say:

In our Bicycles division, although sales are behind last year overall by 20%, results in Q2 are significantly ahead of the equivalent period in the prior year as we continue to release new products.

So Q1 & Q2 are down 20% on last year, but Q2 is significantly ahead of last year!

We had to turn to the broker’s note to get an idea of what is going on. And they have been guided that this is an inline update. And therein lies the problem. “In line” is this:

i.e. an EV/EBITDA of 8, even if everything goes well and they successfully mitigate all their challenges. A debt-adjusted P/E of 11 for 2024, even after the share price fall in response to this statement, doesn't look particularly cheap. They have historically traded on single-digit P/Es.

On the plus side, they are now approaching 0.5x TBV. However, there is no sign of these assets becoming productive anytime soon. And this book value hasn’t stopped recent share price falls, nor do we expect it to mitigate future ones.

Vertu Motors (VTU.L) - AGM Trading Update

A strong update from Vertu for the first three months reflects well-known market dynamics, especially on the used side. As they say:

New vehicle supply continues to improve whilst constraints in used vehicle supply in the UK are likely to persist, helping to underpin used vehicle values and gross profit.

...but it is important to understand that this dynamic is abnormal, unstable, and cannot continue forever. Uncertainty is building, and it is not clear how much margin for error is included in current-year forecasts:

The market outlook, however, remains unclear due to uncertainty of consumer demand in the light of the impact of inflationary pressures and higher interest rates.

Broker forecasts are unchanged, with the in-progress buyback giving some 1-2% slack on EPS forecasts. EPS is currently forecast to grow to 9.9p for FY February 2024, 10.5p for 2025 and then stay level for 2026. All we know for sure is that the outturn will be less smooth than that.

The market seems unimpressed with this update, perhaps hoping for another upgrade, but was that reasonable given they were last upgraded on 10th May? The recent share price response appears to have been more due to the Looker’s acquisition than the positive trading statement in May. The aggressive buyback has also now stopped, presumably because the management thinks the price has got a little ahead of itself in the short term?

The shares trade at a small premium to TBV, which compares favourably to recent deals in the sector. This is a less-likely takeover candidate due to the capital structure of lots of owned property and the unconcentrated nature of the shareholder base. If a bid did happen, then we think this would be based on similar earnings multiples to Lookers, which, as Zeus points out this week, is only around 85p. So still some upside if an offer does appear, but not spectacular.

That’s it for this week. Enjoy your weekend!