Small Caps Live Weekly Summary

GDP UPGS TRD NICL SNWS GATC TPFG GHS

A busier week for small cap news this week, so we’ll dive right in…

Large Caps Live Monday 1st November

Wayne took a look at whether he should take out a fixed-rate mortgage and then invest the proceeds into “safe” stocks.

Check out the full thread here for details. However, his conclusion was:

We came to the conclusion that leveraging up and gaining circa £1,850 per year by borrowing £100,000 does not seem very attractive.

Particularly when the downside risk is so great:

We are risking our principal home as security…Why risk a £100,000 addition to our mortgage/house for circa £2k per year after tax and the risk that it could all blow up.

Small Caps Live Wednesday 3rd November

Goldplat (GDP.L) – Q1 Trading Update

Microcap gold recovery specialist Goldplat released their Q1 results this morning, where the flat result masks 2 quite different divisional performances:

The Ghana operations continue to perform well as a result of the steady supply of material and achieved an operating profit for Q1 of £839,000 (Q1, 30 September 2020: £280,000). The South African operation achieved an operating profit for Q1 of £564,000 (Q1, 30 September 2020: £1,123,000), reflecting a significantly lower gold price in Rand terms in the period.

Here’s what that divisional performance looks like over the last couple of years:

As you can see, Ghana continues to go from strength to strength, whereas South Africa is struggling. The reason given is:

Although the gold produced and sold year-on-year was similar, the average gold price in South African Rands ('ZAR') for Q1 was 19.3% lower year-on-year, resulting in operating profits being lower by 50%.

Although the gold price in $ hasn’t been that weak, the rand strength means that operating profits have been weaker than the gold price move would initially suggest. Something Sylvania Platinum has found for PGM pricing too.

Unlike a straight gold miner, Goldplat has the ability to flex its business to the gold price. They pay less for the waste material they process when the gold price is lower and can process lower grade material when the gold price is higher. However, since they have a pipeline of material, these changes can lag the gold price. The South African operation’s performance is likely to recover in the coming quarters for this reason. Plus, they have some unrealised profits to unwind from inventory that will help:

Unrealised profits contained in material remains high at GBP900,000 (30 June 2021 - GBP1,100,000) and is partly due to the increase in gravity gold production and the longer sales cycle it takes to realise the profit. We are focussed on reducing the turnover time and the figure should return to normal levels, circa GBP500,000 within the next two quarters.

Given the different tax rates and minority interest in South Africa, a pound operating profit in Ghana is worth 30% more net to shareholders. If we assume that both divisions can average about £800k operating profit per quarter for the rest of FY22 then this would be around 2.2p EPS, which compares very favourably with a current share price of 7.2p.

In terms of the balance sheet, they had £2.34m cash at Q1 end, and have taken on £3.1m of debt to buy out some of the South African Minority Interest.

They also say:

We have agreed with Caracal Gold to take up the remainder of the initial share consideration on the sale of Kilimapesa at the initial listing price of Caracal Gold and as a result, Caracal Gold has allotted an additional circa 32 878 000 shares in lieu of a cash payment of US$450,000, increasing the Group's shareholding in Caracal to 9.2%.

They had 103.8m shares in Caracal, making their current holding 136.7m. The current bid price is 1.35p, making this holding worth £1.85m, although they have a lock-up in place and would need to place the shares at maybe a discount if they came to sell. This makes net cash and investments about £1m.

For the first time in a number of years there seems to be some momentum behind a number of their growth initiatives:

During Q1 we have built our strategic precious metals ('PGM') material to a level to warrant capital expenditure of USD 300,000 on a plant to extract its value. This new plant will also enable us to further develop our PGM recovery business.

The “plat” part of the Goldplat name shows that they have always intended to be a PGM producer but haven’t had the scale to develop this area. As the likes of Sylvania Platinum have shown recovery of PGM from mining waste tailings is a very profitable area. With Sylvania, the market is also pricing in a strong recovery in PGM pricing in the future too. Although the longevity of any PGM recovery will require ICE cars to still be a significant part of our future.

As part our strategy to build partnerships in industry and to create longer term visibility of supply of materials and associated earnings, we have agreed with West Wits Mining Limited (ASX: WWI), as announced on 12 October 2021, to process material from their early mine programme through our plant on a toll treatment basis. The initial programme will last approximately 6 months with material processed through our largest CIL circuit, with the option to extend.

Toll treatment here gives a fairly guaranteed income for one of the largest parts of their operation in the near term, and the ability to develop longer-term relationships with a new gold producer.

Towards the end of October 2021 an application was made to get environmental approval for the installation of a pipeline to a process facility in the area. This pipeline could provide us with an avenue to pump and process our current tailings facility which contains circa 82,000 ounces of gold ('See the announcement dated 29 January 2016'). The approval process will take approximately 12 months.

This pipeline is perhaps to DRDGold, since there was historically a pipeline that ran close to the Goldplat plant to the DRDGold operation. Progress here has been incredibly slow and the latest plan was for this material to be dried and trucked, or for them to develop the processing capacity themselves, both of which could take another few years. However, if they can deliver this via pipeline then margins should be higher, and there will be no need for drying the material. There is, of course, recovery percentage and costs to consider, but the in-situ gold here is over £100m worth so any option that progresses this could well be material to the £12m market cap company.

And in Ghana, there seems to be further momentum with progress made in being able to access material from Cote D’Ivoire, pre-processing facilities planned for South America, and access to artisanal tailings material in Ghana itself.

With the challenges of Kilimapesa behind them, then it seems that management effort has been able to be focussed on areas of profitable growth for the first time in a long while. This should pay dividends in time, literally:

With initial consideration on the sale of Kilimapesa and majority of the restructuring within the Group completed, we will evaluate our options to return value to shareholders.

UP Global Sourcing (UPGS.L) – Final Results

These were in line with the FY update and so it is the history and outlook that is more important, although we will go through the statement a little.

First, the history:

They hadn't been on the market they long, and a year or so after floating they disappointed shareholders with several profit warnings. Clearly, this lost them a lot of credibility, and they took a long time to recover shareholder confidence even after the business returned to growth.

Then COVID came along, longer-term forecasts were withdrawn and short-term ones slashed, and shareholders got another chance to buy in the 30s. Even allowing for initial over-caution and some luck (UK discounters allowed to stay open), execution during the period has been outstanding and as you can see above the share price rallied strongly above the 150p float price.

Things were starting to look a bit toppy in the middle of this year, but proponents pointed to very considerable financial firepower for possible acquisitions. After a very small one, the opportunity came up to buy the Salter brand which they had previously been licencing, and the high share price allowed for some share issuance to fund part of it.

Then concerns over shipping started to hit them really hard. Many argued that if anybody could cope with this well then it would be UPGS, but questions remained about what the impact would be. The FY 2021 update assured us that it was fine for the year to 31st July, but then of course concern switched to the FY 2022. The share price fell 30%, leaving institutions who participated in the fundraise significantly underwater, again. This is the context in which they issued their FY results yesterday:

Total revenue increased 17.9 % to £136.4 m (FY 20: £115.7 m)

Though already known, this was an outstanding outcome under the circumstances, being also well above FY 20219 of £123m. Acquisitions in the period made a minimal impact, perhaps £0.6m of revenue. The acquisition is now fully integrated and is expected to significantly enhance earnings in FY 22, perhaps not hard given a good proportion of it was debt-funded.

Underlying EBITDA up 28.3 % to £13.3 m (FY 20: £10.4 m)

Underlying Earnings Per Share^ up 34.2 % to 10.6 p (FY 20: 7.9 p)

Again, it is fairer to compare with 2019, which was £10.8m & 8.1p.

The major concern going into this update was, of course, logistics, about which they say:

For importers such as ourselves, this drop in global capacity has led to a significant increase in the cost of shipping leading to downward pressure on gross margins. We have taken various steps to mitigate this but gross margins in H2 FY 21 nonetheless were 1.4 % lower than H1 FY 21. Given the scale of increased shipping costs, we were pleased with this outcome.

In addition, the reduced shipping capacity has led to reduced availability of shipping slots with importers typically having to prioritise, ration and reduce the volume of imported product. In our case, we have prioritised our forward orders from retail customers ahead of stock purchases which has had the effect of reducing stock availability for the other parts of our business, including online, during H2 FY 21. Without these constraints on availability, we would have expected higher revenues in H2 FY 21.

We believe that global shipping will remain disrupted until after Chinese New Year (February 2022). While this will continue to make stock availability tighter than we would like, we nonetheless anticipate growth in FY 22 driven through our FOB and forward order channels. This disruption is also predicted to keep shipping costs high, although we expect this to be further mitigated in FY 22 by an improved and largely contracted GBP/USD exchange rate.

Note that on the subsequent investor call they gave more detail and clarified that by "until after CNY" they meant throughout the next year to end July 2022, at least, but there may be several major tailwinds kicking in from 2022H2:

The FY 2022 forecasts are based on the shipping situation remaining "as is", despite the fact that costs now appear to be on a falling trend.

They have reported that retailers remain short of stock and so the demand side will remain strong. They are still underrepresented in supermarkets so considerable scope there, and Tesco were in the other day.

They know they have gained market share and expect to at least retain those gains.

Geographically there's still loads to go in Germany and Poland (relative to the UK, where they are reliant on market share gains) and are making early progress in Australia / New Zealand.

Yet Equity Development are still predicting 6% revenue growth every year (FY 2022 they have adjusted for Salter, so a bigger jump then). So it is clear that, yet again, forecasts are very conservative. They are forecasting 14.1p in FY 2022 and 15.3p in FY 2023.

There is clearly much uncertainty for FY 2022, but given the above tailwinds, it is still possible for them to beat EPS forecasts for 2022 and 2023. If they get to 20p EPS for FY 2023, which Leo thinks is very possible, the current 200p share price doesn't look expensive.

Mark has a concern though: a lot of the EPS growth for 2022 comes from the Salter acquisition. But this has come at a price. Although they issued about 10% equity to finance the deal, they also took on significant debt. Together with the working capital build, this has led them to be dependent on some short-term facilities, including invoice discounting which tends to be the most expensive and least secure form of debt.

The current ratio is now just 1.24. What is a secure value changes depending on industry dynamics, but as a distributor you’d normally want the current ratio to be higher than this. If there are unexpected further issues with the supply chain then running their finances this tight could lead to problems. There are some mitigating factors, such as the low cost of debt, and the presence of insurance which means the chance of this coming back to bite them is very slim, but the risk here has increased as well as the upside from the Salter acquisition.

On balance, this increased risk wouldn’t be enough to prevent Mark from investing, given the right price, but, until they rebuild their balance sheet it would be wise to keep an eye out for any signs of weakness and get out at the first sign of trouble.

Triad (TRD.L) – Half Year Results

IT recruiter & outsourcer Triad announced their Half Year Results this week. This is a tightly-held stock, with a controlling septuagenarian Executive Chairman where, having met him, we doubt his executive capacity. There has been a falling out with a major shareholder, and the latest non-exec appointment was the Chairman’s daughter. So this is not exactly the most shareholder-friendly company.

This means that we don’t get regular trading statements but instead have to wait for the results to find out how they are doing. Quite well as it turns out, at least on the profit side:

They have had a recent strategy of increasing permanent headcount. This bit them during the initial covid panic but is now starting to deliver, as increased utilisation delivers increased margin and profits:

This has been a very strong first half, building on the progress made during last year. The Group continued to recruit more permanent staff, with 34 consultants joining in the period. The increase in headcount, taking the Group total to over 100 during the period, contributed significantly to improved gross profit without diluting utilisation levels. Gross profit as a percentage of sales also increased significantly versus the same time last year, as well as improving on the second half of last year.

For many years, Triad traded in the 40-70p range reflecting that it is a people business with cyclical characteristics. There were a few good years followed by a few bad, and hence, while this is often a cash-generative business, it deserved a relatively low rating, particularly since management tended to hang on to that cash rather than return it to shareholders.

At the end of 2020, however, people decided that Triad was now a blockchain company and the price soared to over £1.50/share. The only link to blockchain we could identify, however, was that they hired a consultant who had mentioned this on his CV and a partnership with a company called Stratis.

Indeed, the only mention of blockchain in these results says:

On the other side of the award process, the Group is proud to be supporting the forthcoming blockchain hackathon run by our technology partner Stratis.

A companies’ house search reveals that Stratis filed micro-company accounts on 31st October showing they had just 2 employees.

As far as we know, this partnership hasn't generated any revenue yet. Indeed, it appears to be costing them money as they are sponsoring the "hackathon". When all this nonsense is over then it is likely we will be debating whether Triad is worth investing back at the bottom of its usual trading range at 30-40p/share in a few years’ time.

Small Caps Live Friday 5th November

Nichols (NICL.L) - Trading Update

This is known as the Vimto company, popular in the Middle East, but also:

Nichols plc is an international diversified soft drinks business with sales in over 73 countries, selling products in both the Still and Carbonate categories. The Group is home to the iconic Vimto brand which is popular in the UK and around the world, particularly in the Middle East and Africa. Other brands in its portfolio include SLUSH PUPPiE, Feel Good, Starslush, ICEE, Levi Roots and Sunkist.

Here's the meat of this week’s trading update:

Group revenue for the period was ahead of the Board's expectations, increasing by 17% year on year to £107m.

The Vimto brand has continued to deliver a strong performance across all of its markets. In the UK, Vimto brand value has increased by 4.5% YTD, according to Nielsen1. In Africa, the Middle East, Europe and the US the brand continued to see progress year on year, with International revenues increasing 36% versus the prior year. The Group's Out of Home ("OoH") route to market continues to recover from the impact of the pandemic and has seen growth of 29% year on year.

So, has anybody seen Vimto for sale in their local pub? Or restaurant? So presumably the OoH market is overwhelmingly overseas.

Cash generation has continued to be very positive through 2021 and despite the ongoing financial challenges posed by the pandemic, cash and cash equivalents at the end of the period were £55.6m (30 September 2020: £45.4m).

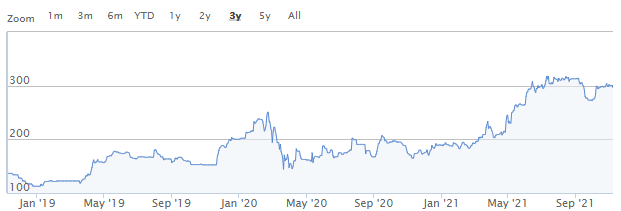

The market cap is £415m, so that's generous but not massive amounts of cash. Looking at that brand list it seems they might be in the market for more 3rd tier brands. The chart is interesting:

A rare stock that is trading below pre-covid levels. And it seems unlikely that covid has fundamentally changed their business for the worse.

The concern could be that this is known as a high sugar drink and this is unsustainable. However, they say that all their products are exempt from the Soft Drink Sugar Tax.

Since 2015, our sugar usage* has reduced by 36% despite our volume in litres growing by 34%, and on our flagship Vimto brand, No Added Sugar (NAS) commands a greater share of our overall brand sales, having moved from 33% to 52%. Within dilutes, we have seen an equally positive and significant shift, with the share of NAS products rising from 46.8% to 60.5% of sales**, while average calories per litre have fallen by 22% over the same period.

Our focus on consumer health extends to our international business. We launched a new NAS cordial in the Middle East. We’ve also reduced sugar levels in our carbonated products in a number of markets across Africa.

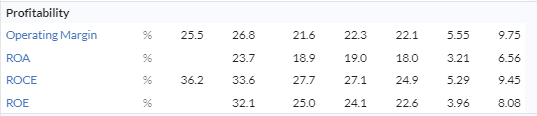

The argument here has always been that Nichols deserves a high rating due to its high ROCE. However, that ROCE is only high as long as earnings remain high, which they haven’t of late:

And ROCE is meaningless unless you can generate growth as high levels of incremental capital.

However, the outlook is good:

Although uncertainty remains regarding Q4 trading as a result of increasing Covid-19 infection rates in the UK, in light of the strong trading in the year to date the Board now believes that Adjusted Profit Before Tax ("Adjusted PBT")2 for FY21 will be ahead of the current market consensus3. The Board now anticipates that Adjusted PBT for FY21 will be in the range of £21m - £22m.

Whilst the Group's revenue momentum is expected to continue into 2022, the outlook for the next financial year is adversely impacted by inflationary pressures including logistics, labour and materials, therefore profit expectations for 2022 remain unchanged.

And broker N+1 Singer have updated forecasts:

Our current year PBT forecasts were conservatively pitched to reflect a degree of reopening/Covid caution.

They have only upgraded FY23 PBT by £2.2m though. So this doesn't sound like a growth company. Which leaves the P/E of 20 fairly inexplicable.

Smith News (SNWS.L) – Full Year Results

Smiths News reported full-year results yesterday, and they start off well:

Performance ahead of full year market expectations

Stockopedia had a 9.68p consensus so the 10.8p reported is an 11% beat:

With a historical P/E now under 4, this appears to be very cheap.

Despite the beat, the share price was largely flat yesterday, presumably due to concerns on cost inflation, where they say:

Recent inflationary pressures on distribution costs tempering expectations for FY2022

Usefully, they quantify these effects:

The situation is likely to be fluid for some months, hence we are monitoring the situation closely while seeking to make compensatory savings subject to maintaining our service KPIs. Currently, we estimate the impact on EBITDA in FY2022 to be in the region of £2m after mitigation.

Broker Edison don’t appear to have updated their forecasts to reflect this yet, but this is about 5% of EBITDA so not too significant.

As usual, though, the skeletons can be found in the balance sheet: a current ratio of just 0.83, and Negative Tangible Asset Value means that there is little downside protection here. Past mistakes, such as the takeover and subsequent sale of Tuffnells for a loss, plus a declining print industry have taken their toll.

Normally, we would stop any analysis there. However, there are reasons why this may be worth considering.

The first is that the debt appears to be reducing rapidly. Like Reach, they have been able to cut costs more rapidly than the decline in their revenue and use this cash flow to pay down debt. It only took a small change in the outlook for Reach, and a slowing in the decline of their revenue for the share price to go from 50p to the current 300p.

Although Reach is now net cash and Smiths still has debt, Reach has a very large pension deficit whereas Smiths has a pension surplus which they are in the process of being able to access:

The Company does not recognise the £14.8m pre-tax surplus, noted in the table above, as an asset, as it does not yet have an unconditional right to the asset…The surplus of circa £8m, is expected to be paid to the Company in November 2021. The surplus received by the Company will be used to repay existing debt.

So that is an £8m reduction in net debt that isn’t current on the balance sheet. Plus, some deferred consideration is due:

In addition to the repayment of the working capital loan in October 2020, the Company received a payment of £6.5m on 2 November 2021 in relation to the 1st instalment of deferred consideration arising from the sale of Tuffnells in May 2020. A further payment of £4.25m is scheduled to be received in August 2022, and a final settlement of £4.25m is due on the third anniversary of sale in May 2023.

Although presumably, these are already receivables in the balance sheet.

When assessing this sort of company, you can ignore the P/E ratio. Instead, Mark likes to calculate an earnings and free cash flow yield, i.e. Earnings/EV and FCF/EV, where the EV doesn’t just consider debt and cash as usual, but is also adjusted for negative working capital, net lease liabilities and any pension deficit. On this measure, Smiths are on a forward free-cashflow yield of around 15%, which is hard to find elsewhere in the current market.

Given that this is a “melting ice-cube” this may still be too expensive for some investors. However, Reach, in comparison, is on a FCF yield of around 6% by the same measure. Reach has a digital business but this is not necessarily valuable as a stand-alone business without the print side, and Smiths has a regional monopoly so it is not clear which is a better business overall.

However, whatever conclusion that investors come to on valuation, they would be wise limiting their position size, given the risks that the current balance sheet presents.

Gattaca (GATC.L) – Preliminary Results

Gattaca also reported FY results yesterday. These look poor, with almost all operating metrics down 20-40%:

Partly this is timing, with larger competitors such as Robert Walters who have reported to 30th June also showing NFI down 17% for the six month period. However, Robert Walters reported operating profit up 11%.

The Gattaca outlook is given as:

Notwithstanding evolving pandemic and macro supply chain factors, the business continues to trade in line with market expectations. We continue to invest to ensure sustainable growth over the long-term in our chosen markets.

Broker Equity Development forecasts that Net Fee Income will be 4.3% lower still in 2022. And, although the EBITDA is forecast to be almost 50% higher, this is presumably due to ongoing cost-cutting rather than top-line growth. Given that the share price has risen 275% in the last year, ongoing falls in NFI into 2022 are clearly not good enough.

The always bombastic Equity Development put a brave face on it, titling their note “Buoyant jobs market, bullish outlook” but the market was not convinced, and the share price reacted negatively to these results, down about 15% yesterday.

Gattaca retains a high cash balance. However, this will reduce going forward as the recovery draws in working capital. And at the balance sheet date, £7.1m of the cash was classified as restricted cash collected from customers relating to the non-recourse facility.

ED are forecasting around £17m net cash for FY22 and this to be the low-point in the cycle. With a £58m market cap this is not insignificant, and if you believe the Equity Development forecasts then a forward earnings yield of c.12% doesn’t look that expensive, even less so if you take ED forecasts further out. into the future.

We can see a couple of problems with this approach, though:

Cost-cutting is the least sustainable way of generating EBITDA growth, so the investment case requires trusting ED forecasts a long way into the future when top-line growth is forecast to return. Something which is rarely wise to do.

Larger & better run peers appear to be cheaper, according to Equity Development:

(Although this chart was created prior to yesterday’s fall.)

Even if you do trust the forecasts, ED have c.21p EPS forecast for 2023, which is close to the level they achieved in 2019. A year where they traded in a range between 100-150p/share. So, this has rarely traded as expensively as it does today, and that is on forecasts 2 years hence.

Although we are not particularly fans of the sector or the history of Gattaca, it is no denying that recruiters should be doing well in the current market, and if this continues its current share price trajectory below say £1, it would be worth a second look.

The Property Franchise Group (TPFG.L) - Trading Update

This is the first time we've seen an upcoming Mello event explicitly precipitate a trading update. They recently bought another estate agents brand, Hunters. Thus:

Group revenue increased 126% to £17.9m (2020: £7.9m)

34% like for like increase to £10.6m

These guys have presented a few times and always sounded interesting, but it was not something Leo was familiar with and so didn't look into further. He'd want to make sure he'd correctly modelled the fixed + variable franchise fees and natural attrition rates before considering an investment. But they have done very well share price-wise so far this year:

£100m market cap, so often a sweet spot where the market has liquidity, attracts smaller fund managers but is still potentially underfollowed. They have a nominal P/E of 12.5x. As a franchiser it is perhaps easier to justify competing with themselves:

EweMove sold 46 new territories (2020: 6)

EweMove had 161 territories under contract as of 30 September 2021 (2020: 116)

(We’re assuming that's a PurpleBricks-alike)

We try not to worry too much about macro, and Leo has been predicting property market falls for many years, but we still don't like the property exposure here. Anyway, there's an update from the broker:

We leave forecasts unchanged for now but note the upside risk, quality of earningsand attractive valuation i.e. trading on a CY21 PE of 12.8x, falling to 11.7x andyielding 3.7% rising to 4.2%.

So, unlike some of the other companies we have reviewed today, well worth a further look at the current valuation.

Gresham House Strategic (GHS.L) – Update

Gresham House Strategic is a listed investment trust we follow because it invests in a similar style to us – small cap, relatively concentrated and often value focussed. Of course, their ability to take strategic stakes is something we cannot do but otherwise, this is our sort of strategy. We have also chatted to their former manager, and now Escape Hunt CFO, Graham Bird, a number of times at investor events and he was highly knowledgeable about markets and companies.

What has gone on here has highlighted a couple of issues with listed micro-cap trusts. The first is that they are often hamstrung by their size – too small for the fees to be worth it to the manager unless they charge a high percentage, too large to trade in and out of small caps stocks, as Leo likes to do. The second is that the trust board is independent of the manager. So although this bears Gresham House’s name, there is no obligation for them to remain manager.

Due to these issues, plus perhaps illiquidity, this investment trust has traded at a discount to NAV for many years. Sometimes close to 30%. This led the trust board to initiate a strategic review, and in stepped Harwood Capital, offering to reduce management fees and add funds to scale up the trust. The board accepted this offer and gave notice to Gresham House…which they clearly didn’t like, since they were also a major shareholder in the trust. So tried to have the board removed.

A bun fight ensued, and an offer from Harwood to buy out Gresham House at NAV was rejected, and Gresham House preferred a run-off for all shareholders, as part of their belief in treating all shareholders equally. A run-off sells the assets in an orderly manner and returns the cash to shareholders.

The outcome appears to have been settled today:

Following the appointment of Harwood becoming unconditional, Harwood will be the Investment Manager and in the anticipated event of a change of Investing Policy, is expected to manage the run-off. The Company has received a conditional proposal from Harwood to waive its entitlement to management and performance fees during a run-off process of up to 24 months, provided that there is no early termination of its investment management agreement.

With a NAV as of 29th October of 1,881p and a share price of 1,820p, it would seem daft to buy the trust on such a low discount to NAV, given the runoff. Not only will you have to wait 24+months for all your money, but you can expect that given that these are micro-cap stocks in many cases then they will need to take a haircut to get them away. Some may be taken by Gresham House or Harwood Capital into other funds, but some will have to be placed at a discount.

Which brings us to the real investment idea. I’ve summarised their top 10 holdings, ex-Augean which has been taken over, plus 2 companies I already knew they held notifiable amounts in, to look for where the run-off may have the biggest impact. Look out for weakness in the following stocks where GHS holds a decent-sized stake – you may be able to get a bargain:

There are some interesting but very illiquid companies in there, and ones which we have analysed on SCL in the past. Often, where we have said we would own, at the right price.

That’s it for this week. Have a good weekend all!