Small Caps Live Weekly Summary

SSE DRAX CNA Evergrande RGD PGH FCAP DFS SCS

A reduced service this week I’m afraid since both Mark & Leo were away on (separate) holidays.

This meant lots of news we didn’t have time to look at in detail this week: Ebiquity (good, but perhaps no longer cheap, with a recovery already priced in), Eve Sleep (not good with EBITDA loss increased and cash balance being eroded), Centamin (geology update, with perhaps read-through to lots of extra work for Capital Ltd.), Warpaint London (Good but looking very fully priced at over 30x 22E P/E), Parity (bad), SDI (good, but looking very fully priced on 40x 23E P/E), Pennant (not great), SIG (very bad considering the industry they operate in), and Billington (not great).

Next week should be a bit more normal with Leo on the Mello BASH panel and Mark doing a book review on the same show, so be sure to catch that.

Wayne still held the live fort this week with Large Caps Live. Plus here’s the rest of the commentary that we found time to look at in between beach time…

Large Caps Live Monday 20th September

Power Companies

Given the news stories surrounding gas & electricity supply, I have been thinking about Drax, SSE, Centrica & Others. For instance, SSE has a lot of renewable energy assets.

BUT I have a problem. The problem I am having is trying to work out whether high electricity prices are a positive or a negative (ie have they committed at long term contracted prices, and on their gas power stations will they be making a loss).

Obviously, it will also depend on whether and how well they have hedged their inputs (ie gas etc). I was looking at SSE's investor presentation last night and saw that they had made a considerable amount from their hedges last year.

However, I am always wary of companies being 'hedged' because of specific issues:

a. in commodities there is always the 'force majeure' risk ie an unforeseen circumstance that means that your counterpart is unable to supply you what they have contracted to when they promised to

b. corporate treasury departments sometimes do stuff to screw up the hedge. An example is that eg they might buy a call at money for the hedge but then they SELL a call at 20% out of the money to reduce the cost of the hedge and because the commodity has never traded there before.

- that is if u are lucky

- and if you are unlucky and the graduate trainee is allowed to play then he works out that by selling TWO calls at 20% out the money it totally offsets the cost of the hedge at the money. And usually some accountant or other signs off on it.

- of course, if the spot then moves up 40% the firm is then SHORT a call - so any rises above that are loss-making!

So a big squeeze such as currently completely screws the firm

I am not saying any of the majors in the UK are doing this but it would not surprise me if we find at least one small player somewhere in the world whose hedges 'flip' signs during the extreme gas moves. Indeed I wonder if part of the gas 'squeeze' is because the amount available on 'spot' (ie not long term contracts) is actually small vs the overall size of the market.

And that brings us to the current issue of the UK electricity market - and indeed the gas market. A CEO on the radio (?Ecotricity) was moaning that the spread or margin that the electricity/gas service providers 'retailers' make is circa 2%. I thought that was disingenuous for a number of reasons:

1. Many of the small 'retail' power groups sell at a discounted price to attract customers

2. They do NOT make the major capital investments of the folks that own the power stations/wind farms etc so they can have potentially very high returns on capital with a 2% margin.

3. They screwed up by selling long duration (ie long term contracts - whether fixed-price or spot with cap) without securing their supply (ie output agreements) or hedging their inputs.

So for all the above reasons I am attracted to the bigger players such as SSE, Centrica, Drax.

Evergrande

The thing that has struck me in all of the Evergrande stuff is that some analysts/investors have ignored basic accounting and just focussed on if the Chinese govt will back Evergrande or not.

“How did you go bankrupt?” Bill asked. “Two ways,” Mike said. “Gradually, then suddenly.”

From Ernest Hemingway’s “The Sun Also Rises”.

So regarding Evergrande:

1. A company is not viable if it is not solvent ie its liabilities exceed its assets

2. But usually a bankruptcy is precipitated by liquidity

So I want to explore liquidity briefly:

- liquidity is the ability to pay your bills as they are presented

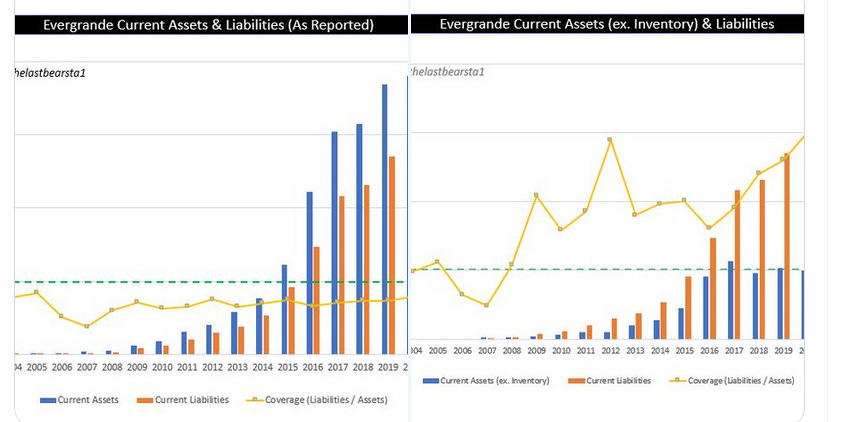

In the times of old accountants and investors were taught about the current ratio = current assets / current liabilities.

A great fallacy in the case of Evergrande was that inventory was assumed to be a current asset ie that it could be easily liquidated for cash. As anyone who has bought or sold a house will report - houses are not always easily sold - it can take months - or sometimes years unless u take a massive discount.

So a tweet by Alex Frey caught my attention where he looked at the current ratio removing the inventory:

I would recommend reading the whole thread but the key point is that Evergrande can only pay its bills if it liquidates a lot of inventory - ie its balance sheet as it stands is illiquid. An individual can sell an apartment at 30% below market for an immediate sale. However, if you own a million apartments or houses then it is hard to complete all of them to a finished state where they can be sold; and it is hard to maintain price discipline if you 'dump' them all on the market. This is before you even delve into the quality of the building and whether all the apartments could be completed for the costs that the company estimates and what the remediation costs will be.

In this thread:

The Last Bear Standing (who actually put the charts together) goes through a lot of other Chinese housebuilders again looking at current assets ex inventory vs current liabilities.

The key point is that a similar situation applies to a lot of other developers as well. So the next question is how big is the impact? Statista says that the real estate sector in 2019 was nearly 10% of China's GDP. But this FT Article from 2020 suggests it is closer to 25%. That the great and the good of Wall Street went to Beijing last week to meet officials tells us that they are concerned.

What I am thinking is:

1. If real estate is indeed 10 - 20% (let alone the 25% mentioned by the FT) of Chinese GDP

2. It is clear that MULTIPLE major property developers in China are facing LIQUIDITY crunches

3. That the supply chain for bulk commodities are already congested (see the shipping pic above)

4. Then it is not surprising that iron ore or other prices have fallen:

And so we get the major miners falling:

So what happens now? I think that the Chinese govt - via the banks will extend short term money. BUT it is clear that the quality of the balance sheets of the major developers is an issue - is the inventory really reflecting market prices? I suspect not. So I suspect many will be barely solvent - or frankly may be bust. So that then leads to what the govt does to resolve this.

But for us as UK investors the real questions are:

1. What are the exposures of the major UK miners - and frankly, I find it hard to believe that Chinese new property development in 2 years time will be as frenetic - so iron and copper demand globally will go down and hence prices

2. What are the implications for the major UK banks.

3. If I was trading FX I would also be wondering about the Australian Dollar (AUD) and whether to short it

4. There is a non-zero risk that some major intermediary in China fails to pay bills to someone else in the commodities supply chain. I have no idea what credit insurance is like in China. But any defaults leading to insurance companies getting burnt has implications for creditworthiness and the cost of trade going forward.

Certainly, one to be concerned about. Watch all the usual stress indicators because we have no idea where the risks reside

Small Caps (Not) Live

Real Good Food (RGD.L) - Final Results

Apart from a brief mention at the time of the last Downing letter, we last covered them here. Last week they had to extend their loan notes again, again, although it appeared that there was no additional fee, just a continuation of the 12% interest rate. This week we have final results.

Revenue from continuing businesses decreased by 9.5% to £37.3 million (2020: £41.2 million), in a year affected by covid-19.

Recall that a major product line is selling diet products to the overweight. This is of course a great business. However, the pandemic stopped face-to-face meetings at Weight Watchers which was a major sales route.

The Group delivered an adjusted underlying EBITDA* on continuing businesses of £0.2 million (2020: loss of £1.6 million), despite the impact of covid-19 on the continuing business.

The actual P&L is somehow missing from the financial highlights. Loss from continuing operations was actually £6m. However, there has been a genuine reduction in central costs and improvement from last year's result. It is confirmed that there are no redemption/extension fees on the loan notes any longer:

The Board renegotiated interest rates on convertible loan notes to a simple 12% per annum with effect from 1 January 2021, and in September 2021 extended the redemption dates to 2023.

We’d imagine the negotiation went something like this: "Look, you control the company anyway, why not make things simpler for all of us?". Last time we suggested that they only remained listed in order to leave the possibility of facilitating a debt for equity swap. However, now they say:

The Board remains focussed on reviewing all initiatives to continue to improve the capital structure of the Group; including the intention to delist the Group from AIM to save costs and provide greater agility and flexibility to maximise shareholder value.

There's actually some good news in there. Sure, delisting would be pretty disastrous for most equity holders, but the use of the word "shareholder" rather than "stakeholder" is quite pointed. It seems management insists there is some equity value left.

Leo previously said:

Traditionally debt ranks ahead of equity, with equity being wiped out first, but for expediency this isn't always the case.

Basically, he was arguing that the equity had some value because the shareholders’ vote means that they have leverage over debt holders. Unfortunately, the dreaded "stakeholders" word is mentioned later:

After a particularly challenging year in the period to 31 March 2021, where employees and all stakeholders have experienced situations never seen before, the Board wishes to thank all the Group's and businesses' stakeholders for their understanding and continued support.

That understanding included waivers and extensions by loan noteholders.

The Board is grateful for the continued support of all stakeholders who have shown confidence in the Group during the past year and will make every effort to retain the positive momentum which is now evident in the underlying business. The Board is confident in the future prospects of the Group.

Reiterating that the company's continued existence and going concern status is dependent on the loan noteholders. So, if the company is delisted what happens to shareholder leverage? That is not clear to us, but clearly, it is weakened and so this has to be the most important part of this statement.

Plans for delisting seem well progressed:

As stated at the time of announcing the sale of Brighter Foods Limited on 22 April 2021, the Board has been considering all options to save costs and to return shareholder value. At the AGM, the Independent Directors, with the support of the rest of the Board, will be proposing that the Company cancels the listing of the Company's shares on AIM. This will save approximately £150,000 a year in costs and provide greater agility and flexibility to maximise shareholder value. The volume of shares traded is very small and an AIM listing adds a disproportionate expense and burden on the Company. The Company has arranged for a matched bargain facility to be in place by JP Jenkins.

Out of academic interest, we'll talk about the business itself. They have sold the chocolate bars business, leaving just cake decorations. Despite the baking boom during the lockdown, this has somehow been affected by covid, possibly suggesting underlying weakness. But now:

Group revenues and profit are in line with Board expectations, and ahead of pre-pandemic levels (FY20), for the first five months of the new financial year, with good retail and international sales.

The business mostly seems to be about processing sugar. Therefore you might have thought this was worth a mention. But apparently not. The company fundamentally remains worthless and you can expect the share price to become more closely aligned to this reality shortly.

Personal Group (PGH.L) - H1 Results

Recall that this company's ability to make sales in its core hospital cash plan insurance business has been severely affected by not being able to hold face-to-face presentations in workplaces. Combined with natural attrition this has resulted in a declining recurring revenue book that will take years to recover.

They decide to lead on the most irrelevant number:

Group revenue rose 12.2% to £34.2m (2020: £30.4m), driven primarily by increased pass-through transactional spend via the Hapi platform of £13.4m (2020: £8.5m);

The margins are so low on much of the Hapi revenue that they really need to come up with an alternative revenue metric that excludes it.

Adjusted EBITDA* declined 17.7% to £4.1m as anticipated (2020: £5.0m), reflecting the change in revenue mix driven by Covid-19 related restrictions on face-to-face insurance sales over the last 18 months;

There we go.

Here's some detail on the core, highly profitable business:

Premium income declined to £12.5m, and the number of policies reduced to 236,000 as at 30 June 2021, as expected, primarily a result of the restrictions placed on face-to-face meetings.

Outlook:

However, with the resumption of face-to-face, the Insurance benefits business has reached an inflection point and from July we have started to see growth in our policyholder numbers. We expect the re-building of our insurance book to continue into the second half and into 2022.

Going into the period the number of policies in force was 260,468, down from 288,134 a year before. This resulted in a drop in gross premiums written from £15.1m to £12.8m with a claims ratio of around 23% and so a drop of £1.8m in gross profit. Given that policies were down to 236k entering H2, it can be seen that the H2 performance in the core business will be significantly worse still.

However, this should be the low point. This is why full-year adjusted EBITDA forecasts are £6.0m vs £4.1m in H1, and adjusted EPS is forecast at just 11.9p. The key bull point here is that they have signed up several large employers that have agreed for them to sell to their staff. This gives them a much greater pool of potential policyholders. Furthermore, a greater proportion of these employers are back on site compared to the economy as a whole due to the white-collar, large organisation bias.

However, even in the best case, 2019 EPS levels of 25p are unlikely to be achieved before 2024 (well, H2 2023 + H1 2024), making the current share price of over 300p difficult to justify to anyone.

finnCap (FCAP.L) - AGM Trading Statement

Leo did a pre-AGM statement write up of his analysis of finnCap on his blog. Both Mark & Leo had been concerned that a lack of obvious IPO & placing deals RNSed would lead to weakness in the ECM part of the business. M&A was likely to be strong but how strong was the big question. Indeed, the market was probably worried about this too, hence the weakness in the share price going into this week’s statement.

As it was we needn’t have been worried, at least about H1 performance:

In July, we reported that Q1 revenue was ahead of the prior year with a strong pipeline and balance sheet and that the directors expected revenue to be between £40m and £50m for FY22. Trading since then has been strong and our overall revenue trend is currently slightly above the top end of these full year revenue expectations with significant, incremental M&A deals with the potential to close before the end of the half year.

Looks like the less transparent Cavendish M&A Advisory has saved the day:

In finnCap Capital Markets, although our equity capital markets activity is a little lower than in H1 21, we have completed a significant number of equity transactions as institutions continue to support strong business cases and we have seen a good contribution from both debt advisory and the initial launch of finnCap Analytics. finnCap Cavendish has benefited from the continued and vigorous M&A market we saw towards the end of FY21 and its performance is well ahead of the same period last year.

That they are cash-generative and cash-rich is good to hear but should not surprise anyone:

Our cash position has further improved and is ahead of our position at Q1 (£17.2m), after payment of our £1.65m dividend to shareholders in August.

On the outlook they say:

Our pipeline remains solid and we are confident that this, combined with our performance to date, underpins our confidence in delivering a result within our full year expected revenue range.

At, say, £52m revenue, EPS is probably around 5.2p. However, broker Progressive have not upgraded and retained a £44m revenue estimate and 3.9p EPS forecast, saying:

…a reminder of how the pattern of reported revenue from finnCap Cavendish can sometimes reflect a smaller number of large deals which complete in a particular reporting period. Hence, despite the very encouraging update, we are maintaining our estimates at present.

Perhaps reflecting the inherent uncertainty and timing of potential revenue-generating deals. Delivery of a couple of IPO’s soon that they have spoken about in the past would give greater confidence that they will hit or exceed FY expectations. Still, anywhere close to FY expectations is very cheap on an earnings basis, and it comes with an underlying long-term growth story attached.

DFS (DFS.L) - Preliminary Results

DFS’s preliminary results with a trading update provided a good read-across to SCS, which looks compelling value compared to DFS on pretty much every metric.

As detailed in our year end trading statement, strong customer demand in the final quarter of FY21 was already expected to underpin revenues and profits in the first half of FY22. Order intake has also remained strong in the current financial year to date, well ahead of our previous scenario of +7% growth on FY19, resulting in an order bank that continues to grow and which in absolute terms is very significantly ahead of normal levels. This order intake provides significant resilience, and confidence in our outlook. However the constraining factor on our reported short-term financial performance will be our pace of conversion of the order bank, which depends on both our supplier partner manufacturing capacity and also the capacity of our proprietary logistics operations. We believe the Group is well placed to achieve the medium scenario of our range of FY22 profit outcomes identified back in June.

The number 1 metric for DFS / ScS is order intake. They get very few cancellations and so almost all will convert to revenue further down the line. These are chickens you can count. What could go wrong for either of them is if customers no longer are willing to put up with extended delivery times, and the main reason this would happen is if a competitor starts out-competing them in this regard.

We already have increased output capacity significantly in FY21. We continue to strengthen our operations, increasing warehouse capacity and resourcing levels, to meet customer demand. Notwithstanding this, it should be recognised that the short-term operational environment continues to be exceptionally uncertain and difficult, given well-reported logistics disruption, cost inflation pressures and unplanned Covid absences. We believe that we have the right plans in place to mitigate these impacts, underpinned by our scale, operating experience and long-standing relationships, and we are focused on delivering good customer service, protecting our colleagues and creating long-term value.

So any concerns SCS investors may be having over supply constraints don’t seem to be an isolated issue, which is good news…of sorts.

That’s it from the sun, have a great weekend all!