Small Caps Live Weekly Summary

Banks JOUL FCAP WIX TND MPAC DFS PMP BKS ITX

Markets continue to be challenging, with early optimism this week quickly extinguished by the US CPI reading running hot. One factor many investors forget when assessing UK stocks is that many have US dollar earnings. With the pound only buying $1.14 at the moment, those dollar earnings and dividends are worth a lot more than at the start of the year. But such companies have often de-rated as much as everything else. This really is a stockpicker’s market.

Large Caps Live

I was interested to hear that individuals on discord talking about banks offering them cheap money. Some of the companies I have been talking to have had real difficulty speaking to banks. I don't know why but we seem to have lost what used to be called 'trade banks, ' i.e. banks that would help finance international trade. I guess the one bank that still does a lot of that is HSBC, but it really is hard to raise trade/working capital finance for a small business right now.

I was also helping the CFO of a small company raise funds for an acquisition. In this case, they eventually got one of the big banks to finance it, but it was a close call. The attractive aspect was that the acquisition contained enough cash to fund the deal, but it would take some time to assimilate and extract - but very hard to even get bankers to listen.

As background, I have spent the last few weeks rewatching The Big Short and rereading the book of the same name, and some things caught my attention regarding the situation at the time:

(1) A background of rapid property rises

(2) A lot of mortgages at or above 100%

(3) A lot of unverified income/lack of credit checks

(4) A lot of NINJA loans, ie no income, no job, no assets

(5) A lot of securitisation, so no long-term commitment to the loans.

(6) A lot of loans are through intermediaries, ie not the originating bank itself

(7) A lot of property bought for rental

(8) A lot of second mortgages (in the US, they were called equity loans or home equity lines of credit HELOC)

(9) A lot of mortgages on 2 - 5 year teaser rates before switching to variable rates (remember in the US, the background was historically that there were a lot of fixed rate long term loans, but from about 2001 there was a big push to ARMs - adjustable rate mortgages).

(10) There were some extremes, eg negative amortising loans

(11) A significant number of INTEREST ONLY loans

So with that lens, I have been looking at the UK market, and a couple of things struck me. Firstly, let me say that we do not hit all the above items in my checklist. But the more interesting question in many ways is what is NOT disclosed. And what we focus on in the UK. Many will have heard the term 'prime' or 'subprime'. In the US, it generally applies to your FICO score. FICO - Fair Issac Corporation - is a consumer credit scoring system. The rule of thumb is:

Category FICO Score

Prime 660 - 719

Near prime 620 - 659

Subprime 580 - 619

Deep subprime Below 580

So in the US, it is possible to look at the average FICO score of a loan book and decide if it is prime, subprime etc. As this is a credit score, it means that it gives an indication of the ABILITY to pay the monthly payments. In the UK, we do not seem to have a nationally consistent credit scoring system. At least no UK banks, as far as I can see, have details of the credit scores of their customers. We are asked to take it on 'trust'.

The banks in the UK focus on LTV - loan to value. The point about LTV is that it does not tell you the chance of default - only the loss-given default. Most banks estimate the probability of default (PD) - we will come onto scenarios and modelling in a bit.

But LTVs are made up. That is a bit radical so let me be more precise. New LTV are probably fairly accurate - after all, someone has just bought a house. But older mortgages have made up LTVs. The reason I say that is that the banks undertake a 'paper' or 'desk-based' exercise every quarter or half year or so where they look at all the houses they have lent against and estimate what the current price is using the HPI (house price index).

This is where it gets really interesting - some banks seem to do it quarterly. I think some do it half-yearly. Most are vague or do not disclose. I think one bank might do it yearly.

There are also likely to be issues with Buy to Let going forward:

(1) Section 24 - this came into force in the tax year starting April 2021 - so for the year ended April 2022, and I suspect some landlords are hence only just realising as they face their annual tax bill. This is the change in tax rules meaning that interest cannot be fully offset vs tax. (To be fair, it was being phased in from 2017).

(2) EPC - my understanding is that all rented property has to have an energy performance certificate, but from this year, the level at which the property EPC has to be in order to rent has increased.

(3) A lot of landlords had difficulties during Covid - rents fell, and they were now recovering. But a lot have withdrawn from the market - stories of 30 - 100 people trying to view a property for rent in London and gazumping due to shortage of supply.

(4) A lot of BTL property is financed via INTEREST ONLY loans - sometimes with a 2 - 5 year fix but often then variable rate.

(5) There are also various fire/smoke and electrical wiring upgrades that have been required or are being required, especially for HMOs, ie houses in multiple occupation.

(6) Added afterwards - stamp duty increases for BTL and higher CGT

Bank disclosure can also leave something to be desired. In the case of one major bank, so far, I cannot work out how much of its loans are Interest-only. And I think some banks are obfuscating BTL / Interest only / Retail BTL and commercial BTL. As far as I can tell, no UK bank discloses the split between mortgages distributed via its own network and those distributed via intermediaries - or whether the lifetime experience is different between the two categories. My suspicion is that we are going to find that intermediary distributed mortgages are going to be higher risk / higher defaults.

There are some technical details that some may find worrying too. For example, IFRS 9 requires banks to consider a mortgage in default when the customer has not paid for 90 days which seems pretty reasonable. Lloyds appears to have decided that it does not apply to them, and instead, they have decided to use 180 days. In a 'severe' downside scenario, Lloyds expects GDP still to grow! Their base rate assumptions also look optimistic, given the current trajectory.

In their Annual Report, Natwest appears to say they have ignored the conservative nature of the Basel 3 models and, in their wholesale business, not bothered with any downturn assumptions. Natwest 'thinks' that in a severe downside scenario, house prices will fall 20.4%, but GDP will fall 'only' 3.6%, which seems light. In a milder downside scenario, house prices will fall only 2.9%.

Despite all this, I am becoming increasingly convinced that there is value in the major banks since they will be major beneficiaries from rising interest rates.

However, I am also becoming increasingly certain that they will have to increase their provisioning - the question in my mind is whether that is in calendar 2022 or calendar 2023. The key parameter to watch is the HPI (House Price Index) - as if house prices fall, then the value of houses clearly falls, which impacts the LTV of bank loans. That, in turn, means that banks’ regulatory capital requirements increase.

Because of these factors, I think that dividends will not initially follow underlying earnings. In fact, I would take it further and be very wary of any bank that increases dividends significantly faster than underlying earnings at the moment. I think reading every word of the filings will become really important in 2023 - I appreciate that due to the delays in annual reports coming out, it is retrospective, but I am also convinced that even some of the more 'respectable' large banks have and are doing things on the edge that have historically made their numbers look a tad better than they really are.

Small Caps

Joules (JOUL.L) - Business Update

Next choose not to invest:

Joules confirms that discussions about Next plc acquiring an equity stake in the Group have ceased, however discussions regarding Joules potentially adopting the Next Total Platform in the future will remain ongoing.

This article reports that Next was unable to respond to the trading downturn because they'd promised a minimum price leaving the only option to walk away.

There must be a material risk of insolvency at this point. Founder Tom Joule is coming in to try to avoid that:

Jonathon Brown, the Group's new CEO with effect from today, is pleased to announce that Tom Joule, the Company's founder and a Non-Executive Director of the Group, will lead, in an executive capacity, the Company's renewed product development process for the forthcoming seasons to oversee the Company's product offer and to ensure it surprises and delights our customers.

They flag the potential for an equity raise:

The Group continues to assess its ongoing financing requirements and is considering alternative options, including a possible equity raise, to allow the Company to strengthen its balance sheet.

At this point, it will surely be a deeply discounted rights issue and will require Tom Joule to stump up his share, or they won’t get it away. Expect a share consolidation, too, to try to avoid the embarrassment of a single-digit pence share price.

This is now only worth considering after the rights issue is complete since the share price is likely to trade down to whatever level that gets done at. Anyone interested can then buy in the market at the same price with much-reduced risk.

finnCap (FCAP.L) - AGM Statement

Trading has been in line with the expectations set out at the time of our final results in July.

It is not a high hurdle to be in line with the RNSed outlook with the July results, which summarised:

As a result of market conditions, we expect revenue and financial performance to be substantially lower than in FY22.

And there are no broker forecasts, but they guide:

Overall, revenue to 31 August 2022 was approximately 30% lower than the comparable period in FY22 - our record year

Furthermore, they expect things to improve:

The outlook for the remainder of the financial year is for a somewhat better revenue performance in H2 than in H1 of the current financial year

The pattern of trading with strong M&A and weak ECM is as expected, but here there is a positive slant:

ECM revenue is marginally ahead of our expectation in July but, as expected, substantially lower than last year.

Our preference for brokers with a large M&A component has been the right call in the current market, although it hasn’t been reflected in the share prices. At 2022 revenue levels, 75% of costs were variable staff costs linked pretty much directly to revenue. So a 30% fall in revenue does not result in a loss, even given higher fixed costs. Indeed, 23H1 is looking a bit better than 22H2, which was 35% down on 22H1, and they made a good profit then. And they are guiding H2 to be better still. So potentially, they can maintain profitability through the cycle.

The Group's balance sheet remains strong with cash on 31 August 2022 at £13.1m

This is 7p/share. However, from the last annual report:

Our liquidity objective is to hold more than £10m free cash after taking account of market making funding together with expected dividends, financial and capital commitments, corporation tax liabilities and employee discretionary bonuses.

So unlikely to be much headroom there for any additional distribution to shareholders.

We are also disappointed there have been no presentations from management. A lot has happened recently, and it would be good to hear their perspective on it. It’s like they don’t follow the advice they would give to clients regarding shareholder communication themselves!

Wickes(WIX.L) - Interim Results

These read well. At least in the current context.

Revenue growth of 1.3% to £822.3m (H1 2021 £812.0m) against strong prior year comparatives

Further market share gains in Core[1], and a strong recovery in delivered DIFM sales

Like for Like (‘LFL’)[2] sales up 0.8%, and 23.4% on a three-year basis

Adjusted profit before tax £45.6m (H1 2021 £46.5m)

And the all-important outlook:

As guided in our 26 July trading update, we have seen a recent softening of the DIY market from the very high levels of demand experienced during the pandemic. While the macroeconomic environment remains uncertain, we are confident that we have the right model to continue outperforming the market. We reaffirm our guidance for full year adjusted PBT in the range of £72 - 82m.

This is good news and doesn’t really line up with a 30% share price fall in the last 3 months and a forward P/E of 5, making this look very good value, even in the current markets.

A confident presentation from the company shows that cost savings have largely offset the inflationary impact:

They say there is no pressure to pay increased rents, and rates are also fixed at the moment. Store wages are up +6.6% in line with NMW but offset by some flexibility in store hours. Overall cost increase 3% vs 15% for product cost increase which they pass through on a cash basis. This has a slight negative impact on gross margins but is neutral overall.

The dividend held and will be higher than the 40% payout target in the near term.

So no room for buybacks but an 8.6% forward yield. Their debt is all lease liabilities. Positive working capital will reverse in H2, as is the seasonal norm. Non-underlying costs will remain a small impact in H2 but negligible in 2023.

Overall the balance sheet remains strong and they are confident of outperforming their core market.

Tandem (TND.L) - Half-Year Results

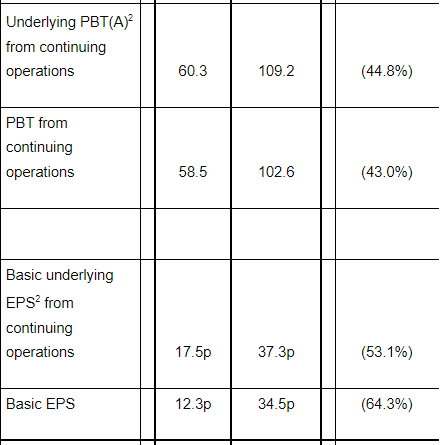

After an exceptional 2021, sales have fallen:

Group revenue in the six months to 30 June 2022 of £12.9 million (H1 2021: £19.3 million)

And profits plummeted:

· Profit before taxation of £0.3 million (H1 2021: £1.9 million)

· Basic earnings per share of 5.8 pence (H1 2021: 31.2 pence per share)

The outlook is in line:

· As a result of management actions taken, profit after tax for the full year ending 31 December 2022 remains in line with market expectations.

However, the 2022 forecasts were recently slashed from 77.6p last year to 56.7p earlier this year and now to 22.2p EPS.

The company has now moved into a net debt position, investing in a new warehouse:

· Net debt after borrowings as at 30 June 2022 of £1.5 million

The share price fell initially on these weaker prospects but bounced quite strongly. Helped by illiquidity and a bit of an entrenched private investor fanbase.

However, on a forward P/E of 13, they are not exactly cheap. This is double the rating of Halfords, which is also exposed to the cycling and e-mobility trends. Halfords is also much more liquid and pays a higher dividend. In reality, investors should demand a big discount to hold the more illiquid and risky Tandem.

MPAC (MPAC.L) - FREYR Framework Agreement

…initial three-year period, for the exclusive supply of the casting and unit cell assembly equipment to the battery cell production line at FREYR's Giga Arctic factory in Norway.

No contract size is given. Three years suggests a longer ramp-up time for the factory than Leo previously envisaged. However, exclusive is the big news. Some other agreements suggested the work might be carved up more than at the QCP, but the wording "casting and unit cell assembly" is identical to that for the QCP. As well as the possibility that the different parts could have been split, the plant is big enough that dual-sourcing would have been a possible option, albeit at a not inconsiderable cost in terms of space and cost.

I am excited about the opportunity to establish Mpac as a market leading provider of automation equipment to the clean energy sector and to support FREYR in achieving their ambitious growth plans for a more sustainable future.

The "and" emphasises there are other customers to be won.

Our collaboration began with our CQP, where we learned that our two companies are well-aligned in our ambitions for speed and scale in producing clean and sustainable battery solutions.

Suggesting scope to win contracts for future FREYR factories. The only note of caution here is that, to some extent, there was already an option agreement in place for the gigafactory as you can see from the redacted contract for the QCP. So you could argue that little has changed with this announcement. But in reality, a lot has changed: Plant 1 was delayed, then Plants 1 & 2 were combined and more recently increased in size by 2.5x. The QCP is also significantly behind schedule, and although it is not clear they were on the critical path, potentially, this was related to issues affecting MPAC.

Equity Development has a new note out. MPAC has guided no upgrades to 2022 or 2023 forecasts, which seems strange as we would expect material revenues in 2023. As this is just a framework agreement, we would not expect the up-front signing fee they received from the QCP contract. Relatively small final payments for the QCP are likely already included in the 2022 estimates but could fall into 2023. For 2024 they say:

At this stage our outlook to FY24 remains unchanged, but we are sensitive to updates in this rapidly developing addition to Mpacs core markets.

They do, however, add:

As indicated by the 3-year agreement announced today, Mpac will seek long-term partnerships in this rapidly-growing segment of the clean energy sector, using its expertise to add production (and battery-size) scale, and with this achieve cost reductions for its clients

Leo now estimates a greater than 50% chance of gaining a contract for another FREYR factory and/or another 24M licensee. However, significant revenue from such contracts would come too far in the future to materially affect his NPV for MPAC at the discount rates he feels are appropriate.

DFD (DFS.L) - Preliminary Results

Most profit measures are down 50% or so:

Net bank debt is up to £90m, and this is on top of £192m of negative working capital. Yet management seems to think they are in a great position:

Board proposes to extend the current £25m share buyback programme by a further £10m and declare a final dividend of 3.7 pence per share for FY22. Following commencement of the Group's special capital return programme, over £75m of excess capital is to be returned to shareholders through ordinary and special distributions in calendar year 2022.

This appears to be foolhardiness. This is pretty much the worst balance sheet we have ever seen, with a current ratio of 0.32! If sales drop, they will bleed cash.

Good job there is no sign of clouds:

In the fourth quarter of FY22 and first quarter of FY23, order volumes for the Group softened markedly relative to pre-pandemic levels, reflecting a trend seen widely across the furniture industry. The macroeconomic environment remains challenging, given the potential effects of the current high-inflationary environment on consumer behaviour.

Oh dear ⛈️

The adjusted P/E is 15.6 even after the 10% fall in share price in response to these results. Just seems bonkers to us.

Portmerion (PMP.L) - Interim Results

These read well:

· Record H1 Group revenue of £45.5 million, an increase of 5% over the prior year (H1 2021: £43.1 million).

· Group sales 30% ahead of pre-pandemic 2019 levels demonstrating significant expansion in our customer base.

· Headline profit before tax1 grew by 30% to £2.0 million (H1 2021: £1.5 million).

And this sounds positive:

Expectation of sales to be at least in line with record sales year in 2021, with profit also ahead of the prior year.

Until you realise that forecasts were for EPS to rise from 27p last year to 57p, and they say:

the ongoing impact of input cost inflation and labour market disruption is more significant than previously forecast

They have largely hedged energy prices out into 2024, but labour and transport costs are a lot harder to hedge.

Their broker, Singer, has now lowered forecasts to 44.5p for FY22 with 52.0p for FY23 and 62.1p for FY24. That is a forward P/E of around 10 after adjusting for debt and pension deficit. Not that bad for a company with strong IP and may be attractive to investors who look through the current challenges. Perhaps the only issue, however, is that other high-end consumer IP-type companies may well be significantly cheaper. Sanderson Design, for example, is on an adjusted forward P/E of 5.7 (if they hit their figures). In this market, everything is relative.

Beeks Financial Cloud (BKS.L) - Product Launch

Following the successful completion of the significantly oversubscribed fundraise in April 2022 to accelerate development of Beeks' offering, Exchange Cloud is now formally launched, with a major equities exchange already under contract to deploy later this year. Additional proof of concept implementations and discussions are underway with potential customers.

So apparently, ICE moved from "proof of concept implementations and discussions" to a signed contract in 3 months, during much of which the financial world was on holiday. However, what happened to that "major equities exchange already under contract"? We don't think just because the data side is part of a group that owns NYSE, that equates to them being a major equities exchange.

However, it does raise the possibility/probability that the originally intended first customer was the NYSE, and this contract will still come to pass at some point. That would be an outstanding reference customer. On to the trading update part:

Beeks has delivered a record trading performance in the year, delivering growth on the prior year and in line with upwardly revised market expectations.

However, no actual revenue figures are given despite the period end being two months ago. Rather they say:

The Group has exited the year with Annualised Committed Monthly Recurring Revenue of over £19.3m, growth of 40% on the prior year, providing a strong basis for further growth in FY23.

The £19.3m annualised in presumably the best month doesn't seem particularly high compared to forecasts of around £19.0m for the whole year. But it does seem supportive of forecasts for around £25m in 2023 (current period).

The shares look very expensive on conventional metrics, and investors need to be aware of the very high capital intensity, but there is significant strategic intangible value in their technology, reputation and customer relationships that should help business performance from here. At 65x Forward Earnings, sooner or later, this potential needs to appear in the financial results, not just the management commentary.

Itaconix (ITX.L) - Half Year Results

First half revenues of $3.1 million were 124% higher than the first half of 2021, 148% higher than the second half of 2021, and 40% higher than our prior record half-year revenues of $2.2 million in the second half of 2020.

But, here's the reminder of why this isn't a particularly good business:

Gross profit margin was 25% compared to 27% for the full year of 2021 This slight decline in gross profit margin was due to a higher percentage of revenues from large detergent customers and price support for two large customers.

25% is not a good gross margin given the nature of the product and the R&D that was required to get them to this point. "price support" means they were forced to cut prices by a customer that was far bigger than them. They are still loss-making, even on the most optimistic of measures:

Adjusted EBITDA1 was a loss of $0.6 million, compared to a loss of $0.7 million for the first half of 2021 and a loss of $0.9 million for the second half of 2021

They'd like you to think that they could have made an (adjusted EBITDA) profit if they had chosen to:

...including continued investment spending on major new revenue opportunities.

But surely they would have preserved cash if not spending was an option since:

Cash and Cash Equivalents as at 30 June 2022 was $0.9 million, compared to $0.7 million as at 31 December 2021.

So looks like they'll be gone in six months. Which leads to the question of how they survived the previous six?

In April 2022, the Company completed an equity raise with gross proceeds of $0.4 million for working capital, predominantly to strengthen finished goods inventories held in the EU to assure reliable and ready delivery times to EU customers.

So did they strengthen finished goods inventories in the EU?

We don't know, as there's no inventory breakdown at H1, let alone by region, but it looks like, rather than using the fundraise to increase inventories, they used it together with decreasing inventories to fund ongoing losses. History may suggest that they can repeat the fundraising trick every year indefinitely, but surely decreasing inventories is unsustainable.

So what's gone wrong? Leo read the full report, and they admit to nothing, however:

Adjusted EBITDA1 loss for full year 2022 is expected to be an improvement on 2021, but below previous market expectations, reflecting continued investment in the growth of the business.

As per above, they lost $0.7m in 21H1 and $0.9m in 21H2, they've lost $0.6m so far this year, so presumably, the loss will be around $1.2m. Without further tightening of working capital (as well as the inventories, they also increased payables ahead of receivables in H1) this means they will run out of cash. So "supportive shareholders" are key here.

Sometimes the going concern statement discusses support from shareholders, letters of intent, and that kind of thing. But not here. Naturally, there was a material uncertainty over going concern, but accounts were prepared as a going concern noting that:

the success of the business is dependent on customer adoption of our products in order to increase revenue and profit growth

Perhaps the auditors asked major shareholders, and they were not supportive!

That’s all for this week, have a great long weekend. RIP HM The Queen.

I do hope Joules turn it around, there is a market for this type of store and clothing which appeals very much to the lower middle class aspirational crowd along with an upper middle class crowd.