Small Caps Live Weekly Summary

CARD PMP DBOX HFD BWNG DSM MORE MRK NANO XAR RCH

Risk is back baby! After a torrid 2022 for many UK small cap investors, 2023 has started with a bang. Lots of small caps are bouncing, not on news, but simply because they appear oversold. As is often the case, companies can remain unloved for months, but once they start moving, investors get FOMO and start to buy simply because others are buying. This effect will be magnified by investors holding above-average cash holdings during the downturn.

A case in point is one of the companies we discuss most on SCL: Capital Limited (CAPD.L). One of the commonly quoted bear points is that the share price often fails to respond to good news or broker upgrades. However, this week the shares hit an all-time high with decent volume, on no news and no broker upgrades:

Sometimes you simply have to be in it to win it.

Small Caps

Card Factory (CARD.L) - Trading ahead of expectations; good momentum

A good trading update from Card Factory as the rampy headline suggests:

The Board believes that EBITDA for FY23 will be at least £106 million versus current consensus of £96.9 million. This EBITDA would approximate to PBT of around £48 million. The Board is encouraged by the strong trading momentum and remains confident in the long-term prospects of the business.

This is mirroring a lot of what we are seeing in retail - that consumers are either trading up or down. Being a value retailer, Card Factory has benefitted from these trends.

The reaction to this update was quite muted, though. This suggests that the share price had already got a bit ahead of itself. The share price is at recent highs:

Yet forecasts remain significantly below where they were 18 months ago:

Given the share price momentum, we can see why some may not be in a rush to sell. However, history suggests that there will be much better buying opportunities in he future.

Portmeirion (PMP.L) - Trading Update

Portmerion start the year with a beat:

We are pleased to report a strong Christmas trading period with robust demand across our portfolio of consumer goods brands. As a result, FY22 sales are now expected to be at least £110 million, 4% ahead of 2021 and 4% ahead of consensus market expectations. Group sales are now 18% above pre-Covid 2019 levels.

Part of this they say is due to FX:

The sales outperformance benefits from the retranslation of US dollar sales at a lower rate (which benefits revenue but not profitability) and also a stronger than expected seasonal trading performance in our US market and continued momentum in South Korea.

Although we are a bit confused. Clearly, the exchange rate helped compared to expectations a year ago, but not in the last three months:

So compared to the (downgraded) FY guidance given with the H1 results, this looks like a small beat as only the "seasonal trading performance in our US market and continued momentum in South Korea." has occurred since.

However, we don't know what margin was obtained and the high inventories at H1 give cause for concern both for these and cash conversion. They imply they were up but only really comment on future margins:

We expect to improve operating margins further in 2023 through ongoing implementation of operational efficiencies, driving operating margin towards our longer-term target of more than 13%.

Also, they fail to comment on the pension deficit. The position was potentially slightly better at H1, suggesting it may have improved further, but you can't be sure about these things.

Broker Singer report that FY PBT expectations are unchanged.:

The main headline message is a £4m revenue beat (c.4%) vs consensus, resulting in £110m of sales (+4% y/y). Around 40% of the beat was FX related (strong $ vs £)

As you can see from the exchange rate graph above, since the date of the last update the dollar has been weaker so this is innumerate nonsense, rather undermines credibility, and suggests that previous guidance assumed an exchange rate other than the then-current one.

Singers again:

We understand almost half of the revenue beat was offset by FX transactional costs and the balance at c.45% GM absorbed by cost inflation.

The argument for a much higher valuation at Portmeirion has recently been increased margins, but they have consistently disappointed here. And they do not have the excuse of energy rising prices - at H1, they said:

Long term energy hedge until Q1/2024 continues to insulate the Group against ongoing volatility in energy prices.

Prices are currently falling rapidly and so there may be opportunities to extend these over the next year.

Although the company talks about strong momentum, Singers comment:

Given the Group generates 60% of PBT in H2 we feel it is far too early in the year to be adjusting our FY23 PBT forecast.

All in all, a bit of a non-update. However, we think the real story is this:

Does that graph fairly reflect the changing prospects for the group? There was a 20% multi-year EPS downgrade in September, but things now seem to have fully stabilised. Much of the worst in terms of potential energy costs and consumer spending seems to be over. Singer argues:

A lowly rating of 6x P/E, 4x EV/EBITDA and a 5% yield is in deep value territory given future earnings potential. Today’s update should go some way to reassure investors.

As before, we suggest adjusting EV for 3x annual pension payments of £0.9m. But apart from that, this seems a fair assessment. And it is this that has caused the 20% rise in the share price.

One of the arguments for not holding Portmerion is that Sanderson Design serves a very similar high-end market and has appeared materially cheaper for some time despite Portmerion halving in the last year. That gap has narrowed somewhat recently. Although it may widen again if Sanderson delivers a similar beat against expectations.

Digitalbox (DBOX.L) - FY2022 Trading Update

This update starts off very bullish:

Despite the challenging conditions across the entire media industry in Q4 2022 - traditionally the Company's most important trading period - management action ensured the Company continued to deliver very strong margins. As a result, Digitalbox expects EBITDA* for the year ended 31 December 2022 to be comfortably ahead of the £1m delivered in 2021

But appears to have been written by the satirical daily mash team since it is ultimately a mild profits warning:

…broadly in line with the most recent market guidance, despite the economic headwinds resulting in revenue below market expectations.

Then they quote gross cash of £2.8m which is of course, meaningless if no net cash figure is also quoted. This is in line with the figure at H1, so the assumption could be a similar net cash figure or about a quarter of the market cap.

They did a small acquisition in the period, but no figures were given, and with only £170k revenue acquired, it suggests they paid very little. Perhaps the best that can be said for H2, then is that they didn’t lose money. Not exactly the most attractive investment proposition!

Halfords (HFD.L) - Q3 Trading Update

Halfords report reasonable revenue growth figures in current markets:

Group revenue grew +38.3% and +12.6% LFL vs FY20 (+21.7%, +4.6% LFL vs FY22) reflecting strong sales in Motoring and needs-based categories, but overall revenues were impacted by softer than expected cycling and tyre markets

However, ultimately this is another cut in the profitability guidance range:

As a result of these revisions to our forecast, we are reducing our FY23 underlying profit before tax (“PBT”) guidance to £50m to £60m.

With cycling being one of the weak areas, there is a possible read-through to Tandem, who are much more exposed to cycling sales as a percentage of revenue.

Tyres may be customers delaying changes, or trading down the brands, although it seems labour shortages are an issue:

…the labour market remains very challenging, and we have been unable to recruit enough skilled technicians in our Autocentres business which we now expect will limit growth of higher margin sales during the important upcoming Q4 MOT peak.

The outlook is all about uncertainty:

As we look to FY24, it remains particularly difficult forecasting with any certainty.

Which brokers have interpreted as a similar level to the revised 2023 estimates:

Understandably the market didn’t like this with the shares trading down 20% on the day. This is still only a forward P/E of 8, however, and this appears to support the price, somewhat. The last time Halfords downgraded their profits estimate the share price regained its fall within a day or so. It may well take a bit longer this time, however.

N Brown (BWNG.L) - Settlement of a Legal Dispute & Trading Statement

N Brown start the week off by settling their outstanding litigation by paying £49.5m. This is £24m more than they provided for in August accounts, so in that sense is bad news. However, it always looked like it was going to be more, and it removes the uncertainty.

The company has enough cash on hand to meet the payment from that and debt facilities for when they need working capital. (January will be a cash balance high point). The market really didn’t know how to take this and moved from -7% to +8% in the opening 5 mins on this announcement. Unfortunately, we have no idea either.

Later in the week hey updated us on Christmas trading. This showed a weak Q3 but was in-line with expectations. FY EBITDA is also expected to be in line. In the common theme, customers are either going for value or premium ranges., and more are taking finance.

The default rates normalised post-COVID, but we do wonder if they are storing up trouble for the future? So does the market, though, hence the big discount to TBV. This may prove too large if they can make those assets productive again, or Mike Ashley swoops in and does it for them.

Downing Strategic (DSM.L) - Cash Exit Facility

Downing Strategic are becoming increasingly aware of the looming cash exit:

The Board has previously announced its intention to offer shareholders a 50% share redemption opportunity in May 2024 at NAV (less costs) (the "Cash Exit Facility").

If shareholders go for it, which they’d be daft not to given the discount, then the fund will be subscale and then put into wind down:

Nevertheless, should the Cash Exit Facility be fully subscribed and, as a result, the Company becomes sub-scale, the Board intends to conduct a strategic review (the "Strategic Review"). This review would consider putting to shareholders a continuation vote, or, alternatively, a potential roll-over into another suitable investment company, possibly coupled with a cash exit. If a continuation vote were proposed and not passed, the Company would be placed into a wind down strategy with the objective of realising the remainder of the Company's portfolio in an orderly manner.

They are subscale already so halving the AUM means the death of the fund. Their answer is buybacks to narrow the discount. This makes sense, but unless they get the share price to a premium of NAV, then shareholders would be daft not to take the 50% cash exit in 2024. They say that:

Over the period of 12 months to 31 December 2022, the Company’s NAV declined by 16.8% compared to a decline of 30.7% in the FTSE AIM All Share TR index. Despite this out-performance...

Comparing against an AIM index is poor form for any fund, as is quoting brokers’ target prices as if they are gospel:

the Company’s investment portfolio is currently valued at a discount of over 40% to consensus share price targets in the market.the Company’s investment portfolio is currently valued at a discount of over 40% to consensus share price targets in the market.

Leading to them repeatedly talking about a bogus "double discount", which makes them sound like an advert for ScS.

The Company currently holds 15.7% of its assets in cash.

So nowhere near enough to meet the cash exit facility, so:

The Manager has undertaken a liquidity analysis of the Company’s investments. Based on this current analysis, the Board is confident that the Manager can maintain a pool of investments sufficient to realise adequate cash, through market liquidity, anticipated corporate events, and capturing the embedded value in the portfolio, to exceed the amount required to fund the Cash Exit Facility. New investment opportunities will be considered within this liquidity analysis.

They will clearly be pushing their holdings to put themselves up for sale since this will save their blushes. Otherwise, they are going to become forced sellers in the following stocks:

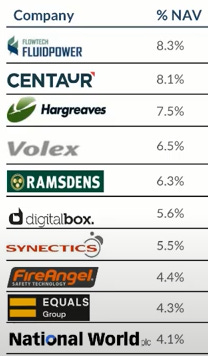

Although they seem to already be selling down their most liquid holding: Volex.

Hostmore (MORE.L) - Trading Update

Trading updates so far have generally suggested that consumer spending held up better than expected in the lead-up to and through Christmas. But how has one of the country's worst restaurant chains fared?

The brief answer is that they have chosen not to tell us, only providing 26-week figures vs 2019 and comparisons with a covid-affected December 2021:

On a statutory like-for-like ("LFL") basis, revenue for the 26 weeks ended 1 January 2023 continued at 14% below the comparative FY19 period.

-14% is clearly bad, and some excuses are clearly required:

This result was achieved despite the impact of Her Majesty the Queen's passing, national rail strikes, the Football World Cup, and the unusually cold weather during the period.

OK, so there was an extra bank holiday and this certainly affected spending that week and month. But should it really be visible in 6-month figures? Let's be generous and say that, as a primarily drive-to venue, they gained no benefit from people crowding into Central London and completely lost the equivalent of two days of revenue. That's 0.55% of trading over six months.

And then, let's simultaneously claim the complete opposite and that they have primarily Central London locations only accessible by train. 19 days of strikes. Let's say trading halved on each. So that's a 2.6% hit.

What about the football cup? Again, a halving of trading in the affected times would be a 3.5% hit.

Cold weather? The argument here is that having some colder (but dryer) than average weather for ten days in December badly affected trading, while far better than average for almost every other day in the period had no positive effect?! We are pretty sure they would argue heatwaves were bad too - presumably, the ideal weather would be continuous light drizzle as this would make being inside a TGI Friday's marginally more appealing than being outside?

And remember that these are 2019 LFL comparisons. Surely they have increased prices by at least 15% since then? So these are terrible figures, with no excuses. How do they compare with expectations? finnCap say:

Recent trading has been mixed, with excellent weeks interspersed with too many poor weeks

This actually explains the excuses in the RNS commentary - all the factors highlighted would have resulted in poor weeks, it is just they don't explain a poor six months. EPS forecasts are cut significantly, most notably for losses to double in the period just ended, but profits are still expected to flow from FY 2024, now at the rate of 1.8p EPS. They do not include cash forecasts in today's update and make it clear that the strong cash performance to the year-end was strictly down to one-off factors.

The main bull case here has been continuous director buying, but not from the CEO, who has now resigned. Although progress has since been made, he was far too slow to realise that the rollout needed to be put on hold until the fundamental issues with the quality of the offering and the finances were sorted out. However, there's still a chance that Hostmore could survive.

Marks Electrical (MRK.L) - Trading Update

This is an in-line statement well received by the market:

· Strong trading period in Q3-23 (October to December) with revenue growth of 33.4% to £29.8m (Q3-22 £22.3m)

· Year to date (YTD) revenue growth of 22.0% to £72.9m (2022 YTD: £59.8m)

As previously highlighted, their customers have the cash to invest on energy saving:

Strong performance driven across product categories but particularly in A-rated energy efficient laundry appliances, televisions, refrigeration and small domestic appliances

And of course, 22% revenue growth looks phenomenal compared to AO. down 17% for the year! Although AO are targeting margins at this stage. It is Currys that Marks need to worry about.

Part of their USP is in-house delivery drivers, so subcontracting installation was always a concern for customer satisfaction. It is good that the transition is going well:

In-house fleet of delivery vehicles achieved record delivery volumes in the quarter, during which we also saw continued adoption of our in-house installation service with over 3,000 installations now completed since launch in August 2022

Out-of-home and London is a reference to the London Underground campaign:

To continue our focus on growing brand awareness, we further invested in highly targeted television, radio and out-of-home campaigns over the Black Friday and Christmas sales peaks. This led to increased website traffic and broad-based revenue growth across the UK, but with particularly strong improvements year-on-year in London, South East England and the East Midlands.

Equity Development are strongly hinting that they will beat FY forecasts:

Given trading uncertainties which are associated with the current domestic and international geopolitical backdrop, we believe it is prudent to leave our full year forecasts unchanged.

However, we note that with 82% of our FY2023 target already achieved, the company is in a strong position to meet current expectations for sales revenue and profitability.

Taken in isolation, today's update would deserve a bigger increase in share price. We're clearly on the borderline of a 10% EPS beat with strong momentum into the following year. But the share price had already risen 60% from the lows. The main concern here is that it is now overbought. And we also know that insider sales are coming when it reaches its post-IPO highs.

Nanoco (NANO.L) - Litigation Settlement Update

With the share price rising strongly last week, Nanoco have clearly been forced to pour some cold water on it:

-- The gross settlement value should be expected to be towards the lower end of the range of expectations for a successful jury trial outcome as previously guided by the Company.

-- A settlement removes the risks of the litigation process, potential appeal processes of the trial and the ongoing appeal of the Patent Trial and Appeal Board decisions, further litigation costs, and the time value of money.

-- Historical precedent shows that any final agreement is likely to be a one off payment, with no forward royalties, for the full and final settlement of all current and future patent litigation between the Parties in all jurisdictions (colloquially referred to as "patent peace").

So a one-off payment at the lower end of the range for a jury award with no ongoing royalty. Edison & Turner Pope suggested low-end values of c.$200m for USA, and that is 1/3rd of global sales so $600m but up to 50% goes to the funder.

The court docket had $120-400m as the estimates. It would seem that the $150m for the US part is probably about right, but that we can’t just treble it for global, we think Samsung will want a discount on that, plus maybe for early settlement. So perhaps, $250m, of which, say, 40% to the litigation funder = $150m = c£123m.

So around the current market cap at 37p per share. But there is little indication that the management will pay all of this out, they may keep a good chunk of it to pay board salaries. Apart from this litigation, there is little sign that they have a successful business to fall back on:

So the risk-reward only really favours buying at a significant discount to today’s market price.

Xaar (XAR.L) - Trading Update

They generated 9% organic revenue growth, however, this is only in line with H1 in terms of both organic growth rate and absolute revenue. They also guide a return to profitability at an adjusted level for the FY, but given that they had this at H1, this is really just saying H2 wasn’t loss-making. And given the level adjustments, this may not be true after you account for discontinued operations & restructuring costs, let alone the SBP charge and amortisation of acquired intangibles.

For cash, they say:

The Group remains well capitalised with a strong balance sheet with a net cash position as at 31 December 2022 of £8.6 million

But somehow forget to mention that this was £12.7m six months ago. So that is another £4.1m cash outflow from operations for the six months, on top of the £7m in H1. Part of this is working capital, but it seems that unless they make changes, that cash will all be gone.

We saw nothing here that justified a £158m market cap, and neither did the market, with the shares falling 15%. Still looks significantly overvalued, despite this fall.

Reach (RCH.L) - Trading Update

While the macroeconomic environment remains challenging for the whole sector, we are continuing to deliver on our strategic priorities.

Strategic priorities appear to be increasing tenuous local news stories such as “Birmingham residents impacted by [National] proposed law”.

Consistent growth in audience engagement, an increasingly active user base and a growing pool of customer data is supporting a higher quality digital mix, with data-led, strategically driven revenue c. 30% of our digital business.

We have consistently argued, measuring quality by "number of clicks" is not the way to maintain brand value. But apparently, there's always scope to cut costs further:

We expect current market headwinds will continue during 2023 and have therefore taken decisive action, putting in place a further cost reduction plan.

Here's the impressive bit:

Circulation revenue for the period grew by 1.8%, continuing to benefit from cover price rises earlier in the year

But in the current environment, the problem is always going to be with advertising.

Digital revenue and print advertising for Q4 declined by 5.9% and 20.2% respectively (July-August2 digital grew 5.9% and print advertising declined 17.0%).

Lower than forecast group revenue in Q4 and the less profitable revenue mix of stronger circulation but lower advertising, is expected to impact profit and the Board now expects operating profit for FY22 will be below the current market consensus3 by mid-single digits %.

That really isn't bad, and surely the market knew this was coming as advertising rates are hardly a secret. So 27% down seems a significant overreaction in the share price.

The trouble is that Reach still doesn't look super cheap by historical standards. For example, in April 2019 the share price was not a million miles away from today at 67p, but the forward PE was 1.8x, the yield was 9.6% and debt (based on Stockopedia EV) was £40m. Now there is no debt, but the yield may be in doubt and the PE is maybe 2.9x. They are not cheap compared to their listed competitor, National World, either.

Also, they have now taken a second opportunity to refuse to disclose the impact on their pension scheme from their LDI exposure.

That’s it for this week, have a great weekend!