Small Caps Live Weekly Summary

SCL Social Demergers CMCX MWE RBG G4M TUNE FCAP NTQ ARDN INCE CAR

The big news this week - we are planning a Small Caps Live social. Details TBC, but most likely on a day in the week commencing 29th November. In the meantime, please fill in the following survey which will help us plan it.

Large Caps Live 15th November

Demergers are becoming all the rage, with recent announcements from GSK, GE, Johnson & Johnson, Toshiba, and now CMC Markets.

So on opening the CMCX announcement I decided to play word bingo with the opening para:

Some points:

1. It drives me mad when every company claims it is a ‘leading’ company in its field. To be fair to CMCX it probably has more of a claim than many.

2. ‘very early stages of evaluating the merits of a managed separation’ – I thought this was interesting wording. Usually, a demerger is fairly straightforward as the divisions are separate businesses often with no synergies. It is not clear to me how CMCX is organised internally and the above makes me wonder if whole new structures will need to be put in place. I read this phrase as very cautious – so would be interested in knowing what others think.

3. ‘shareholder value’ is used twice – ‘to unlock’ and ‘to maximise’ shareholder value. A cynic might suggest that the value is the same whether the two halves of the business are together or separate – but that if separated there will be additional costs.

4. Looking at the ‘early stages’ together with ‘continuous evaluation’ makes me think the board is trying to say this is just business as normal and we might not do anything.

So given it has rallied this morning, and that Mark and Leo have discussed in the past that the ‘traditional’ brokerage side of CMCX – if put on an AJB or HL multiple – means that the rest of the business is free.

It is not entirely clear to me that CMCX leveraged side and the brokering side are entirely different businesses…both ultimately need a similar front end and back end - at the front a strong brand name and marketing to acquire customers; and at the back end to trade shares etc.

I think the issue with this is that the Australian business has just been acquired from ANZ so there is a risk of some churn of customers. Furthermore, the strategic intent of growing the traditional stockbroker business is really only become clear in the last year or two.

Reading today's statement, maybe what is really saying is "look, this company is undervalued and don't think we won't do something about it if it persists". They are probably annoyed for getting punished for being low on the earnings side while expensing a lot of tech development that should drive future growth. Of course, the answer to that is to capitalise some of the development if they can show auditors that there is a high likelihood of those expenditures leading to revenue and profits in the future. The method available to most companies who generate high cash flow and remain undervalued in the eyes of their management is usually a share buyback. However, that avenue is closed to CMC Markets with Cruddas still owning a large proportion of the shares.

Maybe the valuation indeed doesn't reflect the opportunities and existing customer base, but they don't need to raise any money so does it really matters to long term investors? Two years time if everything has gone to plan and if the share price hasn't responded would be a better time to demerge. Also with a company with a market cap of circa £754M - splitting them probably gives u two companies with a market cap of £370M each - or more likely one half will be bigger than the other so you will get a company of, say, £500M and £250M. Not many institutional clients want to own £250M market cap companies.

Small Caps Not Live

Capital Ltd (CAPD.L) - Equity Portfolio Valuation

Although there hasn’t been RNS’ed news from Capital this week, that doesn’t mean that the business outlook hasn’t changed. Specifically, the price of gold has been strong. Which has led to a number of Capital’s portfolio holdings performing well. For example, their largest holding, Predictive Discovery, hit a new high on Thursday. By our calculations this means that the value of the equity portfolio is now above $60m and approaching 30% of the market cap.

We get the argument that a number of these stakes are strategic and part of a business development strategy that means the company will be preferred for drilling contracts, and therefore perhaps should not be included at face value. However, we think the argument that says these are strategic and therefore should be valued close to zero (as the market currently appears to be doing) is not right. The company has confirmed that none of their drilling contracts require them to keep hold of their equity stakes. Indeed, they have been relatively active traders - selling out of Arrow Minerals through on-market sales earlier in the year, selling some of their FireFinch into recent strength before exercising their FireFinch options.

We were surprised that the market reacted positive to the Q3 end announcement of the value of the equity portfolio given the ease of calculating this. Our assumptions of some basic market efficiency continue to be eroded by the lack of reaction to positive news here.

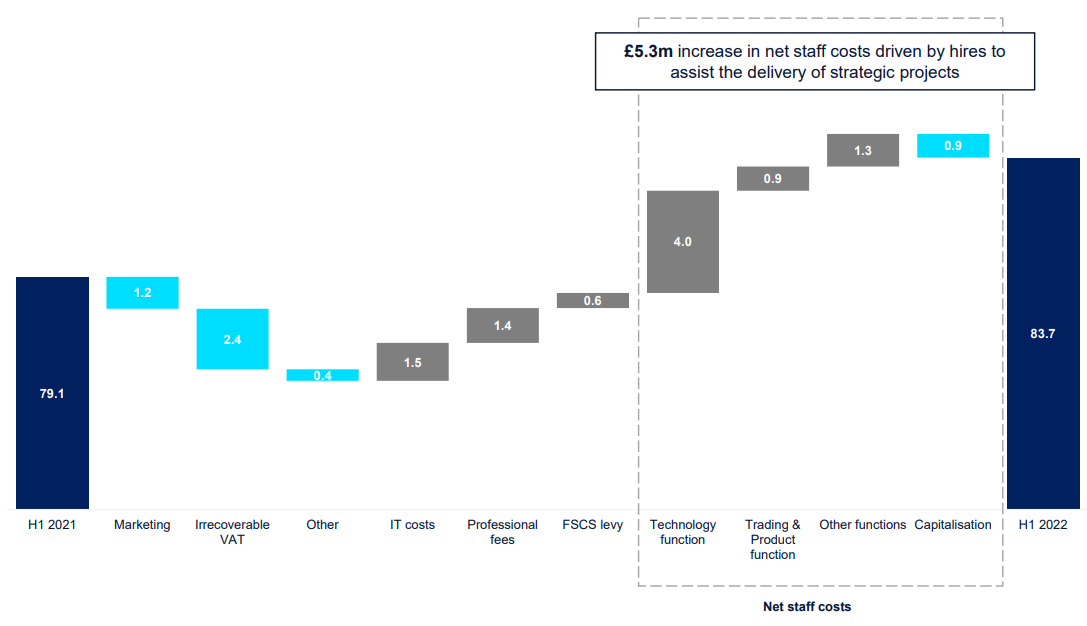

CMC Markets (CMCX.L) - Half Year Results

Having risen in response to the proposed demerger, CMC markets gave back those gains, and then some, in response to its H1 results. On the surface, this seems strange given these results were largely known from the last trading statement. Investors are rarely totally rational, though, and maybe seeing the sheer scale of the mean reversion at work here has spooked a few:

The leveraged side of the business has seen a drop in active clients plus revenue per client as clients traded much less:

There has also been a shift from trading indices to trading shares whereas they get more value from the spread and 2-way trading in indices. The non-leveraged faced the same reduction in client trading, but here active client numbers were more resilient:

The company re-iterates their full-year guidance though:

H1 2022 net operating income was £126.7 million. FY 2022 net operating income guidance reiterated at £250-280 million.

Operating expenses are guided to be about 10% higher for H2 vs H1, which works out to be around 18p of EPS for the full year. Obviously, this is much lower than in recent times. However, on the current price this works out to be an earnings yield somewhere around 10% which is cheap for the current market. And the company are keen to point out that a lot of the cost increase is investment in the new platform for UK B2C:

The new non-leveraged platform for the UK will be ready by middle of next year. The waiting list for the platform is to launch imminently.

As discussed in LCL (this really fits in between our mandates as a mid-cap!), the strategic review on the demerger may not be the greatest of ideas, but it does show a management who think the future potential of their stock is materially mispriced. As Peter Cruddas said on the results call:

There’s an awful lot of locked up value in this company - one day you will see it.

Given recent share price performance, shareholders will be hoping “one day” comes sooner rather than later.

MTI Wireless (MWE.L) - Q3 Results

MTI wireless released their 9-month results this week. Usefully, these are full results not just an operational update so we have an income statement, balance sheet and cash flow statement.

This was another positive quarter for the Group, leading to an 11% increase in profitability for the first nine months, and I believe that we are well placed to achieve a good result for the full year. Operationally we are close to normal now, with nearly all of our markets functioning as they did pre-pandemic, but travel limitations and the availability and cost of shipment continue to be part of our challenges as part of the "new normal".

This company didn't show much obvious impact from COVID on their financial numbers, so there will be a limited bounce back effect - but it shows how well the management navigated this period.

In the third quarter we saw a lower gross margin rate due to our product mix, shipment costs and strengthening of the Israeli currency against the USD and the Euro , but these factors were offset due to the economies of scale achieved from the additional revenues in the Period, enabling us to increase our operational profitability.

All this is potentially expected given the general market backdrop. However, since the report is for the 9 months, we need to do a little maths to work out Q3 results alone. And here the numbers are less impressive. Revenue growth for Q3 on Q3 is just 7%. Profit growth 6% showing little operational gearing.

Compared to Q2 of this year sales, gross margin, profit and EBITDA are all down.

The balance sheet remains strong though:

The financial base of the Company remains strong with a high level of cash generation, no debt and cash balances of $9.3 million.

The story from management is one of growth in multiple markets, across 5G aerials, defence and water management. However, the current growth looks decidedly lacklustre. Particularly, since they describe 2020 as covid affected.

In the Investor Meet Company Presentation following these results the CEO says that they are targeting 7-10% revenue growth with EPS growth in double digits. However, I'm not sure I see that in the EBITDA they have been reporting.

If we assume that for Q4 they will do somewhere between the $1.4m EBITDA they did in Q3 and the $1.6m EBITDA they did for Q2, then this is a forward EV/EBITDA of between 14-15x. This looks expensive for the rather lacklustre growth in EBITDA. The rating is also much higher than it has been in the past, which was at a time the company was growing much faster and had the same multi-year tailwinds.

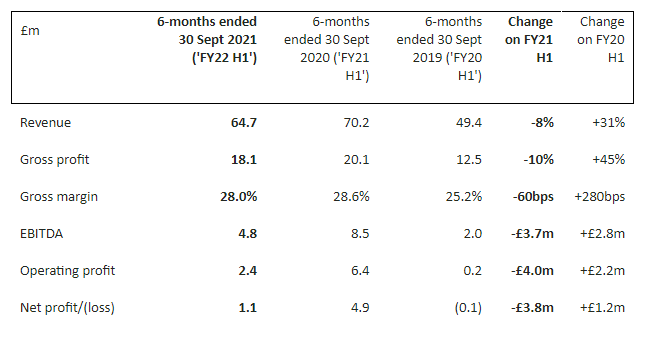

Revolution Bars Group (RBG.L) - Preliminary Results

This is for the year ending 3rd July, the trading figures for which have long been known. Today two things are important - current trading and balance sheet / detailed financial position.

Although the company has had a lot of government support, some ongoing, and has raised a lot of money from shareholders, and some commentators are very positive about their financial position, we were less convinced last time we looked at them. This isn't a good start:

The Financial Review provides information on liquidity and going concern, and also the full going concern disclosures, which include references to material uncertainty, can be found in note 1.

They summarise later:

No forecast breach of the banking covenant arises under either forecast scenario but there is very limited headroom under the severe but plausible downside forecast scenario under which headroom is minimised to £0.9 million at the end in April 2022.

£0.9 headroom is not a lot. The low level of liquidity headroom relative to the minimum liquidity covenant in the severe but plausible downside case, and the material uncertainty caused by COVID coupled with forecasting difficulties as a result of constantly changing operating restrictions means that the Group cannot be assured that it will not breach the minimum liquidity covenant.

However, in current market conditions we agree with this:

[given] the Group's existing relationships with its main creditors, its success in recent years in obtaining covenant waivers and renegotiating its banking facilities and recent equity fundraisings, that a request for a waiver of a covenant breach or renegotiation of the banking facilities would be successful.

Revolution are unlikely to be put under by their banks given that they have shifted most of the risk to the Government by replacing RCF's etc. with CBILS loans. The risk of insolvency comes from landlords. It seems they still haven't fully paid back rent for their period of closure:

Management continued to negotiate beneficial payment and contract terms through periods of closure with key suppliers and landlords and the Group thanks them for their support. As discussed in the Group Annual Report and Accounts 2020, the Group completed the Company Voluntary Arrangement ("CVA") of Revolution Bars Limited which was approved on 13 November 2020.

These must have been landlords who had parent company guarantees so couldn't be CVA'ed. Their going concern statement includes what they would consider severe future disruption. What is plausible, if unlikely, however, is being closed as a nightclub and having to trade as a pub for the next 12 months, and receive no government support. For a company like Revolution, this would be at least as bad as their "severe" scenario.

This is what they have to say about future trading:

At the time of writing total revenue is currently 137% of FY21, with FY22 LFL2 revenue since 19 July, when restrictions fully relaxed in England, 14% ahead of the comparable period in FY20.

Guests continue to choose our bars in ever greater numbers, with weekends busier than ever. We are very pleased to see guests and colleagues creating fun and memorable experiences;

So we are seeing strong trading from their young customers, with a focus on the weekend. Trading during the week is implied to be poor, presumably due to a lack of socialising after work. Supporting their base case of subdued LFL Christmas trading, they say:

Christmas bookings have been building more slowly than we would normally expect, which we believe is due to a level of uncertainty around the "return to office" and the UK Government COVID autumn and winter plan; this leads us to believe the shape of Christmas trading will be different, including smaller parties and much higher levels of walk-ins which we have previously been unable to accommodate.

House broker, finnCap has a £18.2m EBITDA forecast for RBG for 2022. The adjusted EV, after correcting for negative working capital and net lease liabilities is around £115m. This is a forward EV/EBITDA of 6.3. So this isn't exactly cheap given that it is a fairly CAPEX heavy business, is not really growing, and is still financially weak despite multiple equity raises.

Gear4Music (G4M.L) - Interim Results

It does seem to be the tale of two musical retailers this week. Whoever it was on our discord channel that called Gear4Music as the next company to face post-lock-down headwinds called this right:

So everything is up against 2019 but down against 2020. Looks like this was at least expected, with EPS forecasts for FY22 on Stockopedia set to be about half that of FY21.

There is a lot to analyse here to understand where this company is going because;

2016-2019 you had rapid revenue growth but very patchy profitability

2019-2020 revenue was flat but featured a return to strong profitability.

Then you have seasonality - people buy cheap instruments (presumably for their closest enemies) at Christmas.

Overlaid with this is the lockdown effect.

Anyway, these results came with a profits warning:

FY22 Q3 revenue to date slower than expected due to on-going Brexit related supply chain challenges, leading the Board to revise FY22 full year EBITDA guidance to not less than £12m (FY21 EBITDA: £18.9m, FY20: £7.8m)

So you can add understanding Brexshit to the list of factors to analyse. So we know what the forward EBITDA is estimated to be, but we really have very little idea what multiple to apply to this. Is this now a plodder where 5xEBITDA is fair value, or should we have it up there with the racehorses on 15-20x?

The EV is £155m after today's 17% fall so that is 13x forward EV/EBITDA. So if this remains a thoroughbred then there is a decent upside, but also a big downside if it has gone lame. Given all the potential factors to analyse, understand and forecast, Mark is simply putting this in the too-hard category. That said, it is not a bad company and if what they say about profits warnings always coming in threes is true, and it dropped back down to its pre-covid levels of around £2 per share, then the risk-reward would look a lot more favourable.

Focusrite (TUNE.L) - Final Results

Focusrite is the other music-related company reporting this week:

These numbers are fantastic. We have a bit of a problem with acquisitive companies adjusting out acquisition costs - but then they do separate out organic & LFL growth, which many acquisitive companies conveniently fail to do! And their higher gross margin means that sales growth drops through to EBITDA more readily.

At £47.5m EBITDA and with £17.6m net cash this is on 19.8x EV/EBITDA after a 9% rise in response to these results. This isn't Mark’s sort of share, though. This valuation in a company close to £1b market cap just leaves too much risk for him, should growth slow. He doesn’t believe he would see the mean reversion coming and hence would be the patsy if he owned this sort of thing.

Is this a sign of mean reversion appearing, for example?

Whilst there remains considerable opportunity for operational leverage across the Group as revenue increases, in FY22 operating costs will increase to reflect current tightness in supply chains, travel resuming and our intention to increase investment, where appropriate, in order to fuel future growth in the business.

But then the overall tone of the outlook is very positive:

We look forward to another year of innovation and expansion.

Gun to his head, however, he’d prefer to own Focusrite on a 20x EV/EBITDA multiple than Gear4Music on 13x.

finnCap (FCAP.L) - Interim Results

These results were largely known since revenue was announced in the trading statement and costs tend to be roughly proportional to revenue. Adjusted EPS comes in at 3.54p for the half-year, cementing this as one of the cheapest shares on the market on earnings. Although, we would typically not adjust out share-based payments since these are a real cost borne by shareholders.

Management are of the view that fully diluted EPS is a better measure of the true performance than applying IFRS2 to calculate share-based payments. This means that 3.17p fully diluted but adjusted EPS is probably a reasonable figure to take. So still cheap.

The increase in cash is not as large as the earnings due to deals completed towards the end of the period ending up in receivables:

Cash balances: £22.6m at 30 September 2021 (31 Mar 2021: £20.4m)

To get a better feel of this, Mark dusts off his trusty friend: shareholders cash. This is cash - debt + NWC (if it is negative) - any provisions. Although finnCap has a requirement to hold regulatory capital, movements in shareholders cash give a good feel for how value has accrued to shareholders in the period. In finnCap's case, we will include in the NWC longer-term financial assets and liabilities plus tax owed since these real assets and liabilities.

"Shareholders cash" has gone from £8.5m on 30th September 2020, to £12.0m on 31st March 2021 to £18.5m in these results to 30th September 2021. This makes net cash about 1/3rd of the current market cap.

On top of this a £0.8m dividend was paid in H2 last year, and £1.6m during this period so the last 12 months has generated £12.4m of value net to shareholders. In addition, they said in the InvestorMeetCompany presentation that the current cash balance is considerably higher at the moment vs period end.

A further increase in dividend guidance has been given with these results:

Given the strong financial performance so far in FY22 and the Group's much improved balance sheet position, the directors intend to pay an interim dividend of 0.6p per share, a rise of 20% on last year.

In addition, following the upgrade in our revenue guidance range, the Board has increased its dividend payment intention for FY22 to a total of 1.75p per share (subject to unforeseen circumstances).

This is about a 4.7% dividend yield. Clearly, they could afford to pay much more, but priorities are for growing the business in the short term:

In addition to our equity sales and trading team hires, we have also hired junior execution team members in both Capital Markets and M&A to ensure we have the capacity to service the future needs of our clients...

We continue to review potential M&A opportunities. We are currently focusing on ESG related consultancies with established track records and repeatable revenue as part of our strategy to broaden our range of strategic advisory to the C-suite and expanding our business potentially beyond its core financial services offering.

In terms of outlook, finnCap retain their guidance:

revenue expected to be in the £45-£50m range; staff costs (excluding share-based payments) c.58-62% and non-staff costs c.£10m.

Broker Progressive have made a very minor upgrade to their forecasts:

We have increased our revenue forecast for the current year by 2% to £48.5m, based on a positive trading outlook.

This means that progressive are forecasting 0.95p of adjusted EPS for H2. £48.5m Revenue implies that they do £16.8m for H2.

On Cavendish they say:

Activity levels are now lower than in H1, but the finnCap Cavendish team has already completed a further two deals since the half year end and we expect the team to deliver a good full year result with revenue above £20m.

So that is more than £3.9m for H2, but seems a very low bar, and would be one of the lowest Cavendish half-years since listing. Interestingly, on the IMC presentation, they say that they typically have 1-year visibility on these deals and the pipeline out into the future is also strong.

On transactions:

Overall, market volumes and activity have decreased during H1 but the sales and trading team delivered revenue ahead of last year benefitting from one very significant sell down and the first contribution from the finnCap Analytics team.

On ECM overall:

After experiencing very high client activity last year, in our strongest sectors, delivering H2 revenue at levels similar to H1 would be an excellent outcome for the Capital Markets team.

So it sounds like H1's £15.6m ECM revenue is their target but likely to come up a bit short. Still, that would easily beat Progressive's forecast revenue. Management say that they aren’t sandbagging with their current guidance, but they know the importance of hitting market forecasts, so there is still a chance they plan to underpromise & over-deliver.

Although in our analysis on here we have tended to focus on short term trading, one thing the management was keen to point out was their ability to grow whatever the market conditions. Saying "we are a long-term growth play".

Their strategy is to build a very different financial services business. They have recruited 30 people this year and said in the IMC presentation “we are a great place to work....well ahead of competitors as a good place to work” which is key to talent retention. They have plenty of interesting, good value M&A opportunities too, but it is not in the strategy to buy competitors due to the difficulty in adapting cultures.

If they can deliver on their long-term growth ambitions, then the current rating looks much too low for a growth business.

Enteq Technologies (NTQ.L) - Interim Results

You can tell a set of results is going to be bad when the highlights don't feature any of the financials! When you get to the financials then these look very poor:

This shouldn't really be a surprise, given that we highlighted a few weeks back that the US rig count was coming back much more slowly than past oil cycles.

The attraction of Enteq in the past was a large discount to Tangible Book Value. However, in what is perhaps the definition of a value trap, losses have eroded the TBV which has been falling faster than the share price. This now trades at 1.12xTBV so doesn't even have that going for it.

As we have said multiple times now: if you strongly believe that the rig cycle is just slow rather than permanently broken then buy Hunting rather than Enteq, since this is a much better company on almost every metric, and trades at half the valuation.

Arden (ARDN.L) & Ince (INCE.L) - Takeover

We return to a story we covered at the end of October: Arden recommended an all-share offer from Ince, partly because Ince shares are much more liquid than Arden's.

Unfortunately, Ince shares were then suspended as Arden was their NOMAD and had to resign. That's about as illiquid as you can get. Ince investor relations blamed this on bad advice from the LSE, but said they knew they'd have to change NOMAD and signing up a replacement was already in progress. However, as of today they still have no NOMAD.

Friday morning, the price of Arden has been marked down below what it was before the offer was made, an offer that nominally was at a premium of 40%. It is tempting to think that buying Arden shares may be a buy at this level. However, what started as minor incompetence is now well into shitshow territory, with Ince now having only 5 full working days to sign up a NOMAD before trading on AIM is cancelled.

Some investors don't seem to have a high regard for the management at Ince, and Leo notes that when Zeus tried to buy a NOMAD to expand their service the FCA raised fit and proper concerns. As best approval would take some time, and surely falling foul of AIM rule number 1 doesn't look good for a prospective owner of a NOMAD.

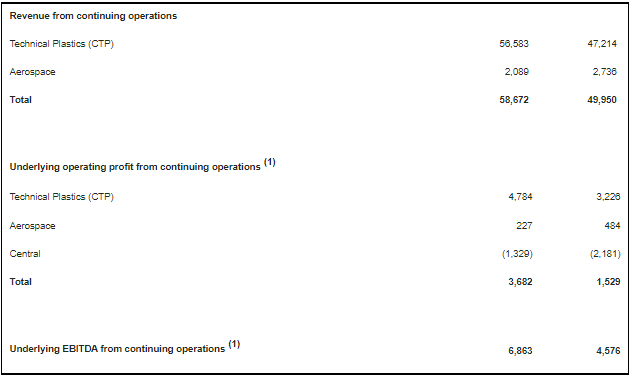

Carclo (CAR.L) - Interim Results

These show a decent recovery from last year, with the technical plastics division obviously doing the heavy lifting:

The headline numbers of 7.5p EPS compare well to a share price of around 45p. However, this benefits from one-off tax credits, US COVID grants and discontinued operations. The underlying EPS is 2.5p. If we annualise that to say 5p, that is a P/E of 9. Again, on the surface, pretty cheap. However, there is an elephant in the room. Indeed, 2 elephants.

Net debt excluding lease liabilities at 30 September 2021 was £21.6m, a reduction of £2.8m compared to 30 September 2020.

With a £32m market cap, then this makes the net debt adjusted P/E about 15. Not so cheap. And then elephant 2 squeezes in:

IAS19 Retirement Benefit liability down to £33.4m, reduced by £24.7m since September 2020 (and reduced by £3.9m since March 2021) from improved asset returns, additional employer contributions, and initiatives progressed with the Trustees

Of course, this has come down rapidly due to strong equity returns and higher bond yields but also because Carclo has to make large additional contributions of £3-4m per year. This is on a par with their underlying PAT! So almost all of their profits are going into the pension fund. So it is no wonder they say:

Under the terms of its financing agreements the Company is not permitted to make a dividend payment to shareholders up to the period ending in July 2023.

This is probably the debt covenant but we would expect pension trustees to take a similarly dim view. Indeed, it is hard to see this company being financially secure enough to pay a dividend this decade (unless they do a large equity raise in the meantime). This is being run for its bankers and retirees.

As with so many similar companies, such as Mpac or Renold, shareholders don't seem to understand how pension deficits work - IFRS19 which is what you see in the accounts tends to use more aggressive assumptions than the triennial review. However, it is the latter that determines the payments the company has to make. So you can have no IFRS deficit and large ongoing recovery payments being made.

If you take the, currently rather quaint view, that a company is worth the net present value of cash returned to shareholders over the life of the company then this makes such companies worth significantly less than a simple metric such as P/E may imply, since less cash is available to return to shareholders or reinvest into growth.

No dividends, and a lack of re-investment that will be reflected in lower growth, will eventually be accounted for in valuations no matter how much investors fail to understand this effect in the short term.

Right, that’s it for this week - don’t forget to give us your views in the SCL social event poll if you haven’t done so already. Have a great weekend.