Small Caps Live Weekly Summary

GDWN JIM RFX SDG SOM

It’s been an interesting week, with global stock markets taking a tumble on Monday. The bounced back, at least partially, on Tuesday. Of course, none of the reasons given for the crash, such as the unwinding of the Yen carry trade, really impact the kind of UK small caps we go hunting in. Yet, it didn’t stop the most popular UK small caps from dropping 10% or more in response. You have to feel sorry for the investors who panic sold at the bottom on Monday (or were stopped out) only to buy back in when the same shares had risen on Tuesday. Crowded trades seem to be in vogue at the moment with some popular stocks bid up to what seem like daft levels, while some others languish on very modest ratings waiting to be tipped somewhere. Thankfully, none of us on SCL are popular!

Here’s some of what we looked at this week:

Goodwin (GDWN.L) - Preliminary Results

The company has produced decent results, with trading profit increasing 27%. However, it has largely flat revenue, so this is about margin improvement rather than sales growth. Like many similar industrial businesses, it has likely benefitted from inflation moderating. Although, they also suffered from currency headwinds.

Still, it is easy to make the argument that this is worth 20x earnings adjusting for any debt. Trading PAT would be £18m on normalised tax rates. so 20x£18 - £43m debt = £318m. Sadly the market cap is almost twice this level, and as such the business needs to perform a lot better in the future, particularly on the sales side, or this will come back down to earth eventually.

There are a couple of growth drivers that aren’t in the current numbers, such as East and Duvelco, and like the Goodwin family, many investors will simply take the long-term view. However, holders will need to ask themselves, if this isn’t a sell at 40x earnings, where is it a sell? 60x, 80x? No company, no matter how well run, is a buy at any price.

Ramsdens (RFX.L) - Trading Update

Nice to get an ahead statement on a week that started like this:

As a result, the Board now expects FY24 Profit Before Tax to be at least £11m, which is ahead of its previous expectations* (FY23: Profit Before Tax of £10.1m).

This didn’t really surprise us. The main reason given for the beat is higher gold sales:

This positive performance continues to reflect the strengths of the Group's diversified income streams, the ongoing and successful investments made in enhancing the customer proposition, and the high gold price driving a better-than-expected performance in the Precious Metals segment.

Ramsdens have a track record of beating expectations so we think the main reason for the beat is actually conservative forecasting. FX usually contributes the largest proportion of their gross profits and this slightly missed management expectations - as reported by the airlines, the market suddenly weakened in June. Gold sales ahead may have been enough to counteract this, but little more.

This makes it a bit of a mystery why the market didn’t price this in. Perhaps it has given the rather modest rise in the news. It may be that the gold price gains are perhaps the least sustainable or at least the most volatile, of its profit stream. If we are right, it is much better if it is due to conservative forecasting rather than a one-if gain from gold that may reverse.

Also, you don't issue an unscheduled trading update two months before year end just because revenue is running 2.7% ahead or even because PBT is ahead 6% (Liberum's numbers). This is not material under the listing rules, and disclosing it just makes you a hostage to August/September's trading fortunes. So we are pretty confident they see PBT is running 10% ahead of previous forecasts at this time, and even then, we think the conservatism and momentum are pretty ingrained. On the other hand, some of the strength in their gold segment is likely to be down to inventory gains and these could reverse even more quickly than the public's interest in selling.

This beat gives a double whammy. Not only are forecasts now higher, but EPS is growing, which means that the market should give this a higher rating than the current 8x P/E. In addition, this is now quite a bit cheaper than competitor H&T when you account for net cash/debt, yet it is a better-run business, in our opinion. None of this appears to have been priced by the market, making it better value this week than last.

Jarvis Securities (JIM.L) - Half-Year Report

It is a profits warning here, but we have no idea how bad as WH Ireland (now Zeus) removes their forecasts. To be fair to the broker, this means that the company are now saying they have no idea what the skilled person review will cost them.

As well as the profits hit, this seems to be a tacit admission that management are currently utterly distracted from developing the actual business:

Although the regulatory review is ongoing, as a firm we are currently committed to working through it and emerging in a more robust state and ready to focus on the future of the firm and its plans for growth.

The dividend is kept but at 1p for the quarter vs 1.5p last quarter and 1.75p before that. The cash flow statement doesn’t look too bad. Net cash increased during the period, and they did 4.5p EPS in H2, so even if H1 is worse, they look good value at around 50p.

While they continue to earn net interest margin at current levels, the dividend should be easily covered. The big question remains whether the FCA will take that away from them. Many won’t like the uncertainty here and it could be akin to picking up pennies in front of a steam roller. However, there is also scope to increase market share and grow if they finally get to the end of the skilled person’s review.

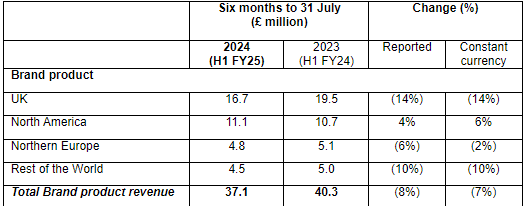

Sanderson Design (SDG.L) - Half Year Trading Update

Better news here as July saw some rebound in trading. North America is the highlight and is increasingly becoming an important part of the business

However, they keep the revised (down) forecasts. We think the reality is that, like many companies, they don't know exactly why sales dropped off and now have to be pretty cautious going forward. The amount of detail in this update is very useful. For example, on licensing:

Licensing revenue declined to £4.1 million, compared with £6.9 million in the same period last year when two major licensing deals, with NEXT and Sainsbury's, led to accelerated income of £4.9 million in H1 FY2024. Accelerated income of £2.7 million in the first half this year reflects the signing of new licensees along with renewals and extensions.

This breakdown of "accelerated" and sales-based continuing licensing revenue saves investors from having to resort to cash accounting.

Full year licensing revenue this year is expected to be approximately the same as last year.

So, unless they are counting un-hatched chickens for new signings, it appears that recurring licencing revenues will be significantly ahead of last year. We are not sure sales dropped off in May & June as much as they have tried to imply, with 24H2 (to January) being a miss ex licensing and trading reported as challenging in April. And it is clear there has been no UK recovery in July. So rather than May / June being a one-off mystery that we might soon be able to forget about, it is the US strength in July that might be the mystery. But the cash, improved pension situation, cost cutting, strong recurring licensing revenues and valuation are good reasons to remain invested.

Somero (SOM.L) - Trading Update

One from last week we forgot to include, but it is a popular stock to discuss on the SCL boards. Sadly it was not good news last week and we have to ask - should they be pleased to announce this?

Somero® is pleased to provide an update on trading ahead of its interim results announcement scheduled to be released on Thursday, 29 August 2024.

While the broad US non-residential construction market remains healthy, supported by an active manufacturing sector, onshoring, and electric vehicle and battery plants, trading in North America continues to be impeded by project start delays and pauses caused by elevated interest rates, labor shortages and concrete rationing, as previously reported in the 20 June 2023 announcement. This has been coupled with significant inclement weather in H1 2024. As a result, H1 2024 trading in North America is expected to end below the comparable H1 2023 period.

At least their statement that they have a very high proportion of variable costs appears to be borne out:

…the Company has initiated a company-wide workforce reduction of approximately 15%, a restructuring that takes effect alongside this trading update. The workforce reduction combined with a reduction in variable expenses tied to revenue and strict cost controls for the remainder of 2024 partly offset the profitability impact of the revised 2024 revenue expectations.

And they quantify the effect:

In consideration of the aforementioned factors, the Company now expects FY 2024 revenues of approximately US$ 110.0m (compared to the previous market consensus estimate of US$ 120.7m), EBITDA of approximately US$ 30.0m (compared to the previous market consensus estimate of US$ 34.0m), and year-end cash of approximately US$ 27.0m (compared to the previous market consensus estimate of US$ 31.7m).

So, this is a relatively minor warning at the EBITDA and cash level. It could be argued that the rating here has forecast some weakness, but the recent price action hasn't, so we expected many to be wrong-footed. However, the share price has held up remarkably well since.

There remains no forecasts beyond the next 5 months of trading. And actually, today is the very first time we got a 2024 forecast. Prior to today Cavendish simply presented a model of what might happen if revenues stayed level. Which they didn't. If the factors behind this weakness don’t moderate 2025 could be much worse.

Somero's story is that the weakness is caused by global factors and record residential construction. If it had been caused by high non-residential construction, presumably, Somero would still be doing well despite their longer-term issues. We think one of the problems is that Somero’s demand is based on peak demand for construction, so anything that flattens the curve, such as a lack of concrete availability, means fewer machines sold. Of course, it may mean the machines wear faster and the demand for servicing is higher in the future. But it doesn’t move the needle in the near term and may never.

That’s it for this week. Have a great weekend!