Small Caps Live Weekly Summary

Small Caps Live Weekly Summary

The Investors Round Table AEP CAPD CMCX DRV DX. MRK NXR PEEL RWA

Mark was featured on a new podcast format this week: The Investors Round Table. The panel debated three UK shares and a controversial topic. Anyone who enjoys SCL will find this an interesting listen:

A week that is dominated by the news that Odey Asset Management will be facing some big changes in the wake of Odey’s alleged misconduct. The FT reports that:

Odey Asset Management is being dismantled, with the hedge fund firm saying it is in “advanced discussions” to transfer certain funds and staff to rival groups in the wake of sexual misconduct allegations against its founder.

We have seen the effects of this with various stakes being sold. Frasers bought their 19% stake in AO. And notably, Plus500 bought back 8.2% of its own share capital from OAM. Not every company has the cash to do this, though, and whether OAM is selling or the expectation is they will need to, it has severely hit the prices of holdings such as Shanta Gold which is down 18% this week. This sort of forced selling can provide opportunities for the patient investor. While the supply-demand imbalance won’t immediately correct, anything that affects the price that is not related to the fundamental performance of the business can be an opportunity.

Anglo-Eastern Plantations (AEP.L) - AGM Statement

Bad news here. Prices are down 39% this year, on average:

The CPO ex-Rotterdam price averaged $1,006/mt for the first five months to 31 May 2023, 39% lower than the average price of the corresponding period in 2022 (first five months to May 2022: $1,650/mt)

Given commodity moves, a lot of this was surely expected by the market. However, current prices are some 16% below the average:

The CPO price ex-Rotterdam closed at $890/mt on 2 June 2023, representing a decrease of 16% from the start of the year at $1,060/mt. We expect a further reduction in CPO prices as crop production improves further in the second half of the year.

And expected to fall further. So that is average commodity prices down 50%+ for the year.

In addition, their production was down 5% for the 5 months, and bought-in palms were down 13%. We’ve not got a detailed model here, but assuming some operational gearing, the profits must be down 70% for this year. Plus, they report delays to growth plans.

There are no forecasts in the market, but 2021 and 2022 look exceptional, and 2020 is more like normal trading that should be expected:

Which puts them on a P/E of 13. There's a fair amount of net cash on the balance sheet:

And they have finally started to consider paying a more reasonable amount out as a dividend. However, this is still only a 2.4% yield. So not exactly cheap given the risk of the business. There's a discount to TBV too, but the assets are not exactly realisable., nor that productive in normal times, it seems. The shares are down 5% on this statement, but this looks like an underreaction to this news.

Capital Limited (CAPD.L) - New Contract Award & Finance Update

…new mining services contract…Earth moving & crushing services for Ivindo Iron SA, majority owned by Fortescue Metals Group ("Fortescue"), at the Ivindo Iron Ore Project ("Ivindo") in Gabon…The contract has a term of up to 5 years and will generate approximately $30 million of revenue per annum once fully operational.

This is a nice contract to win. It is with an existing customer, and they have mobilised initial equipment already, which suggests they knew it was coming when they won the drilling side, and just had to agree on terms. But most importantly, the remaining $15m capex is funded from debt, not equity.

Perhaps the most interesting maths is the ROCE. The capex is $30m for $30m of revenue. Our guesstimate is that their mining contracts tend to have mid-30's GM, so let’s say $10m incremental GP. Some additional admin costs but not too many since they presumably already have facilities on site to support the drilling side. So say $8m incremental EBIT. 27% ROCE, well above their 10% incremental cost of capital (which is the cost of debt). The complicating factor is that this is only a 5yr contract, so although these tend to get extended, 5yrs of $8m EBIT = $40m doesn't compare particularly favourably to the $30m spent today. Although this looks a lot better if they are using $15m worth of existing equipment, and in reality, the equipment should last longer than 5 years in most cases. Plus, the synergies with the drilling side, getting in on the ground with a potential world-class mine, and the diversification of another mineral all make this a good contract win.

We don't think I'm going to suddenly fall in love with the mining side of the business, given how good the drilling and MSALABS businesses are. However, the economics of this contract are reasonable, with the potential to be very good if it allows them to add more fleet/rigs in future.

There were some small broker Price Target upgrades in response to this news. Berenberg from 166p to 170p, Canaccord to 150p and Stifel to 180p. Tamesis just re-iterate their old 160p Price Target but add $27m revenue, $11.6m to EBITDA & $12.4m to FCF in 2024. Here are the old figures:

And now, post-contract win:

This is a decent upgrade, potentially making the 5% share price rise on the day an under-reaction to this news.

CMC Markets (CMCX.L) - Final Results

As will have been widely expected:

Quiet market conditions in the first two and a half months of 2024 have resulted in client trading activity being down 15-20%, which in turn is expected to negatively impact Q1 2024 net operating income.

Longer-term guidance is kept intact and now reads like wishful thinking with some pretty incredible growth rates from here:

Expectations of the underlying 30% net operating income growth from 2022 to 2025 remain unchanged, with growth in the existing business driven by ongoing strength of underlying KPIs including client money AUM, new product delivery and assuming a return to normalised market conditions.

Bad news for those that expected costs to have peaked in 2022/2023 following the delayed and irrelevant launch of their ungeared offering:

Our 2024 investment plans are expected to increase operating expenses excluding variable remuneration to approximately £240 million. Employee numbers are expected to peak in 2024 following successful hiring of additional staff over the past 12 months.

So costs will fall in 2025?

Operating cost expansion is expected to slow in 2025 after two years of significant investment combined with ongoing cost efficiency initiatives.

That's a no. There is also appears to be a general strategy to reduce the quality of earnings: More opaque B2B and a push into crypto.

The 14.7p for FY23 looks a beat vs consensus on Stockopedia:

But 17.9p EPS for 2024 looks like dreamland. Surely it is going to come in at half that? As such, these don’t look particularly cheap, although there is some TBV protection not too much lower than the current price.

Driver (DRV.L) - Half-Year Results

These are not bad, given the issues they had in the Middle East:

Although, as usual, ignoring large share-based payments isn't great. Their statement expecting a profitable year isn't a high bar either, given they reported a profitable H1. However, cost savings should be having an impact from Q4 too:

The overheads review and cost saving measures, previously announced, are ongoing with some savings already realised and with significant further savings anticipated to take effect from Quarter 4 of FY23 and beyond.

We can't help thinking what the business would be worth if they had just concentrated onEuAm all these years:

The EuAm region delivered an underlying profit of £2.9m (2022: £2.4m) while the Middle East region recorded an operational profit of £0.1m (2022: loss £0.2m), underlying loss of £0.1m (2022: underlying loss £0.3m), and the APAC region recorded an underlying loss of £0.1m (2022: underlying loss £0.5m).

Driver Group's business in Europe and the Americas continues to trade very profitably. Performance has strengthened with the implementation of our cost-saving strategies, a limited number of which are already taking effect, and the balance will flow through to the bottom line in the next trading year.

They also highlight the lease break clause and move to a smaller office as a cost-saving. The outlook is a bit weaker than expected due to lots of holidays recently:

While the second half of the year for Driver has been shown historically to be strong. April was slower than expected owing to the timing of the Easter weekend and a succession of public holidays, which affected utilisation. The Board is currently considering its policy on forward guidance, which will reflect the short-term revenue visibility.

It sounds strange not to anticipate Easter, so they clarified in the Equity Development presentation that they expected it to be weak, but the impact of holidays was greater than anticipated.

Our major concern here is the aged receivables. On this front, they say this is a: "massively improved picture" and expect further progress in H2. However, without exact figures you have to take their word for that.

One other snippet that may give long-suffering shareholders hope is that they say share buybacks are "very high on our agenda." Given the size of the cash balance, these could be significant.

DX Group (DX.L) - Tuffnells in Administration

This week we got confirmation of last week’s rumour that Tuffnels had gone into admin. Given the relative market shares in 1-man deliveries, this should be very positive for DX’s short-term trading:

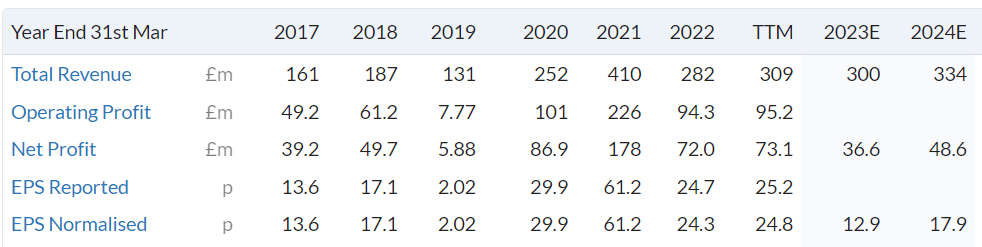

Mark’s Electrical (MRK.L) - FY23 Results

A small beat of 4.8p vs 4.6p forecast EPS for the year. Revenue was up 21.5% as previously guided, but growth seems to have accelerated if anything:

Strong trading momentum in the first two months of FY24, with revenue growth exceeding 30% year-on-year

Broker Equity Development have maintained FY 2024 revenue forecasts of 17.2%, which now looks conservative and have raised EPS forecasts only marginally. April 2025 forecasts have been introduced with EPS of 7.3p on a further slowdown in revenue growth to 14.8%. From this, you can see where they get their fair value of 150p from, although presumably, this is based on more normal equity market conditions.

Blanket advertising at transport hubs has clearly done the trick:

The benefits of the investments being made are coming to fruition, with the Group's brand awareness increasing from 7%(2) in FY22 to 15%(3) in FY23.

ED give some London specific detail:

Mark’s raised awareness levels were notable in London in FY2023, where they increased from 12% to 22% between October 2022 and May 2023

However (in our opinion), they will need to maintain spend to keep the brand at the forefront of customers’ minds ahead of the peak sales period that they give as October to December.

The share price has been strong into these results, but the outlook is undoubtedly stronger than reasonably could have been expected, at least for H1. On the balance sheet, it is impressive that inventories have actually fallen slightly, but on the other hand, receivables have grown well ahead of sales. To the benefit of cash flow, payables have also grown somewhat ahead of sales. High cash ensures a very healthy current ratio. We see no concerns there.

The share price responded positively to these results. However, unfortunately, the shares now look overvalued in the current market.

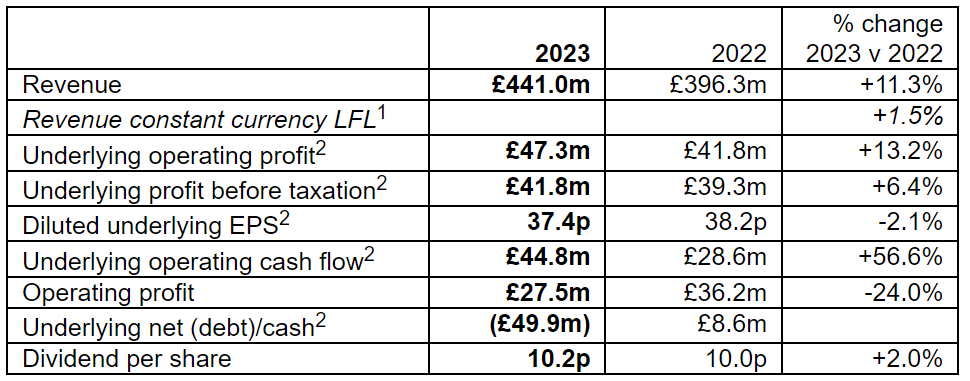

Norcros (NXR.L) - Final Results

This immediately stands out:

Underlying net debt2 of £49.9m (2022: net cash of £8.6m)

But they did spend 78.3m on acquisitions so this isn't too bad in reality. However, that is also the source of their revenue growth. One reason for this strategy and previous acquisitions was to try to outrun the pension scheme. Today they say:

The net position relating to our UK defined benefit pension scheme (as calculated under IAS 19R) remains in a surplus of £14.9m at 31 March 2023 (2022: £19.6m). Deficit repair contributions were £3.8m in the year.

The pension scheme is mature, with an average member age of 78, and experienced a reduction in member numbers in the year from 6,002 to 5,641. We remain confident that our pension obligations continue to be appropriately funded and well managed. The Group recognises that the pension scheme is a key stakeholder, and the Group and the Trustee continue to work constructively together.

Here's the detail of the repayments agreed last year:

Deficit repair contributions have been agreed at £3.8m per annum from 1 April 2022 to March 2027 (increasing with CPI, capped at 5%, each year).

The fear is that they have used LDIs to fully hedge discount rate movements but borrow to invest in risk assets in order to increase the expected future returns for triennial valuations. Their claim at H1 that the pension scheme was well managed despite the losses suggests any such arrangement may still be in place.

Accordingly, the pension situation could have worsened materially since 31st March if their investments have underperformed. Equities look to be broadly flat, but of course, pension funds generally make a point of paying high fees for underperforming funds. A higher risk would be commercial property funds!

Anyway, recent experience shows that this (and most other) pension fund deficits now have a positive correlation with the discount rate due to a fundamental failure to appreciate the relationship between the discount rate and the valuation of risk assets, so as a first-order approximation the fake surplus could now have reduced back to September 2022 levels in line with the discount rate.

Robert Walters (RWA.L) - Trading Update

A big profits warning from this recruiter:

It is now considered likely that profit for the full year ending 31 December 2023 will be significantly lower than current market expectations.

If these guys are struggling, we’d imagine the whole sector is. The thing to look for is the proportion of Temp versus Perm recruitment. Many get sniffy about Temp and consider Perm a higher-quality business, but it is certainly more volatile. I'm sure many of us have heard stories / come across situations where there is a business requirement but a recruitment freeze. The good news is that this tends to snap back eventually. The bad news is that HR departments are about to break up for their traditional 3-month holidays.

Peel Hunt (PEEL.L) - Full-Year Results

The full-year results for the Group consolidate Peel Hunt LLP, a limited liability partnership which, up until the IPO of the Company on 29 September 2021, had a corporate member and individual members. Profits derived from the partnership during the year ended 31 March 2022 ('FY22') were allocated between the members.

The first question shareholders should ask is whether the LLC structure was actually more appropriate and the plc structure will prove a short-term anomaly. The second one is under which circumstances Peel Hunt would advise its own clients to release results on a Friday!

Revenue of £82.3m (FY22: £131.0m) and loss before tax (LBT) of £(1.5)m (FY22: profit before tax (PBT) £41.2m)

On the face of it, this looks good: large PBT in a good year, only a small loss in one of the worst years in recent history. A revenue breakdown is given for each of the three legs, but no profitability breakdown of any kind. The assumption will be that the likes of market making and research made profits, but the ECM side made losses on lower activity.

Looking half-by-half, PBT was £0.1m in H1, so unless the outlook has improved, you'd expect £3.2m of losses next year. That is relatively modest compared to the tangible asset position of around £92m. Anyway, on to the outlook:

Whilst the macro-economic backdrop may remain challenging for some time, we have seen a gradual improvement in our M&A pipeline since the start of FY24, with UK mid-cap valuations remaining attractive, and are seeing tentative signs of a pick-up in capital markets activity.

Also:

Towards the end of Q4, we saw some pick-up in market activity, with a number of new mandates and pipeline deals with a higher M&A weighting. However, it is too early to say what will happen in practice, and execution risk remains amplified.

So several points there:

1) As has been the case for a while, M&A is outperforming, and brokers with strength there are likely to suffer less

2) consolidation is not over

3) we're bumping along the bottom rather than things getting worse

Although, this is what they said on 1st December:

In the first few weeks of our second half we have seen an increase in market activity which has led to an improved trend in the revenue performance of our Execution Services business relative to the first half.

But this apparently came to nothing, with this week them saying:

We have not completely avoided the market turbulence, with lower trading volumes, particularly in small-cap and AIM stocks

The cashflow is poor but not extrapolatable to the future, as:

The business maintained a good cash balance at the year-end of £27.4m, having decreased from £76.7m as at 31 March 2022. This is largely due to the settlement of amounts attributable to the period before the IPO, in addition to investment in the trading book and payment of the dividend in July 2022. We have now completed all non-recurring payments due in relation to the period before the IPO.

At H1, they said:

Healthy cash balances of £41.4m

A further £3m of debt was repaid in H2, but clearly, it is prudent not to pay a dividend. They can comfortably survive a couple more years of these market conditions, but the question is how strong the recovery will be when it comes and how much of the benefits will accrue to shareholders rather than staff.

That’s it for this week. Have a great weekend!