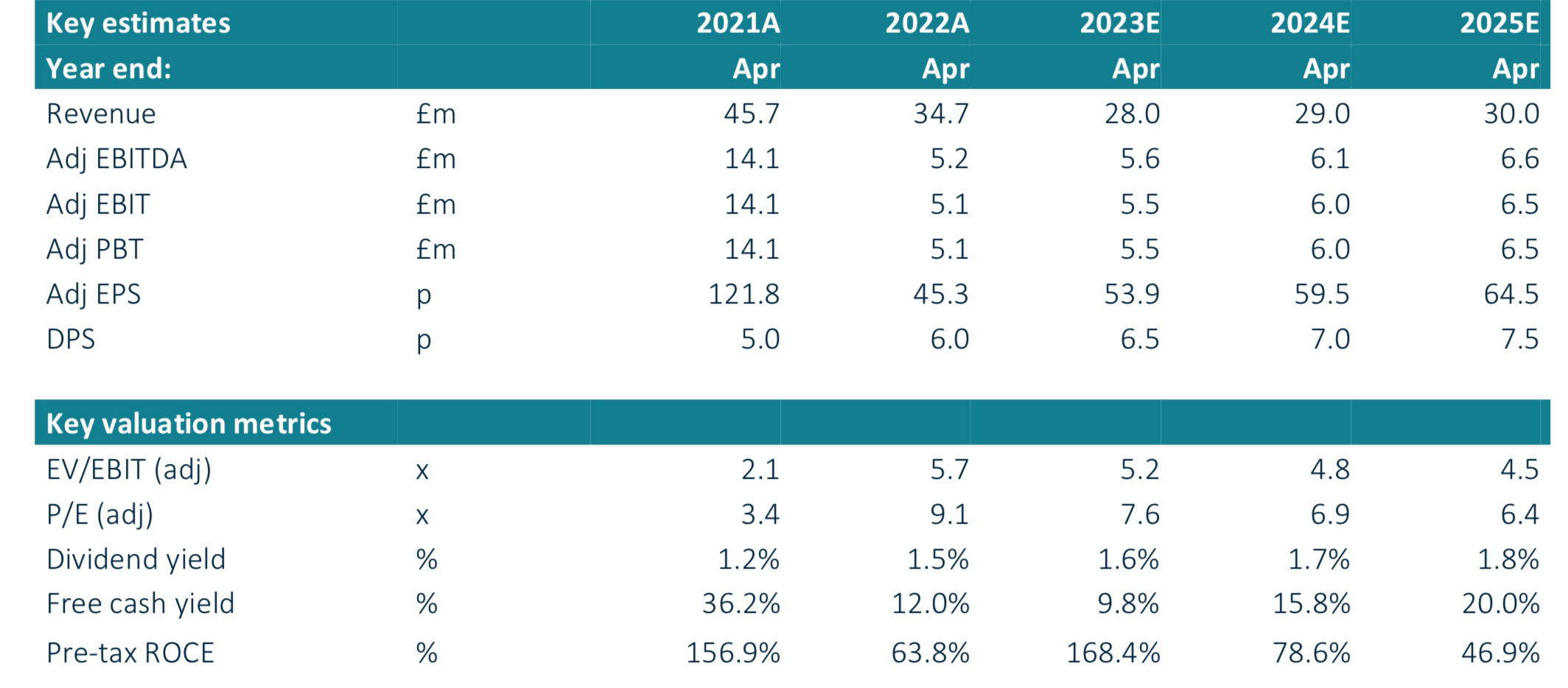

Small Caps Live Weekly Summary

Behavioral Biases KETL BOTB STAF PTY INL PDG AGFX BSE CTO

One of the biases that we all suffer from as investors is that we overweight the first piece of information we receive about a company. When combined with confirmation bias - the tendency only to seek confirmatory information - it can lead us to be dangerously miscalibrated. Particularly if the first thing we read about a company is the broker’s note.

Compare, for example, how Strix (KETL.L) reports this week’s Pre-Close Trading Update and how their broker Equity Development interprets this.

Strix:

Strix is continuing to implement a range of strategic initiatives in order to minimise the impact of the headwinds it is facing. These include a new internal restructuring programme and a focus on the reduction of inventory in order to maximise cash generation for the Group.

Translation - We are going to have to fire people to stay competitive.

ED:

Cash levels will be boosted as the supply chain relaxes post-lockdowns, enabling the Group to reduce inventory levels, and marketing expenditure is likely to decline.

Strix:

Strix is focused and committed to returning to its core operating model of being highly cash generative with no further M&A activity or investment into new factory builds, significantly reduced capex and working capital over the medium term.

Translation - we can’t afford to buy anything else or invest at the moment

ED:

The focus is now on revenue generation and shorter investment payback periods.

Strix:

The Group's net debt(1) was £87m as at 31 December 2022. Capital allocation decisions will prioritise debt reduction with a clear plan to get net debt / EBITDA to below 2.0x during 2023 and the Board is currently reviewing the level of the final dividend and further details will be provided at the Preliminary Results.

Translation - we are cutting our dividend

ED:

We reduced our dividend estimates in early December, reflecting the level of indebtedness but this still suggests a highly attractive yield of 7% for FY22, rising to 7.6% in FY23.

To be fair to Equity Development, they are doing exactly what they are being paid to do. Their disclaimer says that their notes are marketing communications. Brokers’ notes can be useful sources of additional information about a company. The problem arises is if an investor first (or only) reads the note rather than going direct to the source. Always read the real announcement first. Otherwise, you are putting on a permanent pair of rose-tinted spectacles.

In unrelated news, Mark is currently googling to see if the name Pig Lipstick is taken, in case he wants to start his own paid-for research house.

Best of the Best PLC - Half-year Report

Revenue of £13.65 million (H1 2021 £19.12m), significantly greater than the £7.60 million delivered pre-pandemic in H1 2020, the most appropriate comparative period

And:

Profit before tax of £2.71 million (H1 2021: £3.04 million), again greater than the £1.38 million generated in H1 2020

However, earnings are strong, especially as they are higher than H1 last year:

Earnings per share 27.95p (H1 2021: 27.26p)

It seems that they have cut one of their games:

As previously reported, in order to put the business in a better position for the reduced levels of revenue post-pandemic we have made changes to the product line-up, re-balancing our three principal weekly competitions - to two enhanced ones with an additional 'Friday Fun' competition under trial. We are pleased with the results of these changes, which have enhanced margins and make the business better operationally geared for future increases in revenue.

Their broker, finnCap, have more details:

In response to changing market conditions, the two mid-week competitions have been consolidated into one at a loss of c.£4.0m pa of revenue, which is reflected in our new forecasts, but there is no impact to EBITDA.

Overall, they say:

Trading since the period end has continued in line with our expectations.

And finnCap leave forecasts unchanged:

Even on unchanged forecasts, that FCF yield does make the company look very cheap if it is realistic. Doing our own basic calculations: annualising the H1 earnings, in a business with little seasonality, would be 56p, and distributable cash is probably around £2.5m or 30p per share. If you said a P/E of 10 then that’s around £6/share as a very undemanding price target. finnCap keep theirs at £9.90.

On the downside, we still don’t have any details on the GIL “Licensing and Distribution Agreement and a Marketing and Collaboration Agreement”, and finnCap now expects this with results in June. And no dividend was declared (they don’t normally declare an interim dividend, but do sometimes do a special), and we have management that sold most of their shares for £4. Still, the low valuation is likely to trump these concerns in the short term.

Staffline Group PLC - Trading Update & Notice of Results

There’s a bit of Partridge about this trading update due to the number of times they mention ahead of expectations, for example:

cash flows substantially ahead of market expectations.

Because when you look at the numbers in isolation:

To the untrained eye, this could look rubbish and that they haven’t bounced back!

Revenue growth is just 0.4% in a wage-inflationary environment. And cash is down even though they say it was forecast to be lower, with good reason due to the repayment of government support, but still down. Operating profit isn’t too bad, though:

underlying operating profit marginally ahead

However, this is clearly a revenue miss, (Liberum were forecasting £974m in August and they did £947m), which they make no mention of.

PeoplePlus still looks a risky business, as it is reliant on government contracts:

Certain funding claims made by PeoplePlus for services delivered in 2020 and earlier years are now the subject of a dispute. While we are vigorously defending our position and the final outcome is uncertain, we have decided to provide £2.5m which, based on the legacy nature of the item, has been recorded through reserves.

The outlook is cautious too:

Looking ahead, we expect the macroeconomic headwinds to persist. Low unemployment will continue to constrain volumes in PeoplePlus' Skills and Restart businesses. While we expect to grow market share in the competitive temporary labour market, the Recruitment divisions will not be immune to the broader short term market challenges, where data is showing that demand for permanent recruitment is weakening.

In the context of current expectations for the UK economy, the Board has adopted a cautious approach to FY 2023.

Which broker Zeus translates as:

Market conditions in FY23 are expected to be more challenging, with some softening of recruitment demand – as such, we trim our forecasts, reducing FY23 and FY24 underlying EBIT by 25.5% and 23.2%, respectively.

2023 EPS falls from 5.2 to 3.4p, growing to 3.9p for 2024.

A small net debt is forecast by 2023 year-end, but with their large fixed-rate debt facilities in place, Leo thinks it opens the possibility of dividends, share buybacks or earnings-enhancing M&A. On the InvestorMeetCompany presentation, the management said that they have:

Potential firepower to take advantage of any opportunities that may arise.

And hint at buybacks later in the year. Mark is more cautious and would want to see that balance sheet before being confident of that assertion. Potentially, all of those factors that have led to better cash balance are reversible or vary during the year. In addition, they are likely to have window dressed for year-end, and the turnover is so large they could easily have very large monthly swings in debt.

Overall, their IMC presentation had a positive but appropriately cautious tone regarding FY23. There's plenty of potential here, but on an FY23 P/E of around 10 doesn't look particularly cheap, given the uncertainty.

After this trading statement, the CEO bought £16k worth. However, his total holding is currently valued at £165k versus his total 2021 remuneration of £749k. So perhaps not a ringing endorsement. The EBT has been a more aggressive buyer, however, taking £165k worth.

Parity (PTY.L) - Trading Update

This doesn’t look great:

Net Fee Income for FY2022 expected to be £3.5m compared to £4.1m in FY2021.

However, EBITDA is recovering somewhat:

Adjusted EBITDA(1) for FY2022 expected to be circa £0.4m vs £0.1m in the prior year.

Well, on an adjusted basis, at least. They scrape a profit out of it by selling and leasing back the trademark to their own name. When you think through the heart of the transaction, they get cash in the account today in return for future payments they make, and if they default, they don’t have a business. That’s a long-term loan in our book. To anyone but the accounting rule-makers, this is unsecured lending that they manage to put through the income statement as a profit!

How on earth this retains a £7m market cap is anyone’s guess.

Inland Homes (INL.L) - Sale of Strategic Land Portfolio & Trading Update

We can see why the CEO scarpered after only a month in the role:

As a result of the items referred to above, the expected loss before tax for the year ending 30 September 2022 is now approximately £91.0m and the net assets at the balance sheet date approximately £90.0m, which represents an IFRS net asset value of approximately 40p per ordinary share, which excludes any EPRA uplift.

So a £91m loss is half their NAV. In one year! Leaving them needing banking covenant waivers.

The share price is down to 10.75p, which with 40p of NAV, makes them look incredibly cheap. The problem is that the debt is a fact, and the assets are a matter of opinion. And any ongoing losses from housebuilding will erode those further. This is only for the very brave or those able to assess the future value of their land bank accurately. i.e. not us.

Pendragon (PDG.L) - Full Year Trading Update

We already know that trading in calendar Q4 was better than it was reasonable to expect earlier in the year. The last update to Pendragon's forecasts was a cut to EPS of around 10% after Russia invaded, and there have been no upgrades since. In contrast, Lookers and Vertu have been upgrading throughout the year. So this can't be much of a surprise:

Overall financial performance for the fourth quarter of FY22 was slightly ahead of the Board's expectations, with a strong underlying trading performance more than offsetting higher operating and interest cost pressures.

Nor are the reasons - Q4 was a sweet spot of increasing supply and stable prices:

Trading during the quarter was underpinned by strong volume growth in new cars, with the Group delivering like-for-like volume growth of 4.6%, and outperforming the retail new car market growth of 1.0%. Used car volumes also grew by 5.2% on a like-for-like basis in Q4, a notable improvement on the declines seen in the third quarter.

As a result:

As a result of this performance, FY22 Group underlying profit before tax is expected to be approximately £57m (FY21: £83.0m), slightly ahead of market expectations1.

1 Market expectations based on an average underlying profit before tax of £54m and a range of £53m to £55.3m for FY22, as at 24 January 2023

Zeus thinks this translates to an increase from 3.1p to 3.2p EPS. Surely it must round quite close to 3.3p. The impression Leo gets is that while new car sales (which can't be recognised until delivery) will continue to rise at least through H1, we are now finally past the best as regards used car pricing. So it is the outlook that is of most interest:

We expect constraints in both new and used vehicle supply to continue into 2023, however, the new car order bank remains strong and there are some early signs that new car supply may be beginning to improve which we expect to drive growth in new car volumes during 2023. We expect our ongoing initiatives and growth opportunities to more than offset operating cost inflation within the business. Accordingly, the Board remains confident in the prospects for the Group in the year ahead.

Zeus cut forecasts for 2023 and 2024 last week and, as you would expect, do not adjust them again this week. A rise in interest rate costs was behind the FY 23 EPS cut from 3.1p to 2.7p, which still stands.

Pendragon shares fell from 28p to 18p on the collapse of the takeover offer, apparently due to a legal claim on their software business, but have subsequently recovered to 20p in line with the market. That leaves them more expensive than Vertu on pretty much every measure.

There also seems to be some sector strength due to general takeover speculation triggered by a sector report from Zeus that is covered here. However, the same arguments have been made several times over the past few years, although one-off benefits from used car shortages have made historic valuations look especially cheap.

Argentex Group PLC - Trading Statement

Argentex reports strong revenue growth:

trading has remained strong and expects to report nine month revenues of £41m, a 63% increase compared to the same period last year (FY2021: £25m)*.

But we are not convinced it really has much to do with their execution, merely strong markets after Truss/KamiKwasi FX volatility.

Argentex continues to focus on its customer service proposition by attracting market-leading talent. In line with its accelerated growth plans, Argentex will continue to invest to double the footprint of its UK and European headquarters over H1 2023.

So does this mean costs are doubling to deliver the 63% rise in revenue? They don’t mention profits in today’s update (although it is a 9m one, not the FY). We remain sceptical.

Base Resources (BSE.L)- Quarterly Activities Report

First up, the mining rate exceeded Mark’s expectations, as did the production:

He had expected more like Dec 22 figures, and of course, rutile and zircon are the most valuable products. However, the pricing achieved is below his expectations:

And here they say:

Rutile prices experienced further gains while ilmenite and zircon prices declined. Subdued conditions in most downstream markets are applying downward price pressure across all products for the March quarter, however demand for most products is expected to stabilise and provide a steady footing for future prices.

So we can expect pricing to be a little weaker still in this quarter. However, there is a large element of mix in this result. Just 21% of sales were higher value Rutile and Zircon in the quarter versus 30% for the record $740/tonne achieved in the March quarter of FY22. Sales volumes are down, but this is simply the timing of shipments. In the last six months, they have stockpiled 33.8kt of Ilmenite, 9.5kt of rutile and 2.8kt of zircon. This is over $30m of product that has gone into inventory and will likely be shipped in 23H2.

Costs are slightly high but not out of the ordinary at $19.3m. Overall this means that they should have had a very similar performance to Q1, with FCF of around $23m for the quarter. Going forward, production will reduce due to blending lower grade North Dune ore in. This means that profitability reduces but lasts longer. If we assume they catch up with shipments and hit production targets, H2 should generate a further $67m of FCF.

So why were the shares down 6% in Australia on this news? It is hard to believe that it is the pricing. After all, Kenmare missed their production targets, have the same pricing outlook and the share have been strong on their quarterly ops update.

In summary, as at 31 December 2022, the Company had net cash of US$60.2 million consisting of cash and cash equivalents of US$60.2 million and no debt.

Despite recording strong sales in the quarter, the Company’s net cash position decreased, primarily due to Bumamani Project implementation expenditure, corporate tax instalment payments, dividend withholding tax payments and the majority of the sales occurring late in the quarter, leading to an increase in receivables of US$17.2 million.

By Mark’s estimates, using the figures from the activities report, Kwale will have produced c$22m of Free Cash Flow in the quarter after $9.9m of capex and paying 7% royalties and 15% tax on profits. Given that cash went down from $73.1m to $60.2m, this implies a cash outflow of $34.9m in the quarter, of which $17.2m went into working capital. They also spent $0.4m on exploration and $2.6m progressing Toliara, and corporate costs are usually about $2m per quarter. This implies that around $13m of cash taxes were paid in the quarter above the standard tax charge and royalties. The company has confirmed that a good chunk of this is a dividend withholding tax on cash that is leaving Kenya to the corporate coffers. This means we can either expect another large dividend to be declared next month or for the Madagascan government to finally agree on fiscal terms for Toliara to progress. Either of which should be well-received by the market.

TClarke (CTO.L) - Trading Statement

Good second half trading here:

The Board is pleased to report that trading in the second half of the year has continued strongly and that the Group's financial performance for the full year is in line with market expectations.

Our order book has now increased to £555m (2021: £534m).

This is what we really want to know:

our average month end net cash during FY2022 was £2.6m

The Group is expecting to achieve its target turnover of £500m in 2023.

This is on a P/E of 6x, so very good value. The worst EPS in 6 years was in 2017, at half current levels, so even if that repeats, they are not expensive. Yield is 4.3%. Forecasts were for a tiny increase in EPS on an increase from £410m to £500m turnover, although some of this will be down to tax. Also, that jump is quite big compared to the increase in the order book. However, they did beat on revenue, which came in at £425m. Although, the order book is clearly multiyear and so timing will vary.

Cenkos 2022 adjusted EPS forecast increased from 19.0p to 19.3p, but 2023 from 19.7p to 18.9p on a higher interest charge. We have seen brokers for a number of companies reduce forecasts due to a higher interest rate charge recently, but the process is by far from incomplete. There are also quite a few companies that stand to benefit from higher rates.

Overall a reassuring and positive update for those that had done their sums on interest rates. The big downside remains the very high board pay. In 2021 the dividend cost £1.9m, whereas the board cost £2.9m. If board pay was half this figure, PAT would be some 20% higher.

That’s it for another busy week. have a great weekend!