Small Caps Live Weekly Summary

DSM VLX GDP BSE SDG CAPD CMCX MPAC

There was no large Caps Live this week so we go straight in with the small caps.

If you didn’t get a chance to listen last week, check out Mark on the Capital Employed podcast talking about how he invests, including a couple of small cap ideas.

Small Caps Live Wednesday 1st September

Downing Strategic Microcap Fund (DSM.L) – Investor Letter

Downing Strategic are one of very few listed microcap investment funds. The reason they are one of very few is, of course, that the whole concept of a microcap investment fund doesn't tend to work. At the moment this invests mostly in mid-caps, debt and unlisted equity!

Just because they tend to be terrible performers doesn't make their Investor Letters not worth reading though.

Although that chart looks like a backward tick, in this week’s investor letter they claim it is the start of a forward tick, or as people like to say nowadays: a J-curve.

We feel we are through the trough of the J‐curve we endured at the beginning of this investing journey. Boards have been reshaped, strategies refocused, and tough positions exited with the proceeds recycled. As we own more vintages of investments, future J‐curves are unlikely to be correlated going forwards, reducing drawdown;

Investors have often noted that Downing Strategic was best followed with a 6-month lag rather than investing directly in the fund and they now seem to be admitting this themselves. Although the lag is more like 3 years. In many ways, this is a demonstration of how private investors can outperform by choosing when they buy, rather than having to wait for an "event".

Their only significantly strong performer has been Volex. Here Judith got in at the right time and for the right reason, as well as getting the right result. And Leo certainly has to thank her for explaining her reasoning to him personally. Downing spends most of their time in the letter explaining why this has much further to go.

VOLEX continues to impress us, so much so, that we have been adding modestly to our position on bad days – the market is becoming impatient, and we are more than happy to take advantage of this.

So, it is understandable that a micro-cap fund might want to hold their best performer as they become a mid-cap, but to continue to add...? Perhaps they'll give up the whole microcap investing thing? Anyway, they say:

We are also bullish on the recovery within healthcare, with management signalling run rates now at or exceeding pre‐Covid levels

Weak healthcare sales in many areas, as healthcare collapsed, has been one of the unexpected outcomes of COVID-19. We got caught out on this with Medica in the early days. Bioventix is now potentially being hit by a claimed worldwide medical glassware shortage. So perhaps it is coming to an end as healthcare systems adjust.

As the valuation rises, Volex has now become a rollup:

Finally, and perhaps the most eagerly awaited, is further bolt‐on M&A. We think the most likely scenario here this financial year, if not this calendar year, is an acquisition (or several acquisitions) similar in size to DE‐KA (i.e. around $60 million of revenues) at around the 10% adjusted operating profit level, with Volex likely to pay in the region of 6‐7x adjusted operating profit, or perhaps slightly more for a higher growth and quality asset. It seems reasonable to assume therefore that a further $6+ million of annualised operating profit could be brought into the group in short order.

But it was by buying too many companies and going into lower margin business that got themselves into the mess that needed Downing's investment in the first place. So, we may have an unstable situation here.

We were also very concerned when the CFO left, as it was him and the COO that were effectively running the company. Investors have always been concerned with Nat Rothschild as Executive Chairman as we have discussed this at length in the past, too. In this context, I think the share buys by the COO are extremely relevant:

Volex plc (AIM:VLX) was notified on Friday 27 August 2021 that Mrs Sharon Molloy, wife of John Molloy, Chief Operating Officer, purchased 61,000 Ordinary Shares of 25 pence in the Company ("Ordinary Shares") on 27 August 2021, at an average price of 390 pence per Ordinary Share.

This suggests to be that he is

a) still running the show rather than being side-lined; and

b) confident about the outlook.

Downing's letter seemed to support the share price yesterday and the above this morning. And I think there is some logic in that. But, as with Victoria Carpets, we don't like rollups, seeing them as inevitably unstable. If they are on low ratings, then maybe. But this isn't any more.

Goldplat (GDP.L) – Sale of Kilmapesa

Goldplat finally get their Kenyan mine transaction over the line:

Goldplat has received 103,846,154 shares in Caracal (representing 7.17% of its issued share capital) as consideration for the sale of Kilimapesa, to be held for minimum of 12 months. In addition, the Group is due to receive a further cash payment of USD450,000 in the next two weeks and is also entitled to a 1% net smelter royalty, limited to USD1,500,000, of which circa USD14,000 is already payable.

Caracal Gold has a bid-offer of 0.95-1.0 making their stake worth about £1m. So looks like they did the right thing by not demanding cash payment in lieu of shares. I can’t help thinking that if Caracal is valued at £15m and effectively holds a recapitalised Kilimapesa mine, that Goldplat has missed a trick not floating this themselves.

Still, this way is lower risk and should accelerate the return to paying dividends, which is what shareholders really want from the cash-generative gold recovery ops.

Base Resources (BSE.L) – Final Results

Base Resources issued final results on Monday in Aus, so these were released in the UK on Tuesday. We looked at these in scl on the 4th of August following the Q4 Ops update and could largely forecast the outcome. Free Cash Flow was slightly lower than we forecast but due to slightly higher investment and a working capital build due to shipments of HMS occurring late in Q4, and hence payment being made into 22Q1, but this is nothing to be worried about.

Perhaps the biggest surprise is the size of the dividend payment here:

With net cash of US$64.9 million at the end of the year and the timing of the Toliara Project final investment decision still uncertain, the Board has determined a full-year dividend of AUD 4.0 cents per share (unfranked), totalling US$34.2 million, which will be paid wholly from conduit foreign income. This will bring total dividends in respect of FY21 to US$60.8 million, representing AUD 7.0 cents per share (unfranked).

AUS4.0c is about 2.1p so the final dividend alone represents a 12% yield. 21% on the full-year dividend, even after a 10% or so rise in the share price in response to these results.

Of course, this is unsustainable. When they get approval to move forward with Toliara then the cash will go to develop the new mine, although the equity portion of the funding is likely to come from a Joint Venture structure with existing customers. They said that discussions with counterparties for the JV have become more intense, due to limited forward supply in the market and ongoing demand from economic recovery post-COVID. Which bodes well for pricing going forward:

(These are from their results presentation.)

I think it is also worth considering what the capital market cycle looks like for Heavy Mineral Sands. New HMS capacity is required but, like a lot of mining, the CAPEX has not been put into the sector globally for the last 5 years or so and it takes 5 years of planning & construction to develop greenfield sites. South Africa has faced production issues and Vietnam & India are not coming back on stream for political reasons. And the only world-class resource that is in advanced planning and that is Toliara, which has been delayed.

There is another world-class resource that is a few years behind Toliara in planning which is owned by listed Bluejay (JAY.L) in Greenland but it is: a) poorly located for Chinese customers b) is planned to produce at half the rate of Toliara Phase 1 and c) only has a PFS not a DFS so is a couple of years behind Toliara even with the lack of activity on the ground in Madagascar over the last 18 months. It is worth noting, however, that Bluejay has a market cap of $165m as an explorer.

Then we have Kenmare (KMR.L), have increased production by adding an additional Wet Concentrator Plant last year but this has easily been accommodated by the market. They are obviously in production, but producing at a level that will be similar to the final rate at Toliara with the same very long LoM. Toliara is cheaper due to the much higher grades. Kenmare has a $700m+EV and still looks reasonable value at that valuation.

In the near term, ilmenite might see a limit to price rises as informal Chinese supply becomes economic but this is generally lower quality. So this may prevent price spikes but it is unlikely to dampen prices below the current level, merely limit the rises.

So all indications that current HMS prices are largely sustainable or on an upward trajectory, barring any severe global economic demand shocks.

For Base increased production targets for FY22 plus this pricing environment means that we could easily see $100m of FCF from Kwale, even after paying group costs and slightly increased capex requirements, but excluding any working capital flows or cash going into Toliara development.

So, if Toliara isn’t progressed in FY22, we could see a further 6p dividend or 35% of the current price if they choose to pay out all FCF as dividends.

Of course, Kwale has a very limited Life of Mine. Recent news of license extensions and the PFS released later this week showing the ability to mine a small but high-grade area close to the existing infrastructure should push production out to the end of FY24. However, they are looking for further sources of material in Kenya. I've got to say that I have been a bit disappointed with the near exploration. Not least since they have faced issues with land access and leases.

It is notable that Tanzania has issued explo licenses over the border while they are still waiting in Kenya. This is despite Base being a large proportion of the Kenyan mining industry, and one of the major employers in the region.

So they now have explo licenses about 80km away with high prospectivity. Mark quizzed the management on this, assuming they would move the plant, but they seem to think that this was not a good idea and they would add a concentrator or pre-concentrator locally and truck to the MSP plant. This sounds expensive but they are pretty good at only doing things that generate the right economic return. Given that Toliara has world-class grades and has a Life of Mine of 50 years+ then if they extend Kwale then that is simply a bonus at current valuations.

Sanderson Design Group (SDG.L) - Direct-to-consumer brand

Sanderson Design Group PLC (AIM: SDG), the luxury interior design and furnishings group, announces the online launch today of a new brand, Archive by Sanderson Design, which will be sold from a dedicated brand website and also, from next month, through an exclusive retail partnership with Selfridges, the leading international fashion retailer.

The Archive by Sanderson Design brand reinterprets heritage designs in inventive compositions and elaborate colourways for a fashion-forward, maximalist audience who are not currently served by the Company's existing brands or routes to market.

Clearly, distributors take very high margins on their existing model which is an impediment to direct sales. So this is a good way to go online, introduce some price discrimination and have more control of their own destiny.

The long-term trends are with this company. Although at 17x Forward Earnings this may largely be in the price. They have certainly been more promotional recently with 7 RNS-NON announcements in 2021, whereas they barely made any before 2020. It may indicate a ramp-up in activity or merely a ramp-up in promotion. We’ll leave readers to judge whether they think this is a good thing or a bad thing.

Small Caps Live Friday 3rd September

Capital Limited (CAPD.L) - Broker Upgrade

A broker upgrade wouldn’t normally be worth commentating on but given that we still believe that this company offers exceptional value we tend to track it very closely. In light of our comments about the capital market cycle above it is also noteworthy what Capital’s competitor Major Drilling said on their recent results call:

I'm confident that the cyclical recovery is well underway, and we will continue to see increased activity in the industry...As a management team, we are confident in our belief that the industry is still very early in a long cyclical upturn.

They go on to give much more detail on why they think this is a multi-year cycle analogous to 2004-2012:

So when we reached 2004, both precious and base metal companies were facing serious reserve issues brought on by that lack of exploration over the prior 6 years. That created an upcycle that lasted 8 years between 2004 and 2012, of course, temporarily interrupted by the financial crisis.

It is Peel Hunt that has upgraded, saying:

The CAPD team look well set to capitalise on a strong drilling market through the enlarged fleet, driving a significant increase to our 2022E estimates. As a result our target price increases to 115p and we retain our Buy recommendation.

That said I think they miss a couple of things. The first is that their fair valuation metric of 3.1x EV/EBITDA is based on the assumption that we are close to peak cycle, and this is at odds with what the industry is saying. The second is that they don’t break out MSALABS separately in their valuation. Since this generates little EBITDA, then little value is attributed to the business. However, in the latest H1 results then Capital have started breaking out the MSALABS revenue:

(H2 estimates are based on company comments from conference calls.) So this is growing sales at 100%. For fun, I looked at what the median TTM Price-to-Sales was of listed companies growing at a similar rate and it came out at 15x. Applying this to MSALABS gives a valuation of $170m, of which Capital hold 75%. Of course, I don’t think this is worth that much, but it is not worth the close to zero that brokers are valuing it at.

In general, it is good news when brokers are behind the curve.

CMC Markets (CMCX.L) - Trading Update

It is much less good when a company itself is behind the curve on their trading. In CMC Market’s case, in their Q1 Trading Update on 29th July they said:

As previously stated, whilst client trading activity has moderated from average FY 2021 levels our latest client cohort continues to show characteristics similar to those of clients onboarded over prior years. In addition, client income retention remained in excess of 80%, but below the levels reported for FY 2021, as previously guided….As a result, the Board remains confident in achieving net operating income in excess of £330 million for FY 2022.

So quite a change in outlook to be saying this, only a month later:

As a result, should current market conditions prevail for the remainder of the year the Group now expects FY 2022 net operating income to settle in a range between £250-280million.

We clearly called this one wrong and although we clocked from the poor trading at Best of The Best that this sort of business was facing short-term headwinds, and personally felt the low volumes and lack of interest in investing over the summer. However, we were also assuaged by the company re-iterating the >£330m NOI guidance in July.

They are facing two factors together here. Lack of trading plus lower hedging gains:

In addition to lower activity, year to date client income retention has also been tracking moderately below the targeted 80% although is expected to recover through the remaining seven months of the year based on a reversion towards historical averages in the mix of asset class trading.

The trouble is that the outcome was and remains very uncertain. And the management had consistently beaten forecasts for some time. Under these circumstances, they were unwilling to admit that to the market that trading had deteriorated until it was significant. Basically, they'd promised us £330m and wanted to stick to that. We like to call these the Wiley E. Coyote moments - where trading has fallen off a cliff but gravity hasn’t yet appeared to impact the shareprice.

Apart from any lessons learnt, dwelling on the past is rarely useful in investing. So what interests us now is if a) CMC Markets is a buy or a sell at the current price and b) which companies are likely to face a Wiley E Coyote moment in the future.

With a mid-case revenue then we get 22p EPS for FY22, which largely matches updated broker consensus. The challenge here is that the costs remain elevated since they have been adding tech development headcount. So that is a big decrease in EPS. But then you have a very large amount of product development going on that is being expensed not capitalised. If this was an industrial company launching a new product, the factory and all the production equipment would be a capitalised cost, and only a small amount of additional SG&A would be expensed. If you kept costs at FY20 levels and assumed the rest was growth capex then EPS would be more like 31p. If they deliver on their aim to take on Hargreaves Landsdown and AJ Bell, then buying below £3 looks good value.

This brings us to b) - the next companies to fall off a trading cliff. Direct competitor IG Index has fallen on the CMC Markets news so perhaps represents less opportunity. However, it is noteworthy that CMC talks about both leveraged and non-leveraged facing reduced volumes. So the stockbrokers could be next to report the effect. Hargreaves Landsdown is now on c25x earnings having had a wobble following results outlook in August:

However, AJ Bell has yet to have any update to brokers for this effect:

And indeed, their broker consensus looks remarkably similar to CMC’s prior to this week’s news:

The last trading update from AJ Bell was on the 22nd July for Q3 ending 30th June. AJ Bell is also on a P/E of 40, which looks anomalous compared to Hargreaves's now 25 too. So are AJB due to disappoint shortly? And could we see a major rout in the share price given the very high multiple?

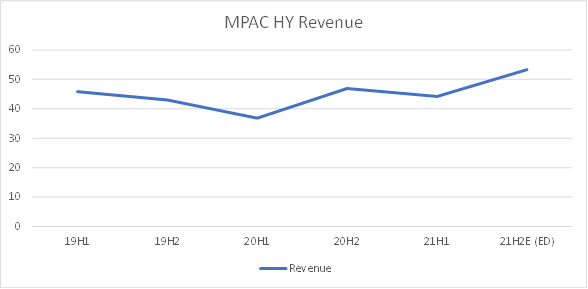

Mpac (MPAC.L) - Half-Year Results

Mpac has had a fantastic turnaround since they disposed of the cigarette packing business. It also survived the coronavirus crisis very well for a company that depends on capital equipment expenditure. In 2020 revenues were only down a few per cent. And now they have returned to growth at the H1 stage:

Group revenue of £44.2m (2020: £36.8m), with a 25% growth in Original Equipment revenue and continued progression in service revenues

But even more importantly:

Strong commercial rebound with a 69% increase in order intake to £51.7m (2020: £30.5m)

There wasn't much about post-period end trading in the statement, but the presentation makes it clear this was very strong, with momentum further building, if anything. These H1 results were achieved despite a number of headwinds that are already unwinding and will continue to do so throughout H2 and 2022H1:

* Weak EMEA due to covid

* Weak healthcare and pharma due to covid

* Weak service revenues due to covid

On top of this, they have the potential new stream of battery packaging business. This was elaborated on in the presentation where it was clear the CEO was positively excited about the prospects for further near-term sales to FREYR and also medium-term sales to other manufacturers which they are already in discussions with.

Furthermore, they have spare cash and loan facilities to make earnings-enhancing acquisitions.

None of those last two bull points are factored into the following EPS forecasts:

2021: 32p, 2022: 35p, 2023: 37p.

So on the surface, the 630p share price is just 18x 2022 earnings for a company that has continuously beat expectations and has considerable "hidden" potential.

However, is it actually growing? Well, no. In the results call, management admitted that their like-for-likes are slightly down. Not that this really matters in the current market, where headlines matter not reality. Similar to lunch, like-for-likes are for wimps.

The short-term future growth forecast in revenue isn’t that impressive either when you consider the acquisitions made:

It looks even worse when you look at the bottom line:

This also highlights, what they report as underlying profit after tax. Even if you think it is fair that they exclude acquisition costs & amortisation of acquired intangibles despite being a serial acquirer, or that the excluded one-off reorg costs appear to be far from a one-off, then I think there is still one set of costs that shouldn’t be ignored: the pension deficit.

“But surely this is now in surplus?” I hear you ask. Yes, on an accounting basis. However, an accounting basis means almost nothing. Again in the conference call, and only when pressed, did the CFO reveal that the actuarial deficit is £35m. This is why they have to keep making £3m or so of recovery payments each year. This is real cash that goes out of the company each year so the profits should be adjusted for these payments in my opinion. (Or the £35m deficit considered as a debt.)

Then there are the pension admin costs. These are ongoing, regular costs that will last as long as the company has a pension fund so excluding these seems to border on the daft. When asked about this on the call the company said that it was because they hope to get a buyout of the pension fund.

Well, Mark hopes to be crowned Miss Universe one day, but being a middle-aged man, the odds are against him. About the same odds as Mpac getting a buyout of the fund at the moment. The way it works is that the buyout valuations are more conservative than actuarial deficits, which are in turn more conservative than accounting valuations. So it would probably cost them somewhere in the region of a £50-100m payment to get rid of the pension scheme now.

When you take these ongoing payments into account this is what the real EPS figures look like:

So you see, it takes them until 2023 to exceed the real underlying EPS that they did in 2019 when they traded at a share price between £1-2.

In this light, you now have a company:

a) On a real forward P/E of over 40

b) Not growing revenue recently without acquisition.

c) Not forecast to be growing profit after tax in the near term.

d) With a management team that tend to gloss over the negatives and only mention the positives.

Doesn’t sound so great does it?

That’s it for this week, have a great weekend all.