Small Caps Live Weekly Summary

BILN CAPD GATC NXQ RFX RWA

A strange week, with a sell-off in the US damaging what appeared to be the start of a recovery in UK small caps. Here’s some of the news we covered:

Billington Holdings (BILN.L) - Final Results

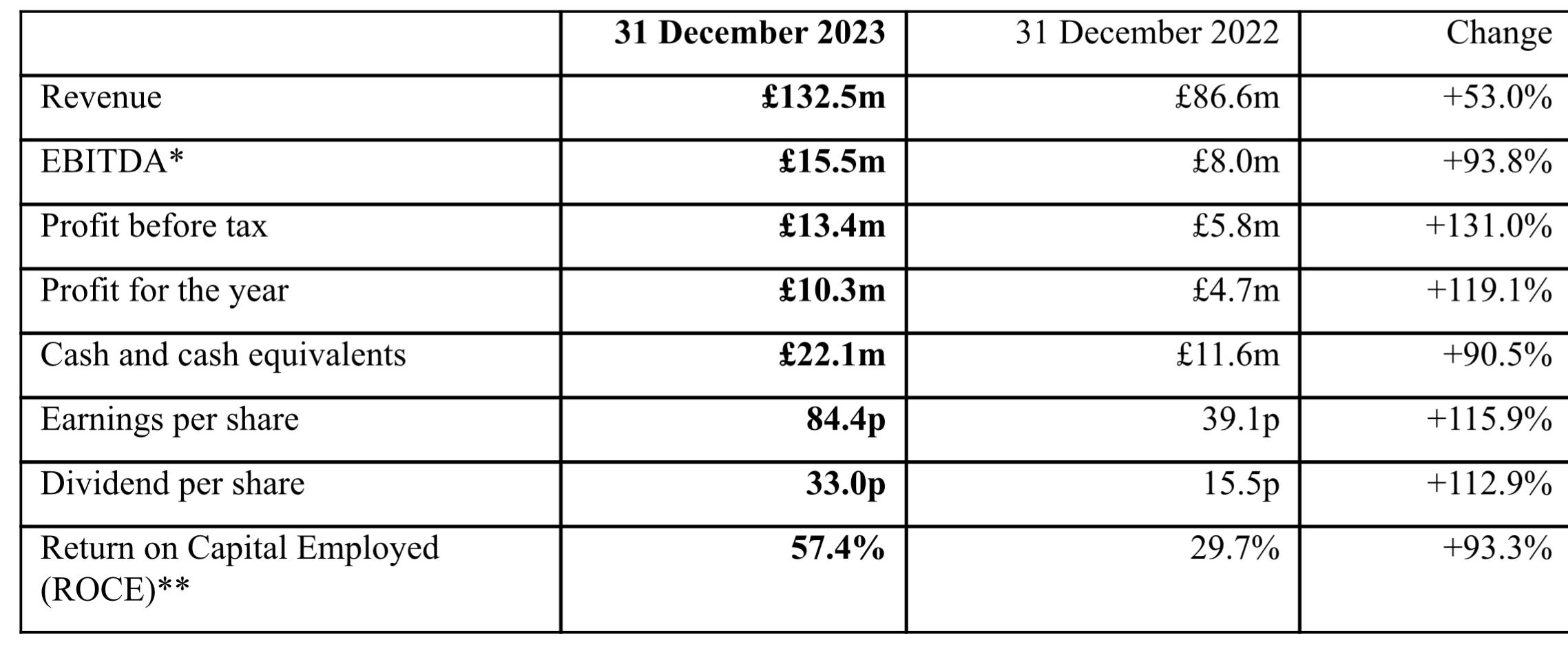

These results look phenomenal:

These are the sort of increases we are used to seeing from small software companies on a P/E of 30+, not a structural steel company. Perhaps the clue that this isn’t a tech company is that this growth is largely organic and that the word "adjusted" does not appear in these results.

However, some of this performance is from one-off gains from price rises on quoted work coming in lower than expected. Pretty much every area of the business is performing well too:

Billington Structures performed exceptionally in 2023, driven by a number of high value contracts across a variety of sectors including high tech manufacturing, data centres, energy from waste, distribution and commercial office developments...

Peter Marshall Steel Stairs continued the strong performance seen over the past three years, recording record revenues for the year…

Hoard-it enjoyed a record year in 2023, as it continued to expand and diversify its offerings…

Specialist Protective Coatings (SPC)’s …performance was ahead of management's expectations in 2023 and the Company enjoyed its first year of profitability. With SPC operating at full capacity for the foreseeable future we expect it to continue to deliver a strong performance.

This was the only bit that was not firing on all cyclinders:

The Easi-Edge perimeter edge protection and fall prevention business faced a challenging period in 2023, although it remained a significant contributor to Group profits.

The markets are still described as challenging

We are conscious that many of the main construction contractors continue to operate under significant pressure, with a number ceasing business in 2023, and the Group has experienced deferred and cancelled contracts.

You have to wonder how well they would have done in better market conditions. This is a period of significant capex, yet net cash still rose. Although average cash balances are less impressive:

The gross cash balance at the year end was £22,084,000 (2022: £11,634,000). The average gross cash balance during the year was £9,168,000 (2022: £7,890,000). The strong cash position leaves the Group well placed to achieve both its short and long-term objectives to maximise returns, while providing financial security and providing the ability to invest and seek opportunities for diversification.

Still, this has enabled a doubling of the dividend, although some of it is guided as a special dividend.

The outlook is strong:

we are seeing a consistent stream of opportunities at sustainable margins, and with a strong balance sheet and a record order book, I believe Billington is well placed to deliver a strong performance again in 2024.

However, this isn’t really reflected in the forecasts, with EPS going back down to 52.1p. The company says it is trading in line with these. It seems the one-off nature of pricing is proving temporary. Given the upgrades this year, it has the feel of a business that is going to beat these forecasts. But even if it doesn't, a 10x P/E with 1/3rd of the market cap in cash, despite a recent period of elevated capex, looks too cheap.

Capital Limited (CAPD.L) - Q1 Trading Update

As predicted, a weak quarter, with timing and rig moves affecting the utilisation rates, partially offset by stronger performance of the remaining contracts:

- Fleet utilisation for the quarter reduced to 66%, from 77% in Q1 2023 and 72% in Q4 2023. The reduction was driven by reduced activity at Tembo, Tanzania and continued subdued activity in West Africa, particularly Mali. H1 2024 will see a higher level of asset mobilisation and utilisation is set to increase thereafter as we move through the year; and

- Average monthly revenue per operating rig ("ARPOR") was US$202,000 in Q1 2024, up 5.2% on Q1 2023 ($192,000) and 7.4% on Q4 2023 (US$188,000). This strengthening in ARPOR is primarily the result of the ramp up of high-quality contracts, while also a continued focus on efficiency at our more established sites.

The FY guidance remains the same, which is for a decent increase versus the previous year:

While the quarter has seen a higher than average level of asset mobilisation, particularly in drilling, we are in a strong position now to see positive momentum through the remainder of the year and we remain confident in the $355 - 375 million revenue guidance we set at our FY23 results.

The market must be starting to believe them, though, maybe aided by the very strong gold price recently. The shares actually rose on the day despite going ex-dividend on the same date as the trading statement. Perhaps going up on bad news is good news for the share price at last!

Gatacca (GATC.L) - Interim Results

There is a particularly annoying trend amongst companies to subtitle their announcements. Gatacca have gone for "Focus on our core strengths”. Sadly, one of those core strengths doesn’t appear to be generating meaningful profits:

Broker Equity Development join in the headline game, going for:

Trading report in-line with sector peers.

But if you thought that going from 0.7p EPS in H1 to 6.5p for the full year would be a stretch, you would have thought right. What is missing from the note’s headline is that they have cut FY24E EPS from 6.5p to 4.7p and FY25E from 10.8p to 6.0p. Seems pretty cheeky to us to include the word “in-line” in the title of the note when the results are anything but in-line and have led to a 45% downgrade to 2025 numbers. Not only that, but this sounds like there may be further risks to these forecasts going forward, too:

We have taken a more conservative view of the outlook, reducing FY24 estimates in line with new guidance, albeit still anticipating meaningful growth in activity levels.

None of these titling games help assuage the fear that recruiters are a sector to avoid, at least in the medium term, probably always.

Nexteq (NXQ.L) - AGM Statement

When Canaccord title their accompanying note “Robust margin and cash performance” then you can be sure the revenue isn’t particularly robust!

The robust gross margin performance seen in 2023 has continued into 2024, mitigating the anticipated subdued revenues seen in the first quarter amid wider economic uncertainty.

However, maintaining Densitron's margins is good news, as their improvement was largely due to one-off price rises for their products in this sector. Ultimately, this is an in-line statement, and you wouldn’t expect any difference from the very recent results statement. The risk remains that the guided H2 weighting doesn’t arrive. Or, in the short term, that the recent enthusiastic tip buyers are less enthused when they see the H1 results.

Ramsdens (RFX.L) - Downing Overhang

In the past couple of weeks, we’ve examined some of the permutations surrounding the winding down of the Downing Strategic Microcap trust. One thing is clear: their selling in the market has acted as an overhang for a number of their holdings. One such company is Ramsdens. While we usually respond to trading updates or results as the trigger to look into the details of a business, Leo used the presence of the overhang as an opportunity to look at this company in more detail, and it’s worth summarising it here.

Here is the breakdown of their gross profit by business type:

This is a company, that should be doing well. The outlook for FX looks strong due to holiday booking levels and as per last month's trading update ("3% yoy with encouraging momentum building"). Although not the cheapest way of getting hold of foreign currency cash or spending abroad, this offer is reasonably compelling. The fee of just 1.6% on cash booked online (walk-in rates are undoubtedly far worse) would be exceptionally hard to beat even with a zero-commission card due to local cash withdrawal fees in many countries. If you're going on holiday tomorrow, then picking up their pre-paid card in a branch is almost certainly the cheapest way to pay by card abroad - charges are again 1.6% to top up, and the only "tricks" are a minimum £50 top-up and non-usage fees after 18 months. In-branch and standard-rate phone support will be of more value to some than others, but I'd say set them far apart from Revolut, etc. I suspect competition has peaked as many of them have/had unsustainable business models.

Jewellery retail probably remains the next most profitable segment and is obviously affected by consumer spending challenges, but an improved mix means gross profit was 5% ahead in the trading update. In the January IMC presentation, they said the competition had structurally eased over time as other retailers moved away from solid gold (presumably to a more Ratner 's-style offering) due to the high gold price, and some had closed after COVID-19.

Last year, they were only a Pawnbroker third (and at just 22% of gross profits), although there is the potential for this to become their second biggest business line, and clearly, it is closely related to buying gold. Unlike H&T, they don't have aggressive growth plans sucking up cash, but it is nonetheless growing, most recently in the March update at a rate of around 10% a year. Continued gold price strength will help here as it will encourage both increased gold sales and protect the value of the collateral they hold against loans.

Looking at the balance sheet, Ramsdens has no goodwill and minimal other intangibles, in sharp contrast to H&T. Adjusted for size, Ramsden's inventories are higher, but so are payables. Cash is twice that of borrowings, whereas H&T has significant debt secured on their far higher pledge book receivables. The starkest difference is the cost of debt: Ramsdens paid 2.4% over base at 30 September, and terms have since been improved (though perhaps this is a reduction in the non-usage fee), but H&T are paying up to 4% floating over base and 8.4% fixed (3% over current base, likely 4-5% over the term).

H&T has proven very poor at forecasting and worse at keeping investors informed. whereas Ramsdens continued to trade in line, probably due to a combination of better and more conservative forecasting rather than mix, which doesn't appear to be a factor. H&T is operating a far more aggressive strategy, which perhaps gives a greater upside, but in our view, this is more than outweighed by risks and high debt costs. Overall, it appears that Ramsdens are the far better business.

On valuation, Ramsdens is on PE of just over 8 with a 5.5% yield and 1.3x book. This seems too cheap for a retailer that is trading well. H&T appears a little cheaper, but only before adjusting for debt, and it has a lower yield. There is undoubtedly poor sentiment in the UK equity market, including general institutional outflows and fears over UK consumer sentiment, particularly with luxury watches. However, this is a business that is very resilient, and benefits from the current high gold price.

After being becalmed for a number of weeks the price has started rising. We won’t know if Downing are out until their portfolio update at the end of the month, but it looks like that anchor may finally have shifted from the stock.

Robert Walters (RWA.L) - Q1 Trading Update

When Equity Development said that Gatacca were trading in-line with sector peers, these were presumably the kind of terrible results they had in mind:

Although Robert Walters highlight strong comparatives from last year.

This shows all the cash isn't always available for acquisitions/shareholder returns:

Balance sheet remains strong with net cash of c.£54m as at 31 March 2024 (31 December 2023: £79.9m), reflecting the typical first quarter working capital profile of the Group.

However, even this reduced number should easily see them through this cycle. This is good as this sounds like full-year profits warning, but with no specifics given:

…the general environment remains one where client and candidate confidence is at low levels, which we expect to continue to be a headwind to fee income growth in the near-term.

The hope of shareholders that a recovery will be soon is repeatedly dashed on the rocks of reality.

That’s it for this week. Have a great weekend!