A short trading week this week, and we are getting ready to have our first scl physical get-together today (limited to 6 sadly) so this week’s weekly summary goes out early.

The get together is almost certainly going to have a celebratory atmosphere, not just with the end of lockdown but because Wey Education has just announced a recommended takeover. This is a large holding for Leo and with a 46% premium, the drinks are on him!

A reminder that to see the full debate you will need to be a ‘member’ of the server. This is free and easy to access, so if you don’t already have it then here is an invite. Links will usually go to the browser version. So if you are a member with the app installed putting the company ticker into the search bar to find the section may be the easiest option for you.

Large Caps Live Monday 29th March

Wayne took a look at the events affecting Archeogos and its forced liquidation.

So where shall we start? Bill Hwang is an ex-Tiger fund manager - so is a Tiger Cub. The reports over the weekend suggest that he managed between $15-20bn.And was levered....and levered...and levered....

Various articles I have read have suggested that his gross book was either $80bn (ie 5 x $16bn) to $80 long / $40bn. The other odd thing is whether he was running a hedge fund or a family office - there seems to be great variation in the articles. And some articles suggest he started the year with $5bn and had built it up to $15bn.

So we now know that Nomura and Credit Suisse have been burnt.On Friday we saw liquidations from Goldmans and Morgan Stanley. Over the weekend it was being suggested that the prime brokers were working together to close down the positions but that one or more prime brokers then jumped the gun.

Since then we have learnt that Credit Suisse and Nomura have faced the bulk of the losses. With Morgan Stanley and Squiddy escaping lightly. The best bit was Goldman analysts downgrading Nomura due to the losses incurred during the liquidation!

This article provides some good speculation about what may have gone down. And the chances of this being an isolated incident or something more systemic.

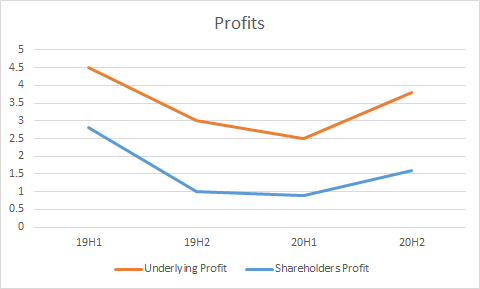

Mark thought that these results were far less impressive than an initial reading might imply.

The headline numbers are what you would expect from a business such as this – a strong rebound in 20H2 following a covided 20H1:

“· H2 order intake £53.4m (H1: £30.5m) contributing to strong closing order book of £55.5m (2019: £52.2m)

· Group full year revenue £83.7m (2019: £88.8m)

· 2020 H2 revenue 27% above H1 as customer investment returned to pre-pandemic levels

· Underlying profit before tax of £6.3m (2019: £7.5m)”

When we looked at these in the past, we have been sceptical about some of the adjustments made here. We’ll leave aside that this is a company that has made a number of acquisitions recently and wants shareholders to count the benefits of increased revenue without considering the costs associated with the acquisitions. This is not unusual in financial markets!

However, the pension side here is a little unusual. An asset & liability matching exercise has allowed the company to remove the pension deficit from the balance sheet. This means that a casual reader of the results may think that this is an asset not a liability at the moment.

The company expect investors to remove the costs of administrating the pension scheme from the underlying results, which we consider to be aggressive. However, the biggest issue is that the reported profits don’t include the large recovery payments the company has to make for the next six years.

“In 2019, the UK scheme's triennial valuation as at 30 June 2018 was completed, with the reported deficit reducing to £35.2m (30 June 2015: £69.6m). The contributions remained at the same level, but the recovery period reduced to six years and one month (30 June 2015: 14 years and 2 months).”

When I adjust for these figures, “Shareholders Profit” i.e. underlying profit actually attributable to shareholders after removing mandatory pension payments is more like £2.5m than the £6.3m reported. And this excludes acquisition costs.

As always the outlook matters:

“Mpac is positioned to serve resilient end markets with long term growth potential leading to continuous customer demand. Supported by our sizeable and increasingly diverse order book we remain well placed, serving Covid-19 resilient markets which have good underlying demand. 2021 has started well across all regions and after taking into consideration the challenge of predicting the impact of the pandemic the Board believes that the Group's long-term prospects remain positive.”

The order book is up but not at exceptional levels:

```H2 order intake £53.4m (H1: £30.5m) contributing to strong closing order book of £55.5m (2019: £52.2m)```

Underwhelming. Particularly bearing in mind 2 acquisitions have been made in this period.

Equity development have a new note out. This has £95m revenue, with an increased Gross Margin. However, A big jump in forecast Operating Expenses sees Adjusted Earnings flat at £6.3m. They chose not to adjust their PBT for Pension Recovery Payments. Although they recognise that these will have a c£3.3m cashflow effect.

The company had been reasonably cash generative in H1, mainly as a result of working capital flows. We had expected these to reverse in H2, which they didn’t fully. I still don’t think that they can run at these levels indefinitely. This means that with Payables some £10m above FY2019. Then the net cash of £14.6m probably needs to be adjected down to more like £5m.

We’ve long commented that these are first-level thinking markets with simple narratives driving returns. If you haven’t dived into the details of MPAC, then it is very easy to see why shareholders may have thought a cash-adjusted P/E of 15 looks reasonable in the current market.

However, when you take the real shareholders’ earnings of c£3.3m after pension payments, apply a P/E of 15 and adjust for a more sustainable net cash figure of £5m you get a market cap of £55m or just £2.70/share.

The stock has had strong momentum in the last year, but if that momentum fades, and investors start to do some real valuation work on the business, it could be a long way down from here.

Leo noted that the investment case wouldn’t look so bleak if the upcoming Triennial Valuation removed the need for recovery payments. For this, we need the Annual Report which hasn’t been released yet. It would be brave to bet on this without seeing some strong evidence, however. Pension Trustees tend to be a conservative lot.

Recruitment company, Gattaca, appears to be another company where shareholders bought into the recovery with too much fervour. Mark noted that:

It is perhaps not surprising then that today’s results have led to a 17% decline to £1.26. These are results to 31st January, and show Net Fee Income at £21.1m vs £31.8m for 20H1. Underlying EBITDA has dropped from £5.7m to £2m and PBT from £3.3m to £0.4m.

Outlook is positive, but suitably vague:

“Whilst the pace of the recovery remains uncertain, we are seeing more encouraging signs in the market and improving activity rates. Over the coming year we will continue to invest in our people and technology, and the Board remains confident on the outlook for the business. Full year 2021 underlying PBT expected to be in line with market expectations.”

Despite these large drops in NFI & profitability, and a H2 forecast to be worse than H1, Equity Development have a bullish note out with a new price target. However, the ED target seems to be on some highly optimistic FY22 numbers and comparing to much larger recruiters who have always generated much higher margins and commanded much higher multiples.

The moral of the story is "beware analysts bearing comparables"!

Yes, I'll start with the positives here: Today's figures are basically the same as they said they would be back in November, so we have good revenue and EBITDA visibility here.

So, that's the positives done. Here's the negatives as I see them.

They have completely failed to compete against Zoom and Teams, forcing them into their Professional Services niche. A 1% increase in Q4 2020 average revenue per day versus pre-pandemic levels in PS, compared with a 31% reduction in non-PS. (PS = Professional Services.)

But clearly, 1% growth in the current environment is terrible. In the initial lockdown, some PS businesses shut down entirely, but that certainly wasn't the case in Q4. There was growth overall due to more customers though, but +18% yoy revenue compares terribly to other covid stocks.

I think the outlook is the main new thing here though:

“FY2021 is set to be a transitional year for the Group as we migrate from a remote meetings business to a broader cloud platform for external and specialist communications.”

I'm pretty sure "transitional" means "bad", at least in terms of superficial numbers. I think they're trying to prepare us for this.

“The Group is exploring a range of potential organic and inorganic platform capability enhancements to advance its strategy as a leading cloud platform for premium external and specialist communications.”

Mark pointed out that when they say:

“That said, we are nevertheless confident in our ability to meet market profitability expectations for the year, albeit at a potentially lower level of top line revenue.”

This would presumably be the Progressive Equity note. Which has a 2021 EPS forecast of negative 0.2p. This is even worse than the 20H2 EPS of 1.5p. When the Annual Report comes out it will be worth checking if they can meet their debt covenants in this loss-making scenario.

On this basis, we can’t see any investment case here.

From results that are much worse than they first appear, Mark transitioned to a terrible situation that may not be as bad as it first seems.

Unfortunately, RA International’s results were overshadowed by this release on Monday:

“Soraya Narfeldt, CEO of RA International: "As has been widely reported, the Cabo Delgado province of Northern Mozambique has seen a persistent threat over a number of months from local insurgents. Over the course of the last few days, there has been a further escalation in hostile activity in the Cabo Delgado province near to where our operations are based. Given the nature of this escalation, we have prioritised the safety and security of our staff, including the evacuation of our people from the area.”

Although the company have yet to comment since this is an ongoing evacuation, the sad news is that they are likely to have lost staff members & contractors in the attack.

It is understandable that the share price dropped around 15% on Monday on this news but I think the results and a subsequent management call indicate that this was an over-reaction, at least on the financial impact to the company:

These are the reasons why:

They were one of the fastest companies to get an evacuation in place.

This has been an ongoing insurgency for years and unfortunately, this type of attack is not unusual.

The Total project that this camp is there to serve is one of the largest investments in Africa & is likely to go ahead with increased security support.

Their camp is some 15km south of the attack, still under the control of their security contractors and has faced no damage.

Loss of personal or property damage is fully insured.

Security costs are running below budget so this is unlikely to negatively impact costs on these contracts.

In light of this the loss of $10m in contract revenue for 2021, although significant, genuinely is delayed not lost.

Covid delays are still the biggest challenge they face. The order book is growing but the delivery times are getting pushed out, negatively affecting revenue recognition. 2022 certainly could be a good year, however. They are bidding for multiple contracts in the $10-50m range which would bolster their existing strong order book.

Concluding:

As always, timing in these sort of contracts is highly uncertain. I think the investment case comes down to whether you trust management to deliver. Nothing of the last few days has changed my mind on this. But I totally understand if investors put this in the too hard/too risky category for them.

Small Caps Live Thursday 1st April

CMC Markets (CMCX.L) - Broker Updates

Leo wanted to give a quick update on broker forecasts that were significantly out of date following an update to guidance for FY 2022.

All the broker research here is top secret, albeit the company will eventually post the average to their website, but you can infer some of it.For example, IG carry Retuters "EUROPE RESEARCH ROUNDUP".

25/3: CMC Markets Plc : Peel Hunt raises target price to 595p from 470p

30/3: CMC Markets Plc : RBC raises target price to 550p from 450p

1/4: CMC Markets Plc : Jefferies raises target price to 530p from 450p

And Koyfin shows the min/max/average/median/std dev of forecasts which I guess would let you derive the individual forecast values for up to 5 brokers. Anyway, it looks like the new average will move from 24p to about 36-67p once all the upgrades are in.

Anyway, I ignore price targets myself, but the fact that the EPS forecasts now approach my own 40p is important, and of course changes how a stock appears to casual investors, e.g. looking at Stockopedia. Share price is now around 490p versus 460-465p when we highlighted these upgrades were coming, but I'm hopefully of seeing more upside in the next few weeks and months.

This is a company that Leo went to see about 18 months ago because:

I like high gross margin, high growth companies. They are often loss making, but it is easy to predict when they will become profitable and the upside can be large.

Today he took a look at his Pre-close trading statement:

“The Group experienced a weak second half in both its Customs and Aviation sub-sectors due to Covid-19 which has adversely impacted revenues. However, the Profit Protection sub-sector performed strongly and continued to strengthen throughout the year. As a result, full year revenues are expected to be around £6.7 million (FY20 £8.0 million), with a consequential impact on profitability.”

H2 is traditionally the weaker half, but things were particularly bad this time.Only £2m revenue, a YoY drop of 35%. But this is what caught my eye here:

“In sharp contrast, the Profit Protection market performed extremely well as the pandemic accelerated the already strong trend of retail moving on-line. Despite challenges with gaining access to customer sites during the various lockdowns, our revenues here grew by over 40% relative to last year and we received our first orders from 16 new Profit Protection customers in the year, with 12 of these in the second half. These new customers included both Third Party Logistics providers (3PLs) such as FedEx (in the US), CEVA, Clipper, Unipart and DPD and retailers ASOS, ASDA, Fanatics (in the US) and Clicks (in South Africa). We also received further orders during the year from existing customers including JD Sports, Sony, and Next.

So a lot of H2 and, I suspect, Q4 customer wins.Many of them are large with very many sites and will continue to rollout for years. Although this is mostly capital sales, the machines they sold 3-5 years ago are already coming up for replacement/ upgrade, so we will get repeating revenues of a kind.

My modelling shows potential breakeven in H1 2022, but FY losses and no significant profits until the FY to December 2025.Of course, growth rates could suddenly jump, as it could with any company.

The maket makers marked them down heavily this morning, but it looks like there were many buyers.I was, and still am, hoping to get a better price than 20p.

Mark looked at this geotechnical company after making the following acquisition:

“…has acquired 100% of the share capital of ScrewFast Foundations Limited ('ScrewFast'), an innovative helical piling and steel modular foundations company for a maximum consideration of £3.68m (the 'Acquisition'). An initial consideration of £1.76m is payable in cash on completion, with up to a further £1.92m of deferred and performance-based cash consideration payable in August 2023.”

Looks a nice bolt-on in a complementary area:

“The Board of Van Elle believes that ScrewFast is an attractive addition to the Group as customers increasingly seek faster, modular forms of construction. It is profitable, cash generative, and operates in complementary market sectors with strong growth potential in each. ScrewFast is highly regarded by its clients and by Van Elle, with both companies having worked alongside one another on Smart Motorways projects for several years.

…ScrewFast will benefit from the scale, broad capabilities and financial strength of the Group, which will facilitate an immediate increase in capacity and access to additional cross-selling and growth opportunities.”

Financials are given as:

“For the twelve months ended 30 May 2020, ScrewFast recorded revenues of £5.9m, EBITDA of £0.65m and a profit before tax of £0.36m. Net assets at 31 March 2021 were £1.85m and the order book stood at £5.1m.”

5.7x EBITDA doesn’t look that cheap but a third of the payment is contingent on future performance. And you have to expect that this may have been covided in the last few months of that trading period.

In general, I think the numbers don’t matter too much here at the moment. The acquisition is more of a sign that things are getting back to normal after a turbulent few years of boardroom bust ups and then covid restrictions. This is one of the few shares that hasn't bounced significantly off COVID-19 lows, although they raised money from the market last year so there has been some dilution.

That alone makes them an interesting proposition in the current markets. We've not covered this before on scl but I watched the Interim Results Presentation and came away with generally a positive feel about the management. Worthy of further research in my opinion.

Finally for this week, Mark looked at this update:

“The Kwale North PFS concluded that it is not currently viable to mine the entirety of these deposits primarily due to the combined low heavy mineral grade, high land acquisition costs and elevated slimes content and associated tailings disposal costs.”

I always thought this was borderline, at best, given the grades, so this doesn't come as much of a surprise.

“While the Kwale North PFS does not support mining of the entirety of the deposits, the Company has commenced an assessment of the potential feasibility for mining a higher-grade sub-set of the North Dune and Bumamani deposits, targeting low capital investment and the use of existing processing plant and tailings disposal capacity.”

In my DCF, I have operations ending at Kwale when the South Dune runs out and this still looks good value with production shifting to Toliara in Madagascar.

This is a big issue for Kwale County though. Base is something like 60% of the Kenyan mining industry, and the largest employer in the region. For the sake of all stakeholders, I hope this concentrates minds and allows them to access prospective lands in the region to be able to continue high-grade production in 2024 and beyond.

Happy Easter everyone! Enjoy the extended weekend.