Small Caps Live Weekly Summary

FTSE100 Value, BSE FUL RFX EVE CMCX DFS

A busy week personally plus a slow week news-wise means another week where we only looked at a few companies. However, WayneJ was back on Monday with a Large Caps Live looking at finding value in the FTSE100.

Large Caps Live

There is one question on my mind right now: Is there any value in the large caps space?

Let’s look first at FTSE 100 companies trading at over 5% yield. There are 14 companies according to Stockopedia:

What I found interesting about the list is the sectors:

(1) Financials

(2) Basic materials

(3) Consumer cyclicals

(4) Consumer defensives

The consumer defensives are the tobacco stocks – and they usually trade on a rich yield so nothing really surprising there perhaps. The financials are the biggest sector and deserve some more investigation than I have done. However, I would point out that financials are a broad sector and the above list includes a closed book insurer (Phoenix), two asset managers - M&G and the artist formerly known as Aberdeen and a number of insurers – Admiral, L&G and Aviva. Obviously, Admiral is different from the other insurers mentioned

What strikes me about them is the valuations across the financials in the list:

Of course, if we are looking at price to tangible book we ought to also be looking at return on TANGIBLE equity (as opposed to all equity). And single years can be distorted by one-offs. I think particularly striking are L&G and Abdn - both on high yields with ROEs of over 10% and P/TB which are not crazy.

Abrdn is clearly going through some changes, with the rebranding & acquisition of Interactive Investor. That says to me that they feel challenged in distribution. That may indicate a shift in relative power between them and platforms like Hargreaves - or actually more the actual wealth management platforms. I know that in the past there used to be concern about the acquisition policy of Aberdeen under Martin Gilbert - people used to say that if they ever stopped acquiring the risk was the wheels would fall off. Have a look at this:

From Abrdn's analyst pack. You can see the fee revenue yield is far more attractive on personal (61 bps) but that they have limited AUM there:

But the real problem is flows - and that depends on performance. And that in turn depends on whether the board and management understand what leads to good performance vs bad performance.

If I read that correctly, their profits have been via disposals rather than operations. Also, note the restructuring and corporate transaction expenses line. And the writedown of goodwill last year (for a business that has grown by acquisition).

Regarding the other financial stocks, I am not sure I can draw any hard conclusions from any of the above. However I am intrigued as to how L&G does a 19.5% ROE vs 1.5% at M&G, 2.66% at AV/ and Phoenix has a negative ROE. The big issue for me is:

How sensitive are each of these businesses to rising interest rates

How sensitive are they to inflationary expectations

Why is their long term ROE progression and is there a structural issue that means that they can either sustain or have to cut dividends

Let’s turn to the basic materials:

- Polymetal is clearly a Russian exposure company which explains its valuation

- RIO and Anglos are perhaps more interesting in a world where the consensus seems to be that we are short of many minerals

- What I would point out though is the near-vertical move in both AAL and RIO in recent weeks (I also threw BHP on that chart):

That is a 10-15% swing in a month depending on where you got in. Not sure I have much to add to the general market commentary on commodities. Except perhaps that it will be interesting to see the impact of China restarting.

The other area to point out in the above list is that consumer cyclicals comprise the big house builders – Persimmon, Taylor Wimpey and Barratts. Clearly, the question with all three is going to be what happens to their balance sheet if we have a slowdown.

I should also point out that the big banks (eg Lloyds, NatWest, HSBC) are just outside this screen with dividend yields of circa 5.4%. (I think that the dates for slicing dividend yield on Stockopedia are different from the dividend yield shown on the pages of the StockReport).

Small Caps

Base Resources (BSE.L) - Operational Impact of Rains

This series of rainstorms over recent days resulted in flash flooding that overwhelmed the dewatering systems for the three operating hydraulic mining units (HMUs). Recovery work is underway, with one of three HMUs back in operation and delivering approximately 45% of normal mining volumes. The remaining two HMUs are currently not operating as they continue to be dewatered and replacement of the pump motors progresses.

So bad news. Although not of the company's making. However, the good news is:

While the timing for returning to full mining volumes is uncertain, it is not currently expected that the Company’s production guidance for financial year 2022 will need to be revised.

This guidance is:

Kwale Operations production guidance for the 2022 financial year (FY22) remains at:

Rutile - 73,000 to 83,000 tonnes.

Ilmenite - 310,000 to 340,000 tonnes.

Zircon - 24,000 to 28,000 tonnes.

Which is based on:

This guidance is based on the following assumptions:

Mining of 17.4Mt at an average HM grade of 3.53%.

Average MSP feed rate of 68tph.

Average MSP product recoveries of 101% for rutile, 101.5% for ilmenite and 84.5% for zircon.

The 17.4mt already looked a stretch, however, the grade so far has exceeded that guidance. Mark thinks it is fair to assume that they will be towards the lower end of that guidance due to these disruptions. HMS pricing remains very strong, however. Mark expects Kwale to still produce IRO $140m FCF before movements in Working Capital or dividend taxes in 2022 even on the lower end of the production guidance.

That the market cap is just $245m reflects the short Life of Mine in Kwale and doubts that the company's other projects will get the permitting required.

Fulham Shore (FUL.L) - Trading Update

We like this rollout of Franco Manca & Real Greek restaurants, both as a company and a place to get a good value meal in London. However, when we looked at it last we had concerns over the valuation and their ability to finance their rapid expansion plans. This is what they say this week:

first two months of its financial year ending 26 March 2023.

The Group has continued to trade well and in line with management expectations during April and May 2022.

Tourists seem to have returned to London's West End and many cities around the UK. The small number of Franco Manca and The Real Greek restaurants that are located in areas with a high proportion of offices still have a way to go to return to pre-pandemic levels but are showing continued improvement.

Anybody who has been to London recently will probably have had the same experience.

The Group grew by 10 new restaurants in the financial year ended 27 March 2022 and has opened three more since the year end: The Real Greek in Newcastle and two Franco Manca pizzeria in Canterbury and Kingston upon Thames.

So it seems we were wrong about them not having enough capital to rapidly expand. There was a placing after that September update detailed above, but it was a secondary one for directors to sell their exercised share options and for some other shareholders to reduce. And there's more:

Overall, 11 new restaurants are on track to open in the first half of this financial year to March 2023 with two further locations already contracted. This will go some way to reach our total target of 18 sites for the whole year.

So how is cash:

The Company's net cash position before lease liabilities recognised under IFRS 16 as at 6 June 2022 was £3.6m.

That's down from:

£4.0m on 25th March 2022

£5.1m on 3rd December 2021

£4.3m on 3rd November 2021

£5.0m on 28th September 2021

£5.1m on 26th September 2021

But that's actually pretty impressive given the number of new openings.

Leo visited two FMs recently. The first one was in "Covent Garden", actually just outside, on Maiden Lane. David Page told me that rents can be as little as half as much one street over, and in this case, it is one over from Henrietta Street and a far far nicer location. They had plenty of tables outside and were full, with one group waiting most of the time. Restaurant management was noticeably excellent. Really fast to take order. Really friendly despite being very busy. They could have turned the pizza around and got us out slightly faster though. The thing is: people will seek out Franco Manca when things are like this and a secondary location is no impediment whatsoever.

The second one was in Chiswick on what is presumably the high street. I don't like Chiswick - terrible location for anything other than Heathrow and very noisy and polluted from traffic in the main shopping areas. Only a few tables outside in this location and not very appealing. Not full inside on a Tuesday evening, as I suppose you'd expect so far out. Just felt like an average pizza restaurant, although the staff were still good.

Back in September, Leo suggested that they should announce an equity raise with their AGM. Instead, they announce an increased debt facility and replaced the CBILS loan with an RCF. This week they confirm:

The Group has undrawn bank facilities of £15.9m, providing substantial financial headroom of over £19m.

This is a massive headroom. and from the H1 results, the RCF was extended by 3 years, we would guess to December 2024.

House broker Singer have issued an updated note.

We make no forecast changes and feel this should assuage any investor concerns given a spate of recent peer downgrades.

This leaves the problem of valuation. Frankly, this has never looked cheap, not even in March 2020 at 5p. Forecast EPS for 2024 is 0.8p and the share price is 15p.

On an adjusted 2024 EBITDA basis (pre-IFRS 16, of course), £15.3m versus a market cap of £90m looks a little better. They've hit growth pains before and no doubt they will do so again. It is difficult to know how big they can get before hitting an insurmountable wall or even when they have over-expanded just like every other rollout before them has done.

The fact the price has gone nowhere for 7 years is partly a reflection of the speedbump they hit with cannibalisation due to short-term overexpansion in suburban Greater London and partly due to losing two years to covid. But the main reason was that the share price was bid up immediately after IPO to crazy levels, which is absolutely outside their control.

Our customer numbers continue to grow and we have an expansion programme targeting prime new locations benefitting from historically low rental levels, the likes of which have not been seen for many years.

And remember it is the rents that are the fixed part (traditionally a third) of the costs that create much of the risk. Staffing and food costs significantly flex with demand. So, in summary, the company is probably the best risk-adjusted value it has been for its entire listed history, making it still about 50% overvalued.

Ramsdens (RFX.L) - Interim Results

Here’s the headlines:

The revenue has bounced back nicely from COVID but at lower gross margins reflecting the lower FX revenues. Currency exchanged has gone from £181m in 2020 to £94m, with Gross Profit down from £4.7m to £3.4m.

The standout is Jewellery retail, where revenue has increased from £7.054 m to £13.085m & it's now contributing 31% of the gross profit mix, up from 19%.

On the outlook, they say:

Trading following the Period end has continued to improve. Foreign currency volumes have increased to approximately 85% of pre-pandemic levels, the pawnbroking loan book has continued to grow, the weight of precious metals purchased has increased and retail jewellery has remained strong.

However, the EPS of 5.6p for the HY and forecast EPS of 14.8p for 2022 mean that the stock is quite some way off the peak EPS of 21.4p they did in 2018. Even the 2023 forecasts don’t show a full recovery in EPS. Yet the share price is higher today than it was for the whole of 2017-2019 making the current rating of around 14x P/E unattractive.

Eve Sleep (EVE.L) - Formal Sales Process & Trading Update

We previously looked at Eve when it was a net net in the dark days of the pandemic and concluded that the level of cash burn made it look unattractive. This didn’t stop the share price multi bagging in the exuberant days of 2021. Reality has slowly been catching up with shareholders here though, bringing us to this week’s announcement:

Having delivered a third consecutive year of growth in revenues and marketing contribution in our core UK & Ireland (“UK&I”) business in 2021, and cognisant of current trading conditions, the Board now wishes to accelerate eve’s push into the wider sleep wellness space.

Sounds great! However:

In order to deliver our objective of creating the first digital sleep wellness retailer, the Board considers that eve would benefit from additional investment.

Hopefully, you saw that one coming. Can you imagine a company going from £37m of cash in mid-2017 to £4.5m at the end of 2021 not thinking they would benefit from some more?

The Company has recently been in discussions with a US-based investor with respect to a strategic investment in the Company. These discussions developed into that party making a preliminary expression of interest in making an offer for the Company.

Again, sounds great! However;

Discussions with the US based investor have since lapsed and the party has withdrawn its interest.

Really this emotional rollercoaster would be much more fun if it wasn't so predictable.

the Board believe that it is now in the best interests of all the Company’s stakeholders to explore all possible strategic and financing options for the business.

Note the use f the word "stakeholders"⚠️So, basically, it would be better for employees like them to string it all out a little more?

In addition to further external investment in the business, these options may include a potential sale of the Company.

So what’s it worth?

In the FY 2022 results issued in March they said:

£4.5m closing net cash balance is sufficient to execute the business plan for 2022

This week they feel this isn’t sufficient.

eve has now essentially completed the three year rebuild strategy, aimed at positioning the business for sustained growth across all of its geographic and product markets. This was built on a planned 10% year-on-year UK&I revenue growth in 2022 with our direct to consumer business performing well ahead of this…

eve continues to outperform a market which is estimated for the first four months of 2022 to be down 29% year-on-year in the UK (source: IMRG Capgemini) and down 37% year-on-year in France (source: FEVAD).

Fancy that! Who'd've predicted that trading would suffer post-covid?

Over the five months to 29 May and against challenging year-on-year comparatives, eve’s direct to consumer sales orders in the UK&I are down 15% and down 3% in France.

That'll have investors queuing up with the chequebook! Ahh, here's the rub:

Based on the first five months of trading, and its expectation that the cost of living crisis is set to continue for some time, the Board does not now expect to meet its previous revenue expectations for the current year, with additional promotional activity also having an impact on gross margins.

And worse of all:

This will have a consequential impact on the Company's anticipated cash balances as the year progresses.

Without a well-financed company willing to take a risk buying this then it looks a zero to us. And in such circumstances, why would the acquirer be willing to pay up? The best they can hope for is a competitive auction. But with the potential US buyer having already pulled out this may be more hope than substance.

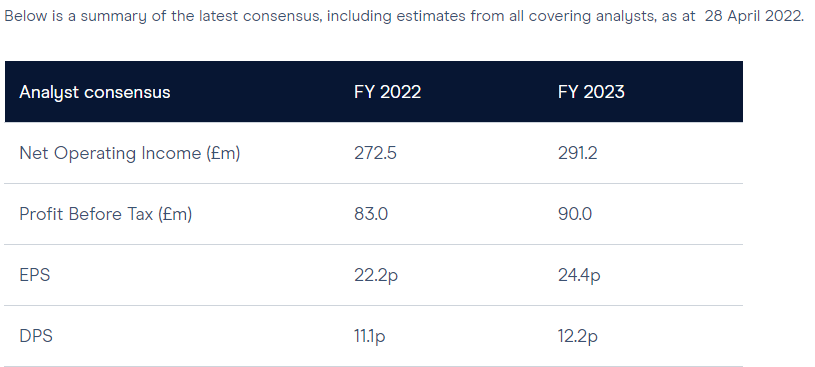

CMC Markets (CMCX.L) - Final Results

Before this week’s results market expectations were given by the company as:

These looked incongruous with the last trading statement that said:

FY 2022 net operating income expected to be approximately £280 million, at the top end of guidance

So we were expecting a small beat to analysts’ consensus in these results.

They duly delivered with a 10% beat on EPS:

Despite the beat the share price had a good run and fell 20%. Leo felt this was due to cost guidance. Costs had already grown to support investment in the non-leveraged offering, initially for the UK:

Operating expenses have increased by 2% to £188 million, primarily due to higher personnel costs to support the ongoing strategic initiatives, partly offset by lower sales costs.

Lower sales costs mean that underlying costs are rising much faster than that, and they are about to get worse:

Our 2023 investment plans are expected to increase operating costs to approximately £205 million excluding variable remuneration

But they'd spend more if they could:

Over two thirds of the new investment will be associated with people, product development and marketing. The rate of spending will be dependent on the Group's ability to make additional personnel hires.

This impression of a lack of cost control was exacerbated by a car-crash presentation where Peter Cruddas said about the investments they are making in their offering:

We don't think about the costs

Although he corrected himself the sentiment was clear. He also said he didn’t know who the potential customers of the service currently trade with and said “I don’t know the market that well”, before bemoaning that the market didn’t understand the company and the share price was too low.

Leo previously commented that he thought their principal new products were late. In the results they said:

CMC Invest UK: the new UK non-leveraged platform has been successfully soft launched to staff and will be rolled out to new clients over coming months.

This doesn’t seem to represent any progress from the April statement:

CMC has this week delivered the initial internal launch of CMC Invest, our UK non-leveraged platform to our UK staff.

Given this and that the waitlist has been “coming soon” since at least March, Leo felt that this offering is now late. He also wasn’t impressed by:

Investment in growth initiatives is expected to result in a 30% increase in net operating income over the next three years. Benefits to be seen from 2023 and are set to deliver profit before tax margin expansion from 2024.

…saying that there were much better opportunities in the market on the basis of models out to 2025 and that in the meantime that the significant P/E premium to IG Index and PLUS Markets stuck out.

DFS (DFS.L) - Trading Update

SamG spotted the trading update first, commenting that the predictable slowing of demand had nonetheless led to a 15% fall in the share price, but that ScS had not reacted in sympathy albeit after a few weak days.

Leo looked at it through the lens of his holding in ScS.

The third quarter of our financial year (ending on 27 March 2022), saw double digit growth in the volume of orders taken across the Group relative to a FY19 pre-pandemic comparative period. This volume growth was achieved despite offsetting significant cost inflation through mitigation and retail price increases.

Of course increasing prices raises revenue, but what they presumably mean is that higher prices have not put off customers by more than than effect.

Moving into the fourth quarter the UK furniture market has seen a change in demand patterns with recent data from Barclaycard suggesting a c. 2.1% reduction in transactions in April1 relative to pre-pandemic periods. We have seen a similar change in order volumes across our Group.

Leo said that he had not seen this in the ScS numbers, which he posts to the ⭐scs channel on discord available to contributors, but rather a small slowdown following the early May bank holiday and limited benefit from the June bank holidays.

While we have increased our weekly production and delivered revenues progressively over Half 2, to record levels in the fourth quarter, the ongoing Covid linked supply-chain disruption, combined with lower order intake since April has led to lower levels of production and deliveries relative to our previous expectations.

Which looks better than ScS where he is not seeing any progress on increased production and deliveries. Regardless of absolute progress, lower that expected deliveries of course mean a revenue and profits miss:

Subject to any variations in the rate of deliveries of the final weeks, we now expect UK & ROI full year revenues of approximately £1,150-1,160m and underlying profit before tax and brand amortisation of £57-£62m, which compares to pre-pandemic FY19 pro forma 52 week revenues of £996.2m and profit before tax of £50.2m.

DFS points to their elevated order bank giving resilience next year, but Leo’s modelling is showing far higher figures at ScS where he expected a miss in the current year but a beat next year. Also ScS has considerable net cash whereas DFS are close to their internal leverage limit after buybacks:

we expect to close the year with a net bank debt position of less than £100m, in line with the upper end of our 0.5x-1.0x target leverage range. The Group remains in a strong financial position with significant available headroom under our £215m bank facility.

That’s it for this week, have a great weekend everybody.