Small Caps Live Weekly Summary

CMCX HTG JSE KINO MACF PEB

A predictably quiet week for news this week. Although with illiquid markets come big share price moves, and it often pays to be paying attention when other market participants aren’t.

CMC Markets (CMCX.L) - Trading Statement

CMC Markets picked the second-best day of the year after Christmas Eve to announce a profits warning:

Whilst underlying market activity has the potential to recover, should year-to-date market conditions continue for the remainder of FY24 then it is expected that net operating income will be between £250 and £280 million.

The reason given is:

subdued market conditions have continued through August with trading and investing net revenues trending 20% lower year-on-year.

Given that they said they were trading in line at the end of July, it seems suspicious that trading in a single month, which is also the quietest month of the year, could have such a big influence.

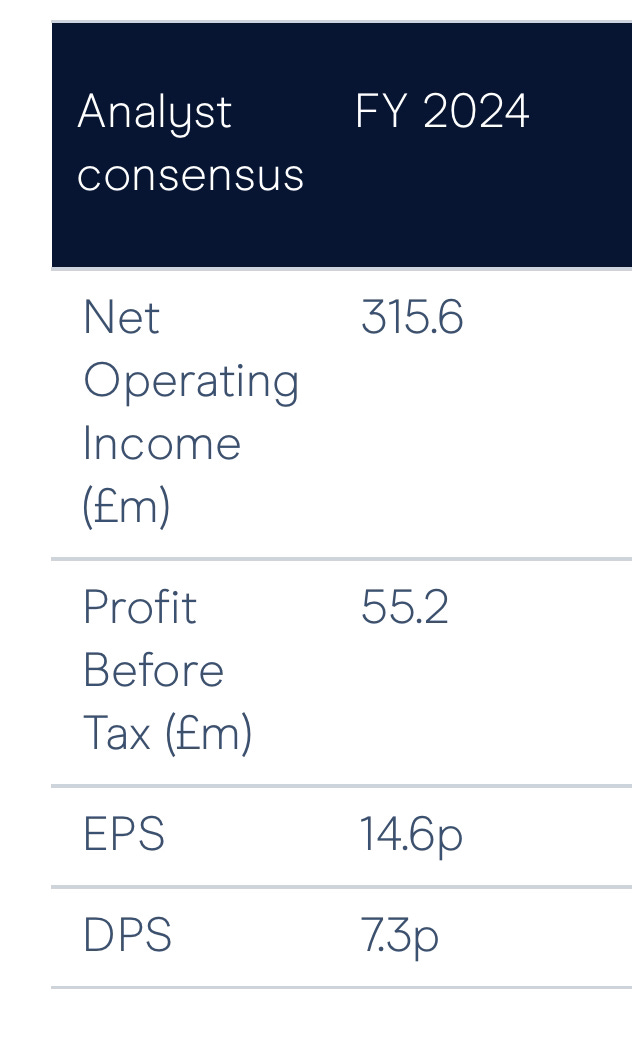

Helpfully, they give current consensus on their website:

This is not the sort of company where mere mortals can access the brokers' notes, but as a midcap, is unduly influenced by those opinions, putting us at somewhat of a disadvantage. Some simple maths shows that perhaps the best the company can hope for at current trading performance is around 5p EPS for FY24, and the worst is a loss. As such, the initial 20% fall in the share price, and subsequent bounce back to just 10% down looks a big under-reaction.

However, the shares now trade at just 0.9xTBV, where the majority of assets are liquid (although perhaps tied up in regulatory capital or similar). Hence, they may appeal to investors who think all the bad news is now in the market and that earnings will bounce back in 2025.

Hunting (HTG.L) - HY Results

The results here were largely known due to recent trading statement. So we simply turn to the outlook:

On this basis, the Board believes Hunting has good momentum going into the second half of the year, with an EBITDA performance similar to what has been delivered in H1 2023. Further improvements in working capital efficiencies are expected in H2 2023, with the Group's total cash and bank borrowing position expected to unwind by the year-end as larger projects are completed in H2 2023 which will deliver strong cash generation from operating activities.

We had wondered if they were saving a further upgrade to come for FY23. However, this is looking less likely based on their “similar performance” for H2 statement.

Moving to net debt may scare some investors, and be behind the c.8% fall on the day of these results, but checking the Balance Sheet shows it all being working capital, and they reiterate the expectation that this reverses on H2.

At 0.77x TBV, where the assets are largely liquid, this is another company that will appeal to the asset-focused investor.

Jadestone Energy (JSE.L) - Montara Operations Update

Inspections and repairs here are confirmed as going to plan. They say that these are expected to take less than 60 days. Hence, the implication (although not explicitly said) is that there will be no issues with RBL. Overall, the fall here looked massively out of proportion to the issue, and the shares bounced almost 30% on the day. This is still a long way below where they were trading when this minor issue was announced and materially below the recent 45p placing, so there could be a significant further upside here. However, it will take a lot longer than 60 days to repair the management's reputation.

Kinovo (KINO.L) - Potential Offer

Kinovo…today announces that it has received a non-binding indicative offer from Rx3 Holdings Limited ("Rx3") which may or may not lead to an offer being made by Rx3 for the entire issued and to be issued share capital of Kinovo at a price of 56 pence per share, payable in cash. Rx3 and Tipacs2 Limited, (which holds c.29.89% of Kinovo's shares), are both ultimately owned by Mr Tim Scott.

This is at very little premium to the share price prior to this news. Rx3 are keen to point out that the minimum price they can offer is even lower:

Rx3 notes the announcement made yesterday by Kinovo in relation to its possible offer for the Company. It confirms that, ..., if Rx3 makes an offer for Kinovo, Rx3 is required to offer a price of not less than 40 pence per share

So they appear to be setting shareholders up for the reality that it may not even bid at 56p. We suspect that the bid, if it comes, will therefore be somewhere between 40p and 56p and will be followed by them asking the board to recommend it. If they don't, then an EGM to remove the board? We expect lots of gnashing of teeth from shareholders who think the offer undervalues the company, and we have some sympathy with that, given the forward P/E is under 8. However, as Best of The Best showed, a 30% holder can easily force the issue if they really want to, and such companies rarely deserve a premium rating.

If no offer is forthcoming, it is unlikely to be due to the price, but that Rx3 find something material in their due diligence. Given the issues in the past with DCB Kent, then this can’t be ruled out. As such, shareholders may be better off simply taking the current market bid and re-investing it into other cheap UK small caps, rather than risk a low-ball offer being pushed through, or some more contract issues appearing.

Macfarlane (MACF.L) - Half-Year Report

2% revenue growth in a difficult market doesn’t seem too bad until you realise there are three acquisitions in there:

A good contribution from the acquisitions of PackMann in May 2022 and Gottlieb in April 2023, combined with organic growth in Europe and new business wins, offset lower demand from customers in the UK and Ireland.

So, although they don’t break it out, like-for-like volumes must be down significantly in an inflationary environment. The acquisitions plus cost-cutting & pricing get them to 9% EPS growth, which is at least slightly higher than inflation. Perhaps around half of the increase is due to the acquisitions. But if we assume they face the same sort of trends on input costs as newspaper publishers, what is likely is that they increased prices in response to inflation, and now cardboard & energy prices have declined, and they haven’t yet passed these on.

These trends plus acquisition benefits are likely to continue in H2, meaning they are confident of hitting FY expectations, which stockopedia has as 11.8p. So a P/E of 9.2, which is undemanding. However, with low single-digit increases in both revenue and EPS forecast for FY24, investors at the current price are still betting on 2025 onwards being a much better period for the company in order to justify even this relatively modest P/E.

As usual, the balance sheet doesn’t look particularly strong, with a current ratio of 1.13 and almost all the assets being intangible. For example, pension assets are obviously not an asset while they continue to have to make recovery contributions. But overall, the net debt is small, so should only have a very minor impact on this valuation.

Pebble Beach Systems (PEB.L) - Half-Year Report

Looks like this was a weak half here:

Adjusted earnings per share down to 0.2p (H1 22: 0.4p)

Although the company believes this is merely timing:

Strength of pipeline and level of customer engagement provides management with confidence in delivering full year growth despite the reduced order intake in the first half, highlighting the resilience of the Company and its ability to deliver project backlog.

With inline guided for the full year, finnCap retains their 1.3p EPS forecast for this year and 1.5p next year. So, assuming the company can make up for poor H1 trading in H2 and isn't simply delaying the profits warning, this puts them on a debt-adjusted P/E of 10 for this year, dropping to about 8 next year. Which could be good value.

However, the balance sheet looks very weak here, even for a software company. They have a big negative working capital position on top of large long-term debt. Although the long-term debt was reduced by the usual amortising amount, the short-term balance sheet position has actually deteriorated this half year. And the balance sheet equity is still negative despite £6.6m intangible assets. As such, this is at the very risky end of UK small caps.

That’s it for this week. Have a great Bank Holiday weekend!