Small Caps Live Weekly Summary

AGFX CAM CARD CTG IGR RCH TGP

It seems that the bull might be returning to the UK small cap market. While the impact is still relatively small, and many stocks are bouncing off multi-year lows, we nonetheless detect a change in sentiment. Investors are no longer seeing an in-line statement as an excuse to sell a stock. Even if the forecasts are for a decline in revenue and profits in the current year, an in-line statement is causing share prices to rise. A small beat or contract win can cause a 20-30% share price rise.

Shareholders appear to be focusing more on future years, in companies where broker forecasts are for EPS to return to growth. Of course, this strategy may be folly - house brokers are often wildly optimistic when it comes to their client's future year performance. As one SCL contributor quipped, “every small cap is a buy according to brokers forecasts two years out!” Still, the sentiment is a welcome change from the doom and gloom of the past two years. Here’s a selection of what we discussed this week:

Argentex (AGFX.L) - Final Results & Fundraise

The raise here comes as a surprise. They have gone from a cash-rich dividend payer to a 45p fundraise. Even more strangely their 3rd highlight in the results announcement says:

· Debt free and cash generative with net cash increasing by £2.1m in FY23 to £18.3m (2)

This is the rationale given:

In the absence of any additional capital and the acceleration of investment plans referred to above, we believe revenue growth in FY26 and beyond is likely to remain in the single digits, with EBITDA margins in the high single digits.

On raising additional capital to accelerate our progression into Alternative Banking, however, we expect growth in the business to accelerate. With the additional investments envisaged, we would anticipate revenue growth in FY26 in the 15% - 20% range, with EBITDA margins in the mid-teens.

They didn’t say how much they are raising which is equally strange given that they claim to have specific plans for the capital. The limiting factor is the 10% without holding an EGM. The maximum shares of 11.321m come to £5.09m, but we know brokers charge 5-10% on these sorts of raises, so they’ll get, say, £4.7m net if they get them all away. As it happened, they only managed to raise £3.25m before expenses, so about £3m after.

Their retail offer stands no chance of being taken up at 45p given that the shares currently trade at less than 35p. This isn’t helped by the EPS coming in at 4.6p vs the 9p that is in the Stockopedia consensus. This is almost certainly stale data from brokers via Refinitiv. However, this is what many individual investors base their investment decisions on. Many individual investors will also have held on here with the idea that they are getting a 7% yield. However, they now say:

However, in light of the Company's financial performance and trading conditions during the second half of FY23, the Board have decided that no further dividends will be declared for FY23.

This makes sense. At least they are not daft enough to raise, pay the broker fees while holding a lot of cash and pay out a dividend. Concurrent Technologies recently did this with a raise far larger than the price they were paying for a small acquisition, while simultaneously claiming they had a large cash balance. They then proceed to declare a dividend. All we can say is that they must have very persuasive brokers.

With Argentex now trading at less than 35p, and larger holders willing to put cash in at 45p, this could be a good entry point for the brave.

Camelia (CAM.L) - Final Results

Things not looking great here:

Trading loss for Agriculture of £5.6 million (2022: trading profit of £15.5 million)

Nor looking forward:

The outlook for 2024 remains challenging, however revenues are expected to be above 2023 but with a significantly higher adjusted loss before tax.

We’re not sure that "but" semantically reverses the "however" in that sentence to the extent required. This looks pretty bad:

The Board is not recommending a final dividend for the year due to the financial performance in 2023 and the uncertain outlook for 2024.

From the 2022 annual report:

In relation to the reserves of the Company, £36.2 million (2021: £41.9 million) is distributable. Other reserves of the Company include capital redemption and revaluation reserves.

Today, they report total reserves down £39.2m but don’t break them out, so quite possibly, they literally can't pay a dividend.

But it is certainly the balance sheet where the value is found. Net assets are £363.3m, of which only £4.7m is intangible, £12.5m is lease right-of-use, £94.6m in India, and £14.8m in South Africa. That leaves £236.7 of fairly hard assets (possibly with some double-counting of deductions) versus a market capitalisation of £127.6m.

Investors will want to take off £10m net assets to account for current year losses, but we don't think they will always make losses as their kind of farming is a cyclical industry:

In 2023 Camellia's results suffered from the impact of lower tea prices in what is a significantly oversupplied market, and serious demand disruption from COVID legacies on macadamia prices. Despite higher avocado exports due to improved quality, higher macadamia volumes, and an increased contribution from BF&M, the Group's profitability was hit hard.

And

Looking to 2024; tea markets are very tough, but there are signs that macadamia demand and prices are recovering, albeit that volumes will be lower than 2023. Avocado prices are currently in line with last year. The soya harvest in Brazil is complete but volumes have been affected by drought and pests and prices are soft.

There’s value here if you believe that the cycle will turn eventually.

Card Factory (CARD.L) - Final Results

A fairly pedestrian top line (at least in real terms) turns into a decent increase in the bottom line, particularly due to reduced debt:

The outlook is inline:

Consequently, expectations for FY25 remain unchanged.

Which means that they look good value on a headline P/E of less than 8. The cautious will want to adjust for the net debt, that lease liabilities exceed lease assets by about £8m and that there is £7.5m of provisions on the balance sheet. This makes the P/E closer to 9. Not expensive, but perhaps not stand out for a company with a flat EPS forecast.

In addition, the arrival of a dreaded second half weighing ups the risk that they may actually miss 2025 expectations:

As anticipated, PBT growth in FY25 is expected to be weighted toward the second half of the year due to the phasing of planned investment and inflationary recovery actions.

The market reacted positively to this update, but it seems brave to jump in with this risk lurking. On the other hand, they can now pay dividends again and 4.5p is fairly chunky as a starter, so this may attract income investors.

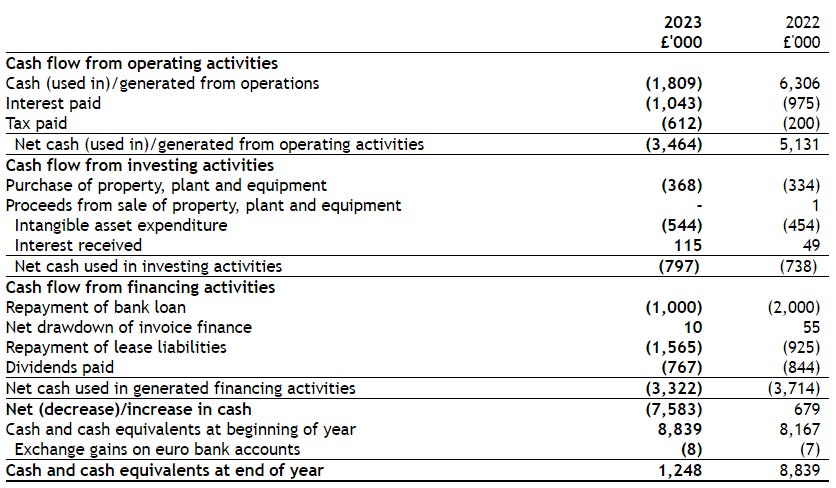

Christie Group (CTG.L) - Final Results

Weak results here with the company dropping to a loss even before exceptionals:

· Revenue down 4.8% to £65.9m (2022: £69.2m)

· Operating loss before non-recurring costs of £0.6m (2022: profit £5.4m)

· Non-recurring costs attributable to board changes and restructuring of £2.7m (2022: £nil)

The cash flow statement makes particularly worrying reading, given that working capital has increased on reduced revenue:

On top of the debt, provisions have increased:

They are paying a small dividend:

· Final dividend reduced to 0.50p (2022: 2.50p) to give total in year of 1.00p (2022: 3.75p) reflecting the challenging year but also the more positive outlook for the business

But for how much longer, given that retained earnings are now negative:

Lots of positive talk in the outlook:

· The Group is well positioned for an improved performance in 2024 with opportunities for growth across all business sectors, in the UK and internationally.

· Current activity levels are encouraging, with our UK transactional brokerage pipelines strongly ahead of this time last year and our finance brokerage business experiencing strong demand

On the back of this, their broker Shore are forecasting a return to profitability but further cash outflow this year. But even this may be in doubt as the dreaded second half weighting makes an appearance:

Nonetheless, the expected timing of many of those transactions points to a second-half weighting to our 2024 performance

History suggests this may well be a triumph of hope over judgment.

IG Design (IGR.L) - Trading Update

Revenue down 10% which looks poor, however it’s a profit beat due to improving margins:

These initiatives have resulted in significant growth in profit and margin for the year. The Group expects to deliver adjusted profit before tax of $25.9m (FY23: $9.2m), which is ahead of market expectations.

“Adjusted” is the key word here too. It looks like a beat only if you exclude the legal liability that has just appeared:

The Group expects to make a provision of c$5.5m* for potential liabilities relating to pre-acquisition era duties owed in the DG Americas division and is taking legal advice on the matter. Due to the historic nature of this issue, the results for the year ended 31 March 2024 will be adjusted accordingly.

However, this should be a genuine one-off. Although one that isn’t fully quantified.

The cash beat isn’t really surprising as lower revenue will see working capital released. However, this gives confidence that the financial difficulties the company got themselves into trying to generate more than $1b in sales are now behind them:

The Group closed the year with a net cash balance of $95 million (FY23: $50m), a $45m year-on-year increase which is well ahead of market expectation. The Group was average cash positive for the year despite its traditional seasonal cycle of working capital movements.

The outlook is for weak end markets but with confidence in FY25 delivery, which is when this would start to look reasonable value on a P/E of 8 if they deliver. The market loved this update, with the shares rising almost 30%. This is exactly the sort of stock where investors have gone from worrying about the near term to buying into the possibility that future trading will be much better.

Reach (RCH.L) - Trading Update

These look terrible, right?

well, obviously not, as the shares rose 6% in response. Presumably, investors are focussing on this:

Trading remains robust in what is a challenging environment, and we remain on track to deliver full year expectations.

It looks like a lot of work to get there based on the Q1 performance, though. Why the Reach share price is doing well, despite better performing and much better run National World trading close to all-time lows, remains a mystery. When you adjust for the provisions and pension deficit that Reach has, National World is on less than half the rating too.

Tekmar (TGP.L) - Disposal of Subsea Innovation

This sounds a reasonable amount compared to the £12.6 m market cap:

the sale of Subsea Innovation Limited … for a total cash consideration of £1.9 million

However, reading the details, they only get £27k of actual money, the £1.4m is money they are owed for work done but not been paid:

The consideration value comprises an initial cash payment of £27,000, a cash payment of £1.4 million relating to a trade debtor, payable post-Completion, and a further cash payment of £549,000 payable 12 months post-Completion.

We have been critical of Tekmar in the past for excessive trade receivables, including large amounts of unbilled contract assets. In addition, much of their billed receivables have been past due at the balance sheet date:

It seems that the company may not have the strongest revenue recognition or is doing business with companies that are consistent late payers. As they also say in the annual report:

This was driven by specific overdue debtor receipts in the Middle East and China. The ageing of debtors has increased across the group due to the specific debts in the Middle East and China. The group has not provided for any credit loss provisions as these debts are considered to be recoverable in full based on prior trading history with these customers.

On top of being paid with their own money for Subsea, they have to give the acquirer a year's rent fee on a £2.8m property, so this is pretty close to selling the business for a nominal sum.

It did lose £1.4m last year, so it should improve the P&L going forward. However, it’s only neutral for earnings to 30 September, so there must be significant transaction costs or similar. Again, highlighting this is a nominal sum sale not a strategic disposal.

They paid £4m for the business in 2018 but did get the property as part of the transaction, so this isn’t quite as bad as it seems at first. We note that the original seller of Subsea was a related party, though:

Subsea Innovation is wholly owned by its founder Gary Ritchie-Bland, the father of James Ritchie-Bland, CEO of Tekmar Group.

However, given the recent losses, shareholders will be hoping this is the last kick in the nuts from the former CEO, and the business will start to recover from here.

That’s it for this week. Have a great long weekend!