Small Caps Live Weekly Summary

APP PAY UGS GATC TGP

It seems a strange market this week. While UK large cap indices are making new highs (at least briefly), small caps remain fairly unloved. That is, of course, until something is tipped. The return of the big tip rise suggests that either a lot of newbie investors have entered the market or everyone is feeling really uncertain about the future and needs the hand-holding that a tip provides. As we regularly now warn readers, buying on tips, particularly after the price has already been marked up, is usually a terrible strategy. This week our summary contains two cautionary tales about this, UP Global Sourcing and Gattaca. Sadly, the rest of the rather sparse news that we’ve looked at is fairly gloomy too. We are hoping to bring you more cheery outcomes next week.

Appreciate/Paypoint (APP.L/PAY.L) - Merger Arb

We’ve been following this takeover offer for a while since, for structural reasons (larger shareholders selling in the market ahead of any potential CGT tax changes that had been rumoured), there was a reasonable arb on offer. The absolute return of 7-8% wasn’t groundbreaking, but the fact that it was virtually risk-free and paid out within a few months made the annualised return pretty mouthwatering.

And we were not the only people thinking so; several merger arb hedge funds have joined the shareholder register. As a reminder, shareholders get 33p in cash (the shares are already ex-dividend for a 0.8p payment) and 0.019 Paypoint shares. This means the price trajectory of the Paypoint shares really matters. With Paypoint 488p to sell, the arb is now down to just 1%. The now biggest Appreciate holder, Samson Rock, appears to be fully hedged. However, Syquant Capital have not fully hedged, and the latest announcements show that as of the 15th of February, they are under-hedged by about 39k Paypoint shares. Last week they were under-hedged by about 52k shares. At this rate, they will fail to get their book square before the deal completes and will have to sell the rest of their Paypoint shares in the market when they get them.

They will no doubt be joined by a lot of smaller Appreciate holders who don’t want the rump of Paypoint shares. We like the idea of owning Paypoint shares long term, not least because they have all that Appreciate customers cash earning increasing interest rate margins. Paypoint shares have to go below 458p to be worth taking 41.7p for Appreciate shares in the market today (excluding costs, time value of money and opportunity cost), although it has been possible to sell at slightly higher prices this week. The real question is if Syquant (or any other arbitrageurs who have failed to get square that we don’t know about) plus all the smaller shareholders selling will take the price below 458p?

UP Global Sourcing (UPGS.L) - Trading Update

UPGS brought us an H1 trading update this week:

Unaudited Group revenues increased 2% to £87.6m (H1 2022: £85.7m).

That sounds terrible and corresponds to something like an 8% real-term drop in sales volume once you account for inflation. And although there was no direct acquisition impact on sales in the period, you would have expected Salter to be delivering more sales as it matures. So what went wrong?

Encouragingly, the level of general retailer overstocking experienced during 2022 which, along with the challenging macroeconomic environment, caused retailer customers to be cautious in the size of their forward orders, is now reducing in the UK and more normal patterns of order placing have recommenced.

This has been flagged up before, but they have much less exposure to the UK and feast-or-famine discounters in particular than they did in the past, so it is disappointing it had such a large impact. Their great hope for future growth is Germany, but there is no mention of them in today's update. Instead, it is online that is really shining:

Online channels were the main driver of this growth, supported by the continued normalisation of global supply chains.

As you may recall, they had previously had to limit supply to this channel to meet commitments to their retailing customers, so some of this is a natural bounceback. However, it is still impressive to grow online when everybody else is struggling. Broker, Equity Development say:

Online was a record 16.4% of sales in FY2022 compared with 15.1% in FY2021 and can be inferred from today’s release to have risen in FY2023 H1.

UPGS also reference the air fryer fad:

In addition, consumer demand for energy efficient and money saving products has remained buoyant across all channels throughout the period.

It was notable at the Spring Fair how few air fryers they were promoting for new orders, so this may be a headwind going forward. They end this update with:

The Board anticipates a full year performance in line with current market expectations.

However, unsurprisingly, the share price was weak on this update. They have a lot of catching up to do to transform 2% in H1 to 6% for the FY. Equity Development calculates that they require 11% sales growth in the seasonally quieter H2 to get there. If they do somehow manage to hit forecasts, then the debt/cash adjusted P/E is around 12, which is toward the upper end of the typical trading range for the company. Mainly because the price was given a boost earlier this year by various tipsters. We see little reason for this enthusiasm given the high chance of a miss for the full year.

Gattaca (GATC.L) - Trading Statement

This struggling recruiter was tipped last week by Simon Thompson in the Investors’ Chronicle, with the price rising 22% in response. This week the tip buyers got the usual lesson in why being the least-informed investor is usually a bad idea when the company issued a trading statement:

Group NFI1 expected to be £22.7m (H1 22: £21.6m), an increase of 5.1% YoY

So NFI is up 5%, slightly behind inflation, but no guidance was given on profit, leaving investors to guess the bottom line. And then there was a further sting in the tail:

Permanent hiring has shown signs of weakness since the turn of the year

Having failed to capitalise on booming STEM markets over the last few years, the outlook is now much weaker for the company. A slow share price reaction on the morning suggests that many had missed that their broker Equity Development were given a fuller picture and said:

Indeed, the company reiterated today that it was well on track to achieve its medium & long term goals

So not on track for its short-term goals then! And indeed, they reveal that this is really a profits warning:

Given the ‘blustery’ economic conditions, we’ve prudently trimmed our FY’23 and FY’24 PBT forecasts to £1.8m (£256k LY) and £4.25m respectively on NFI up 5.3% & 8.9%, alongside adjusting the valuation to 130p/share vs 160p before.

The Equity Development analyst for this company is Paul Hill, so readers may want to apply their own calibration to the word "prudent"!

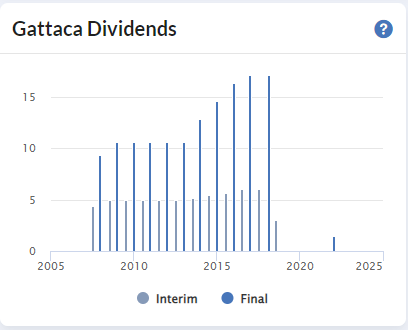

Part of the reason that investors may have missed this profits warning was that net cash was up significantly to £21m, and this compares favourably with a £26m market cap at 80p. However, this is a company that has a very high turnover and hence large working capital swings. Very little, if any, of this cash is likely to be distributable. As the very paltry recent dividend record attests:

Tekmar (TGP.L) - Update on Formal Sale and Strategic Review

Inexplicably, Tekmar shareholders appear to have forgotten that they face a very large dilution sub-10p, and the price had been rising back to 16p. This week, the company returns to remind shareholders that this is actually the best case:

On 17 November 2022, the Company announced that following a review of the proposals received, a preferred partner was granted a period of exclusivity to carry out due diligence and finalise its proposal…This exclusivity period was extended in January 2023.

So, why the delay when placings routinely get sorted in a matter of weeks? We see two possibilities, which are not mutually exclusive:

1) Problems with Tekmar

2) Problems with the institutional investor

The problems with Tekmar have been known about for years: customers are simply not paying for work Tekmar claim to have carried out, suggesting problems with revenue recognition and/or severe contractual issues. They did disclose they were in dispute with (probably) their largest customer. As far as we know, that is ongoing, but subsequent orders from them suggest it isn't fatal to the relationship.

We also haven’t seen results from the company. One possibility is that the results are being delayed until they have funding rather than admit a second consecutive material uncertainty related to going concern. In this case, results may not be announced until funding is in place, but this is a highly risky strategy as it places them at the mercy of this "institutional investor". They are likely to be suspended at the end of this month.

So to summarise this update:

No progress on funding

No progress on results

Re-reiterates that funding, if it proceeds, would be around the 17 November price, i.e. 9.25p.

As Hummingbird Resources showed last week, in weak markets, share prices tend to go below placing prices in the short term, even when the shares are placed with a strategic investor who can’t flip the shares. Presumably, since this provides a psychological anchor.

That’s it for this week. Have a great weekend!