Small Caps Live Weekly Summary

Housebuilders Banks VLX TND LAM

Another difficult week in the markets this week. It is becoming clear that, for many companies, 2021 was an exceptional year driven by post-lockdown demand, and inventory builds. It can be tempting to think that investors are already aware of this mean-reversion and that this is all in the price for many stocks. However, the evidence is that any bad news in this market will be met by persistent selling. Even the usual Twitter “gurus” fail to generate any interest in the stocks they promote.

We have no idea how long these market conditions will last. Although this period is painful for all, this is healthy for the markets long term. Less speculation, and more focus on companies generating strong cash flows in all market conditions and reinvesting those cash flows in future growth or returning them to shareholders, leads to better capital allocation. We believe the ability to buy such companies at modest ratings will very much enhance our future expected returns even if they are doing the opposite for our current returns.

Large Caps Live

This week, WayneJ led a wide-ranging discussion on interest rates, housing, housebuilders, banks and EV charging infrastructure. Check it out on discord to get the full run-down.

Small Caps

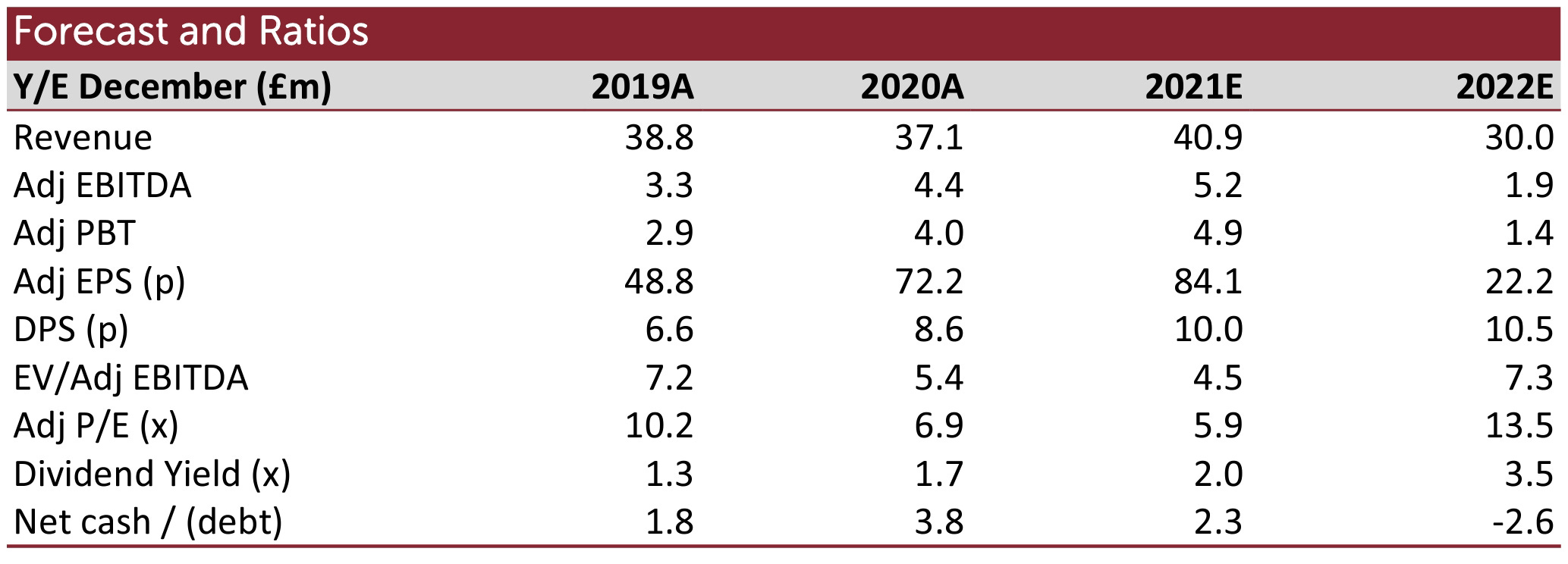

Volex (VLX.L) - Preliminary Results

Let’s start with a couple of red flags. First up, they miss the organic growth rate in the summary:

Group revenue increased by 38.6% to $614.6 million (FY2021: $443.3 million) through strong organic growth and acquisitions

This isn’t ideal for a serial acquirer, but we do find it eventually, way down the statement:

This included organic revenue growth of 19% and the contribution from our FY2022 acquisitions and the remainder of the first 12 months of our FY2021 acquisitions.

19% isn’t actually a bad growth rate, but it should have been in the summary. Secondly, we don't like revenue targets:

Our ambition is to deliver revenue of $1.2 billion by the end of FY2027

Ones that aim to break through the 1bn barrier (in any currency) seem particularly bad since this has caused several companies to come unstuck in the past pursuing revenue growth at the cost of profits and cash flow. It seems this is often more about prestige and justifying high board pay rather than shareholder returns.

We aim to achieve this with underlying operating profit margin in the range of 9-10%

Thirdly, their margin target appears to be a reduction from the previous target of 10% and excludes the historically high exceptional costs that occur most years.

Leo struggled to find their last set of strategic goals from the 5-year plan that they claim to have now met. The remuneration reports suggests these were secret! But Their NOMAD, Singer, has mentioned 10% on several occasions, e.g. December 2021:

Margins have risen strongly over the last 5 years as Volex has been operationally refocused. The pandemic has slowed expected margin progression only modestly, whilst the opportunity for 10% margins by FY2024E remains very much intact.

Again this year there are no exceptional charges. The question is whether this is now the new normal? This is an enormously complex business and made more so by recent acquisitions and some kind of restructuring or switch of investment will inevitably be required at one site or another most years. If they have been treating this as BAU then great. If they have been putting it off then it will catch up with them.

With those caveats excepted, these look a strong set of historical results. The key to future returns will be the outlook:

· The year has started strongly with high levels of customer demand and orders, particularly for more complex products with longer lead times

· Inflationary pressures and variable lead times are expected to continue but are manageable

· Our global footprint is a beneficiary of the recent trend towards "near-shoring" production

· We have an exciting pipeline of acquisition opportunities and financial flexibility

This seems very positive. Note they cite "near-shoring", or as Leo has heard it called recently "friend-shoring". They do indeed have this flexibility to react to and possibly profit from changes in the economics and politics of globalisation but major dislocations would result in exceptional costs.

Cash is down and borrowings are up, as would be expected after making four acquisitions in the last year. But they have quite a lot of debt firepower:

The Group started the period with a $70.0m multi-currency combined revolving overdraft and guarantee facility.

In September 2021 the Group activated the $30.0m accordion feature on the facility. In February 2022 the Group completed a refinancing with a syndicate of five banks, replacing its existing $100 million revolving credit facility with a new $200 million committed facility (the "Facility") together with an additional $100 million uncommitted accordion (the "Accordion").

But now is clearly not the time to leverage up too aggressively and we would expect them to issue part equity as they have in the past to keep good covenant headroom if nothing else.

This was a good set of results and in any normal conditions, we would say a PE of 10 is too cheap. Clearly, that EV growth, in particular, is fantastic and is now at the size where it is very material to total revenue growth. Broker, Singer, says results were ahead of expectations and has modestly increased forecasts. Perhaps the only thing preventing us from buying is the presence of even cheaper-rated stocks in the current market.

Tandem (TND.L) - AGM Statement

A detailed AGM statement from Tandem this week, with some rather scary numbers:

Both national retailer and independent dealer bicycle sales were disappointing during the period to 17 June 2022, with overall Bicycle division turnover 55% behind that of the prior period.

Basically, bikes and garden products have seen very significant mean reversion post-COVID. The rest is hiding up better but didn’t have the covid boom. And overstocking seems to be a major issue:

We have continued to experience customers cancelling and delaying orders, which has meant, in conjunction with completion of back orders, the current order book of £10.0 million is well behind compared to £35.4 million this time last year, which is more in line with levels seen at the same point in 2020 when they were £10.8 million.

The same point in 2020 is just after the first lockdown, so seems a very weak comparator and being below that level does not bode well. And they talk about “promotional activity” which is basically price cuts. Not great on an inflationary environment (although perhaps indicates inflation could be more transitory than we think at the moment?)

At the end, they dangle the carrot of a strong long-term outlook for e-bikes and e-scooters:

The UK government continues to invest in alternative transport infrastructure, but remains behind European counterparts such as Germany, France and Spain. The change in French legislation on e-scooters resulted in an increase in e-scooter unit sales by more than 8 fold between 2017 and 2021, and had a total market value of €458m in 2021, compared to the UK which was estimated to be around £75m in 2021. The Group is already well placed to take advantage of the potentially large forthcoming uptake of e-scooters.

Market data also suggests that the e-bike market is set to grow significantly in the coming years, as consumers better understand the benefits of an electrically assisted bicycle. The UK has already seen a 72% unit growth between 2019 and 2021 to around 160,000 units, but is still well behind Germany where it is around 2 million units. The UK is estimated to be 4 to 5 years behind mainland Europe….

However, saying the UK is 5 years behind mainland Europe perhaps misses that cycling in major European cities is largely safe with good cycling infrastructure, whereas the UK seems to want to naturally cull the cycling population with poorly designed cycling infrastructure and terrible driving attitudes towards cyclists.

In terms of the impact on the bottom line numbers then we have to turn to house broker, Cenkos - at least Tandem now have forecasts in the market.

Cenkos previously had c.56p EPS forecast for FY22 so this has been reduced by over 60% following this week’s update. And down over 70% vs where the EPS forecasts started the year. The forecast is also now for net debt instead of net cash.

With the share price only down 55% this year, this looks like an under-reaction, given the drop in EPS. Of course, at this level, we are starting to see support from the Tangible Book Value. It’s not clear to us that these assets will ever be particularly productive though, a lot depends on them being able to grow the business to fill the new warehouse (and not just with unsold stock!). In the short term, asset value could also be eroded by the need to discount inventory. So it’s not clear to us that they are yet cheap enough to buy as an asset play.

There are no forecasts from Cenkos for 2023. There will be a c£500k cost benefit from them consolidating sites, but it is not clear if overall trading will recover in 2023.

The other factor to consider is if you wanted exposure to the growth trend in e-bikes then the market leader Halfords looks cheaper and more resilient on earnings due to its auto servicing division (although without any tangible asset backing) - surely you’d want a big discount to own Tandem instead?

Lamprell (LAM.L) - Trading & Liquidity Update

Not the market to be issuing an update with the word “liquidity” in. The market has reacted on Friday morning by marked them down a whopping 77%.

They raised $30m from the market last year to fund working capital but were clear that they would need more this year. Perhaps they were hoping to raise at a higher price…a gamble that certainly hasn’t paid off.

One of the major shareholders is looking to make an offer for the company so is clearly not looking to bail out the other shareholders. Hence, the offer RNS contains the following:

The Board is considering the Possible Offer in light of the Group's liquidity position and the Company's funding requirements of $75 million over the next two months. Blofeld's proposal in respect of the Possible Offer is at a very significant discount to the prevailing share price and any acceptable offer would need to include an interim funding solution or bridge financing.

In the current market, Blofeld can name pretty much name their price and we wouldn’t expect it to be much above the 5p per share the market is currently trading at post-fall. The clue was perhaps in the name.

That’s all for this week. Enjoy your weekend!